Joined November 2019

- Tweets 2,870

- Following 620

- Followers 43,840

- Likes 3,434

999 Photos and videos

Jun 11

All eyes on tomorrow now 👀

Seat belt on🛟

Jun 11

🚨 SOMETHING VERY STRANGE IS HAPPENING

SpaceX will go public tomorrow at a $1.75T valuation.

The biggest IPO in market history.

And Wall Street just changed the rules right before it happens.

I've been trading for more than 15 years and have never seen them rewrite the rules so urgently:

IPO access now lowered from $500,000 to $2,000 (-99.6% cut).

That means millions of investors can suddenly enter a deal and buy shares tomorrow.

One day before the most expensive IPO in history.

And suddenly...

SpaceX reserved up to 30% of the deal for regular investors.

Three times the normal share.

Why?

Because retail investors need to buy what insiders sell.

And here is the part most people are missing:

SpaceX does not just create demand for SpaceX.

It pulls liquidity out of everything else:

- Retail sells stocks to chase the IPO.

- Funds sell stocks to prepare for forced buying.

- Brokers open access to generate demand.

- Everyone needs cash at the same time.

That is why the market is selling now.

First, insiders create the hype.

Then brokers open the gates.

Then regular investors rush in.

And by the time the crowd realizes what happened, the exit door is already closed.

We’ve seen this before.

2000:

Dotcom IPOs became the symbol of the bubble.

Then Nasdaq collapsed 80%.

2021:

SPACs, Coinbase, Robinhood, Rivian.

Retail thought they were buying the future.

They were buying the exit.

Now the same playbook is back.

Only this time, it is much bigger.

When Wall Street cuts the entry ticket from $500K to $2K right before a $1.75T IPO, they are not giving retail a gift.

They are creating buyers.

Remember:

Insiders need liquidity.

Funds need allocation.

The market needs a dream.

And Wall Street needs someone to hold the bag.

That is what tomorrow is really about.

Reminder: I’ve called all the market tops and bottoms for the last 15 years, including the Bitcoin bottom at $16,000 and the top at $126,000.

The next call will be even more important.

When I exit the markets completely, I’ll post it here publicly like I always do.

Turn notifications on. If you’re not following yet, you’ll understand why that was a mistake later.

2

1

5

330

Jun 10

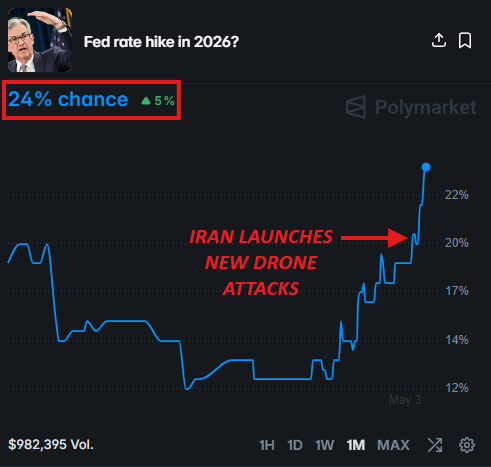

May CPI: 4.2%. 🔥

Highest since April 2023.

Core CPI: 2.9% — highest since Sept 2025.

Inflation is back above 4%. More than DOUBLE the Fed's target.

The consensus a year ago: "3 cuts in 2026."

The consensus today: rate HIKES on the table.

The Fed has no clean option:

→ Cut → inflation rips

→ Hold → yields rip

→ Hike → something breaks

Cash bleeds 4% per year. By design.

The pivot is dead. The squeeze is real.

Own assets or be left behind 👇

mux.network

1

168

Jun 9

🫡🫡

Jun 9

JUST IN: 🇺🇸 Top crypto companies send joint letter urging Congress to include legal protections for developers in crypto Clarity Act.

• a16z

• Aave

• 1inch

• Block

• BitGo

• Aptos

• Zcash

• Solana

• Galaxy

• Ledger

• Kraken

• Uniswap

• Coinbase

• Hyperliquid

• Many others

1

4

278

Jun 5

Counterintuitive truth: 🔄

The more BTC Saylor sold this week, the harder BTC bounces.

The scenarios:

🔴 Sold $0 → disaster

🟡 Sold $1B → partial fix, lower prices

🟢 Sold $2B → flywheel restart, bounce setup

Why?

Strategy's USD runway is ~6 months. A $2B sale extends it to ~20 months. That's the level where STRC trades back to par.

STRC at par = more issuance = more BTC buying power.

The "sell to buy" inflection.

The 32 BTC test wasn't random. It was a signal.

Monday's tape decides the next leg.

Trade it on MUX 👇

mux.network

Jun 5

Near-term BTC price action is going to be heavily dependent on one thing:

Did Saylor sell enough BTC this past week?

If he sold zero, that’d be a massive mistake on his end and we’re probably cooked.

If he sold $1B of BTC, that helps, but realistically I don’t think it’s enough and we probably continue lower.

If he sold at least $2B, that’s where it gets interesting and sets up a bounce.

The more he sold, the harder we bounce.

My base case is that he sold at least $2B. I also think there’s a decent chance BTC bottoms into Monday if the market starts pricing in that he sold some.

Rationale:

Selling none is my lowest probability scenario. He needs the money.

He already did that weird 32 BTC “test” sale and I have a hard time understanding the purpose of it. If he was planning on selling more, all the test did was give him worse execution. If he wasn't planning on selling more, then he nuked the market for no reason. The latter seems completely ridiculous, so my guess is it was indeed a test and he was planning on selling more.

A tiny sale ($500m) is the worst of both worlds. It damages the “never sell” narrative without solving the liquidity problem. If you’re going to sell, sell enough to matter.

That’s the key here.

A material sale does two things at once. It adds real cash runway, but it also sends an important signal to STRC buyers: he is willing to sell meaningful amounts of BTC to keep funding the dividend.

That signal matters a lot.

Strategy has roughly $871M left in its USD reserve. Against the current preferred debt cash burden, that’s only about 6 months of runway.

If he sold $1B, that takes runway from ~6 months to ~13 months. Helpful, but probably not enough. 13 months is enough to reduce near-term stress, but not enough to make STRC feel like a self-sustaining issuance product again. STRC buyers are still underwriting a shrinking cash cushion and hoping the market rallies materially within that window. I think it becomes very hard for STRC to get back to 100 in that scenario.

If he sold $2B, that takes the reserve to ~$2.9B and extends runway to roughly 20 months. That is a very different setup. At ~20 months of coverage, blow-up risk gets pushed much further out, STRC buyers can believe the dividend is properly covered by cash on hand, and the product has a real chance of trading back to 100.

It also changes how STRC buyers think about the balance sheet. They’re not just relying on new issuance to get paid. They’re backed by a massive BTC treasury that Saylor has now shown he is willing to selectively monetize to support the credit stack.

Once STRC is back at 100, the flywheel can restart.

This is the “sell to buy” point.

A large BTC sale does not just create cash runway. It can increase his ability to issue STRC, which then gives him the ability to buy more BTC than he sold.

So the hierarchy is simple:

Selling zero is the disaster scenario.

Selling too little helps, but probably does not fix the flywheel.

Selling enough to matter is what gives STRC a path back to 100 and gives BTC a reason to bounce.

3

1

11

392

Jun 4

Saylor sold. 🚨

For the first time since 2022, Strategy (formerly MicroStrategy) sold Bitcoin.

32 BTC. $2.5M. Avg $77,135/coin.

The size is irrelevant. The symbolism is everything.

The "never sell" era is officially over.

The data behind the decision:

📉 Q1 2026 net loss: $12.54 BILLION

💸 Annual preferred dividend obligations: $1.5B

🔴 STRC dividend ratcheted to 11.25%

🏦 Long-term debt: ~$8.2B

📊 MSTR stock: down from $457 to $125 (52-wk)

This isn't an ideological retreat. It's a balance sheet equation.

2

4

853

Jun 4

2/

The reflexivity trap:

→ BTC drops → Mark-to-market losses widen

→ Preferred stock pressures mount

→ Sell BTC to fund dividends

→ Market reads weakness → BTC drops more

This is what happens when treasury strategy meets financial gravity.

The lesson for traders:

Even the largest corporate BTC holder can be forced into selling. "Diamond hands" works until the cash flow math doesn't.

Volatility creates winners and losers. The flexible ones win.

Trade both sides on MUX 👇

100x leverage | 0 Price Impact on BTC & ETH

mux.network

4

366

Jun 3

The US stock market has a new owner. 🌍

→ Foreigners: $20T (19% of all US equities) — TRIPLED since 2000

→ Passive funds: $17T (15%) — TRIPLED since 2008

→ Active funds: $11T (10%) — HALVED since 2008

~34% of US stocks now owned by foreigners passive funds.

Stock pickers are dying. Index buyers are the market.

What this means:

→ Mega-caps get richer mechanically

→ Dollar moves matter more than ever

→ Less fundamental price discovery

→ More violent unwinds when flows reverse

The market is mechanical now. Trade like it 👇

mux.network

3

4

372

Jun 1

Call option volume is going PARABOLIC. 🚀

The data:

📊 Calls = 70% of total options volume

→ Highest in 4 years

→ 25 points since early April (largest 2-month spike on record)

→ Previous peak: 68% (late 2025)

→ 2-year average: 55%

📊 S&P 500 call notional / market cap: 4.1x

→ New all-time record

→ Doubled in 2 months

Translation: traders are betting on upside at the most aggressive pace in 4 years.

The FOMO machine is running hot.

3

1

6

420

Jun 1

2/

What this tells you:

✅ Bullish appetite is real — capital is deploying, not hedging

⚠️ Extreme positioning can extend rallies further than anyone expects

⚠️ It can also create violent unwinds when sentiment flips

This isn't a top signal yet. It's a tension signal.

When positioning gets this lopsided, volatility on BOTH sides explodes.

Directional bets get punished. Flexible traders print.

Long the squeeze. Short the unwind. Trade both 👇

100x leverage | 0 price impact on BTC & ETH

mux.network

2

296

May 29

A huge step!

May 29

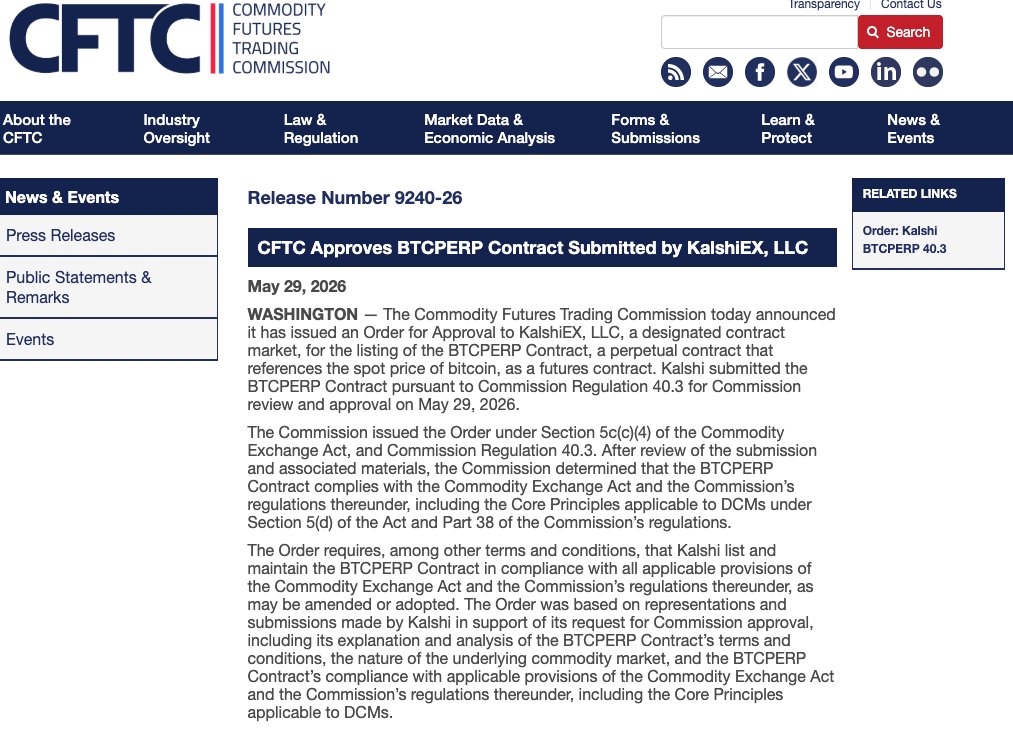

🇺🇸 CFTC Approves First US-Regulated Bitcoin Perpetual Futures

👉 The agency approved @Kalshi 's BTCPERP contract, the first bitcoin perpetual on a registered U.S. exchange.

👉 In a separate action, it cleared @coinbase to route customers to its offshore Deribit affiliate.

🧠 Together, the moves open an onshore path for a product long pushed abroad and raise the competitive stakes for dominant venues such as @HyperliquidX.

Read more here:

thedefiant.io/news/regulatio…

1

3

276

May 27

Semis are now 18% of the entire S&P 500. 🔥

Record concentration. More than TRIPLE the 2022 low.

$SOX since start of 2025: 159%

Mag 7 over the same window: 30%

The gap is the widest since mid-2020.

For context: at the dot-com peak, Tech Hardware topped at 26%. We're at 18% — in ONE sub-industry.

This run is unlike anything in market history.

Most beautiful trade in the market… until the rotation comes.

Long the trend. Short the unwind. Trade both.

mux.network

3

1

7

268

May 26

S&P 500 just hit a new all-time high: 7,539.09. 🔥

On track for its first 9-week winning streak since 2023.

Last week alone: $1 TRILLION added to market cap.

The fuel? Q1 earnings came in 27.7% YoY — the strongest print since 2021.

This is the rally bears keep saying can't last… but it does.

4

3

343

May 26

2/

→ Every dip gets bought

→ Red opens close green

→ Overbought calls get steamrolled by earnings beats

Yes, RSI is hot. Yes, some indicators flash overbought.

But "overbought" only matters if there's a catalyst to break the trend.

Right now? There isn't one.

1

3

224

May 26

3/

✅ Earnings accelerating

✅ AI capex climbing

✅ Liquidity stable

✅ Fed not tightening

For this streak to end, something real has to crack:

→ A mega-cap earnings miss

→ A Fed surprise

→ Genuine doubt in the AI spend story

None of that is here yet.

The path of least resistance is up and to the right.

Trade the trend, not the prediction 👇

100x leverage | 0 price impact on BTC & ETH

mux.network

2

196

May 23

Recession prediction is lower?

👀

2

4

822

May 20

🚨 The Fed just admitted it.

Newly released minutes: the MAJORITY of officials said rate HIKES may be needed if inflation persists.

Not cuts. HIKES.

From the Fed itself.

The pivot narrative isn't dying anymore. It's buried.

12 months ago: markets pricing 3 cuts.

Months ago: zero cuts became the base case.

Today: hikes are officially on the table.

The entire macro playbook just got rewritten.

3

4

473

May 20

2/

What this means:

→ Cash bleeds harder

→ Duration trades get punished

→ Real yields stay elevated

→ Scarce assets win

When the Fed and the market finally agree the next move is up — the regime has changed.

Position for the new reality 👇

100x leverage | 0% price impact on BTC & ETH

mux.network

2

171

May 19

🚨 Japan's 10Y yield just broke above 2.80%.

For the first time in HISTORY.

Look at this chart. 📈

A decade of zero (and sub-zero) yields. Now a vertical breakout.

35% in months. Years of suppression unwinding in real time.

2

5

420

May 19

2/

Why this matters globally:

Japan has been the world's largest exporter of cheap capital for 30 years. The yen carry trade funded everything — US tech, EM debt, crypto leverage, real estate.

When Japanese yields rip higher:

→ Capital repatriates back to Japan

→ The carry trade unwinds

→ Global liquidity tightens

→ Risk assets feel the squeeze

This isn't a Japan story. It's a global liquidity story.

The BOJ has lost control of the long end. Same trap the Fed is in.

When the world's biggest source of cheap money disappears — everything reprices.

Volatility is here. Trade it on both sides 👇

100x leverage | 0% price impact on BTC & ETH

mux.network

1

192