The stock market rewards patience, discipline, and perspective.

Joined December 2021

- Tweets 2,452

- Following 2,402

- Followers 1,849

- Likes 6,306

895 Photos and videos

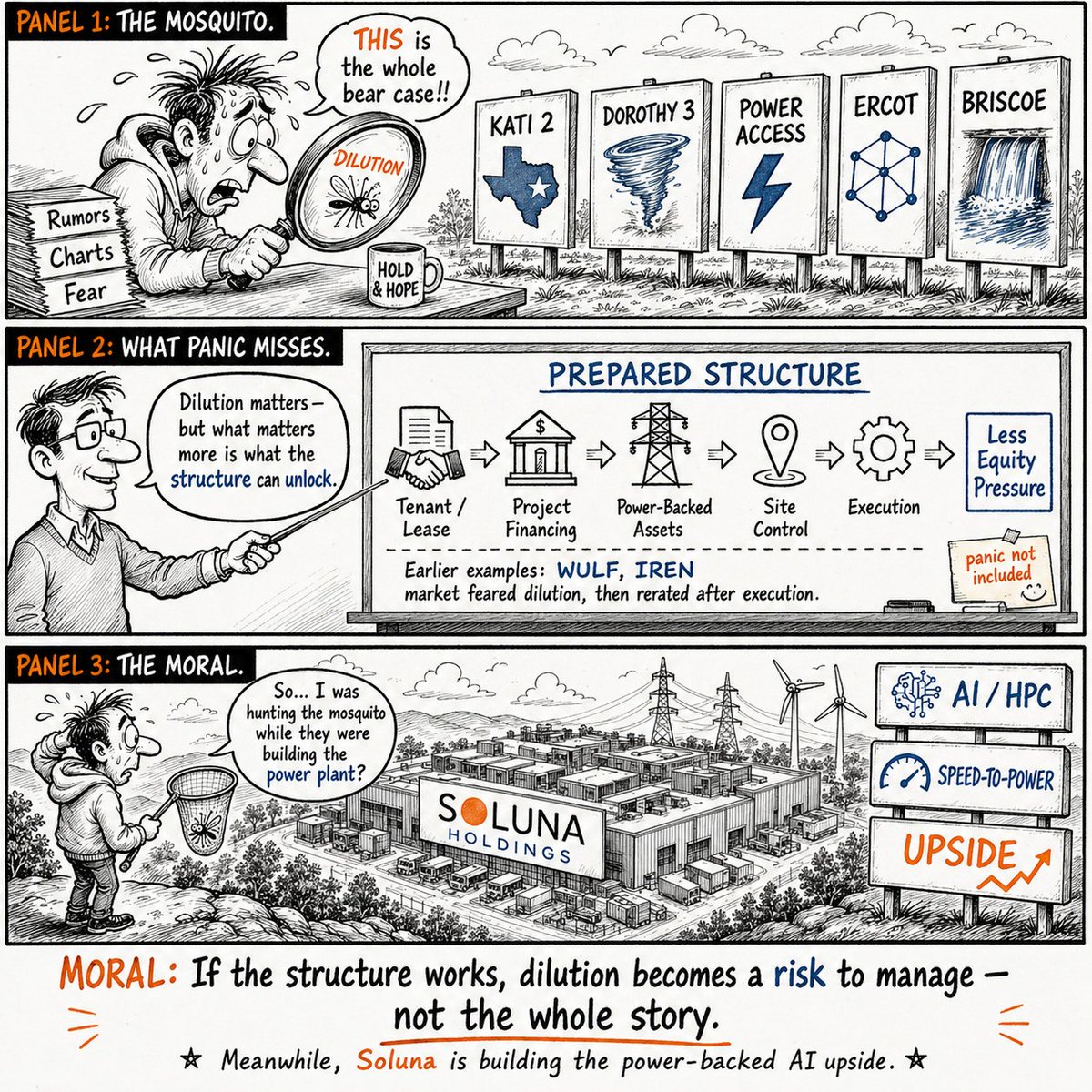

$SLNH @SolunaHoldings Well, this question keeps coming up again and again because people still don’t understand how this works. Dilution is not automatically the monster under the bed.

The question is: what is the company getting in return?

If shares are issued just to keep the lights on, that is bad dilution.

But if capital, project financing, leases, JVs or tenant-backed structures help unlock 100MW, 200MW or more of power-backed AI infrastructure, then the dilution becomes more like paying the toll before crossing the bridge.

People are staring at the toll booth while ignoring the city being built on the other side.

Jun 13

When will share holders stop being diluted?

9

4

42

3,284

$slnh

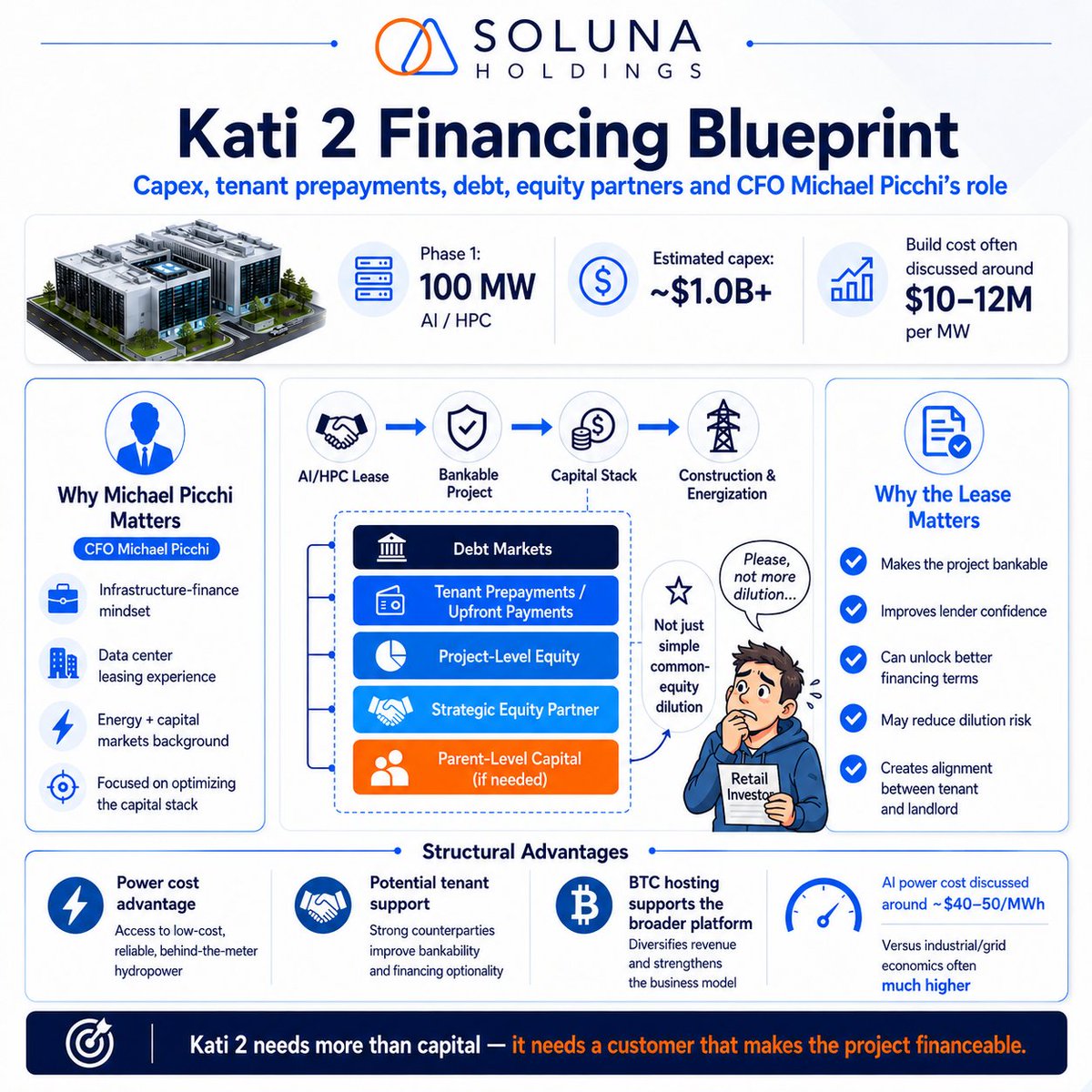

I’ll start with the financing part, because that is where I see most of the questions around @SolunaHoldings right now.

A lot of investors look at Kati 2 and immediately ask the same thing:

How can Soluna finance a project of that size without massive dilution?

That is a fair question.

But after listening to the interview, I think the better way to look at it is that Kati 2 is not being positioned as a simple parent-level equity-funded project.

John talked much more like this is an infrastructure-finance structure.

The first 100MW phase could easily represent $1B of capex if we use the rough $10–12M per MW range discussed for AI/HPC colocation builds. That number sounds huge when compared to Soluna’s current market cap.

But the key is the capital stack.

The discussion was not “raise common equity and build.”

It was about lease-driven financing, debt markets, tenant support, upfront payments, project-level equity, strategic equity partners and optimizing the full capital structure.

This is where CFO Michael Picchi becomes important.

John basically described him as the right CFO for this stage of the company because his background sits at the intersection of energy infrastructure, capital markets and data center leasing. The interview also highlighted that Picchi has prior experience around data center lease structures and has successfully worked with upfront tenant payments in the past to help accelerate buildout timelines.

Soluna is not only trying to finance a building. They are trying to finance large-scale AI/HPC infrastructure around power, lease contracts, tenants, equipment timelines and project-level capital.

A strong AI/HPC lease does not only create future revenue. It can make the project bankable. It can improve lender confidence. It can support debt financing. It can attract infrastructure capital. It can also open the door for tenant prepayments or upfront capital if speed-to-power is critical.

In a market where AI capacity is scarce and power is the bottleneck, that kind of structure could matter a lot.

This is also why Picchi’s hire looks well-timed.

Soluna does not just need a CFO who can manage reporting. They need someone who understands how to structure a large capital stack around data center demand, power economics, infrastructure capital and tenant credit.

That does not mean dilution risk disappears.

Kati 2 is still a huge project, and the final terms will decide how much value Soluna keeps. But I think the market often frames the question too simply.

The question is not:

“Can Soluna fund $1B alone?”

The real question is:

“Can Soluna land a bankable AI/HPC tenant that unlocks debt, tenant support and project-level capital?”

That is the financing inflection point.

And that is why the first Kati 2 lease matters so much.

6

1,125

$SLNH $CIFR

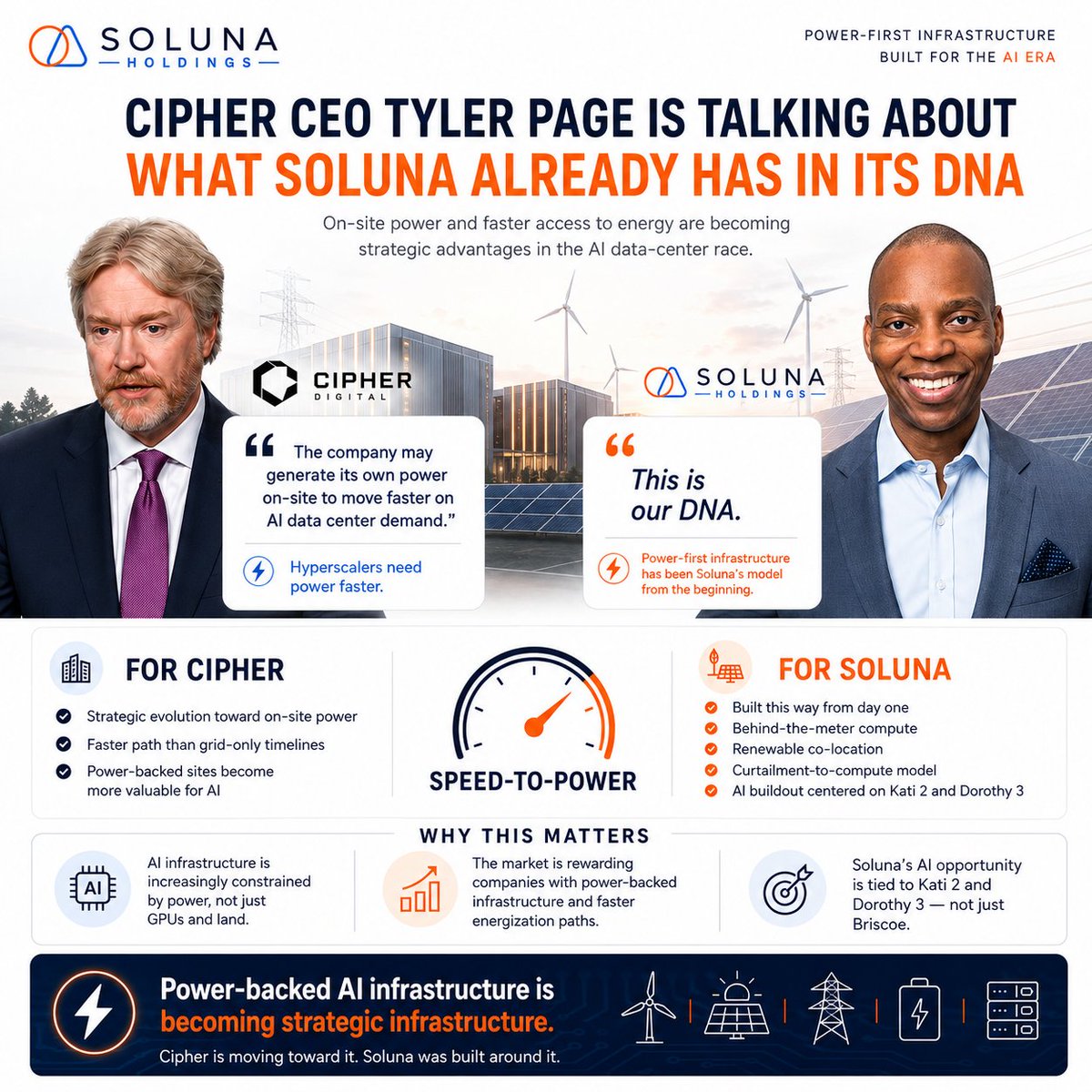

Cipher Digital’s CEO is now talking about something very important: the ability to add own/on-site power generation or secure power faster through power-backed sites.

AI infrastructure is clealy no longer only about data centers, GPUs, or land. The real bottleneck is becoming power.

Cipher is not a small example. The company has talked about a 4.2 GW data center portfolio, 600 MW of HPC facilities for hyperscaler tenants, and around 3.4 GW of pipeline. They also already have major AI/HPC exposure, including a 168 MW Fluidstack deal, where Google backstops $1.4B of Fluidstack’s obligations.

But the key difference is this:

For Cipher, this is a strategic development.

For Soluna, this has been the business model from the beginning.

Soluna was not built around the idea of “we have data centers, now let’s find power.”

Soluna was built around the opposite idea: find underutilized or wasted renewable power first, place compute next to it, and turn curtailment into revenue.

That is Soluna’s DNA.

Behind-the-meter infrastructure. Co-location next to wind and solar. Renewable compute. Monetizing energy that otherwise would have been lost.

The market is starting to value companies that can solve speed-to-power. Cipher, WULF, IREN and others have already been re-rated as investors realized the value of power-backed infrastructure.

Solunas business model is almost directly built for the exact problem the AI infrastructure market is now trying to solve.

Jun 6

$CIFR CEO Tyler Page says the company may generate its own power on-site to move faster on AI data center demand.

Hyperscalers need power faster and Cipher may be able to “tap the pipeline” instead of waiting years on the grid.

5

5

57

5,214

More info here

x.com/i/status/2054969777878…

$SLNH Soluna Holdings was featured today in Data Centre Magazine, and the message is clear: AI infrastructure is no longer just about GPUs. It is about power.

@jbelizaireCEO frames the industry’s real bottleneck directly:

“The real constraint today is energy access.”

The article highlights that US grid interconnection queues can stretch 5–7 years in many markets, meaning even well-funded AI data center projects can be delayed for years waiting for power.

That is exactly where Soluna’s model becomes interesting.

Instead of building a conventional data center and then searching for grid capacity, Soluna starts with the energy asset itself:

“Where a conventional facility begins with the building and then pursues a power connection, Soluna starts with the energy asset and constructs computing infrastructure around it.”

This is the core thesis: compute follows energy.

Soluna’s facilities are colocated with renewable generation, connected behind the meter, and designed to absorb curtailed or stranded energy that would otherwise be wasted. The article also emphasizes Soluna’s modular infrastructure, MaestroOS energy management software, and the ability to act as flexible load for the grid.

One of the strongest quotes:

“The broader point is that flexible load transforms a data centre from a fixed draw on the energy system into a grid asset.”

And the bigger strategic point:

“Operators that control their power supply will have durable advantages over those dependent on utility allocation.”

That directly connects to Soluna’s recent Briscoe Wind Farm acquisition in West Texas a clear move toward vertical integration between energy and compute.

The article’s conclusion is powerful:

“Computing will begin to follow energy rather than the other way around.”

5

500

Perspez retweeted

$SLNH is moving much faster than anticipated.

In my recent interview with the CEO, I was surprised that they may have two major AI/HPC deals already in 2026.

That'd be lightning fast in a market that's prioritizing speed to power.

We know that Kati 2 is already advancing with at least one prospective tenant and the fully integrated Dorothy 3 is coming up behind it.

These are both 300MW sites with Kati 2 in particular potentially having the ability to become a 1GW site given the surrounding energy infrastructure.

As I mentioned in the interview, this is the most excited I've been as a shareholder covering the company.

Here is a link to my recent interview with the CEO.

x.com/disruptorinvest/status…

Please do your own research when making investment decisions. This is not financial advice.

1

18

140

10,720

$SLNH

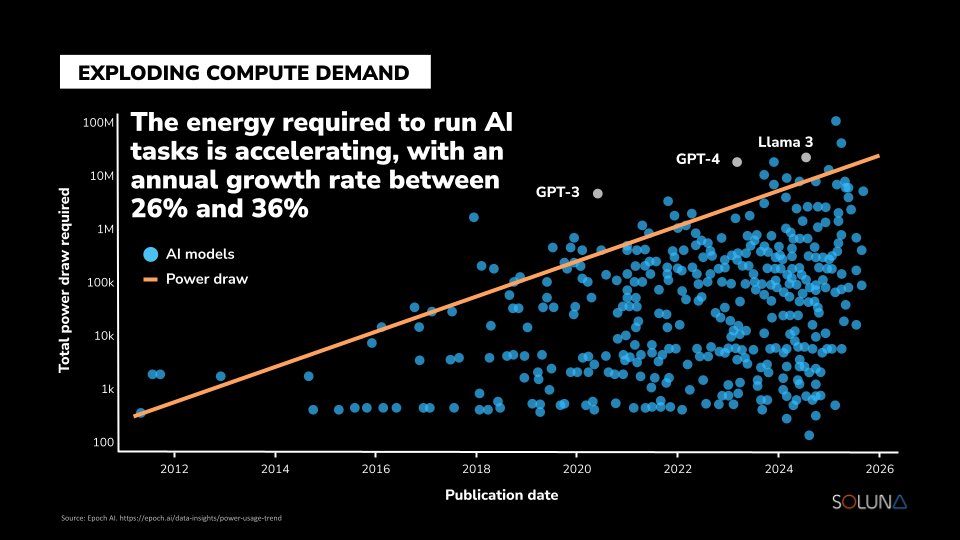

For the last two years, most of the AI conversation has been about chips.

Nvidia, GPUs, model training, inference demand, and who gets access to the next generation of compute.

But the market is slowly realizing that the next bottleneck is not only silicon.

It is power.

It is land.

It is interconnection.

It is construction speed.

It is the ability to turn electricity into usable AI infrastructure.

That is why the recent Goldman Sachs capex analysis is so important for understanding where this cycle is going.

According to Yahoo Finance, Goldman strategist Ben Snider expects the major U.S. hyperscalers: Amazon, Google/Alphabet, Meta, Microsoft and Oracle – to spend around $755B on capex in 2026, up roughly 83% year over year.

The most important part is not just the size of the number.

Goldman estimates that this level of capex would reach roughly 100% of their cash flow from operations, leaving very little room for shareholder returns without using cash balances or adding debt.

That tells you how aggressive this AI infrastructure race has become.

These companies are still generating enormous cash flow, but almost all of it is being recycled back into data centers, GPUs, networking, cooling, substations, grid access, backup power and physical infrastructure.

Goldman’s newer June update points in the same direction. Wall Street consensus is around $920B of hyperscaler capex in 2027, while Goldman sees a higher figure closer to $1.1T, with a bull case around $1.4T.

So the bigger picture is clear:

AI demand is no longer theoretical.

The problem is turning that demand into real megawatts, real data halls and real energized capacity.

And that is where Soluna becomes interesting.

Soluna is not trying to compete with Nvidia or the hyperscalers. The opportunity is more specific: power-backed AI/HPC infrastructure at sites where renewable energy, land and grid access can be converted into compute capacity.

Project Kati 2 is the clearest example. Through the Soluna/Metrobloks partnership, the project targets an initial 100 MW AI/HPC phase in South Texas, with a larger expansion path toward 300MW / 350MW scale.

Dorothy 3 adds another potential 300MW AI/HPC campus, supported by the Briscoe Wind Farm acquisition and Soluna’s strategy of vertically integrating the power layer.

This is why the Goldman data matters for $SLNH.

It shows that hyperscalers and neoclouds are not just looking for more chips. They need power-ready infrastructure that can actually be built, energized and financed.

Of course, this also makes execution more important.

When capex consumes almost all operating cash flow, customers will be selective. They will not fund every AI pipeline story. They will prioritize projects with credible power, uptime, financing, fiber, construction path and speed-to-market.

1

13

35

1,763

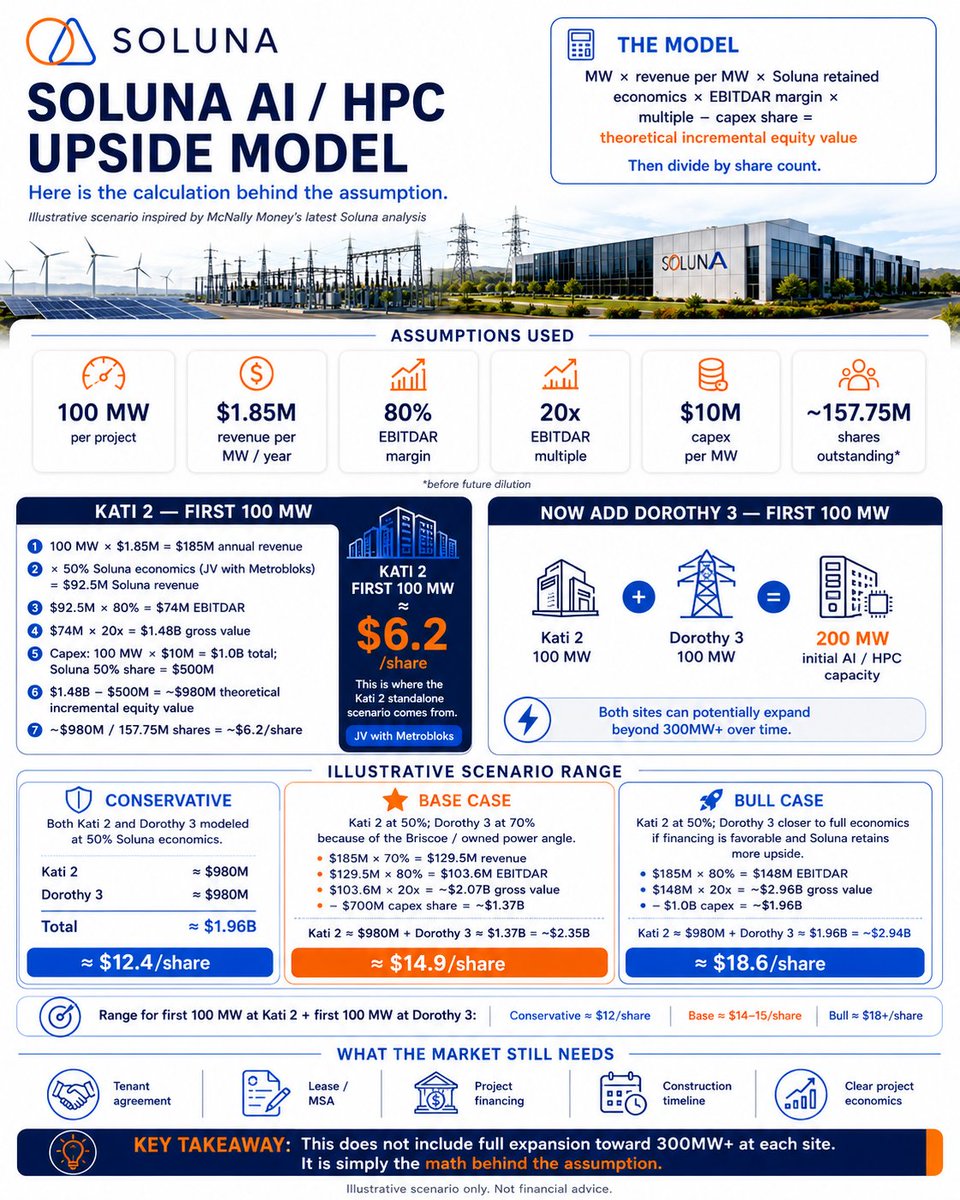

$SLNH A scenario inspired by @McnallieM latest Soluna analysis. The AI infrastructure race is no longer just about GPUs. It is becoming a race for power, grid access, land, speed-to-market and data center capacity.

Anthropic alone has announced massive infrastructure commitments, including tens of billions of dollars for U.S. data centers, multiple gigawatts of next-generation compute capacity with Google and Broadcom, and up to 5GW of additional compute through Amazon.

That tells you something important.

Frontier AI demand is growing faster than available power-ready infrastructure.

Soluna is not trying to be another generic data center developer. The company is trying to turn renewable power, constrained energy sites and behind-the-meter infrastructure into AI/HPC data center capacity.

Kati 2 alone is already meaningful. Soluna now has a definitive JV with Metrobloks, the initial design package is complete, the RFP is out for the first 100MW critical IT phase, and the company has confirmed that formal commercial negotiations have started with at least one potential tenant.

But the more interesting scenario is not just Kati 2.

It is Kati 2 first 100 MW plus Dorothy 3 first 100 MW.

That would represent 200 MW of initial AI/HPC capacity. And the key point is that both projects can potentially expand to 300MW over time. So the first 100 MW at each site is not the endgame. It is the proof point.

Using the same basic logic from McNally Money’s model, Kati 2 first 100 MW alone could represent roughly $6 per share of incremental theoretical value under their assumptions. If we then add Dorothy 3’s first 100 MW, the story becomes much more interesting.

In a conservative scenario, both projects work but Soluna has to share a large part of the economics with partners or financiers. That would mean modeling both 100 MW phases closer to 50/50 economics. Even then, the first 200 MW could represent roughly $12 per share of theoretical incremental value.

In a more realistic base case, Kati 2 should still be modeled conservatively because of the Metrobloks JV, while Dorothy 3 may allow Soluna to retain more economics because of the Briscoe/owned power angle. Under that type of scenario, the first 100 MW at Kati 2 plus the first 100 MW at Dorothy 3 could move closer to $14–15 per share of theoretical incremental value.

In a bull case, Kati 2 lands a strong tenant, financing is structured well, and Dorothy 3 follows with better retained economics for Soluna. In that case, the first 200 MW could move toward $18 per share of theoretical incremental value.

And that still only models the first 100 MW at each site.

It does not model full expansion toward 300MW at Kati 2 and Dorothy 3.

Of course, this does not mean the stock should trade there tomorrow. The market still needs proof: tenant agreement, lease/MSA, project financing, construction timeline and clear project economics.

But this is exactly why I think $SLNH is being misunderstood.

If Kati 2 lands first, Soluna can start being valued as a real AI infrastructure developer. If Dorothy 3 follows, the market may start pricing repeatability.

And if both sites eventually scale toward 300MW , then the upside case becomes much bigger than just one project.

If share count increases, the per-share value obviously comes down, but the project-level value remains the important driver.

5

10

56

5,631

Here is the calculation behind the assumption. $SLNH

The model is simple:

MW × revenue per MW × Soluna retained economics × EBITDAR margin × multiple − capex share = theoretical incremental equity value.

Then divide by share count.

Assumptions used:

100 MW per project

$1.85M revenue per MW/year

80% EBITDAR margin

20x EBITDAR multiple

$10M capex per MW

~157.75M shares outstanding before future dilution

Kati 2 first 100 MW:

100 MW × $1.85M = $185M annual revenue

Since Kati 2 is a JV with Metrobloks, I model Soluna at 50% economics:

$185M × 50% = $92.5M Soluna revenue

$92.5M × 80% = $74M EBITDAR

$74M × 20x = $1.48B gross value

Minus Soluna’s assumed capex share:

$1.0B total capex × 50% = $500M

So:

$1.48B − $500M = ~$980M theoretical incremental equity value

$980M / 157.75M shares = ~$6.2/share

That is the Kati 2 first 100 MW scenario.

Now add Dorothy 3 first 100 MW.

Conservative case:

Both Kati 2 and Dorothy 3 modeled at 50% Soluna economics.

Kati 2 = ~$980M

Dorothy 3 = ~$980M

Total = ~$1.96B

$1.96B / 157.75M shares = ~$12.4/share

Base case:

Kati 2 at 50% economics.

Dorothy 3 at 70% economics because of the Briscoe / owned power angle.

Dorothy 3 calculation:

$185M revenue × 70% = $129.5M Soluna revenue

$129.5M × 80% = $103.6M EBITDAR

$103.6M × 20x = ~$2.07B gross value

Minus $700M capex share

= ~$1.37B Dorothy 3 value

Kati 2 ~$980M Dorothy 3 ~$1.37B = ~$2.35B

$2.35B / 157.75M shares = ~$14.9/share

Bull case:

Kati 2 stays at 50% economics.

Dorothy 3 is modeled closer to full Soluna economics if financing is favorable and Soluna retains more upside.

Dorothy 3:

$185M revenue × 80% = $148M EBITDAR

$148M × 20x = ~$2.96B gross value

Minus $1.0B capex

= ~$1.96B Dorothy 3 value

Kati 2 ~$980M Dorothy 3 ~$1.96B = ~$2.94B

$2.94B / 157.75M shares = ~$18.6/share

So the illustrative range for only the first 100 MW at Kati 2 first 100 MW at Dorothy 3 becomes:

Conservative: ~$12/share

Base case: ~$14–15/share

Bull case: ~$18 /share

This does not include full expansion toward 300MW at each site.

It also does not assume the stock should trade there tomorrow.

It is simply the math behind the assumption.

The market still needs proof: tenant agreement, lease/MSA, project financing, construction timeline and clear project economics.

Illustrative scenario only. Not financial advice.

⚠️ If share count increases, the per-share value obviously comes down, but the project-level value remains the important driver

1

2

14

714

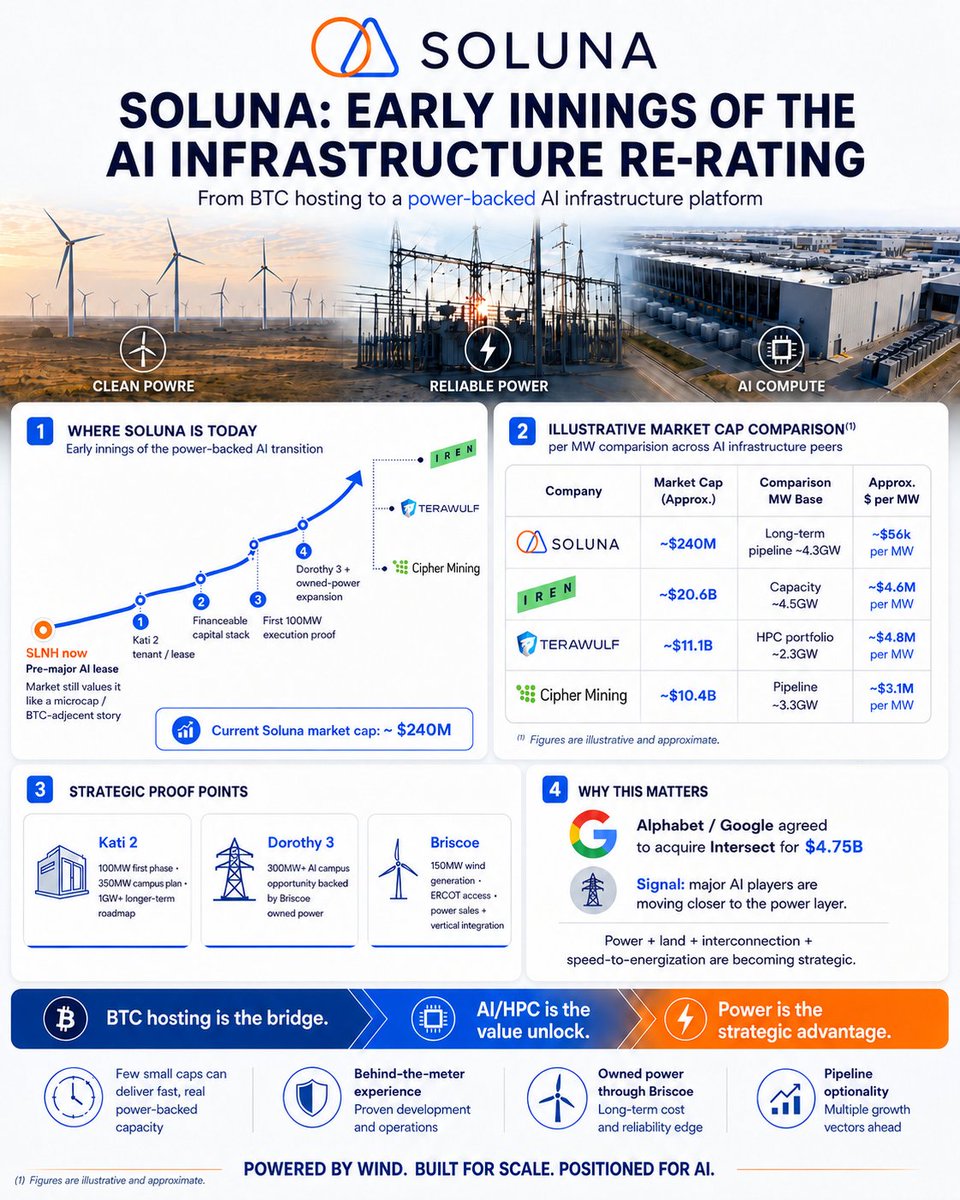

$SLNH Soluna is still in the early innings of the same transition the market has already rewarded in names like $WULF, $IREN and $CIFR.

Those companies were also once viewed mainly as Bitcoin miners.

Then the market started to reprice them when they proved something bigger:

power land interconnection data center infrastructure can become AI/HPC infrastructure.

That is the exact phase Soluna is entering now.

The difference is that $SLNH is still pre-major AI lease, while the others have already proven parts of the model through hyperscaler/neocloud/AI contracts, financing, GPUs, or contracted HPC capacity.

That is why Soluna trades like a microcap today.

But that is also why the setup is interesting.

The need for compute power is enormous, and the bottleneck is becoming more physical than digital. Chips matter, but without electricity, substations, interconnection, land, cooling and time-to-power, those chips cannot generate revenue.

That is exactly what the recent WSJ article highlighted. America’s data center buildout is falling behind schedule because of supply-chain backlogs, permitting fights and power availability. JP Morgan found that more than 60% of planned 2027 data center capacity is not yet under construction, with another 7% already delayed. WSJ also pointed out that having on-site power is becoming a strategic advantage for tech companies.

That is the market Soluna is walking into.

@Google is already moving closer to this model. Alphabet agreed to acquire Intersect for $4.75B, a company providing data center and energy infrastructure solutions. In simple terms, Google is paying billions to get closer to the power layer because AI infrastructure is becoming impossible to scale through traditional grid-dependent models alone.

Soluna is obviously not Google or Intersect.

But the direction is similar:

Power-first infrastructure.

Compute near generation.

Faster path to energization.

Less dependence on congested grid queues.

Flexible power architecture.

That is why Soluna is interesting at this stage.

A lot of players in the AI infrastructure rush are not serious. Some have land but no power. Some have a pipeline but no clear interconnection. Some have AI branding but no realistic path to energization. Some are years away from delivering real capacity.

Soluna is different because it already has operating sites, power relationships, behind-the-meter experience, Briscoe owned generation, ERCOT access, Kati 2 with Metrobloks, Dorothy 3, and a pipeline built around where power actually exists.

Rough market-cap-per-MW framework:

$IREN: ~$20.6B market cap / ~4.5GW capacity = ~$4.6M per MW.

$WULF: ~$11.1B market cap / ~2.3GW HPC portfolio = ~$4.8M per MW.

$CIFR: ~$10.4B market cap / ~3.3GW pipeline = ~$3.1M per MW.

$SLNH: ~$126M market cap / ~4.3GW long-term pipeline = ~$29k per MW.

Even if you ignore Soluna’s full 4.3GW pipeline and only look at Kati 2 Dorothy 3, the gap is still extreme.

Kati 2 has a 100MW first phase, 350MW campus plan, and a longer-term 1GW roadmap mentioned by management.

Dorothy 3 is a 300MW AI campus opportunity backed by Briscoe owned power.

Together, that is roughly 1.3GW of visible AI/HPC roadmap.

At a ~$240M market cap, that is less than ~$100k per MW.

That gap exists for a reason.

Soluna has not yet proven the AI/HPC lease model.

The market is still waiting for the first bankable tenant, the financing structure, and execution on the first 100MW.

But that is exactly the point.

Before WULF, IREN and CIFR were fully repriced, they also had to move through the same “prove it” phase.

Soluna is sitting at the stage before the market gives credit.

$SLNH The Kati 2 / Metrobloks podcast had a few underrated points that I think many people missed.

To me, the most important part was how clearly Metrobloks explained why Kati 2 can stand out in a market full of noise.

First, AI/ML is much more location agnostic than traditional cloud.

Traditional cloud data centers were built around regions, availability zones and latency requirements. AI training and large AI/ML workloads are different. They can increasingly be built where power is available.

“Instead of looking at sites, you’re now chasing power.”

Second, Kati 2 may have a faster development cycle than a normal data center project.

Metrobloks said typical physical data center development can take 36–48 months. But in Kati 2’s case, that timeline could be meaningfully shorter because of the pre-work Soluna has already done.

They bring site control, power entitlements, ERCOT access, wind energy, electrical equipment and energy development work.

In a market where AI customers need capacity in 12–24 months, that pre-work can become very valuable.

Third, Kati 2 has a geographic angle that people are not talking about enough.

A lot of Texas data center capacity is concentrated in West and Central Texas. Metrobloks pointed out that Kati 2’s Southeast / East Texas location can offer a different strategic profile.

For serious AI/HPC customers, location is not just about cheap land. It is about power availability, grid exposure, disaster recovery, fiber routes, regional diversification and avoiding too much concentration in the same “fate zone.”

They also mentioned proximity to the U.S. / Mexico corridor and connectivity tissue between the two markets.

That makes Kati 2 more interesting than just another powered land story.

Fourth, Kati 2 has “plenty of land and plenty of power.”

That matters because AI infrastructure is changing fast.

Traditional racks were often 30–40 kW.

New AI racks are already around 150 kW.

Future systems like GB300 and beyond can push 250 kW per rack, and potentially much higher over time.

If you are trying to retrofit an old data center, that is a nightmare.

Metrobloks basically said retrofitting sounds good in theory, but is extremely hard in practice.

Kati 2 can be designed AI-ready from the beginning.

Fifth, the capital discussion was important.

Metrobloks said tenant quality is what makes the infrastructure attractive.

In other words, the first Kati 2 lease is the unlock.

Customer interest → bankable lease → investor interest → capital formation.

That is why the dilution discussion is often too simplistic.

Soluna does not need to fund the whole vision upfront.

The real path is phased development, tenant-backed financing, project-level capital and infrastructure investors once the customer structure is in place.

This is why Kati 2 matters so much.

It is not only a 100MW AI/HPC campus.

It is the first real proof point.

If Soluna and Metrobloks convert Kati 2 into a bankable AI/HPC lease, it validates the bigger power-to-compute model.

Then Dorothy 3 and the 4.3GW pipeline start to matter in a completely different way.

We are still early.

3

9

77

17,616

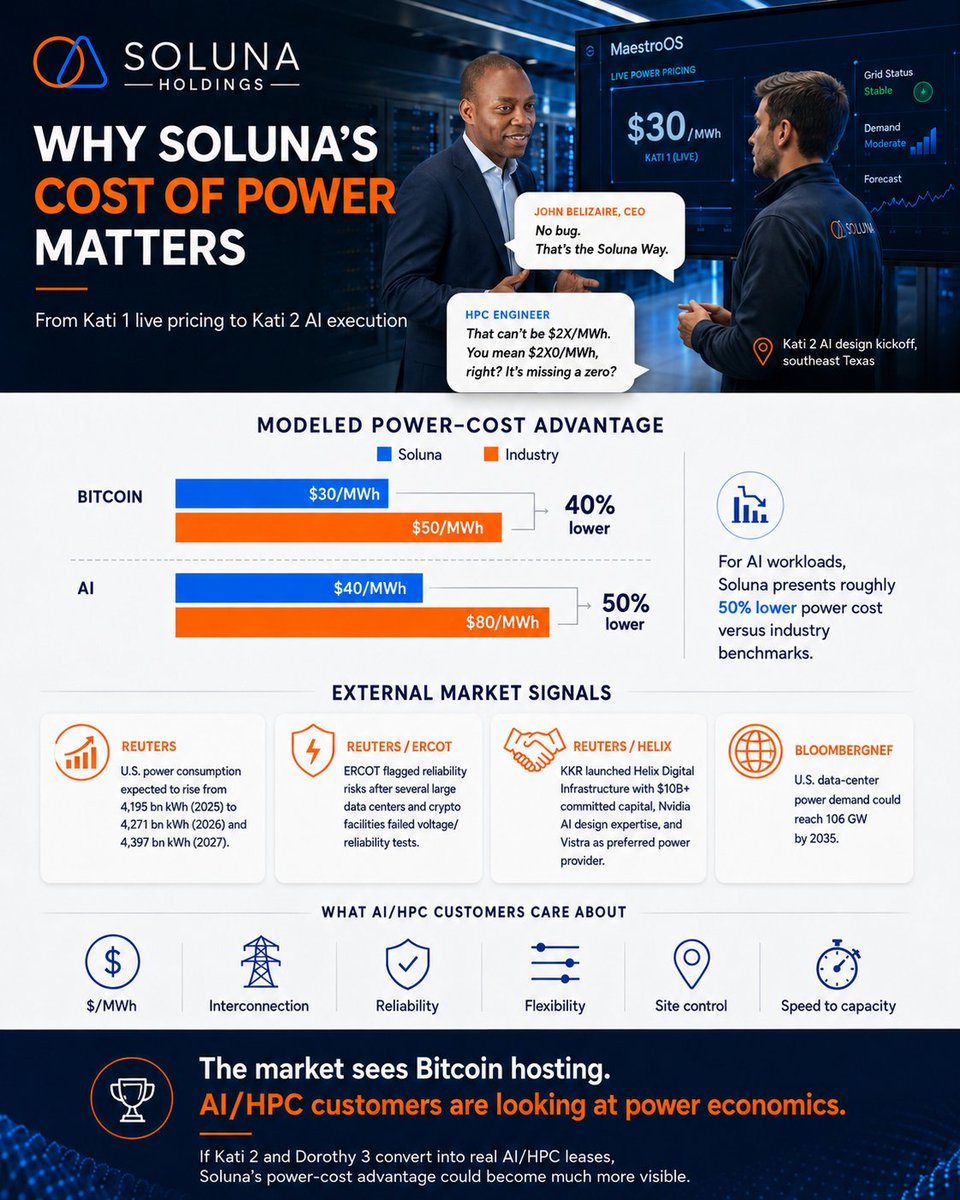

$SLNH What I like about @disruptorinvest post is that it connects directly to something @jbelizaireCEO already hinted at from the Kati 2 AI design kickoff in southeast Texas.

x.com/i/status/2052789217193…

Belizaire described how Soluna walked the HPC design team through the Kati 1 BTC control room and showed them the live all-in power price on MaestroOS. One of the HPC design engineers apparently looked at the screen and thought there had to be a mistake:

“That can’t be $2X/MWh. You mean $2X0/MWh, right? It’s missing a zero?”

That reaction says a lot.

Soluna is showing live all-in power pricing in the $20s/MWh at Kati 1. In the company’s investor material, the power-cost comparison is also very clear:

Bitcoin: $30/MWh vs $50/MWh industry

AI: $40/MWh vs $80/MWh industry

For AI workloads, that implies roughly a 50% lower power cost compared with the industry benchmark Soluna uses. In a market where power is becoming one of the hardest constraints in AI infrastructure, that kind of cost difference can matter a lot.

The external news flow keeps moving in the same direction.

Reuters recently reported that U.S. power consumption is expected to rise from 4,195 billion kWh in 2025 to 4,271 billion kWh in 2026 and 4,397 billion kWh in 2027, with AI data centers, crypto facilities and broader electrification driving demand. Reuters also noted that commercial electricity use is expected to exceed residential use for the first time on record in 2026.

Reuters also reported that ERCOT flagged reliability risks after several large data centers and crypto facilities in Texas failed voltage and reliability tests ahead of peak summer demand. That is important because the AI infrastructure race is increasingly about more than just finding megawatts. The load has to be economically attractive, technically manageable and compatible with the grid.

Then you have the KKR, Nvidia and Vistra announcement. Reuters reported that KKR launched Helix Digital Infrastructure with more than $10B in committed capital, Nvidia bringing AI data-center design expertise, and Vistra acting as the preferred power provider. That kind of structure says a lot about where the market is heading. Power is becoming part of the core AI infrastructure stack.

BloombergNEF is pointing in the same direction as well, with U.S. data-center power demand forecast to reach 106 GW by 2035. BNEF also noted that nearly a quarter of the roughly 150 new projects added to its tracker over the past year were larger than 500 MW.

That is why Soluna’s low-cost renewable compute model deserves more attention.

One major advantage $SLNH has is their cost of power.

It's projected to be roughly half the cost of peers for AI workloads.

I discussed this and many other topics in my recent interview with the CEO of $SLNH.

3

4

42

4,596

$SLNH @jbelizaireCEO of @SolunaHoldings, will be speaking at the 2026 Data Center Frontier Trends Summit on the panel:

“AI Infrastructure Investment: Bubble, Breakthrough, or Both?”

The lineup is pretty interesting.

Ryan Mallory from @flexential.

Phill Lawson-Shanks from @aligneddc.

Hunter Newby from Newby Ventures.

And John Belizaire from Soluna.

Flexential and Aligned are serious names in data center infrastructure. Hunter Newby has a long background in interconnection and carrier-neutral infrastructure. These are people connected to the exact layer of the market where AI infrastructure is running into its biggest challenges: power availability, interconnection, site readiness, cooling, construction timelines and execution.

That is what makes Soluna’s presence interesting.

Soluna is still a much smaller public company, yet Belizaire is sitting in the same discussion as established data center and infrastructure players. The topic of the panel fits Soluna’s positioning almost perfectly: capital is flowing into AI infrastructure, but the market is starting to realize that money alone does not solve the physical bottlenecks.

Power is becoming the center of the AI infrastructure conversation.

Grid access, renewable energy, flexible load, behind-the-meter structures, interconnection strategy and faster site development are moving from niche topics to boardroom-level priorities.

That is exactly where Soluna has been building its model.

Project Dorothy proved they can build and operate renewable-powered computing sites. Kati 1 pushes the platform further. Kati 2 and Dorothy 3 are where the story becomes much bigger, especially if the company can convert its pipeline into AI/HPC customer agreements.

For me, this is another sign that Soluna is gradually being viewed through a different lens.

Not only as a Bitcoin mining-related name, but as a small, energy-integrated infrastructure company positioned around one of the biggest bottlenecks in AI: power.

When a company with Soluna’s market cap starts appearing in serious infrastructure discussions next to much larger and more established players, I pay attention.

The AI buildout is turning into a power and execution race.

Soluna has been preparing for exactly that.

@SolunaHoldings $SLNH @SolunaHoldings has today released its May 2026 business update, and in my view this is one of the most important operational updates so far for the AI/HPC transition.

The key point is simple:

▪︎ Kati 2 is moving from concept toward execution.

▪︎ Soluna confirmed that the definitive JV agreement with Metrobloks has now been signed, replacing the previously announced non-binding MOU. That is a meaningful step. A non-binding MOU is one thing. A definitive JV agreement is a much stronger structure for development, leasing, capital formation and execution.

▪︎ The update also says the design team has completed the initial design package for Kati 2, and that an RFP has been launched for the design-development and construction phase for Phase I, the first 100MW Critical IT.

Here is the actual sequence before a project becomes buildable:

▪︎ JV structure.

▪︎ Initial design package.

▪︎ RFP for design-development and construction.

▪︎ Tenant diligence.

▪︎ Commercial negotiations.

▪︎ Capital raising.

▪︎ Then financing, construction and energization.

The most important sentence in the entire update is probably this:

“Tenant due diligence continues with Hyperscalers and Neoclouds. Formal commercial negotiations have started with at least one potential tenant.”

That is a big step forward. Soluna is no longer just talking about general interest. At least one potential tenant has moved into formal commercial negotiations, while diligence with hyperscalers and neoclouds remains active.

That is exactly the stage you want to see before a bankable AI/HPC lease can happen.

The financing update is also important. Soluna said it has engaged a top-tier investment bank experienced in financing AI infrastructure projects to lead capital raising for Kati 2.

That directly addresses one of the biggest questions investors have had:

How will the first 100MW be financed?

The answer appears to be moving toward a more serious AI-infrastructure capital stack, not just a simple microcap equity raise. If Kati 2 lands a bankable tenant, that can potentially support project-level financing, debt, strategic capital, tenant-backed structures and other infrastructure-style funding options.

Dorothy 3 also continues to move forward.

Soluna signed a definitive purchase agreement with a landowner for 300 acres. Environmental due diligence and survey work are underway. Fiber studies have launched. The company is coordinating with utilities to expand load and convert current BTC load toward AI.

That supports the bigger roadmap:

▪︎ Kati 2 as the first major commercial AI/HPC proof point.

▪︎ Dorothy 3 as the owned-power follow-on backed by Briscoe.

▪︎ Briscoe itself is now integrated into Soluna’s operations, and the company completed scheduled gearbox maintenance on select turbines during May. That may sound boring, but it matters. Briscoe is not just a future AI narrative. It is a real 150MW power generation asset that Soluna is now operating, maintaining and integrating into the Dorothy platform.

The Bitcoin hosting side also continues to support the transition.

Dorothy 1A returned to full capacity after transformer repair work. Dorothy 2 remained strong with all customers at full capacity. Sophie also remained strong. Kati 1 continues to progress, with Galaxy’s 48MW operations steady, K1B Phase 1 reaching substantial completion, Phase 2 achieving mechanical completion and power commissioning, and Phase 3 ongoing ahead of schedule.

That is important because BTC hosting is still the cash-flow bridge while the AI/HPC side matures.

The update also shows that Soluna is building a broader platform, not only one project. Project Grace continues with PSSE/PSCAD modeling in collaboration with Siemens PTI. Annie is being developed for a potential new customer, with capital formation and modular construction design underway. Ellen, Hedy and Rosa are moving through interconnection and transmission processes.

3

3

50

3,814

1

304

$SLNH @SolunaHoldings Following up on my earlier posts about Kati 2’s geography and power setup, Metrobloks’ own description of the site adds another layer to the story.

What stood out to me is how they frame Kati 2 from a data center developer’s perspective, not only from an energy perspective.

Soluna has already shown the power side: Las Majadas, ERCOT access, behind-the-meter renewable power, site control and the ability to build compute close to generation.

Metrobloks adds the commercial site thesis.

They describe Kati 2 as a South Texas AI-ready campus near McAllen, positioned at the U.S.–Mexico gateway, with access to major long-haul fiber routes, proximity to substations, redundant power supply, and a location outside historic flood plains.

That combination is important because hyperscalers and neoclouds evaluate much more than raw MW.

They care about where the power comes from, how fast it can be delivered, how resilient the site is, how the fiber routes look, how much expansion is possible, what regional risks exist, and whether the location gives them a differentiated footprint versus the crowded Texas clusters.

This is where the South Texas / McAllen angle becomes interesting.

A lot of Texas data center activity is concentrated around DFW, Central Texas and West Texas. Those regions are strong, but they are also increasingly competitive for power, land, interconnection, equipment, labor and timelines.

Kati 2 gives Soluna and Metrobloks a different corridor.

South Texas can offer renewable power economics, ERCOT access, major fiber routes, substation proximity, and potential cross-border relevance toward Mexico and LATAM over time.

For some AI/HPC customers, especially those thinking about regional diversification, latency, enterprise workloads or future inference distribution, that geography could become part of the commercial appeal.

$SLNH I think a lot of investors still underestimate the importance of Metrobloks in the Kati 2 setup.

Metrobloks is not just a random partner attached to the project.

According to Metrobloks, its leadership team has helped enable 12 GW of critical IT capacity, $28B in total deal value, 290 data centers developed, acquired or operated, 50 cities, 25 countries, and 100 commercial real estate transactions.

When you look at the team, the background is directly relevant to what @SolunaHoldings is trying to do with Kati 2.

Ernest Popescu, Metrobloks’ CEO, has experience from AWS, Meta/Facebook and Iron Mountain across global data center capacity planning, site development, leasing, real estate, power/interconnection, renewable energy availability and hyperscale strategy.

Scott Couzens, COO, has deep AWS experience in data center planning and analytics, including global infrastructure capacity planning.

Carl Fung, VP Data Center Solutions, brings 30 years of mission-critical infrastructure experience, including hyperscale data centers, power systems, cooling, liquid cooling and next-generation architectures, with prior experience including Equinix and Capstone Green Energy.

Hope Martin brings Microsoft site due diligence experience, including engineering assessments, infrastructure analysis and risk evaluation for global data center expansion.

Edmund Elizalde brings 40 years of data center engineering experience, including Equinix, Vantage, Goodman and EYP Mission Critical Engineering.

This is the type of team that understands how hyperscalers and neoclouds evaluate a site:

- power availability

- interconnection risk

- fiber

- cooling

- density

- cost per kW

- leasing structure

- construction schedule

- permitting

- redundancy

- speed-to-market

That is why the Soluna Metrobloks JV is important.

Soluna brings the power-first platform:

- land

- renewable power access

- behind-the-meter experience

- site control

- ERCOT / interconnection knowledge

- Kati 2 and Dorothy 3 opportunities

Metrobloks brings the hyperscale data center development layer:

- site development

- leasing

- customer requirements

- real estate execution

- capacity planning

- data center design

- engineering

- hyperscale market understanding

Kati 2 is where these two layers meet.

And now the setup is much more serious than before.

Soluna and Metrobloks have moved from a non-binding MOU to a definitive JV agreement. Kati 2 is now structured as a 350MW Critical IT development: 100MW Phase I and 250MW Phase II.

Soluna remains manager of the JV, contributes the Phase I property, has the Phase II property path, and has a waterfall structure where Soluna first receives capital recovery, a 14% IRR, and $100,000 per Gross PPA MW before additional distributions are split 50/50.

At the same time, Soluna’s May update confirmed that tenant due diligence continues with hyperscalers and neoclouds, and that formal commercial negotiations have started with at least one potential tenant.

The initial design package is complete.

The RFP for design-development and construction of Phase I, the first 100MW Critical IT, has been launched.

A top-tier investment bank experienced in AI infrastructure financing is leading capital raising for Kati 2.

To be clear, this does not mean a tenant lease has already been signed.

But I also do not think Metrobloks moves from MOU to definitive JV, Soluna launches the construction-phase RFP, tenant negotiations become formal, and an AI infrastructure investment bank gets engaged unless the project is getting much closer to a real deal.

3

36

2,913

$SLNH I think a lot of investors still underestimate the importance of Metrobloks in the Kati 2 setup.

Metrobloks is not just a random partner attached to the project.

According to Metrobloks, its leadership team has helped enable 12 GW of critical IT capacity, $28B in total deal value, 290 data centers developed, acquired or operated, 50 cities, 25 countries, and 100 commercial real estate transactions.

When you look at the team, the background is directly relevant to what @SolunaHoldings is trying to do with Kati 2.

Ernest Popescu, Metrobloks’ CEO, has experience from AWS, Meta/Facebook and Iron Mountain across global data center capacity planning, site development, leasing, real estate, power/interconnection, renewable energy availability and hyperscale strategy.

Scott Couzens, COO, has deep AWS experience in data center planning and analytics, including global infrastructure capacity planning.

Carl Fung, VP Data Center Solutions, brings 30 years of mission-critical infrastructure experience, including hyperscale data centers, power systems, cooling, liquid cooling and next-generation architectures, with prior experience including Equinix and Capstone Green Energy.

Hope Martin brings Microsoft site due diligence experience, including engineering assessments, infrastructure analysis and risk evaluation for global data center expansion.

Edmund Elizalde brings 40 years of data center engineering experience, including Equinix, Vantage, Goodman and EYP Mission Critical Engineering.

This is the type of team that understands how hyperscalers and neoclouds evaluate a site:

- power availability

- interconnection risk

- fiber

- cooling

- density

- cost per kW

- leasing structure

- construction schedule

- permitting

- redundancy

- speed-to-market

That is why the Soluna Metrobloks JV is important.

Soluna brings the power-first platform:

- land

- renewable power access

- behind-the-meter experience

- site control

- ERCOT / interconnection knowledge

- Kati 2 and Dorothy 3 opportunities

Metrobloks brings the hyperscale data center development layer:

- site development

- leasing

- customer requirements

- real estate execution

- capacity planning

- data center design

- engineering

- hyperscale market understanding

Kati 2 is where these two layers meet.

And now the setup is much more serious than before.

Soluna and Metrobloks have moved from a non-binding MOU to a definitive JV agreement. Kati 2 is now structured as a 350MW Critical IT development: 100MW Phase I and 250MW Phase II.

Soluna remains manager of the JV, contributes the Phase I property, has the Phase II property path, and has a waterfall structure where Soluna first receives capital recovery, a 14% IRR, and $100,000 per Gross PPA MW before additional distributions are split 50/50.

At the same time, Soluna’s May update confirmed that tenant due diligence continues with hyperscalers and neoclouds, and that formal commercial negotiations have started with at least one potential tenant.

The initial design package is complete.

The RFP for design-development and construction of Phase I, the first 100MW Critical IT, has been launched.

A top-tier investment bank experienced in AI infrastructure financing is leading capital raising for Kati 2.

To be clear, this does not mean a tenant lease has already been signed.

But I also do not think Metrobloks moves from MOU to definitive JV, Soluna launches the construction-phase RFP, tenant negotiations become formal, and an AI infrastructure investment bank gets engaged unless the project is getting much closer to a real deal.

@SolunaHoldings $SLNH @SolunaHoldings has today released its May 2026 business update, and in my view this is one of the most important operational updates so far for the AI/HPC transition.

The key point is simple:

▪︎ Kati 2 is moving from concept toward execution.

▪︎ Soluna confirmed that the definitive JV agreement with Metrobloks has now been signed, replacing the previously announced non-binding MOU. That is a meaningful step. A non-binding MOU is one thing. A definitive JV agreement is a much stronger structure for development, leasing, capital formation and execution.

▪︎ The update also says the design team has completed the initial design package for Kati 2, and that an RFP has been launched for the design-development and construction phase for Phase I, the first 100MW Critical IT.

Here is the actual sequence before a project becomes buildable:

▪︎ JV structure.

▪︎ Initial design package.

▪︎ RFP for design-development and construction.

▪︎ Tenant diligence.

▪︎ Commercial negotiations.

▪︎ Capital raising.

▪︎ Then financing, construction and energization.

The most important sentence in the entire update is probably this:

“Tenant due diligence continues with Hyperscalers and Neoclouds. Formal commercial negotiations have started with at least one potential tenant.”

That is a big step forward. Soluna is no longer just talking about general interest. At least one potential tenant has moved into formal commercial negotiations, while diligence with hyperscalers and neoclouds remains active.

That is exactly the stage you want to see before a bankable AI/HPC lease can happen.

The financing update is also important. Soluna said it has engaged a top-tier investment bank experienced in financing AI infrastructure projects to lead capital raising for Kati 2.

That directly addresses one of the biggest questions investors have had:

How will the first 100MW be financed?

The answer appears to be moving toward a more serious AI-infrastructure capital stack, not just a simple microcap equity raise. If Kati 2 lands a bankable tenant, that can potentially support project-level financing, debt, strategic capital, tenant-backed structures and other infrastructure-style funding options.

Dorothy 3 also continues to move forward.

Soluna signed a definitive purchase agreement with a landowner for 300 acres. Environmental due diligence and survey work are underway. Fiber studies have launched. The company is coordinating with utilities to expand load and convert current BTC load toward AI.

That supports the bigger roadmap:

▪︎ Kati 2 as the first major commercial AI/HPC proof point.

▪︎ Dorothy 3 as the owned-power follow-on backed by Briscoe.

▪︎ Briscoe itself is now integrated into Soluna’s operations, and the company completed scheduled gearbox maintenance on select turbines during May. That may sound boring, but it matters. Briscoe is not just a future AI narrative. It is a real 150MW power generation asset that Soluna is now operating, maintaining and integrating into the Dorothy platform.

The Bitcoin hosting side also continues to support the transition.

Dorothy 1A returned to full capacity after transformer repair work. Dorothy 2 remained strong with all customers at full capacity. Sophie also remained strong. Kati 1 continues to progress, with Galaxy’s 48MW operations steady, K1B Phase 1 reaching substantial completion, Phase 2 achieving mechanical completion and power commissioning, and Phase 3 ongoing ahead of schedule.

That is important because BTC hosting is still the cash-flow bridge while the AI/HPC side matures.

The update also shows that Soluna is building a broader platform, not only one project. Project Grace continues with PSSE/PSCAD modeling in collaboration with Siemens PTI. Annie is being developed for a potential new customer, with capital formation and modular construction design underway. Ellen, Hedy and Rosa are moving through interconnection and transmission processes.

1

7

63

7,291

@SolunaHoldings $SLNH @SolunaHoldings has today released its May 2026 business update, and in my view this is one of the most important operational updates so far for the AI/HPC transition.

The key point is simple:

▪︎ Kati 2 is moving from concept toward execution.

▪︎ Soluna confirmed that the definitive JV agreement with Metrobloks has now been signed, replacing the previously announced non-binding MOU. That is a meaningful step. A non-binding MOU is one thing. A definitive JV agreement is a much stronger structure for development, leasing, capital formation and execution.

▪︎ The update also says the design team has completed the initial design package for Kati 2, and that an RFP has been launched for the design-development and construction phase for Phase I, the first 100MW Critical IT.

Here is the actual sequence before a project becomes buildable:

▪︎ JV structure.

▪︎ Initial design package.

▪︎ RFP for design-development and construction.

▪︎ Tenant diligence.

▪︎ Commercial negotiations.

▪︎ Capital raising.

▪︎ Then financing, construction and energization.

The most important sentence in the entire update is probably this:

“Tenant due diligence continues with Hyperscalers and Neoclouds. Formal commercial negotiations have started with at least one potential tenant.”

That is a big step forward. Soluna is no longer just talking about general interest. At least one potential tenant has moved into formal commercial negotiations, while diligence with hyperscalers and neoclouds remains active.

That is exactly the stage you want to see before a bankable AI/HPC lease can happen.

The financing update is also important. Soluna said it has engaged a top-tier investment bank experienced in financing AI infrastructure projects to lead capital raising for Kati 2.

That directly addresses one of the biggest questions investors have had:

How will the first 100MW be financed?

The answer appears to be moving toward a more serious AI-infrastructure capital stack, not just a simple microcap equity raise. If Kati 2 lands a bankable tenant, that can potentially support project-level financing, debt, strategic capital, tenant-backed structures and other infrastructure-style funding options.

Dorothy 3 also continues to move forward.

Soluna signed a definitive purchase agreement with a landowner for 300 acres. Environmental due diligence and survey work are underway. Fiber studies have launched. The company is coordinating with utilities to expand load and convert current BTC load toward AI.

That supports the bigger roadmap:

▪︎ Kati 2 as the first major commercial AI/HPC proof point.

▪︎ Dorothy 3 as the owned-power follow-on backed by Briscoe.

▪︎ Briscoe itself is now integrated into Soluna’s operations, and the company completed scheduled gearbox maintenance on select turbines during May. That may sound boring, but it matters. Briscoe is not just a future AI narrative. It is a real 150MW power generation asset that Soluna is now operating, maintaining and integrating into the Dorothy platform.

The Bitcoin hosting side also continues to support the transition.

Dorothy 1A returned to full capacity after transformer repair work. Dorothy 2 remained strong with all customers at full capacity. Sophie also remained strong. Kati 1 continues to progress, with Galaxy’s 48MW operations steady, K1B Phase 1 reaching substantial completion, Phase 2 achieving mechanical completion and power commissioning, and Phase 3 ongoing ahead of schedule.

That is important because BTC hosting is still the cash-flow bridge while the AI/HPC side matures.

The update also shows that Soluna is building a broader platform, not only one project. Project Grace continues with PSSE/PSCAD modeling in collaboration with Siemens PTI. Annie is being developed for a potential new customer, with capital formation and modular construction design underway. Ellen, Hedy and Rosa are moving through interconnection and transmission processes.

5

4

32

9,128

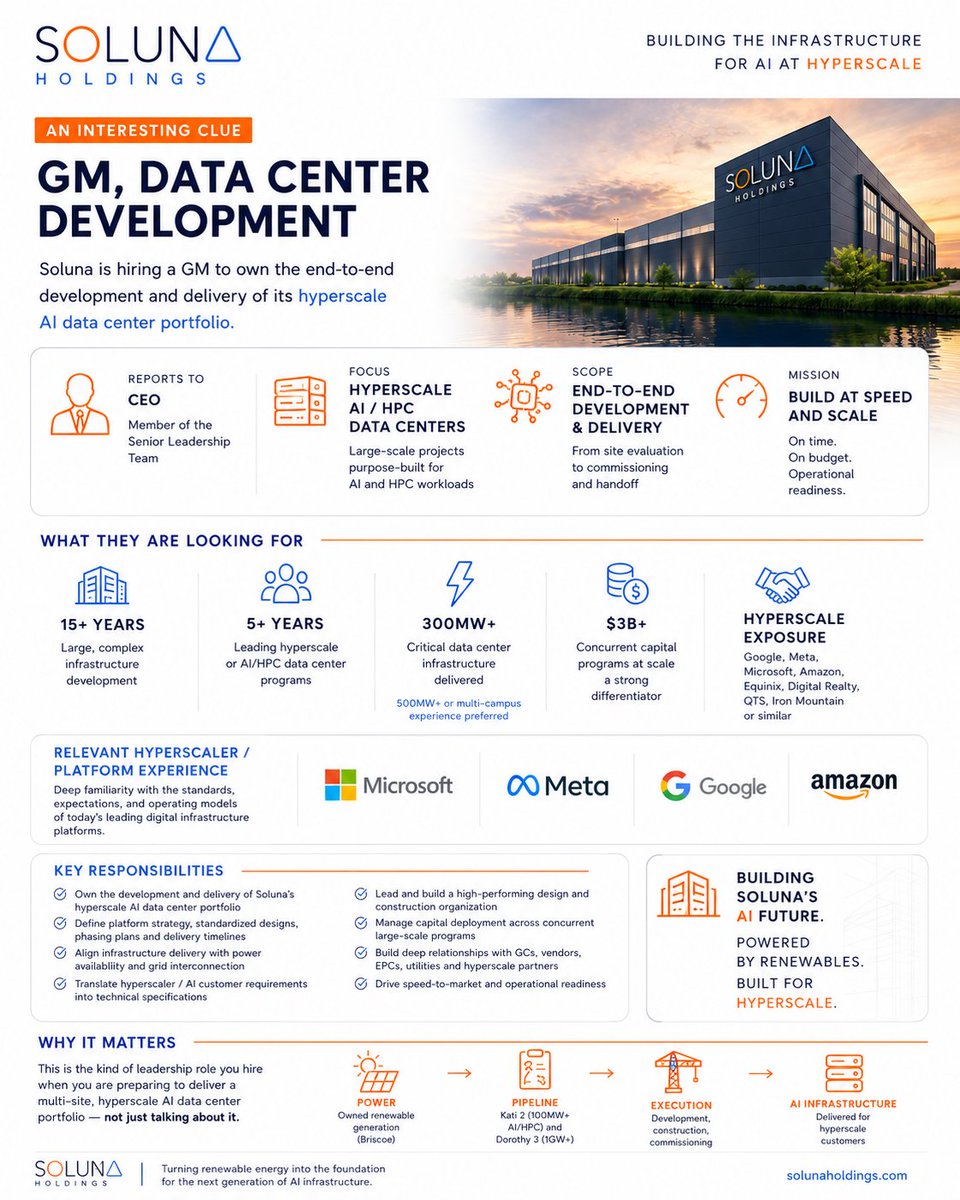

$SLNH One interesting clue in @SolunaHoldings transition is the GM, Data Center Development role on their own careers page.

ats.rippling.com/fr-FR/solun…

The role is described as owning the end-to-end development and delivery of Soluna’s “hyperscale AI data center portfolio.” It reports directly to the CEO and is responsible for large-scale data center projects purpose-built for AI and HPC workloads.

They are not talking about a small container site. They are looking for someone who can define and execute a data center platform strategy, build standardized design frameworks, manage phasing plans, coordinate vendors, align infrastructure delivery with power availability, and translate hyperscaler / AI customer requirements into technical specifications.

The required experience is also very specific: 15 years in large infrastructure development, 5 years leading hyperscale or AI/HPC data center programs, delivery of 300MW of critical data center infrastructure, preferably 500MW or multi-campus experience, and backgrounds from places like Google, Meta, Microsoft, Amazon, Equinix, Digital Realty, QTS or Iron Mountain.

That tells me Soluna is preparing for a very different scale than the old BTC-hosting story.

The wording lines up with everything management has been discussing around Kati 2 and Dorothy 3: hyperscale AI demand, basis of design, speed-to-market, power interconnection, capital deployment, construction, commissioning and multi-site expansion.

For me, this supports the idea that Soluna is not just talking about AI/HPC.

They are building the leadership layer needed to execute it.

Kati 2 is the first commercial test.

Dorothy 3 is the owned-power follow-on.

And this GM role looks like the kind of hire you need when the company is moving from pipeline to real hyperscale AI infrastructure.

41

1,796

$SLNH This is where the valuation disconnect becomes interesting.

Soluna is still valued around ~$200M, while the company is moving into an AI/HPC infrastructure market where contracted capacity can be worth billions over time.

$APDL Applied Digital is a good example of what the sector is starting to price once MW move from “pipeline” to contracted AI/HPC capacity. Their 210MW hyperscaler lease represents around $5.2B in base-term contracted revenue over 15 years. That equals roughly $24.8M of contracted base revenue per MW.

If Soluna lands the first 100MW phase at Kati 2, that same revenue intensity would imply around $2.48B of potential base-term contracted revenue over the lease period.

100MW × ~$24.8M/MW = ~$2.48B.

That alone shows why the first Kati 2 lease matters so much. At a ~$200M market cap, one serious 100MW AI/HPC lease could completely change how the market views Soluna.

But Kati 2 is not only 100MW. The first phase is the proof point. The broader campus plan is 350MW, and management has discussed a longer-term 1GW roadmap.

Using the same rough framework, 350MW would represent about $8.7B of potential base-term contracted revenue.

350MW × ~$24.8M/MW = ~$8.68B.

A 1GW roadmap would obviously be much larger.

Then comes Dorothy 3.

Dorothy 3 is important because it can be the follow-on proof that Soluna’s model is repeatable, especially where Soluna owns the power layer through Briscoe. John has discussed a first AI footprint around 100MW, with the broader Dorothy 3 opportunity at 300MW .

If Dorothy 3 starts with 100MW, the same rough framework would imply another ~$2.48B of potential base-term contracted revenue.

100MW × ~$24.8M/MW = ~$2.48B.

If Dorothy 3 scales toward 300MW , that framework would imply roughly $7.4B .

300MW × ~$24.8M/MW = ~$7.44B.

So the real roadmap is not just “Kati 2 first 100MW.”

It could be:

Kati 2 first 100MW as the commercial proof point.

Kati 2 350MW as the campus expansion case.

Kati 2 1GW as the long-term roadmap.

Dorothy 3 first 100MW as the repeatability proof point.

Dorothy 3 300MW as the owned-power AI campus opportunity.

This is why I think the market is missing the scale of the setup.

Soluna is still being priced like a small BTC-linked company, but the assets they are convertingare power-backed AI infrastructure assets.

Jun 8

$APLD signed a 15-year AI data center lease with a U.S. hyperscaler for 210MW at Delta Forge 2 adding ~$5.2B of contracted revenue.

Applied Digital now has ~$36B contracted across five AI Factory campuses with 1.4GW of contracted IT load and 2.15GW of utility power.

6

10

102

9,922

Wait $CIFR did a 75MW deal with AWS for $2 billion and $SLNH is currently advertising for 100 MW available now at Kati 2 and is trading at a $200 million market cap ?

Jun 8

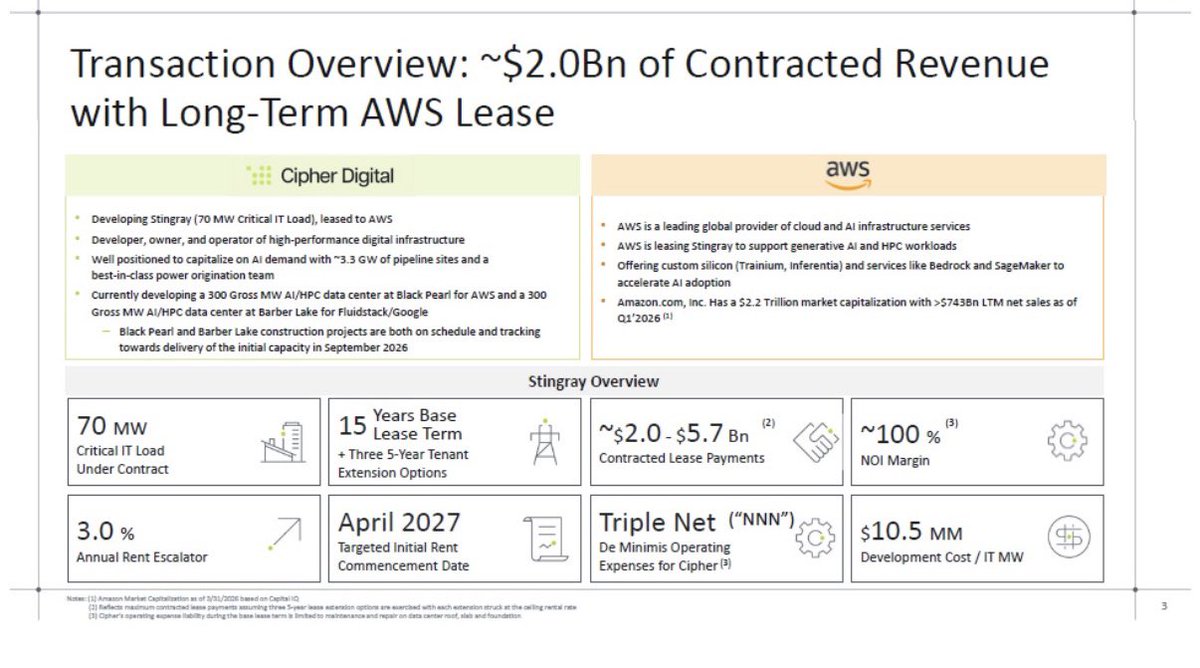

$CIFR Cipher revealed $AMZN AWS as the tenant behind its Stingray data center project

The deal includes a 15-year triple-net lease, nearly 100% NOI margins, and $2 billion in contracted payments

These are some of the strongest AI data center economics we’ve seen disclosed

12

16

162

39,152

Perspez retweeted

Jun 8

What happens when you have the capital for AI but not the ability to deploy it? That is where the industry finds itself.

60% of data-center capacity planned for completion in 2027 is still under construction, and according to a JPMorgan analysis, most delays are power-related.

This isn’t a tech problem; this is an infrastructure problem.

The solution is co-location and behind-the-meter design, not waiting in the interconnection queue.

$SLNH

(Source: WSJ "America’s Data-Center Build-Out Is Falling Way Behind Schedule")

19

20

123

11,465