Sharing the best low risk asymmetric opportunities and earnings trades based on information arbitrage research!

Joined June 2016

- Tweets 3,790

- Following 100

- Followers 3,050

- Likes 13,935

368 Photos and videos

Pinned Tweet

Apr 14

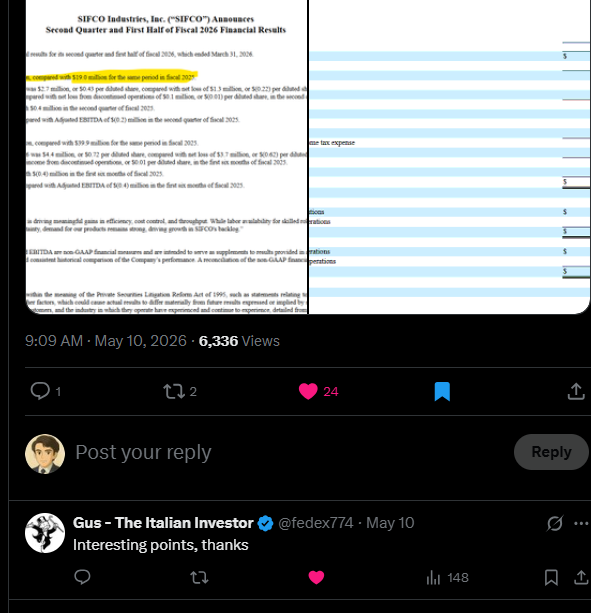

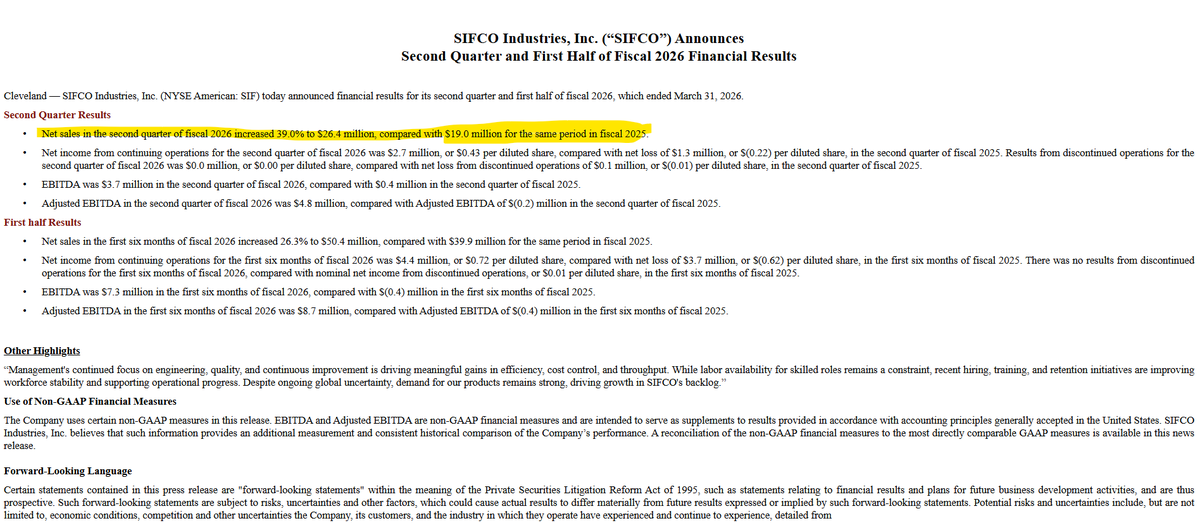

$SIF appears to be offering a massive info arb right now. the more I research this, the more excited I get. Top-line revenue numbers appear to be optically compressed too with some customers now starting to supply their own raw materials. The value of these materials is being completely excluded from the reported net sales in Q1, something that was not present in their earlier annual filings.

While this depresses headline revenue, it simultaneously reduces COGS, meaning the impact on gross profit is entirely neutral. If SIFCO had procured these materials themselves, their reported top-line for the quarter would have been noticeably higher. The quality of these earnings is vastly superior to what the market is currently pricing in.

Furthermore, management explicitly noted that their recent margin surge is being driven by a strategic shift in sales mix and the exit of lower-margin business. As this transition continues, don't be surprised to see SIFCO's numbers continue to inflect with structurally higher margins as Mr. Market finally catches up to the story.

Apr 13

Looking deep into $SIF (SIFCO Industries). It looks incredibly enticing optically with a highly relevant thematic tailwind and a great setup! Well positioned for the aerospace and defense recovery, driven by surging Boeing 737 MAX/787 production and record, stable F-35 contracts from Lockheed. The chart looks great with a low Float and Peter Abrahmson acquiring 6.4% of the float. The backlog is expanding rapidly and jumped $20 million from $119.2M at the end of Q4 2025 to $139.5M by Q1 2026.

Important to note that the earnings quality is high but is currently being masked by LIFO accounting; if FIFO had been used, inventory values would have been $11.1 million higher in Q1 2026, meaning the company's true earnings power is significantly depressed on paper.

Valuation appears cheap too with Enterprise Value below $100M. Given its recent return to profitability and a Q1 sales run-rate pacing near $96M annualized.

Could do really well here as throughput and margins continue to inflect!

7

7,316

Nitin Gupta retweeted

May 30

This guy called this when sentiment was terrible.

$DUOT is now 71% in just 10 days.

Conviction > emotion.

substack.com/@alphametrics1/…

2

6

691

May 29

$WATT CEO/CFO (a lot can be said about that) bought 1,867 shares today at $26.47. This was a widely followed name on here in Q1. Given the market backdrop, this could get interesting.

7

1,233

May 28

$DUOT receives $50.4M from the sale of new APR Energy. Gives them good additional capital runway to execute. Pretty much the only pure-play modular data center company on the market.

May 19

The setup for $DUOT looks good from a risk/reward prespective as several massive catalysts start to converge. The biggest immediate one is the recent FTC filing confirming Elon Musk is acquiring the parent company of APR Energy. Since DUOS holds a 5% equity stake in that entity, this buyout could act as a massive value unlock driver.

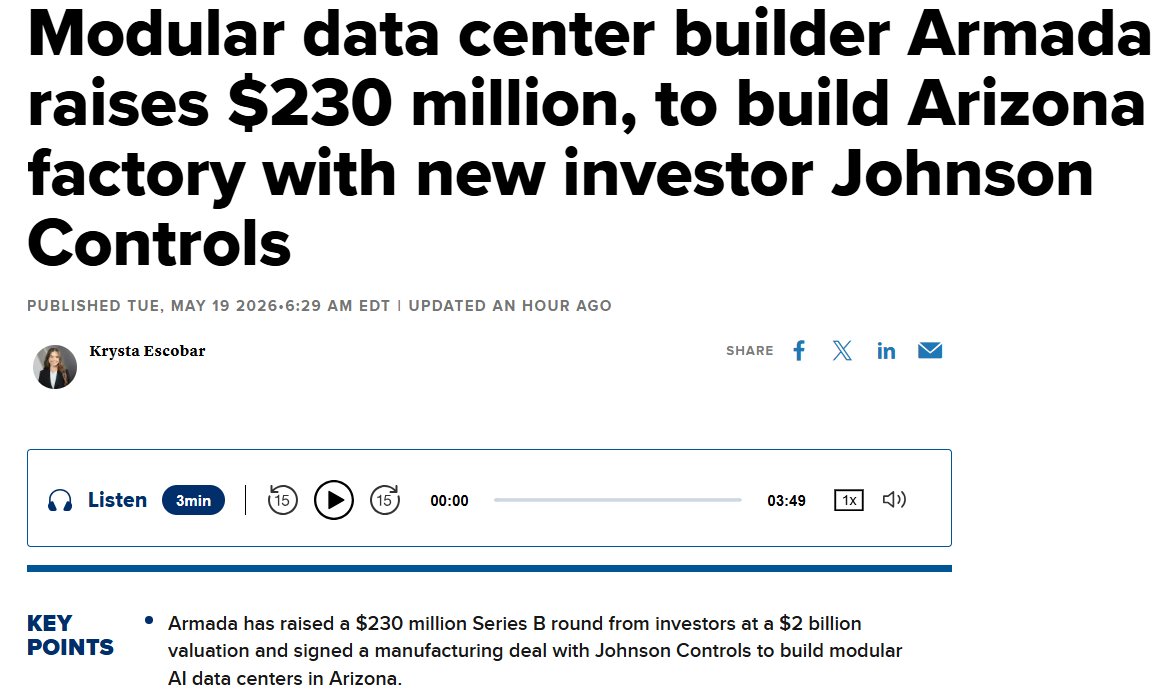

Beyond the APR stake, the operational side is rapidly derisking as well. They have a $176 million contract locked in with Founders Fund-backed Hydra Host, and the $15 million prepayment is already sitting on the balance sheet. The management noted that this relationship is increasingly getting stronger. When you pair that with the news this morning that Armada just raised capital at a $2 billion valuation, the space is starting to get some eyeballs.

The stock is still highly speculative but has a compelling multi-thematic exposure across GPUaaS and Edge AI with the incredibly strategic asset of secured power in Tier 3 and 4 markets. The CEO's track record is strong and he also noted having open conversations with hyperscalers for a potential strategic investment, the stock could catch a bid.

3

12

2,499

May 27

$ALAB talking about CXL in their TD Cowen presentation today. It’s clear everyone is increasingly looking to get the most from every penny spent on memory. CXL was part of conversations in 2025 but didn’t generate material revenue last year, though that is clearly changing. $PENG remains the absolute best way to play this theme.

2

2

21

2,912

Nitin Gupta retweeted

May 18

$SHLS is also looking very good too. BESS optionality, cheap valuation, and with the factory relocation done, subsequent quarters should look better.

1

1

12

1,518

May 26

Looks like FinX is finally discovering $DUOT. Up 70% in a week!

May 19

The setup for $DUOT looks good from a risk/reward prespective as several massive catalysts start to converge. The biggest immediate one is the recent FTC filing confirming Elon Musk is acquiring the parent company of APR Energy. Since DUOS holds a 5% equity stake in that entity, this buyout could act as a massive value unlock driver.

Beyond the APR stake, the operational side is rapidly derisking as well. They have a $176 million contract locked in with Founders Fund-backed Hydra Host, and the $15 million prepayment is already sitting on the balance sheet. The management noted that this relationship is increasingly getting stronger. When you pair that with the news this morning that Armada just raised capital at a $2 billion valuation, the space is starting to get some eyeballs.

The stock is still highly speculative but has a compelling multi-thematic exposure across GPUaaS and Edge AI with the incredibly strategic asset of secured power in Tier 3 and 4 markets. The CEO's track record is strong and he also noted having open conversations with hyperscalers for a potential strategic investment, the stock could catch a bid.

4

15

2,660

Nitin Gupta retweeted

May 8

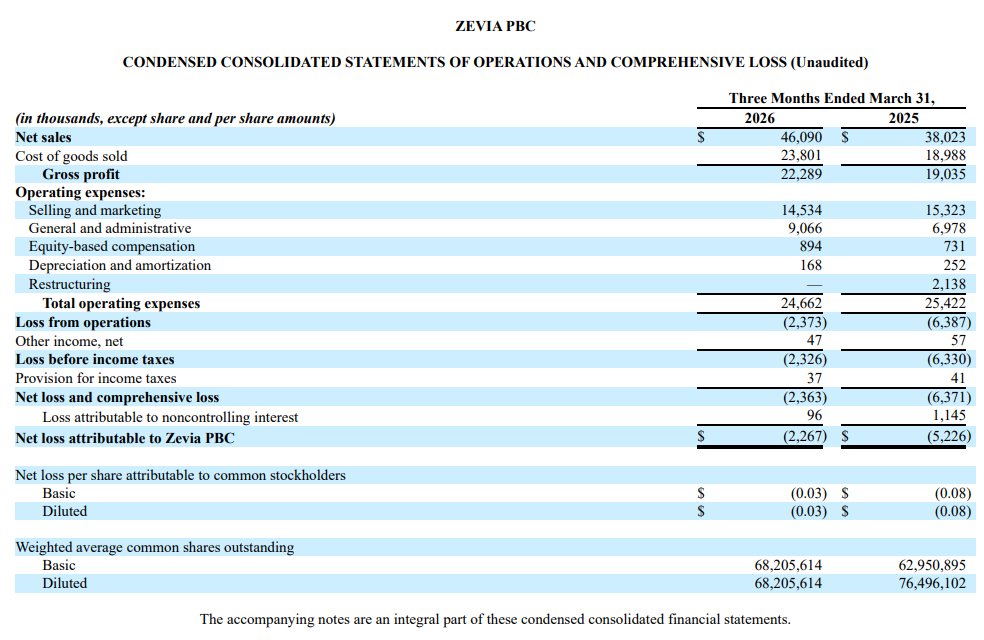

Back in $ZVIA after the call on Wednesday. We traded this very well in Q4 2024 and were lucky to take profits on time. The call was extremely encouraging and the company is showing signs of a real inflection here:

1. Revenue & Volume:

This was Zevia’s best quarter since going public as they recorded first quarter growth of 21%. The growth was entirely volume driven (20.4%) which is a great sign.

2. Channel Expansion:

They executed a successful national Costco rotation and saw acceleration in velocity at Walmart. The e-commerce business is also outperforming expectations. They have expanded in Kroger as well adding incremental flavors along with regional players like HEB and Publix. This quote was particularly interesting to me about Costco:

“The advantage of the national rotation… strengthens our velocities in the markets in which we have permanent distribution as well as helps to spur discussions about future rotations… the hope is that we would get another national rotation in the balance of the year.” — Amy Taylor

3. Cardi B Campaign upside:

This is arguably the most exciting social arb development. Zevia signed Cardi B as a brand ambassador who has the 25th most followed Instagram account. Thisc ould be a step change in reach and awareness for Zevia which they have lacked for years.

This awareness seems to be translating already as the management said that between Cardi B and other marketing programs during the month of March, Zevia saw its highest ever organic social media reach and the highest level of social media engagement of any month since the brand’s launch.

4. Profitability:

Adjusted net loss was just -$0.1M in Q1 2026, compared to -$4.2M a year ago. Selling and marketing as a % of net sales improved dramatically from 40.3% → 31.5%, demonstrating strong operating leverage as revenues scale.

5. The Setup for the Rest of 2026

Net sales guidance raised to 7% growth at midpoint, which I believe is being sandbagged massively after the impressive Q1 results. Q2 comps might be a little harder to lap but comps will get easier in Q3 and Q4.

TLDR: Q1 2026 represents a clear inflection driven by and record revenue growth, a near break-even EBITDA result, broad channel distribution gains, and the launch of the highest-reach marketing campaign in the company’s history. The packaging refresh is still rolling out and the Cardi B summer campaign hasn’t fully hit yet, meaning the biggest catalysts are still ahead. Low conviction position due to the chart looking ugly but risk/reward appears asymmetric

21 Oct 2024

$ZVIA Investment Thesis: Asymmetric Upside Potential Amid Emerging Trends

After recent analysis, I’ve shifted my stance on Zevia, due to the October Amazon data showing a significant surge in e-commerce sales. While the upcoming Q3 results may still underperform based on September data, I believe the guidance could surprise positively, creating an asymmetric risk-reward scenario.

Analysis based on Amazon sales data estimates their Amazon sales for the past month around $2.5M, which annualizes to roughly $30M. Their e-commerce sales are generally around $3M/quarter. With e-commerce making up close to 9% of Zevia’s total sales, this implies total quarterly sales could approximate $75M, and on an annualized basis, reach $300M (currently @ $160M). Given this growth trajectory, an emerging company in the Stevia beverage category should conservatively trade at 2x revenue, putting the potential market cap around $600M—representing an 8x upside from current levels. There are a lot of assumptions in the calculation which are not perfect but the margin of safety looks good due to the potential upside.

Management has also mentioned a $12M cost-cutting initiative and hinted at a major distribution partnership announcement. Sentiment on TikTok is starting to build, with the Stevia-based product gaining popularity among health-conscious consumers, positioning Zevia to grow alongside competitors like Olipop and Poppi.

This is a speculative play due to liquidity concerns and a potentially weak quarter coming up, but I am initiating a 2% position based on the substantial upside. The stock has regained compliance, and any good news could lead to outsized rewards.

Keeping an eye on Dr. Zevia (healthy version of the #2 soda - Dr. Pepper, Caramel Soda and Root beer flavours which have been driving the sales.

1

3

11

3,607

May 22

May 19

The setup for $DUOT looks good from a risk/reward prespective as several massive catalysts start to converge. The biggest immediate one is the recent FTC filing confirming Elon Musk is acquiring the parent company of APR Energy. Since DUOS holds a 5% equity stake in that entity, this buyout could act as a massive value unlock driver.

Beyond the APR stake, the operational side is rapidly derisking as well. They have a $176 million contract locked in with Founders Fund-backed Hydra Host, and the $15 million prepayment is already sitting on the balance sheet. The management noted that this relationship is increasingly getting stronger. When you pair that with the news this morning that Armada just raised capital at a $2 billion valuation, the space is starting to get some eyeballs.

The stock is still highly speculative but has a compelling multi-thematic exposure across GPUaaS and Edge AI with the incredibly strategic asset of secured power in Tier 3 and 4 markets. The CEO's track record is strong and he also noted having open conversations with hyperscalers for a potential strategic investment, the stock could catch a bid.

5

1,460

May 21

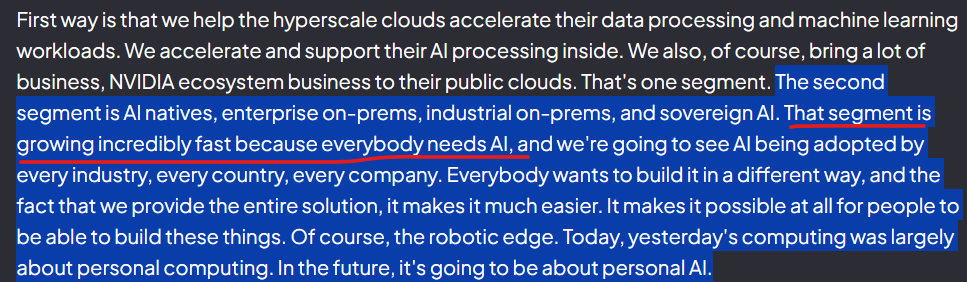

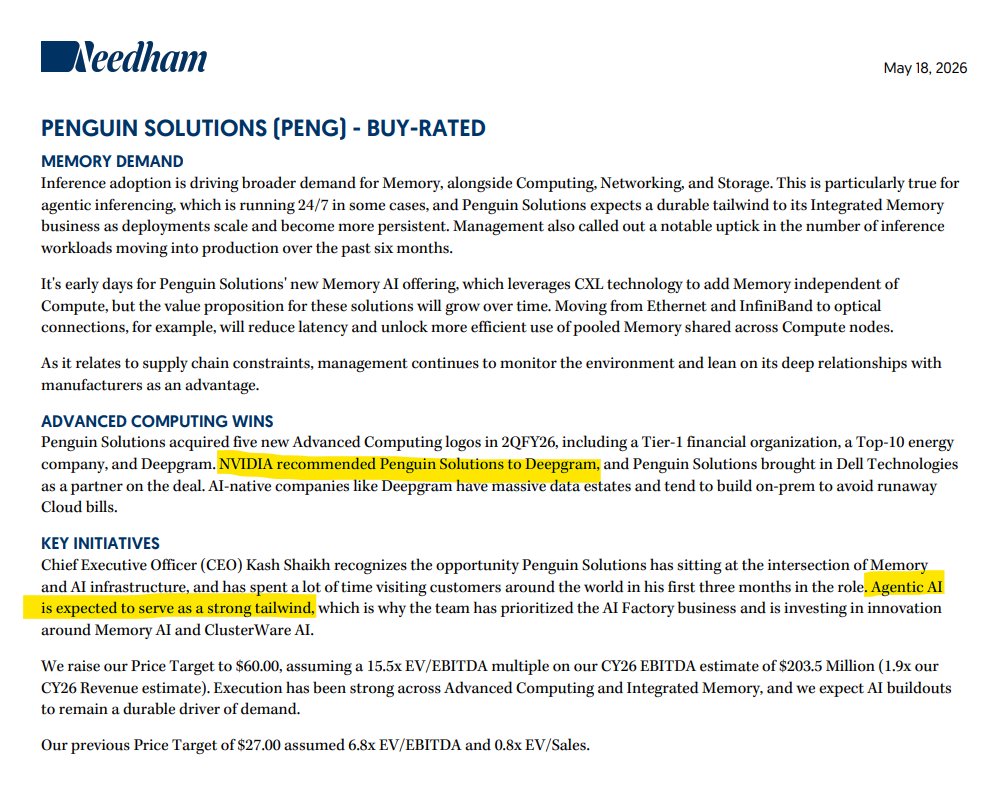

Funny how Jensen mentioned sovereign AI as the fastest-growing segment today especially after Needham's note yesterday about $NVDA actively pushing those exact sovereign AI customers to one specific infrastructure partner.

Must be a total coincidence, right? 🐧 $PENG

May 18

$PENG

Needham out today raising PT from $27 to $60

Saying $NVDA has been recommending $PENG

and citing the massive tailwind agentic AI will be for the 🐧

3

1

29

4,224

May 20

Viavi Solutions $VIAV $500M secondary offering announced today might offer a great entry point tomorrow. They are essentially doing a debt for equity swap. Viavi is eliminating roughly $35-$40 million in annual interest expenses and as per my math, this should immediately lift baseline EPS by approximately 5%.

In my opinion the market is currently mispricing Viavi by assuming top-line growth to stall, ignoring confirmed demand across their target markets. Due to their tremendous operating leverage, even marginal revenue growth will trigger significant bottom-line expansion.

Also, substantial past Net Operating Losses (NOLs) reduce their tax burden to zero. If algos sell the news it could push the price down tomorrow potentially below 30x NTM earnings. This is a great company in a very hot thematic at a reasonable valuation, those opportunities generally don't come along too often.

1

13

2,315

May 19

The setup for $DUOT looks good from a risk/reward prespective as several massive catalysts start to converge. The biggest immediate one is the recent FTC filing confirming Elon Musk is acquiring the parent company of APR Energy. Since DUOS holds a 5% equity stake in that entity, this buyout could act as a massive value unlock driver.

Beyond the APR stake, the operational side is rapidly derisking as well. They have a $176 million contract locked in with Founders Fund-backed Hydra Host, and the $15 million prepayment is already sitting on the balance sheet. The management noted that this relationship is increasingly getting stronger. When you pair that with the news this morning that Armada just raised capital at a $2 billion valuation, the space is starting to get some eyeballs.

The stock is still highly speculative but has a compelling multi-thematic exposure across GPUaaS and Edge AI with the incredibly strategic asset of secured power in Tier 3 and 4 markets. The CEO's track record is strong and he also noted having open conversations with hyperscalers for a potential strategic investment, the stock could catch a bid.

May 18

Thanks for sharing this, Jeff! I'm am getting interested in $DUOT too. The setup is starting to look a lot cleaner with the legacy rail business moving out of the picture. The APR stake could hold some solid hidden value and the Hydra Host partnership seems to be gaining momentum as well, there are a lot of interesting pieces coming together.

That comment about a potential hyperscaler strategic investor was also very interesting. Appreciate the notes!

1

16

10,371

May 13

Revenue for $MSGM came in at $4M. The prior DLC was released on December 9, 2025, whereas this quarter’s release occurred on the final day of the reporting period which probably led to the revenue realization bumping into Q2. The market doesn't seem to be liking the development cost repayment, which was an expected, structured event rather than a negative surprise.

With the enterprise value now standing at roughly $14M post-share retirement, a rapidly growing game, and several upcoming catalysts this year, the underlying valuation remains compelling. I have no plans to reduce my position.

May 10

With Motorsport Games $MSGM scheduled to report their Q1 earnings on Wednesday, May 13th, I wanted to walk through my updated earnings model and share my expectations for the quarter.

Overall, the underlying metrics are pointing in a highly positive direction, but I am keeping my official estimates slightly conservative to account for the timing of the ELMS Pack 3 release which happened on the last day of the quarter. Here is a breakdown of how I am modeling Q1 and the catalysts I'm watching closely.

Based on recent traffic and sales data, I am projecting Q1 total revenue to land between $4.2M and $4.6M, with $4.25M being the most probable scenario.

Here is the breakdown of the underlying data driving this model:

1. Game Sales: Up 15% quarter-over-quarter (QoQ).

2. Average Player Count: Up an impressive 34% QoQ.

3. RaceControl Revenue: Projected at $900K for the quarter, though the model indicates we could see an upside surprise of up to $1.05M.

4. RaceControl Traffic: Up 14% QoQ.

5. The DLC Dynamic: ELMS Pack 3 was launched (last one of the European Series) which will see deferred revenue recognition hitting the books for the players who previously purchased the season pass. Also, the massive influx of new players entering the ecosystem during Q1 creates a compounding effect whereby the new cohort now has a larger catalog of DLCs to purchase to catch up to the Q4 players. Management has already noted that the DLC attach rate is very strong, meaning this larger player base directly translates to a higher revenue per new user.

Why These Numbers Are Conservative

You might look at the 34% jump in average players and wonder why the revenue base case is sitting at $4.25M. The main reason is that unlike previous quarters where the DLCs were released a few days before the end of the quarter, ELMS Pack 3 dropped on the final day of Q1, there is a very high probability that a significant chunk of the direct revenue from the DLC purchase itself took a few days to fully realize, meaning it will spill over into the April (Q2).

My internal assessment was for the revenue to be around $4.5M for the quarter as the engagement numbers were very strong for Q1 with the game hitting the #29 spot on the Steam Top Sellers list.

4

14

2,644

May 13

I make a lot of mistakes executing entries and exits on social arb trades and share them publicly, so happy to have played this well. $GAIN

Apr 22

Took some profits here. Again, my position is entirely in options, and if the recapitalization happens, the NAV will reduce. I will hold the remaining 10% position and sell right before earnings. If my calculation is accurate, the NAV should increase around $1.40–$1.80 driven by Schylling. If the recap happens, the NAV gets reduced. The ideal scenario would be for the stock to sell off on earnings and then rebuy if the recap actually happens but a sale doesn’t. If $GAIN announces a potential sale of Schylling, the stock could continue to go higher (scenario we covered in the deep dive), but I will be more than comfortable missing out if that actually happens.

8

1,342

May 13

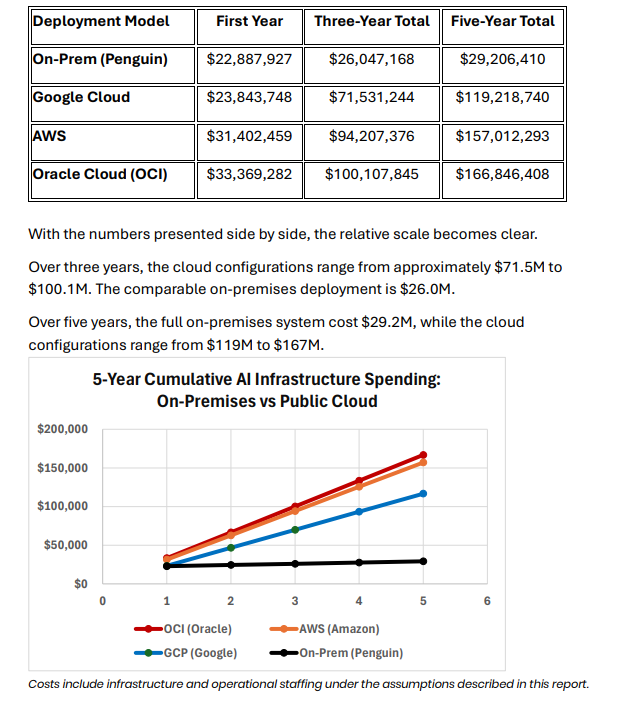

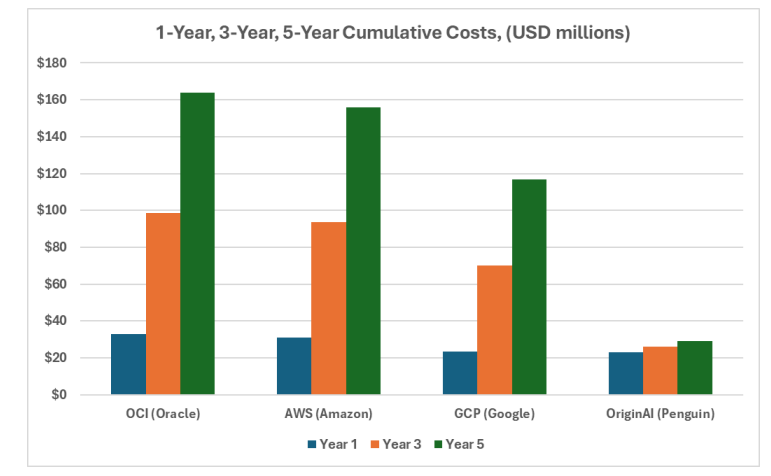

Additionally for $PENG today, I was thinking about what Kash was saying recently regarding the sheer cost of tokens and how fast developers are burning through them with the Agentic AI workflows. It made me want to dig in and see if we could find some actual numbers. I came across a detailed Total Cost of Ownership analysis by Olds Research that models out exactly what this looks like for a steady state 248 GPU enterprise AI cluster, and the math just makes their solutions a no-brainer.

According to them On-Prem (Penguin Solutions) costs $26.0M over 3 years while public cloud (AWS, GCP, OCI) solutions range from $71.5M to $100.1M over 3 years. Renting cloud capacity for these workloads costs an average of over 3.5x more than building on-prem. With the ever increasing costs of compute and deployment it becomes obvious that most enterprises would prefer to have to own their infrastructure for inference and steady-state AI. Additionally, many companies have mentioned the trend of compute moving to the edge which is another thematic they have exposure to.

Add on top of this Penguin's strategic partnerships, especially the integration with SK Hynix and you essentially have a product that sells itself. They have the exact hardware and integration capabilities that these enterprises are scrambling for right now.

May 12

Hey guys, sorry I'm late, it was a crazy busy day at work. I see you guys already shared some great insights on the $PENG Needham call!

For me, the biggest takeaways were the following:

1. If you look at the mid-point of the 12% guide and the segment guides from the Q2 call, my calculations imply an AI factory segment revenue of $1.02B for FY'27. However, with Kash explicitly saying this is well over a $1 billion business, it makes me think they are being conservative and should easily beat that 12% guide for the year.

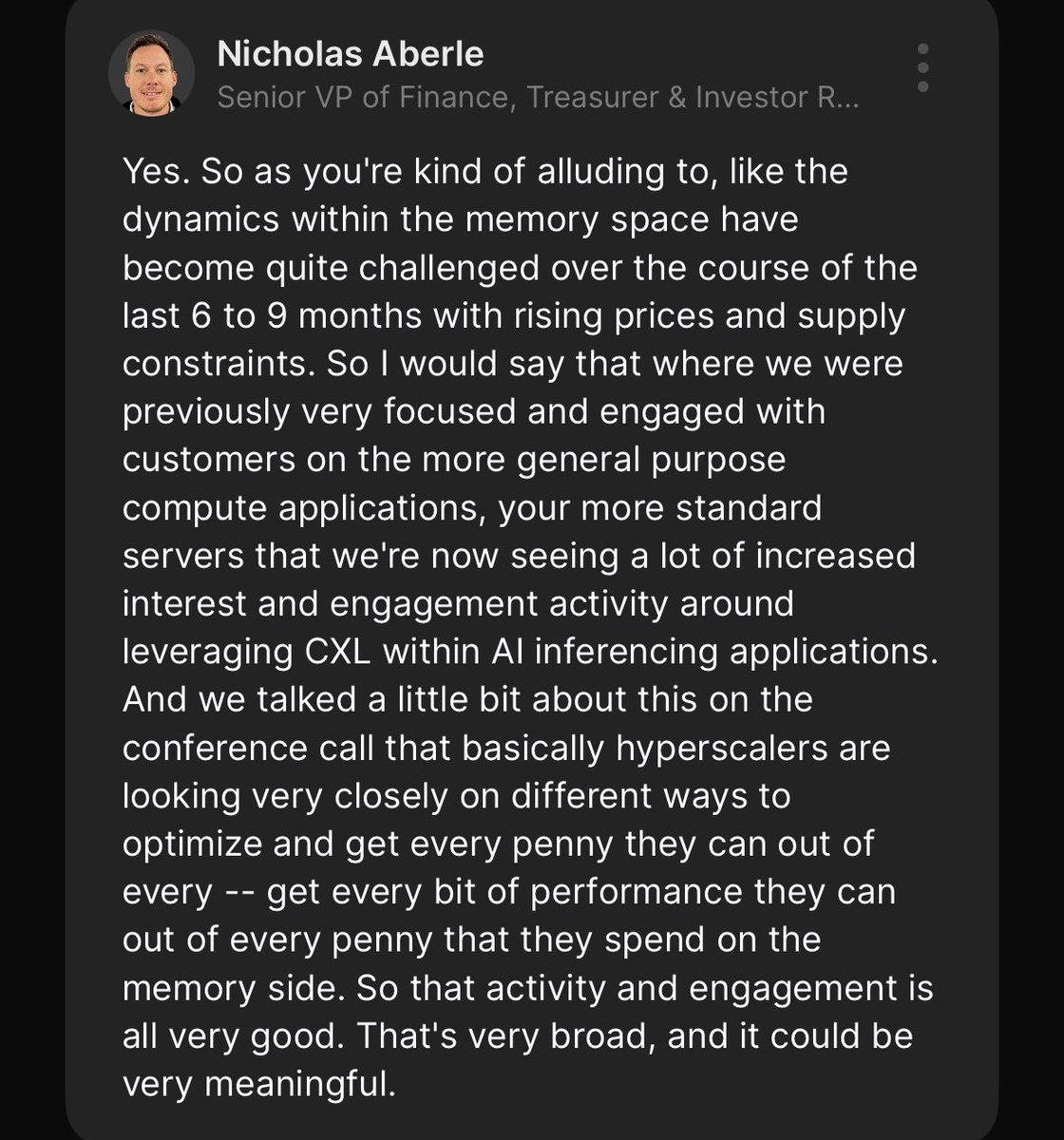

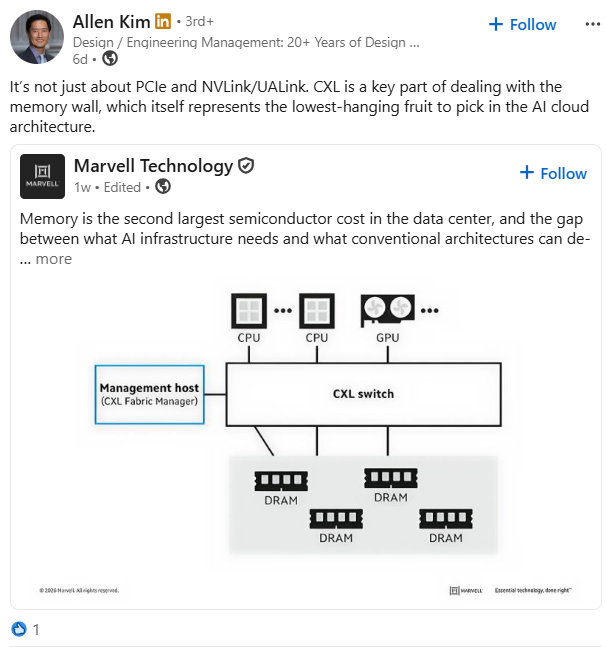

2. With the guidance basically achieved, there is a very good chance their backlog for next year is incredibly strong. They mentioned it takes 3-6 months to convert backlog into revenue, so that pipeline is locked in. Also, "Nobody else in the market has a product like MemoryAI, which is helping our customers and helping us win deals." That CXL product is a massive differentiator right now and their partnership with $MRVL makes this a great opportunity (they also have partnership with $DELL, $AMD, $NVDA as we know).

3. SK Hynix being a strategic investor is incredibly bullish and honestly something I didn't fully realize until they mentioned it. This completely de-risks the supply issue. Procuring demand is a massive constraint for everyone else, but them saying we've been able to access it and serve as much demand as we can and that the relationship helps with margins is quite massive.

Maybe too much of a stretch but long-term, this could possibly lead to SK Hynix promoting PENG's products against competitors. It also gives PENG immense leverage with rack builders and larger enterprises because clients know PENG actually has the supply to deliver. That alone demands a huge premium and is a massive moat in my opinion.

2

12

83

11,546

Nitin Gupta retweeted

May 12

Hey guys, sorry I'm late, it was a crazy busy day at work. I see you guys already shared some great insights on the $PENG Needham call!

For me, the biggest takeaways were the following:

1. If you look at the mid-point of the 12% guide and the segment guides from the Q2 call, my calculations imply an AI factory segment revenue of $1.02B for FY'27. However, with Kash explicitly saying this is well over a $1 billion business, it makes me think they are being conservative and should easily beat that 12% guide for the year.

2. With the guidance basically achieved, there is a very good chance their backlog for next year is incredibly strong. They mentioned it takes 3-6 months to convert backlog into revenue, so that pipeline is locked in. Also, "Nobody else in the market has a product like MemoryAI, which is helping our customers and helping us win deals." That CXL product is a massive differentiator right now and their partnership with $MRVL makes this a great opportunity (they also have partnership with $DELL, $AMD, $NVDA as we know).

3. SK Hynix being a strategic investor is incredibly bullish and honestly something I didn't fully realize until they mentioned it. This completely de-risks the supply issue. Procuring demand is a massive constraint for everyone else, but them saying we've been able to access it and serve as much demand as we can and that the relationship helps with margins is quite massive.

Maybe too much of a stretch but long-term, this could possibly lead to SK Hynix promoting PENG's products against competitors. It also gives PENG immense leverage with rack builders and larger enterprises because clients know PENG actually has the supply to deliver. That alone demands a huge premium and is a massive moat in my opinion.

4

4

45

14,347

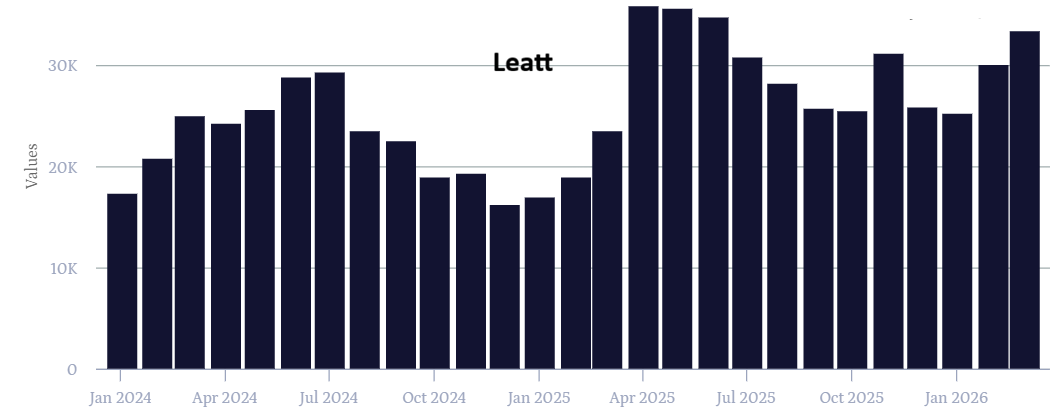

May 12

$LEAT - Pretty much as expected, looking forward to listening to the call.

Apr 30

I initiated a small position in $LEAT (Leatt Inc.), as the setup we are seeing right now is incredibly compelling. Between a pristine balance sheet and shifting industry tides, the risk/reward ratio is highly asymmetrical. Didn't know @OlivierColombo is an analyst on the stock. Last time we were on a stock together - $LSF, it ended up being a multi-bagger.

The company is currently sitting on ~ $13M in cash with almost no debt implying an EV to EBIT of around 11 times with gross margins last year expanding by 3.74% and net margins turning positive with opex remaining flat on revenue growth of almost 40% exhiting tremendous operating leverage.

The End of the Destocking Headwinds:

The protective gear market has been battered by severe destocking over the last year, but the worst appears to be behind us. Looking at recent commentary from Mips (MIPS.ST), the massive inventory headwinds might be clearing.

Alternative data is further suggesting that the artificially low stocking levels across distributors could be depleted much faster than the market anticipates. This rapid drawdown could lead to additional orders in the upcoming quarter (a lot of the sales by these companies are obviously made before the seasonal demand kicks in).

Geographic Tailwinds:

Europe has been a powerhouse of the industry, and Leatt has maintained remarkable strength there regardless of market conditions. However, the narrative in North America could lead to further upside as North America has trailed Europe for some time now.

Mips said "north american market continues to develop well and Asian market has stabilised." Thule also indicated that the North American market is flattening. This flattening is extremely bullish indicator for Leatt. If the trends are finally heading in the right direction and the North American market begins to accelerate, it adds an entirely new layer of growth on top and with operating leverage kicking in, the stock can really catch a bid.

The Moto Catalyst

Moto was Mips' largest growth driver recently, posting a massive 33% growth. Management explicitly stated that "motocross remains the key driver, but also on-road category is starting to accelerate."

While Mips and Leatt are competitors, this could be a leading indicator for the sector. If Leatt was able to command market share and hold their own during a period of severe material headwinds and aggressive industry-wide destocking, they are in a prime position to capitalize if the market accelerates materially.

The aggregate YoY comparative traffic for the major Motorsport websites in North America is finally trending the right direction with US Amazon search trends and google trends all supporting a market on the verge of a major inflection point.

1

22

3,762

May 12

$PENG thesis seems to be very strong, shout out to @pennycheck . $ALAB, $MRVL, and $3529.TWO have all stated they are seeing growing adoption for CXL, and it is almost certain the $PENG management team will reiterate this tomorrow. Super interesting to see what they say regarding the order velocity they are seeing themselves.

$MRVL and Samsung, along with $MU making the famfs file system free and open-source, really makes you think they are actively supporting the CXL movement.

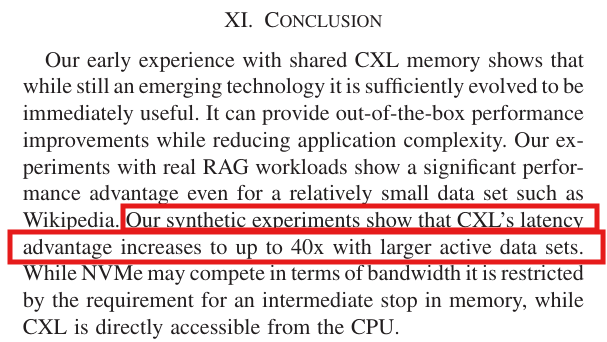

I’d highly recommend reading Alfred Bratterud's paper on the importance of CXL. The potential it offers for AI is insane. They proved it can deliver a 40x latency reduction over high-end NVMe drives and a 3.3x throughput jump when handling massive datasets. It even allows for instant server scaling without moving any data. The tech could really be a game changer.

3

6

138

13,629

May 11

$MSGM player numbers strarting recover from the slump last couple of weeks after the v1.3 update introduced some bugs. The WEC popularity thesis seems to be playing out in real time as the game is dropping rapidly in the best sellers list. Was hovering close to 300 last week and now down to 80.

May 11

$MSGM is and should continue to benefit from this trend as the official partner of WEC, with the e-gaming events set to return this year after the 2023 event. The e-gaming segment should contribute incremental revenues to the PnL at ~50% gross margins and is expected to be bigger this time due to greater traction for both the game and the event. Additionally, GT3 continues to gain hype with Max Verstappen now driving in these events.

1

9

1,747

Nitin Gupta retweeted

May 8

Surprised to see no movement in $BE after $BAM said this on their call today:

“The first deal we did in our AI infrastructure fund was our partnership with Bloom Energy. That was announced, I wanna say, 6 or 9 months ago, a $5 billion partnership. We are already in conversations to expand that partnership, not by percentages, but by multiples. That's very reflective of the opportunity set and the scale that we expect to play.”

5

5

36

6,436