Helping small business owners buy or sell | Simple steps for planning & prep | Better deals, less stress

Joined March 2011

- Tweets 820

- Following 57

- Followers 88

- Likes 918

19 Photos and videos

Pinned Tweet

1 Dec 2025

Super exciting news!

We've launched a podcast!

Deal-Ready is now live on YouTube!

Deal-Ready is a podcast for small business owners to help them plan and prepare for M&A deals. Check it out at youtu.be/ZC5lSX_CkYs?si=JNaU…

We've posted 2 videos - a short introductory clip giving some background on Deal-Ready, and the first "official" episode - What Does it Mean to be Deal-Ready?

We'll be adding new episodes in the coming weeks, and expect to bring on guests to share their M&A stories to help you get ready for your own process.

Like, comment, share, make suggestions for future episodes. Get in touch with ideas, guests we should meet, feedback or to hear more about how Amplify can help you.

Thanks (in advance) for watching!

1

1

9

612

If you didn't already see the Curacao / Germany World Cup result from Sunday, you might want to stop reading now.

Curacao playing in their first World Cup match. Germany? Its 113th. 4 titles to go along with that. Second only to Brazil.

For those that didn't watch the game, Curacao scored first.

It got a little lopsided after that.

And you know what this means in an M&A context.

Your buyer has done it 113 times. Won the trophy 4 times. They've got experience, preparation, planning, teamwork. And so do their lawyers, accountants, tax experts, HR consultants, lenders.

You might score a goal. Maybe 2.

But if you want a chance at the result you want, you can't plan to do it alone. You need the right team. And you need to plan and prepare like you're stepping on to the World Cup pitch for the first time.

And the spoiler?

7-1 Germany. (Kinda looked like my tennis match from last night. I think I need a little more practice...)

43

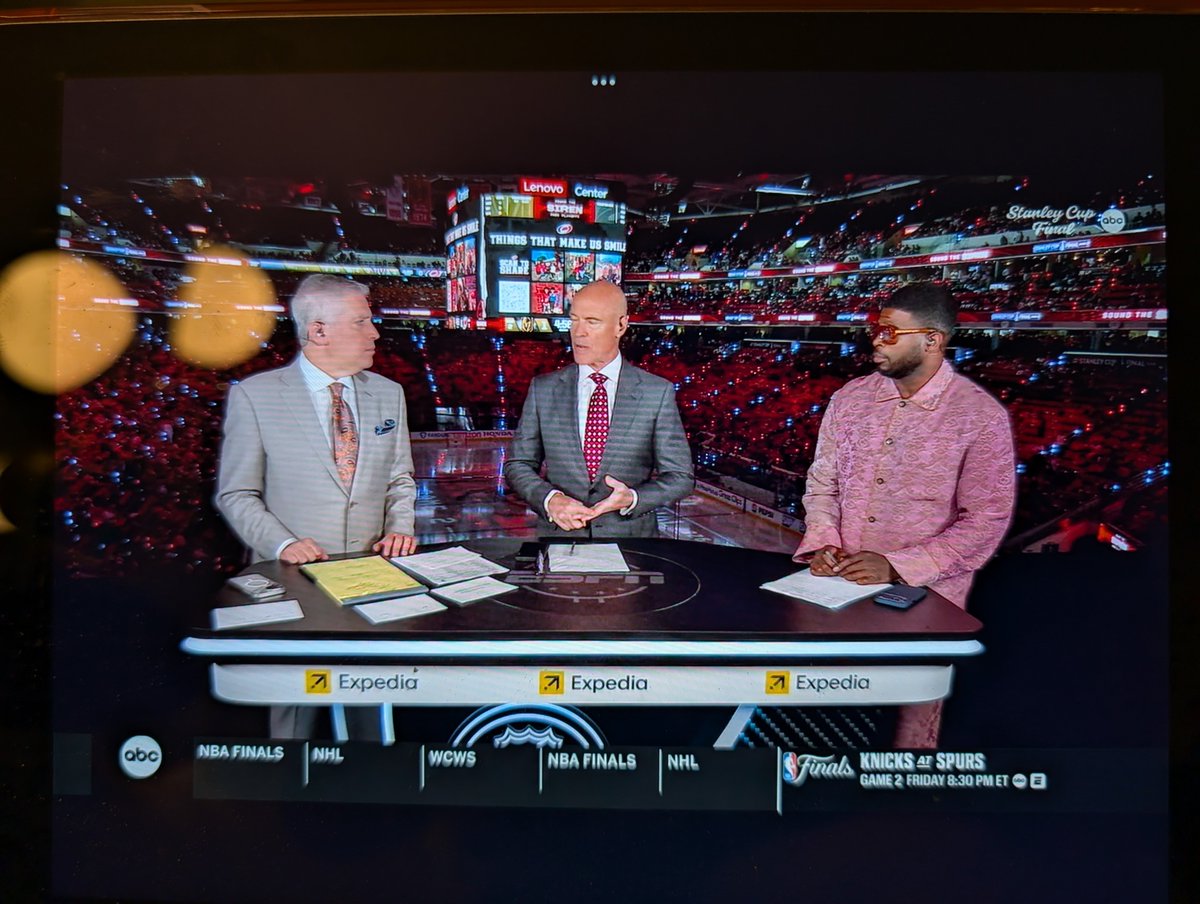

Last night the Carolina Hurricanes won the Stanley Cup (congrats to the champs!).

Arguably the hardest trophy to win in professional sports. I'm not going to disagree with that.

And if you know me, you know despite my team affiliation, I'm very frequently wearing a Carolina Hurricanes hat. Their old logo.

The season's over. But it's right back to work for Carolina and every other team. They're already planning and preparing for next season. Roster moves. New coaches. Prepping for the draft.

And that's the point every small business owner should be thinking about. The season's over. But the work has just begun.

And if you want to sell your business, it's the same situation for you. The work is just beginning. Whether it's your preseason or 20 games into the schedule.

You want to win the Cup? Work for it. Get Deal-Ready.

And add to your coaching staff if you need support getting through training camp.

1

43

There's nothing I hate in small business M&A more than the self-inflicted wound.

You know. Avoidable deal-killers. Costly. Painful. Frustrating.

There are a lot of them. But my three least favorite?

1. Sharing financial info that isn't ready.

2. Hiring advisors with no direct M&A experience.

3. Mistaking the offer for the cash at closing.

Who's with me? Who has something they hate more than these 3?

19

I'm not a basketball fan.

I help small business owners plan and prepare for M&A deals.

There's a LOT to do.

A lot of the time, the deal doesn't close.

Often it's like having a 29-point lead and still losing the game. Don't celebrate before the final horn sounds.

2

67

40 years ago Diego Maradona sent Argentina past England in the World Cup Quarterfinals with perhaps the most legendary handball of all time.

Who knows what we'll see this year. But it's likely replay would catch that today.

And if you're a small business owner, you can't expect to rely on The Hand of God to get you the deal you want.

Only planning, preparation and solid execution can guarantee that.

Go Team USA!

23

As you start thinking about selling your business, it's natural to think about all the questions you're going to have to answer.

But there is really only one that you need to be thinking about:

Will it survive scrutiny?

A buyer won't stop at the documents you provide. They're going to read them. Study them. Analyze them. Ask questions about them.

A lot of questions.

And so will their advisors, and their lenders.

It's not personal. It's business. And in M&A, it's typical.

A good buyer, a sophisticated buyer, isn't just asking questions because they're curious. Ok, sure, yes, there are absolutely going to be things they are genuinely curious about.

But more than that, they're protecting the money.

Their money.

Their partners' money.

Their lenders' money.

So you better believe there's gonna be scrutiny.

How will you deal with it?

• Option A: Anticipate the questions, prepare the narrative, organize the supporting materials, and get ready for the discussion.

• Option B: Take it as it comes. Do your best, even though you haven't really prepared. Hope it isn't too bad. Hope you get through it.

One path keeps the ball rolling, builds momentum, and makes progress towards a deal.

The other? Well, I suppose that's a question.

When you're ready to get deal-ready, let's talk. DM in confidence.

2

2

34

The problem with the due diligence process is that it tends to find things.

Things that you as the business owner might find surprising.

They often fall into 1 of 2 categories:

1). Things you should have known about.

2). Things you've ignored for far too long.

1

43

Did someone tell PK it was pajama day at school?

Go whalers (Canes)!

41

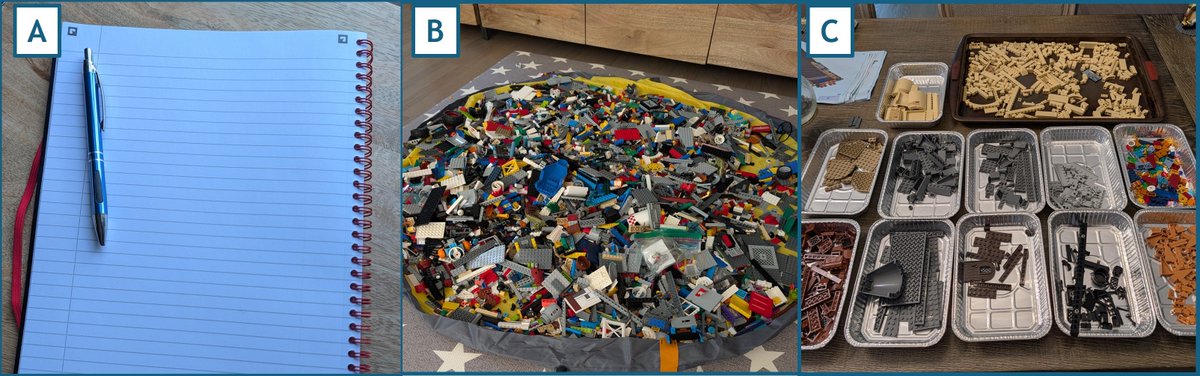

If your data room looks like A or B, it's time for us to talk.

If it looks like C, once you stop patting yourself on the back, it's time to talk.

10

When a buyer reaches out, there are only 4 possible outcomes.

Only 1 of them lets you pass GO and collect $200. (Hopefully more, actually.)

1). You answer the call, and you're ready for the conversation.

2). You answer the call, and you're not prepared.

3). You don't answer the call, and you're prepared.

4). You don't answer the call, and you're not prepared.

Which one describes your current situation?

If it's not 1, then it's time to get started. It's never too early. But it can get late quickly.

And if it's 2, 3 or 4, or you're not sure, DM (or comment) if you want to stress-test your readiness. Let's get you Deal-Ready.

20

When a buyer reaches out, there are only 4 possible outcomes.

Only 1 of them lets you pass GO and collect $200. (Hopefully more, actually.)

1). You answer the call, and you're ready for the conversation.

You know your numbers. Your data room is organized. Your positioning is tight. You're the one holding the dice.

2). You answer the call, and you're not prepared.

You're winging it. Maybe taking a long time to respond to basic due diligence questions. Maybe sharing information too early. Overplaying your hand.

3). You don't answer the call, and you're prepared.

Maybe you're waiting for the right moment. Maybe you're hoping for a better partner. Selectivity may not be a bad quality. Trying to improve your odds.

4). You don't answer the call, and you're not prepared.

You know your house isn't in order. And you know you need to change that. But in the meantime, opportunities may be passing you by.

Which one describes your current situation?

If it's not #1, then it's time to get started. It's never too early. But it can get late quickly.

And if it's not #1, or you're not sure, DM (or comment) if you want to stress-test your readiness. Let's get you Deal-Ready.

2

18

For my birthday this weekend my 6-year old daughter bought me some chocolates (she's asked me to share). She took me to the movies (we saw what she wanted to see). We went for ice cream (she got sprinkles and gummy bears on hers).

10/10 would change nothing.

2

33

Yesterday we celebrated Memorial Day here in the US.

The "unofficial start to summer."

But if you're thinking about selling your business, there's no rest for the weary.

Getting ready to sell your business (let alone actually trying to) is a full-time commitment.

And you probably already have a full-time commitment, right?

Sounds like a busy summer.

If an exit is on the radar, later this year, next year, or later than that, now is not the time to ease up.

M&A isn't a day at the beach.

And buyers...serious buyers, of course...aren't waiting while you shake the sand off your financial model.

Enjoy the summer. Nothing wrong with that. But the buyers are busy and they aren't taking Summer Fridays.

Which is why it's a great time to get some help planning and preparing. It's going to take time and effort right when you're trying to enjoy your summer, official or unofficial. And the choice to be Deal-Ready doesn't have to be binary.

If the right buyer reaches out, do you really want to tell them you'll call them when you get back from the beach?

1

1

28

Data room. Buyer list. Financials. Tax returns. Forecast model. Customer analyses. Employee details. Partner information. Supplier contracts. Customer contracts. Service provider contracts.

I should keep going but I'm getting tired just typing that out. You probably are too.

If you're a small business owner, you either know you need this stuff (plus a LOT more), or you have a sneaking suspicion it's a long list.

On the brink of this holiday weekend here in the US, I'd just like to offer some brief words of encouragement, advice if you will.

Don't let the length of the to-do list stop you from getting started.

Every bit of planning and preparation you do will help you be deal-ready when it's time.

• Smoother process.

• More thoughtful conversations.

• A running start at the beginning of the transaction marathon.

You don't have to tackle the whole mountain today. Just start, one step at a time.

• One document

• One file

• One folder

Enjoy the long weekend. Barbecue. Hang out with your family and friends. Watch the NHL playoffs. Unplug.

And when you're back?

You run your business. I'll help your business get Deal-Ready.

DM in confidence.

28

"I'm not ready to sell, why do I need a data room now?"

That's exactly the point.

You're not ready to sell. Even if you want to.

The best deals happen when everyone is ready before the conversation even starts.

Deal-ready.

1

1

30

Had a colonoscopy this morning.

The prep sucked. The procedure thankfully was not terribly memorable.

But I missed a golden opportunity to tell my 6 year-old my favorite dad joke (again. She's heard it a million times).

How do you know your booty's broken? It has a crack.

41

417 questions.

For a company with less than $15 million in revenue.

That's how many questions the buyer had for a small business owner I recently worked with.

And that doesn't even count the external advisors. Legal, HR, Accounting/Finance, QofE...

Don't even ask me how many were labeled "critical" or "high-priority." You don't want to know.

Sure, over 30 of the questions were duplicates (and that's frustrating in its own right). But a mountain of 387 questions (give or take) is still brutal.

And the business owner was, to put it politely, a bit overwhelmed. Maybe rightfully so. Maybe not.

This could have ended badly.

But the business owner had an ace in the hole. We had been working together for some time to be ready for exactly this situation. By the time we got the (first) long list, we had:

• Built a well-populated data room

• Put together trend analyses and compiled detailed performance data

• Gathered, organized, summarized (and labeled) every contract (and drafted a few to close gaps)

And a lot more data and documents.

It took time, for sure. And it's hard to quantify exactly how much time we saved. But over dinner a few weeks ago, the business owner told me that if he had gotten that 417-question list with no prep work done, he would have walked.

The buyer would have too.

You can't get the deal you want, the deal you deserve, if you can't even have the conversation.

If you want the buyer engaged, and if you want your own sanity during the process, you need to do the work before it's time to go to work.

1

1

50

I spoke with a small business owner last week who got 30 calls so far in May from potential buyers.

30 unsolicited calls. People and businesses he'd never met, never spoken with before.

Let's do a little quick math. We're just a little more than halfway through the month as I type this.

That means he got 2-3 inquiries PER DAY.

I've heard bigger numbers. I've heard smaller ones too.

But there's no doubt there is a maelstrom of activity everywhere you look.

And if you're a small business owner, there's probably going to come a time when you answer the call and agree to sit down, to discuss the possibility.

That's where the maelstrom becomes a Category 5.

No matter who the buyer is, they're heavily incentivized to do their homework as quickly as possible.

• If there's no deal to be done, move on to the next.

• If the financial story doesn't look good, move on to the next.

• If there are critical due diligence issues that can't be resolved, move on to the next.

And if they can't get answers quickly? Move on to the next.

A lot of people talk about the Silver Tsunami as if it's mackerel in the proverbial barrel. But it's a very crowded buyer landscape too.

Serious buyers know it's not just finding a good deal. It's also finding a good deal that they can win.

That's the tricky part. You get 30 calls before May 18th but if you're not ready for a full-speed sprint, that interest may not last.

Which is why I work with business owners to get to "First-Call Readiness." When the right buyer calls, with the right potential deal, you are ready for that sprint.

It's up to you to decide when it's time to answer the call. But if you answer, you need to be ready.

1

20

What's my business worth?

Before you go spend thousands of dollars on the report from that consultant to tell you the answer, let me remind you of three simple truths about valuation:

1). It's not absolute

2). It's not what YOU think it is or should be

3). It's meaningless without context

What do I mean by those "3 simple truths"?

1). It's not absolute. Valuation is fluid. It fluctuates. It's true for a fleeting moment. It's based on things like growth, margin, market opportunity, market context - and about 193 other things that you may or may not be able to control. And it's relative, just to add a little more complexity. What the valuation is today may not be what it is tomorrow. There's a litany of things that might move the number(s).

2). As the business owner, you don't decide valuation. You may set some guidelines, you may have expectations, but no matter what your number is, if no buyer will pay that number, that number is not the valuation.

Of course, you never have to take a price you don't like, so let's not make that mistake, but if no one pays your price, then your price isn't the valuation.

Reality is an agreed-upon deal and nothing else.

3). It's meaningless without context. A lot of people commission reports from experts and bankers and brokers and other folks deeply involved in working with business owners. Those analyses and reports are great for guidance but they're still only part of the answer.

Case in point:

I recently worked with a business owner in an industry with fairly well-established purchase multiples. When a buyer knocked, I told him what I expected the buyer would offer when the conversation got there.

I was right (great, let's throw a party!).

But the business owner didn't want to sell at that price. Since then, I've been working to help him understand that the price isn't going up unless he does some things that buyers value.

He's now doing those things.

It's going to take time. But if he wants $15 million, and the offer was $10 million, that's a big gap and there's work to be done. Even for made-up numbers like these.

So as a small business owner, how should you deal with this?

As much as I say you can't rely on theory to tell you valuation in practice, the reports and analyses can help you at least understand market context, help you set expectations. What attributes buyers are prioritizing. And from there, you can start pointing your business in that direction.

It's going to take some time. Which is why it's time to start planning and preparing, before you hear numbers you don't like.

28

This morning I paid $4.59 per gallon for gas for my beloved Honda.

Less than a year ago I paid $2.85. Same gas station. (Same car.)

That's a 61% increase.

When my costs go 61% higher, I'm doing things a little differently. At least for now.

• I make multiple stops instead of multiple trips.

• I stop racing to the red light, I coast to the stop sign.

• I...er...um...watch my speed. I drove to Hartford on Monday and actually tried to stay at 70 mph or below.

(Sorry mom, I promise I check my blind spots and don't tailgate and signal before changing lanes.)

Point is, the situation changed, so my behavior's changed.

And the same is true if you're a small business owner. When it's time to start thinking about selling your business, it's time to look at your "behaviors." Your business processes, your team, your customers, partners, vendors, and the relationships, and everything else.

• What's working.

• How it works.

• What you can optimize.

• What you can eliminate.

What's killing your "mpg" (your margins).

But you shouldn't wait until the market moves to get started.

These things take time. Effort. Dedication. Discipline. Focus. Introspection. A team effort.

And when the market moves, you don't want to be caught off-guard, still waiting for the perfect moment to get your business deal-ready. Because the market moves both directions, and when the stars align, it's too late to start changing things.

But there's hope! There's help out there!

If you're ready to start taking a closer look at how deal-ready your business is, I'm ready to talk.

DM in confidence before that first buyer even knocks, so you'll have a full tank of $2.85 for the long road ahead.

1

51