255 Photos and videos

Bottom signal, ICP dreams are being crushed again. We're at C - D

2

1

17

1,629

Altcoins historically crash the most at the first signs of bear market. The liquidity events that caused extreme lows happened already, exhausting sell pressure (red - orange)

With two less intense drops to be fulfilled alts can make slightly lower lows 10-20% down, not 90%.

1

2

126

With overarchievers like ICP falling less than BTC and pumping between drops or even during drops, lows look to be heading no lower than $1.8 for this current drop, & finally a good chance of a higher low for the final leveling off crash BTC might have following the 2022 crash.

3

54

Omnia.ICP retweeted

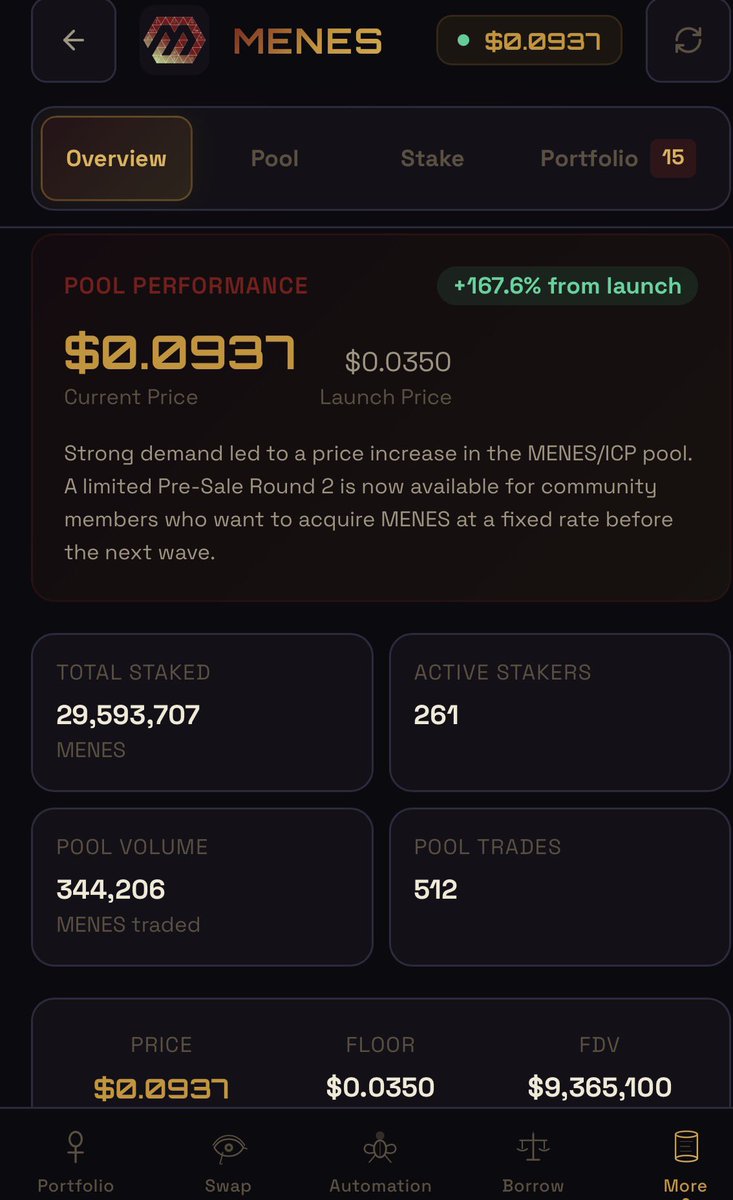

Proud of what we’ve built at Menese Protocol in $ICP with just $70K raised.

We’ve shipped: • New cross-chain innovations • Cross-chain pools

• Investor exit liquidity pool • Fully tested launchpad accepting $XRP, $ETH & $SOL

Every dollar raised was deployed into fee-generating activities; borrowing, lending, cross-chain swaps, bug bounties, and a marketing campaign that already reached 1 million users.

5 enterprise customers hundreds of active users since launch.

You are not bullish enough, we have not started yet going man stream CEX routes!

13

41

191

5,548

Historically when ICP makes a double bottom at this stage of the bear market it rejects further downtrend and taps the green descending trend line again, has a quick sell off back to the accumulation zone, and then leaves these prices behind at $4

These are my targets to dca. I'm looking for a rebound around these levels & only at the bottom of a strong move that coincides with panic & a BTC drop to the historical fib level low around 56-54k.

Thanks to the recent price action we might actually have a higher low this time.

3

166

These are my targets to dca. I'm looking for a rebound around these levels & only at the bottom of a strong move that coincides with panic & a BTC drop to the historical fib level low around 56-54k.

Thanks to the recent price action we might actually have a higher low this time.

1

1

6

643

Sick & TIRED of ICP influencers telling their infinisimps that a trend line has broken. Betch where??????????

Y'all r drawing lines wherever you want 😭😭 go with the exact tops of wicks so u don't call trends breaking early. Also just wait for higher highs & higher lows damn 😮💨

Jun 3

$ICP just did something it hasn't done in years.

Broke out of a multi-year descending resistance — cleanly.

Price: $3.13

Target on chart: $20

That's a 1,041% move projected from current levels.

We're sitting in the accumulation zone right now. Every "L" on this weekly chart was a gift. The last one? Right here. Right now.

Descending trendline = broken ✅

Support zone = holding ✅

Weekly candle = 15% and climbing ✅

The ones who waited since 2023 are about to eat.

#ICP . From $3 to $20. Weekly chart doesn't lie.

6

2

34

3,513

So volatile it doesn't feel like sideways action but zoom out it kinda has been. very glad ICP was resisting downtrend but I want my final dip so I can buy a few thousand more ICP

Still watching for sideways action before a drop to a significant low and rebound for the final spring ICP needs

3

168

Still watching for sideways action before a drop to a significant low and rebound for the final spring ICP needs

The rejection frames that we're not actually out of red bubble, just volatile mid way through like last red bubble, but larger. My new delulu chart imagines a retest of lows, wyckoff spring, and then a smaller pump before exiting the lows and challenging downward trendlines.

8

364

Omnia.ICP retweeted

May 15

Not to be biased, but the objective data backs it up: it's retail that's been doing the selling. The market simply hasn't assigned value to ICP yet, and some longer-term holders have lost patience after several years, which is fair. The market rewards different things, otherwise it would be impossible to explain how memecoins reach market caps dozens of times higher than projects shipping real infrastructure.

And we're not talking about performance here; that's where you could fire back with "but other tokens aren't as inflationary." We're talking market cap, where supply is already baked into the math.

What's actually happening on the adoption side:

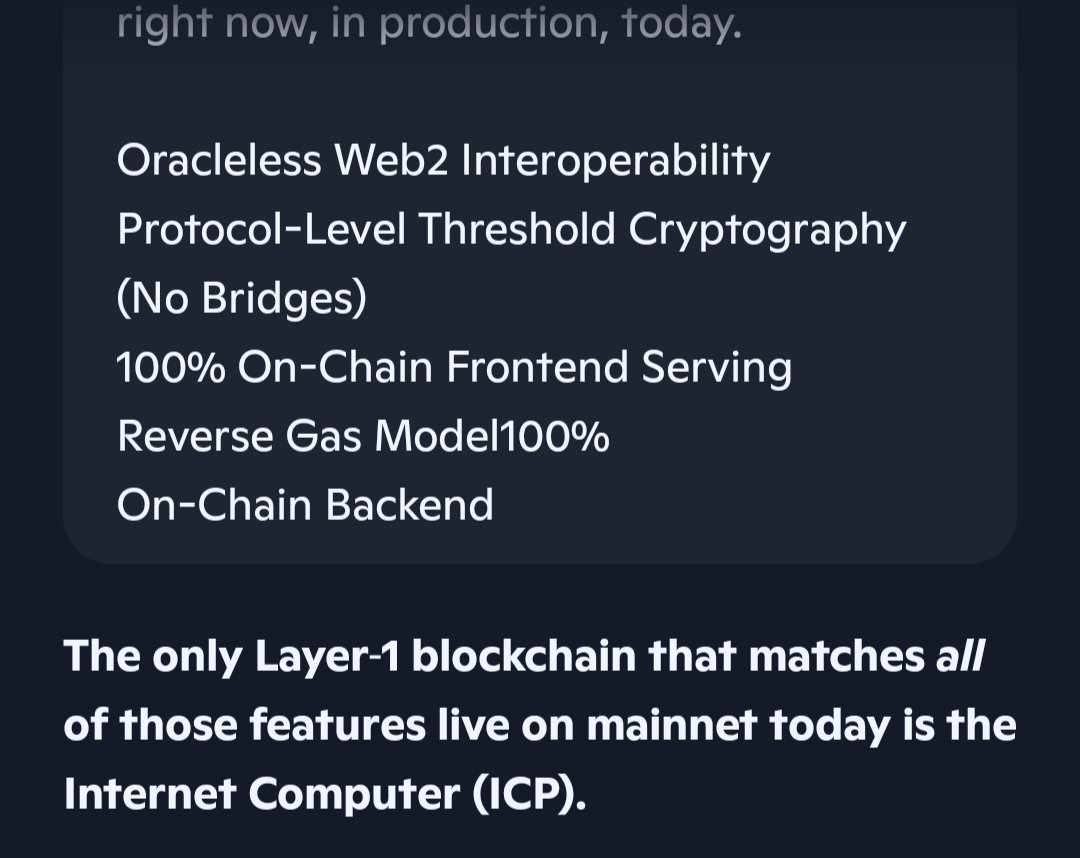

- Pakistan Digital Authority signed an MoU with DFINITY for a sovereign Pakistan Subnet: national-scale AI, in-country data, a national messenger app, 1,500 Caffeine licenses

- Switzerland deployed a sovereign subnet weeks earlier

- DFINITY × UNDP partnership on Universal Trusted Credentials, piloting in Cambodia with plans to scale to 10 countries

What that means for value:

-Sovereign cloud deployments = multi-million-dollar compute lock-in per nation

-Each sovereign subnet = perpetual, non-speculative ICP burn

-UN-level legitimization is something ETH and SOL simply don't have at the nation-state layer

Honest comparison:

- Solana: zero sovereign deployments

- Ethereum: zero significant sovereign deployments

- ICP: multiple confirmed sovereign deployments and pilots

This is exactly the kind of traction the crypto market isn't pricing in, because it reads as "boring infrastructure" vs. "memecoin pump." But it's also exactly what institutional capital looks at.

Now the honest counterpoint, because pretending otherwise would be cope:

Ethereum Classic had the same tech as ETH and stayed near $20 while ETH ran to $4,500. Bitcoin Cash shared BTC's foundation and never recovered. Litecoin was supposed to be "silver to Bitcoin's gold" and has been stagnant for years!

Fundamentals don't automatically translate into price. Narrative, timing, and market structure matter. But the asymmetry on ICP, actual sovereign-scale adoption that no other L1 has, is the kind of thing that, if it ever does get priced, doesn't get priced gradually.

3

9

50

1,054

The rejection frames that we're not actually out of red bubble, just volatile mid way through like last red bubble, but larger. My new delulu chart imagines a retest of lows, wyckoff spring, and then a smaller pump before exiting the lows and challenging downward trendlines.

Red bubble took 3 months to exit this time! If the parttern continues as it has for years now it will head into a pre-parabolic rally!

We can estimate this will take ~3 months, 22 days

given last purple bubble took ~1.24x the time red bubble took.

Vertical action on ~August 26

2

2

27

2,236

Omnia.ICP retweeted

May 14

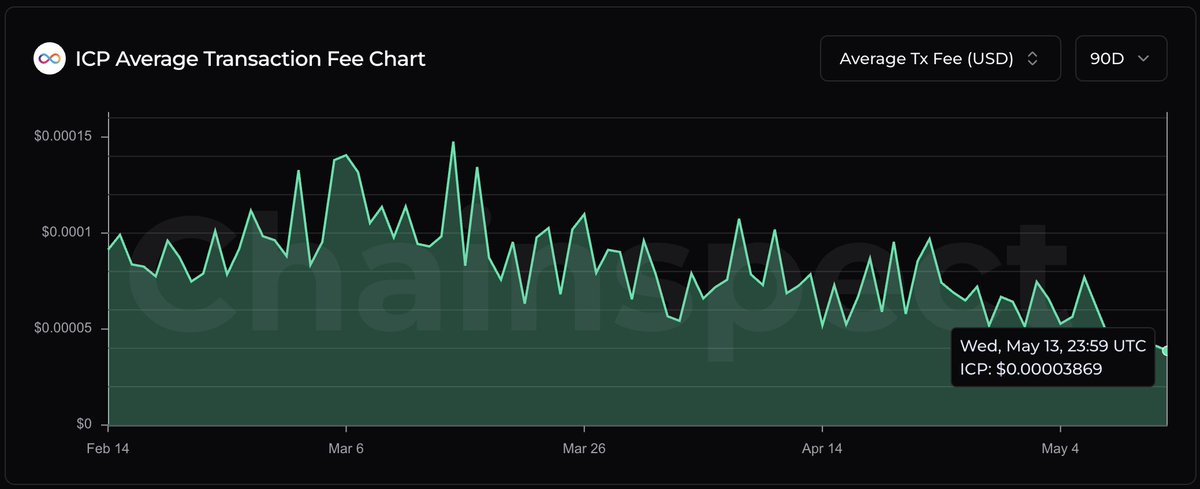

.@dfinity is making Internet-scale compute absurdly cheap

ICP's average transaction fee just dropped to a new 90-day low of $0.0000387, down 6.3% from the previous low

AI-native cloud infrastructure only works when usage costs get this close to zero

📊 chainspect.app/chain/icp?ran…

12

52

204

13,216

Ohshii doing it again 🤯 100% the place to launch a project on ICP. Think of the possibilities with this.

May 14

Looky looky what you can now hold on @ohshiilabs 🦠🔬

Users across the various DAOs will also be able to receive NFT rewards directly on OhShii whenever teams want to reward members for completing actions such as locking, voting, contests, and more

Amazing stuff from the team🔥

1

18

685