⚛️🌈Investor, Crypto Optimist, @cosmos @cosmoshub & @buildonbeam enthusiast⚛️ 🌈 $ATOM $BEAM

Joined November 2024

- Tweets 5,682

- Following 894

- Followers 232

- Likes 9,754

1,304 Photos and videos

Pinned Tweet

Mar 31

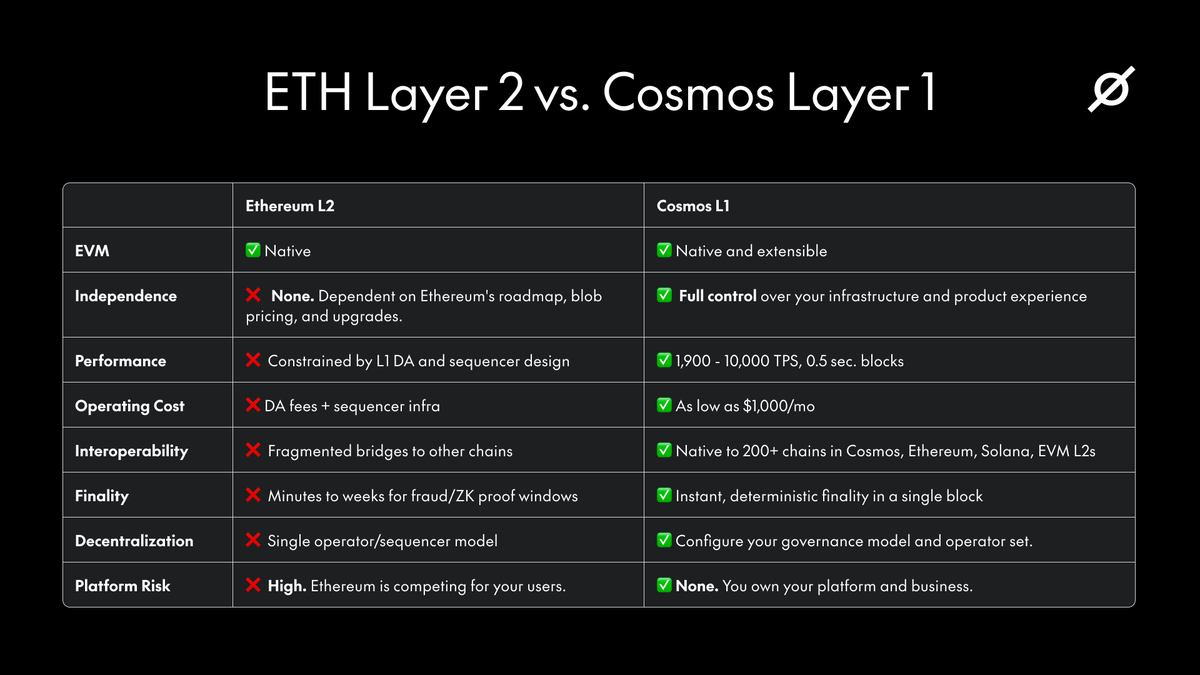

Become sovereign. ⚛️

@cosmos #InternetOfBlockchains

Independence. Control. Scalability.

The Cosmos Stack gives leading businesses a foundational layer for digital assets that will scale for years to come.

3

3

12

2,446

Jasøn retweeted

Another year of forced speculation about Jalen Hurts that makes NO sense if you’re paying attention…

18

15

150

4,919

Jasøn retweeted

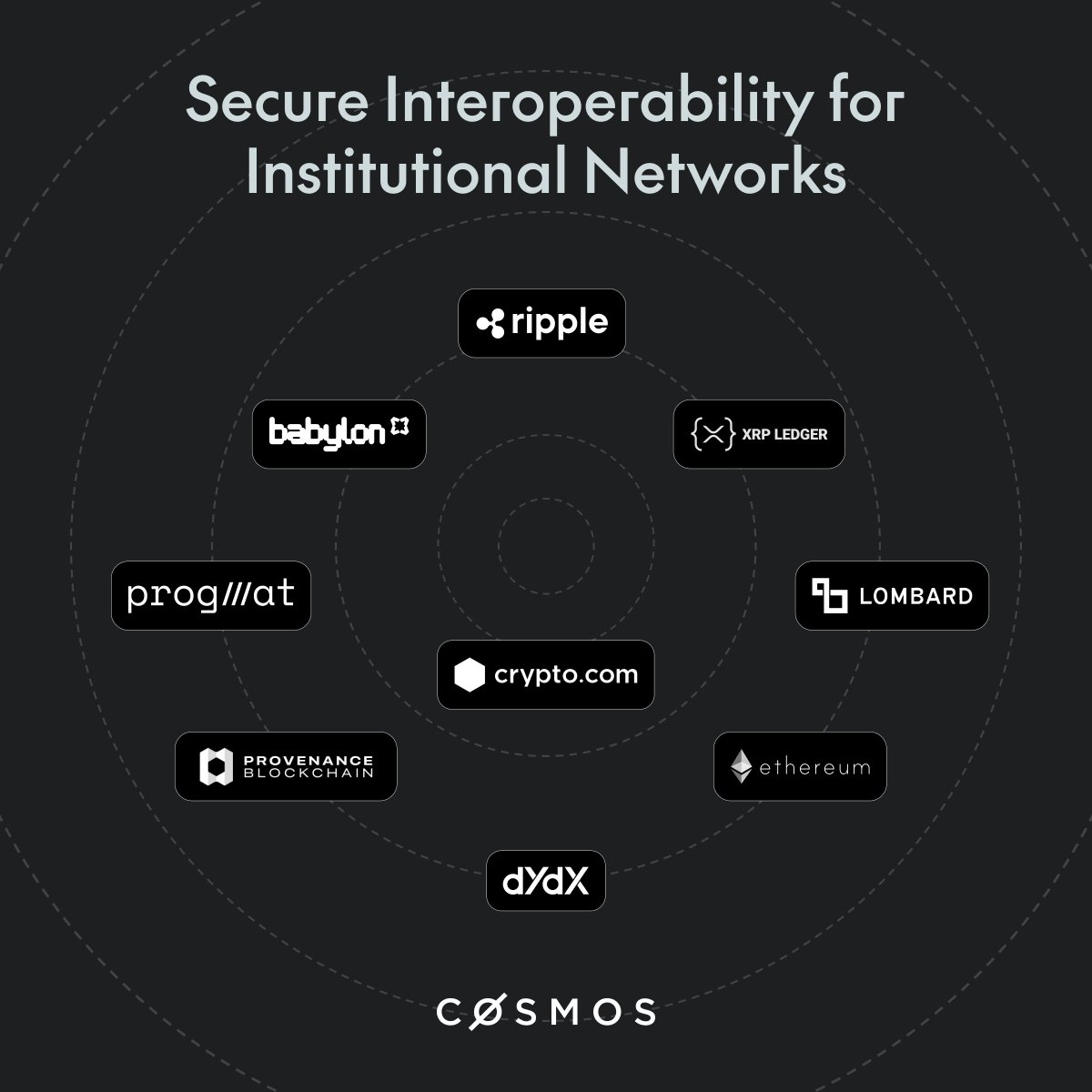

Finance industry players already in the IBC network include @Ripple, @provenancefdn, @progmat_en, @cryptocom, @Lombard_Finance, and more.

Learn how we can help your business: cosmos.network/ibc-interoper…

1

5

22

1,242

Jasøn retweeted

Decision-makers at FIs and payment networks evaluating cross-ledger settlement infrastructure run into the same three gaps.

Here's what they are and how Cosmos's IBC improves the interoperability experience for institutional leaders.

5

14

61

2,422

Jasøn retweeted

Jun 15

Group B of World Cup

368

4,676

64,707

2,399,977

Jasøn retweeted

Jun 15

Most people still think the future of digital money = stablecoins.

That’s incomplete.

The bigger transformation is happening quietly inside the banking system.

While stablecoins dominate headlines, tokenized bank deposits are already moving trillions of dollars annually through financial institutions.

Why does this matter?

Because we are likely moving toward a 3-layer on-chain monetary system, not a winner-takes-all model.

1. Stablecoins → “Money in Motion”

Optimized for speed, programmability, and global accessibility.

They work well for:

• cross-border transfers

• remittances

• payments in underbanked regions

• crypto-native settlement

But stablecoins have limits:

• concentrated issuance (mostly USD)

• regulatory pressure

• limited institutional adoption

• banks lose deposits when customers move capital into third-party issuers

That last point is important.

When someone converts bank deposits into a stablecoin, banks lose part of their funding base and, more importantly, the customer relationship.

2. Tokenized Bank Deposits → “Money at Rest”

This is the underappreciated story.

Instead of replacing bank money, banks are tokenizing their existing deposits on blockchain rails.

Same regulated deposit. Same balance sheet.

Different infrastructure.

This gives banks:

• faster settlement

• programmable money

• atomic transactions

• lower reconciliation costs

• 24/7 transfer capabilities

Without giving up deposits to external stablecoin issuers.

This is why major institutions are investing heavily here.

JPMorgan, Citi, BNY and others are already running pilots or live systems.

Some estimates suggest tokenized deposits already facilitate $4T annually, massively larger than stablecoin payment activity.

3. CBDCs / Tokenized Central Bank Money → “Settlement Money”

Still early.

But this layer matters because it solves something stablecoins and commercial bank deposits cannot:

final settlement without counterparty risk.

Banks can move value between themselves, but true global interoperability ultimately requires a neutral settlement asset backed by central banks.

That’s where wholesale CBDCs could fit.

The key insight:

The future is probably coexistence, not replacement.

Stablecoins for movement.

Tokenized deposits for institutional liquidity.

CBDCs for final settlement.

This mirrors how the financial system already works today — just rebuilt on blockchain infrastructure.

The real disruption isn’t “banks vs crypto.”

It’s the gradual migration of the monetary system itself on-chain.

Read McKinsey’s thoughts on the emerging architecture of on-chain money: mckinsey.com/industries/fina…

2

4

17

595

Jasøn retweeted

They argue that success will be determined by which legal rulebook gains enough signatures to create critical mass.

The best-in-class coordination infrastructure already exists within Cosmos Stack.

2

3

20

1,957

Jasøn retweeted

Interoperability is a primary constraint limiting the adoption of tokenized deposits by banks.

@McKinsey attributes the bottleneck to coordination gaps across institutions, rather than technical immaturity.

6

21

76

5,151

Jasøn retweeted

Jun 15

The biggest bet in crypto is not just speed or hype.

It’s interoperability.

Cosmos has been building the idea of connected sovereign blockchains for years with IBC.

The future may not belong to a single chain.

It may belong to the network that connects them all. ⚛️

2

17

236

Jasøn retweeted

Jun 8

LETS GOOOO🔥🔥🔥

Jun 8

🚨 UPDATE: Crypto Fear & Greed Index dropped further to 8 (Extreme Fear) today, down from 12 yesterday.

1

1

2

147

Jun 13

What happens to the student's first app, or the privacy tool built by a volunteer? Google's mandatory registration blocks them all by default unless they play by Google's rules. keepandroidopen.org #KeepAndroidOpen

18

Jasøn retweeted

Mar 31

Become sovereign. ⚛️

@cosmos #InternetOfBlockchains

Independence. Control. Scalability.

The Cosmos Stack gives leading businesses a foundational layer for digital assets that will scale for years to come.

3

3

12

2,446

Jasøn retweeted

Jun 11

Canada🤝Robinhood

Jun 2

🇨🇦 JUST IN: Robinhood officially enters Canada after closing its acquisition of WonderFi, a leading regulated digital asset platform operator in the country.

80

60

993

131,420

Jasøn retweeted

Jun 10

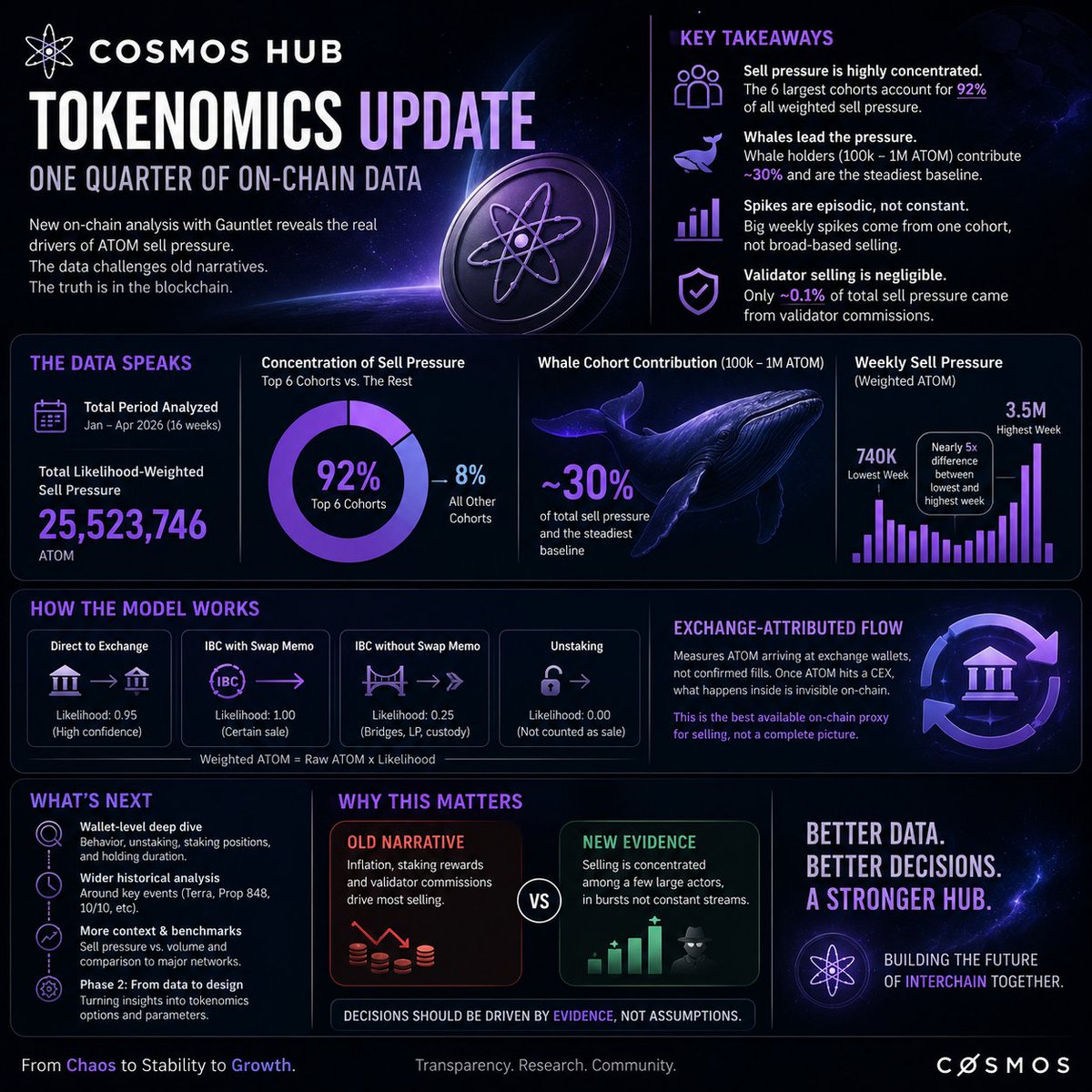

New data from the Cosmos Hub is challenging one of the biggest narratives around $ATOM.

For years many assumed that inflation staking rewards and validator commissions were the main reason behind ATOM’s sell pressure. But after analyzing an entire quarter of on-chain activity January to April 2026 the early findings suggest something very different.

The research conducted with Gauntlet tracked where ATOM movements actually go and measured the probability that these movements represent real selling. Instead of assuming every transfer equals a sell event the model assigns confidence levels based on behavior. For example direct transfers to exchange wallets are treated as highly likely sells while unstaking alone is not counted as selling at all.

The result?

Sell pressure appears to be highly concentrated among a small number of large holders rather than driven by everyday stakers or inflation.

A few key findings stand out:

• The six biggest holder groups accounted for 92% of total estimated sell pressure during the quarter.

• Whale wallets holding 100k–1M ATOM represented around 30% of consistent selling activity.

• Weekly sell pressure varied dramatically with spikes usually caused by single large actors not broad market exits.

• Validator commission selling was almost irrelevant at just ~0.1% of total sell pressure.

Perhaps the biggest takeaway is this:

The data suggests that ATOM inflation may not be the villain many believed it was. Instead of constant sell pressure from staking rewards the market appears to be reacting to episodic moves from a handful of large wallets.

Why does this matter?

Because tokenomics decisions should be driven by evidence not assumptions. If inflation is not the primary source of pressure then future discussions around emissions staking incentives and Hub economics may need a completely different approach.

This is still Phase 1 research but it points toward something important:

The @cosmoshub is finally moving from narratives to data-driven decision making and that could reshape how the market understands ATOM.

forum.cosmos.network/t/token…

5

12

63

1,482

Jasøn retweeted

Intergaze Migration is done ✅

🏆 All collections have migrated to stargaze.zone

🎯 If you didn't register for the migration with your Cosmos wallet, you can still do so via late claims:

migration.intergaze.xyz

@StargazeZone @intergaze_xyz $STARS $INIT #stargaze #intergae @initia #initia

1

5

207

Jasøn retweeted

Jun 12

The Beam ecosystem brings together the most ambitious projects across AI, compute, DeFi, and consumer applications.

Are you on of these and need a little push?

grants.onbeam.com

5

9

51

2,009

We have been quietly putting together an all star team of incredible quality.

@eranbarak and @IamIanKane add to heavyweights like:

- @vladjdk

- “KZ” many without X

- @cozartshmoopler

To grateful to work with these folks

1/ Cosmos new hires 🤝

@cosmoslabs_io just brought in some big names. Could this finally be the dream team $ATOM and Cosmos Hub always needed?

A thread 🧵 👇

4

70

153

4,393