@Strategy modeling enthusiast | $MSTR shareholder | Options seller | $STRC advocate | #Bitcoin | ex-HPC software developer | Loyal fan of @milkmochabear

Joined January 2020

- Tweets 3,409

- Following 135

- Followers 950

- Likes 12,282

141 Photos and videos

Mocha retweeted

Price to Book (P/B) of any equity trades >1x when the expected Return on Equity (ROE) is greater than the Cost of Equity.

The ROE of Bitcoin Treasury Companies can be greater than $BTC ARR, if the cost of leverage is lower than $BTC ARR. This is how leverage works for purchasing any asset.

GBTC had no ability to take on leverage. It didn't have optionality with its capital structure or operations. Plus, it had a drag from its management fees.

46

21

286

49,278

RT @ColeMacro: No single metric tells a full financial picture. The key is understanding the differences and how to use them.

Strive’s two…

46

Mocha retweeted

BPS measures Bitcoin per common share before senior claims. CEBE BPS measures Bitcoin per common share after senior claims. CEBE is the conservative risk metric. BPS is the common equity growth metric. BTC Yield measures BPS execution.

367

340

3,444

351,650

Jun 13

In this post, Brian illustrates why basic mNAV — what I call mGAV, which is any variant of mNAV where debt and preferreds are not factored in — is a borderline useless metric. Definitely worth a read.

I originally implemented seven variants of mNAV in the Monster Model Framework, including three for mGAV, but I removed them several weeks ago because I couldn't find a situation in which they make sense. As Brian explains, they are always misleading except in the trivial case of a company with no debt or preferred stock.

The four remaining variants are: mEV and three variants of price-to-book (P/B) — one each based on basic, effective, and assumed diluted shares outstanding. I believe these are much closer to how the market actually places a multiple on companies like @Strategy and @Strive.

My preference, if I could only pick one, is diluted P/B, but honestly I'm fine with any variant of P/B. 🍻

$MSTR $ASST #Bitcoin

Jun 13

You simply can't look at mNAV in isolation to judge the health of a Bitcoin Treasury Company. You need to know why the numbers are moving.

The latest smear tactic has been to say "look at activity below 1x basic mNAV, it reveals equity destruction."

The trick relies on pretending that liabilities don't exist.

Market Cap / Total Asset Value, by definition, is not multiple to "net" asset value. It matches the market's estimate of the company's net assets plus or minus a premium against the company's total (not net) assets.

Let's consider a hypothetical. To make the math easy we'll assume the market always values the company at P/B = 1x.

The company starts at $1B market cap with $1B of bitcoin. No debt, no prefs, no liabilities.

P/B = $1B / $1B = 1x

Basic mNAV = $1B / $1B = 1x

Now let's say the company takes on $500M of debt to buy $500M of bitcoin. We'll ignore any interest for the moment and just consider the principal. Bitcoin price remains unchanged for the time being.

P/B = $1B / ($1B $500M - $500M) = 1x

Basic mNAV = $1B / ($1B $500M) = 0.67x

Now what if the company takes on a further $500M of debt to buy a further $500M of bitcoin. Bitcoin price still remaining unchanged.

P/B = $1B / ($1B $1B - $1B) = 1x

Basic mNAV = $1B / ($1B $1B) = 0.5x

Price to book remains unchanged in all 3 cases because the new bitcoin purchases net out against the debt incurred.

Basic mNAV alarmists would tell you that "discounted" mNAV signals something is deeply wrong with the stock, when in reality no discounting took place and P/B is simply taking into account liabilities as it should. In this case, basic mNAV below 1x simply reflects the company's leverage.

Now, what if, continuing on from the last scenario, the stock started trading at $1.5B / $1B = 1.5x P/B?

Basic mNAV = $1.5B / $2B = 0.75x

Are shares valued less than *net* bitcoin exposure here? Obviously not. P/B is 1.5x, shares are at a 50% premium to net bitcoin exposure.

mNAV in isolation, no matter the formulation, doesn't tell the whole story. You have to look deeper.

2

8

1,506

Jun 12

diglloyd gets it.

The key — and mostly semantic — distinction that some Bitcoiners cling to is that there exists a time horizon over which @Strategy was a net seller of #BTC, even if it was only a few hours or days.

The pragmatist majority understands that for a carry trade as epic as the one that Saylor and Phong are guiding us through, time horizons shorter than, say, 2-3 weeks are functionally instantaneous.

If we can agree that we are buying #Bitcoin as an investment priced in fiat, then never selling even a tiny amount of your BTC only matters at those moments in history when you will never see those prices again, which are rare.

In most real-world cases, I'll take the certain tax-loss harvesting benefit over the unlikely possibility that those prices are never revisited.

$MSTR $STRC

If I could sell my Bitcoin, take the capital loss, and then rebuy 10% lower (and more of it), I would NOT consider myself to have violated the "never sell your Bitcoin".

It's no different for swapping one set of $100 bills in my wallet for another set, plus some $20's.

1

7

360

Mocha retweeted

You don’t see it. He is Machiavelli and Sun Tzu rolled into one. He is involved in a financial war with the largest criminals on the planet: the Fiat Lords. You think he isn’t going to fight somewhat dirty? You think his strategy (pun intended) isn’t going to evolve? He wants to win. And I believe for the right reasons. I believe his motives are pure and I trust him. A sound money world would massively benefit mankind. Can you nit pick some moves. Sure. But don’t lose sight of the big picture.@saylor @CJ_Bitcoin

44

32

446

25,515

Jun 11

My favorite part of my hours-long co-planning sessions with @claudeai: when I finally get to paste a 176-line prompt into Claude Code and watch Opus do in 15 glorious minutes what would have taken me 6-8 weeks to do by hand.

That's a ~200× boost for the least-fulfilling and most tedious, error-prone part of the project.

So I get most of my time back, and I get to realize my project faster.

These tools are immensely powerful. ⚡️

4

1

5

323

Jun 10

Bobby is among a handful of people I have to thank for being where I am today.

Please consider giving him a follow.

Jun 10

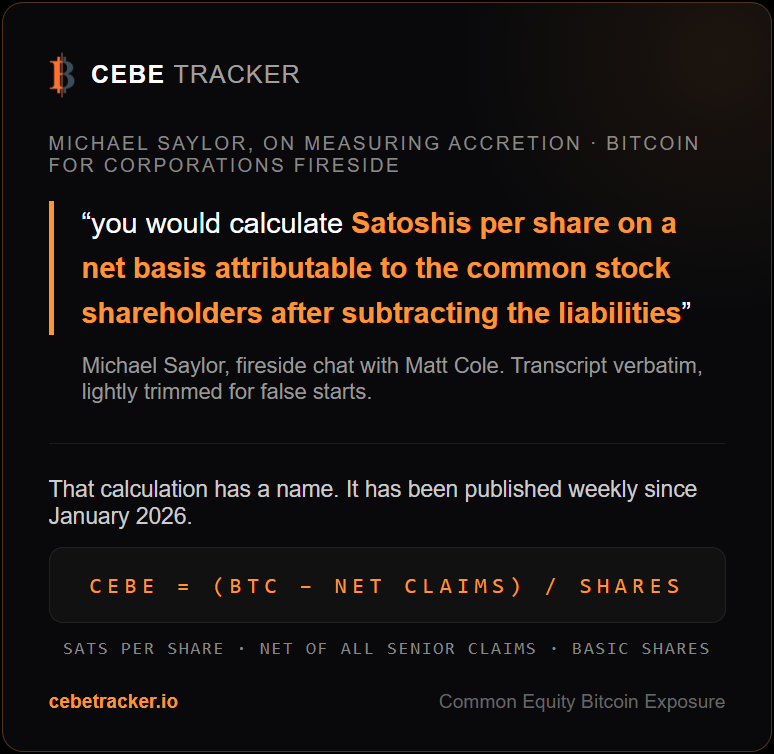

Saylor was asked how to measure whether a deal is accretive. His answer is to calculate satoshis per share, net basis, attributable to common shareholders, after subtracting the liabilities.

That calculation has had a name since January and cebetracker.io publishes it weekly

In the same conversation 'for you to understand whether the company's accreting or diluting, you have to understand all of the tangible assets, the cash, all of the liabilities.'

All of the liabilities, net of cash. That is the entire CEBE methodology in one sentence

He also pushed back on netting preferred, calling it mezzanine capital rather than a balance sheet liability. Fair framing from the issuer's seat. From the common shareholder's seat, the liquidation preference stands ahead of you in every outcome that matters, whatever the balance sheet calls it. CEBE is measured from the common seat. Both views are correct. They answer different question

Another interesting line surfaced, 'there's still a lot of room for debate about what is the right way to value a hybrid credit instrument like STRC.'

Agreed. More on that soon

1

1

8

955

Jun 10

Something I struggle with in community participation is that contributions are not always visible.

Similarly, in relationships, expressions of support are not always public.

To everyone who takes the time to interact with me constructively, I want you to know that I appreciate you.

This holds true regardless of how often I post.

And it is especially true regardless of how often I like or interact with your content.

Lately I have felt that while I adore the Bitcoin community, the X algorithm is not entirely aligned with how I want to contribute to that community.

It's a subtle reminder that my goal is not to live on the app.

My goal is to build.

And I suppose, now that I think about it, most of one's time spent building is done quietly, out of public view.

As I merrily work on the Monster Model Framework website — neck-deep in formulas, CSS, JSON, and TypeScript — please know that I never take for granted the people who show up to engage with me positively and in good faith.

In fact, you are why I keep coming back to X.

This project started off as an ugly spreadsheet. But you helped me understand that it could be something more — something beautiful, powerful, and truly special.

And my hope is that one day, after I'm able to share the final product, it will make more sense.

Thank you sincerely for your support. 🧡

Especially the support that I don't always see. ✨

$MSTR $STRC #Bitcoin

5

2

18

559

Mocha retweeted

Jun 10

My beliefs: Retweets are notifications, not endorsements. Constructive dialogue leads to better outcomes. Bitcoin is hope and economic empowerment for everyone. Every good-faith effort to strengthen the network should be welcomed.

1,126

1,170

10,977

646,431

Jun 8

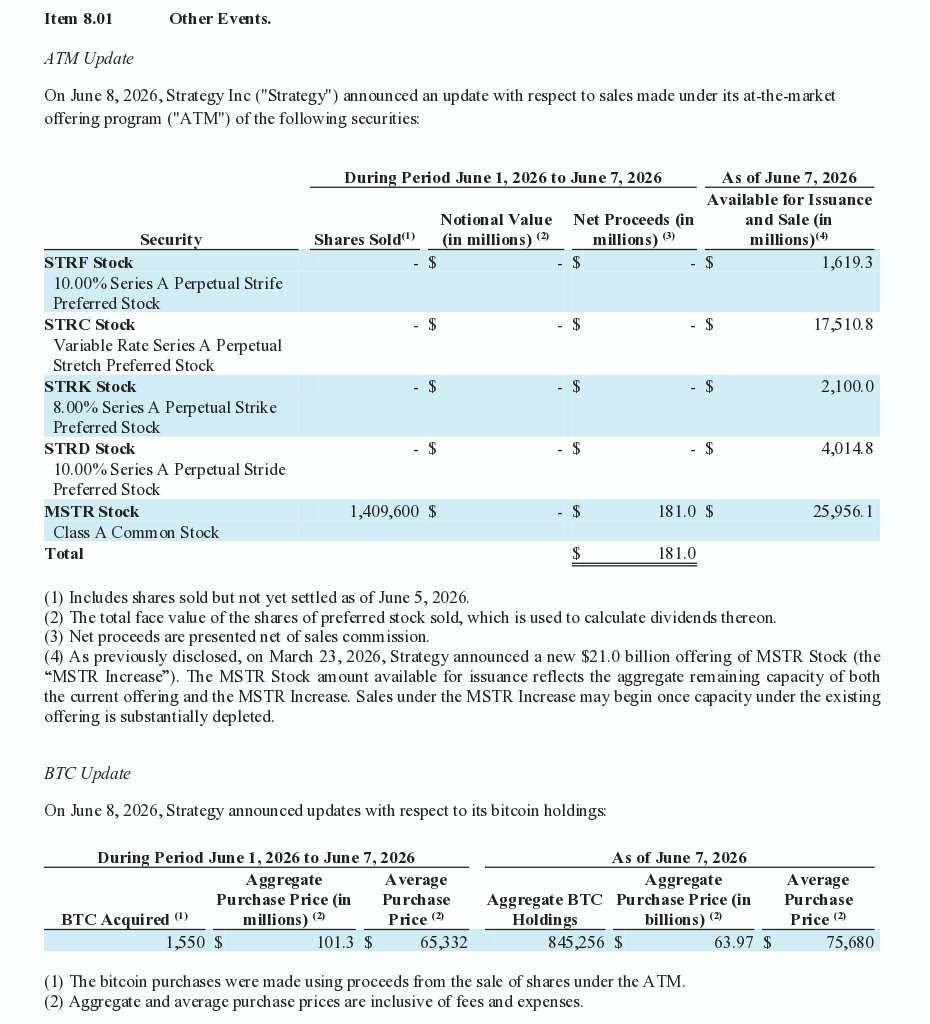

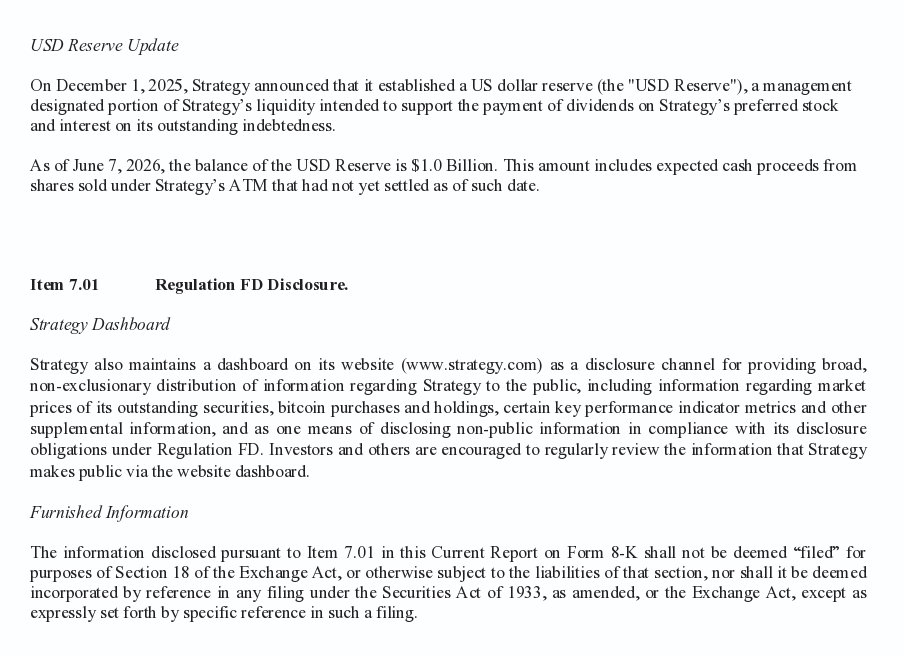

I noticed a small discrepancy in the math behind today's 8-K.

The filing reports that @Strategy raised $181 million in net proceeds from selling $MSTR.

It also reports the purchase of 1,550 #Bitcoin for $101.3 million at an average purchase price of $65,332.

Finally, it reports that the USD Reserve had increased to $1.0 billion, implying a $100 million increase from last week's reported balance.

The 8-K does not appear to report any other source of capital raised for the reported period.

But if we start with $181 million and subtract the $101.3 million in funds spent on the Bitcoin purchase, we are left with only $79.7 million to add to the USD Reserve.

Alternatively, if we start with the $181 million and subtract out the $100 million added to the USD Reserve, we are left with only $81 million for the Bitcoin purchase. At an average price of $65,332, that would purchase only about 1,240 #BTC. Or, if the full 1,550 BTC were purchased with only $81 million, it would imply an average purchase price of about $52,258.

The 8-K contains a line that reads: "As of June 7, 2026, the balance of the USD Reserve is $1.0 Billion. This amount includes expected cash proceeds from shares sold under Strategy’s ATM that had not yet settled as of such date."

At first I thought this might help explain the $21 million discrepancy. But that only works if the $181 million figure excludes some unsettled ATM sales — and my interpretation is that it does not. The 8-K appears to be reporting all shares sold during the reported period, including those whose sales had not yet settled. So I don't think this helps explain the delta.

The cleanest explanation may simply be that the additional ~$21 million came from existing liquidity rather than newly raised capital, since the USD Reserve is described as "a management-designated portion of Strategy's liquidity." But if so, the filing does not make that bridge explicit.

13

2

34

10,218

Jun 8

I haven't given much thought to why @Strategy chose to sell 32 #Bitcoin. (My previous post [1] about base-21 math was intended more as a joke.)

Instead, I've been focusing on the market's reaction. Like many of you, I've been surprised less by the increase in bearish sentiment than the speed and intensity of the turn.

Some of this change in sentiment is undoubtedly macro in origin — the market seems to be pricing in a tighter monetary policy from the Federal Reserve.

Some of the bearishness comes from a few people whose loyalty to Strategy was, at least for now, genuinely broken by their willingness to sell even trivial amounts of #BTC.

Many others have disliked Strategy or Saylor long before the 32 BTC left Strategy's wallets; their noise was merely amplified by the environment or the algorithm (or both).

But suppose the market really did react negatively to Strategy selling 32 BTC — and that the reaction could be triggered again.

That creates an asymmetric opportunity.

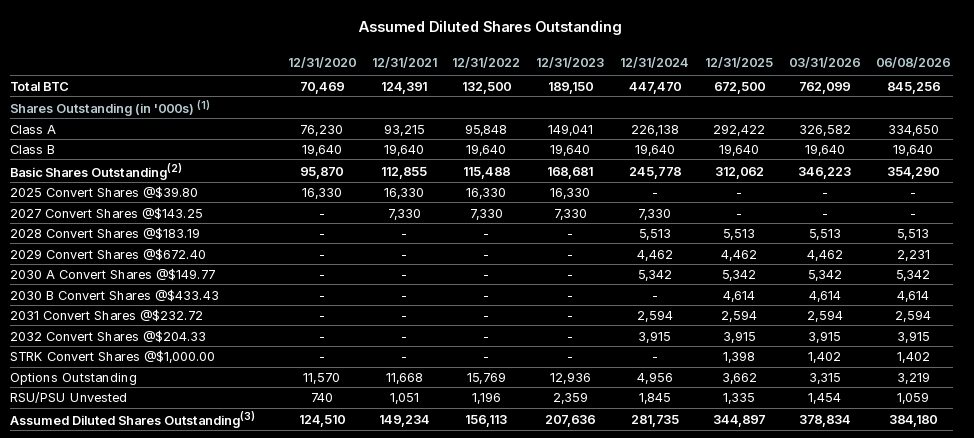

Last week, Strategy sold 32 Bitcoin at an average price of $77,135. If Bitcoin trades around $63,000, the same proceeds could buy roughly 39 BTC — meaning the company could replace the 32 BTC it sold and add about 7 more without raising any new capital.**

In that case, the market's bearish reaction becomes economically advantageous. A small sale can generate cash, potentially bank capital losses towards future gains, and create a better entry for BTC that they were always going to repurchase.

There's a famous clip of Saylor saying "Bitcoin could go to a dollar — a dollar per Bitcoin — we're not getting liquidated, we're just gonna buy all the Bitcoin if it goes to a dollar per Bitcoin and then it's going to go back up again." [2]

I don't think Bitcoin will ever return to $1, but the quote illustrates that, counter to what many of its detractors seem to think, a deep bear market increases Strategy's power over its own destiny in key ways.

At some point, the signal is no longer the initial BTC sale. The signal becomes the increasing net accumulation at steeply discounted prices.

That's when the market stops reacting to the sale itself and starts watching the net result. Did Strategy sell BTC permanently, or did it sell 32 and later buy 39? Did it reduce exposure, or did it increase long-term BTC per share?

This is the behavioral transition bears are missing.

Over time, the market will not only become inured to these sales but will also begin to front-run the eventual repurchases, because they will see Strategy for what they have been all along — a net buyer of a perfectly scarce commodity.

🟠

---

** In practice, their access to $MSTR and $STRC capital markets will always afford them the opportunity to raise cash when needed. Today's 8-K discloses that Strategy purchased 1,550 Bitcoin and added $100 million to their USD reserve after selling $181 million in common equity, even as Bitcoin trades near its 200-week moving average.

[1] x.com/monster_models/status/…

[2] x.com/saylordocs/status/2023…

Feb 17

MICHAEL SAYLOR:

“A lot of people don’t really think — they’re like oh my god MicroStrategy’s going to get liquidated. Well dude no, Bitcoin could go to $1, we’re not getting liquidated, we’re just gonna buy all the Bitcoin.”

Legend!

4

1

10

950

Mocha retweeted

Jun 7

I'm imagining the bears who think that Bitcoin is so weak that if you buy 4% of it and talk a lot, you can destroy the whole network.

It's not even a person, but a group. Bought 4%.

Like, somehow the key weakness of Bitcoin is that if someone buys 4% of it, everything fails.

357

365

5,397

450,126

Mocha retweeted

Saylor can stay solvent longer than the news cycle can stay bearish.

22

46

832

31,895

While markets focus on short-term portfolio adjustments, leaders in the U.S. government are laying the foundation for long-term leadership in Bitcoin and digital assets.

Jun 4

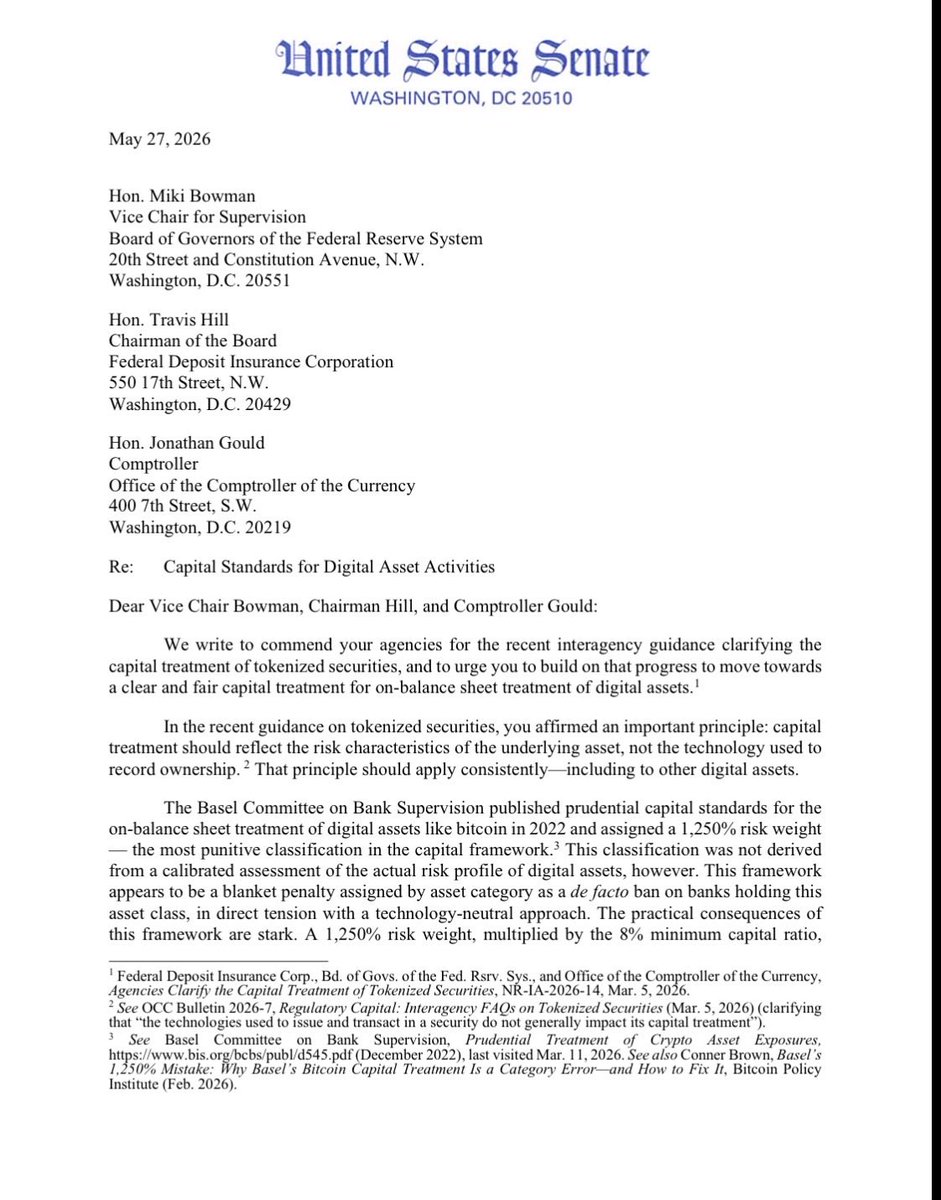

NEW: Sen. Sullivan and Sen. Lummis lead letter to the Fed, FDIC and OCC, calling for revaluation of Basel’s risk weighting for Bitcoin and digital assets.

“A 1,250% risk weight bypasses those calibrated frameworks entirely, applying a blunt penalty …to a transparent, globally traded asset with deep derivatives markets, continuous liquidity, and cryptographic auditability.”

This is a strong signal from Washington that legislators are looking closely at this issue as work on market structure continues. The letter has 6 signatories and 3 are on the Banking Committee.

It’s also great to see BPI’s brief on this topic cited in the third footnote! 😉

We’ll keep you posted on further updates.

52

166

1,423

52,293

Jun 5

I saw my website for the first time today. ✨

The site is imperfect and very incomplete — and yet, somehow, still gorgeous. It was an emotional experience.

Aside from scaffolding Next.js and Tailwind CSS, Claude has helped me write a detailed, 2,500-line SPEC.md file, multiple Python scripts for data processing, and a half-dozen JSON files ready to be fed into the TypeScript engine I'm about to build.

As a former HPC software engineer, that is the step I've been most looking forward to.

And because I've laid most of the foundation, I expect my progress to accelerate going forward.

This would not have been possible without @claudeai and Claude Code.

But AI is just half of the input.

To everyone who has supported me over the last two months in uniquely human ways — thank you. I wouldn't be here without you.

I wouldn't have even tried. 🧡

Jun 4

Our internal data shows Claude is accelerating AI development—a possible path to recursive self-improvement, or AI autonomously building a more capable successor.

It’s happening faster than we thought, and the implications deserve greater attention. anthropic.com/institute/recu…

1

5

946

Mocha retweeted

Jun 4

Unpopular opinion:

Bitcoin's inclusion in the financial system will spur its adoption as more people (and AI agents) realize the value of a provably scarce digital asset to preserve wealth in a world with accelerating monetary debasement.

Maxis that ignore the reality that most people prioritize safety and ease of investing over self sovereignty and censorship resistance ignore this.

Every time Bitcoin, which is still trades like an OPTION on its own adoption, underperforms, our timeline is filled by pundits that ignore all metrics except price.

Sometimes it is best to zoom out...

x.com/dmweisberger/status/20…

22

10

134

5,405

Jun 4

So far, I'm liking the strong bounce off of the 200-week SMA.

But #Bitcoin is going to do Bitcoin things.

Buy, sell, or get out of the way. 🚀

Jun 4

As #Bitcoin rushes down towards its 200-week moving average, I can't help but notice that volume is less than half what it was during the February 5th panic session.

This could be interpreted as bullish or bearish in the short term.

Either way, I'm in $MSTR for the long term. 🟠

1

1

14

822