Joined August 2017

- Tweets 283

- Following 530

- Followers 60,243

- Likes 2,353

33 Photos and videos

Pinned Tweet

Jun 7

ℹ️ SpaceX PreStocks: What Happens After IPO

SpaceX goes public on June 12.

Here’s what $SPACEX holders can expect:

🔁 After IPO, $SPACEX become convertible into a tokenized public stock equivalent.

🔗 Conversion happens through normal trading and is fully onchain. No KYC required.

✂️ The 5-for-1 stock split will be accounted for.

🔒 Like most private shares, SpaceX has a mandatory post-IPO lockup. In this case, the underlying shares unlock in tranches over the first 6 months.

⏳ During the lockup period: because underlying shares are still locked, liquidity is temporarily limited and $SPACEX trades at a discount to the public stock price. The discount is priced by the market and likely narrows as underlying shares unlock over the 6 months. Holders can sell at this discount and new buyers can buy in at this discount.

🔓 After the lockup period: with underlying shares fully unlocked, $SPACEX converts 1:1 into the tokenized public stock equivalent (before liquidity provider fees), with no lockup discount.

⏰ SpaceX PreStocks ($SPACEX) conversion deadline: 11:59pm UTC on March 12, 2027.

⏰ xAI PreStocks ($XAI) conversion deadline: 11:59pm UTC on September 12, 2026 (conversion into $SPACEX at a 1-to-0.1433 ratio, available since February).

🚨 After these conversion deadlines, these tokens will expire worthless and no longer be supported.

41

12

81

33,817

PreStocks retweeted

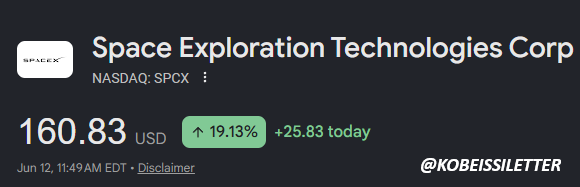

BREAKING: SpaceX, $SPCX, stock officially begins trading, now at $160.83/share, up 19% from the stock's IPO price.

This officially makes SpaceX a $2.1 TRILLION company, the 7th largest public company in the world.

171

337

3,434

290,513

PreStocks retweeted

Many are asking why is SpaceX, $SPCX, NOT trading yet?

Here's exactly how the IPO process works and when the shares will be available to trade (Bookmark this):

The IPO was quoted at 9:50 AM ET and was expected to begin trading at 10:00 AM ET, but that does NOT guarantee shares will trade at that time.

Before trading begins, Nasdaq must complete a price-discovery auction where buy and sell orders are collected and matched.

At around 9:50 AM ET, "first indications" came out which are essentially a "gauge" of where the stock will open.

The first indications on $SPCX came in at $175/share, or a ~30% premium to the $135/share IPO price.

During this process:

1. Orders are entered, but no trades occur yet

2. Nasdaq continuously updates the indicative opening price

3. The opening price is adjusted until supply and demand are balanced

4. Only then does the opening auction occur and the first trade print

For major IPOs, delays are common such as Google in 2004 and Meta in 2012 which saw their first trades over 2 hours after the US market opened.

We expect the SpaceX IPO to open for trading within the next 60 minutes.

Buckle up for a historic day.

214

580

5,770

1,005,935

PreStocks retweeted

BREAKING: The SpaceX, $SPCX, IPO is now receiving first indications as the Nasdaq window opens.

Details include:

1. First indications are coming in at $175/share

2. This implies a ~30% jump from the $135/share offer price

3. The IPO has drawn $350 billion in total demand, $250 billion of institutional demand

4. 70% of shares sold to institutions were allocated to long-only investors

5. SpaceX is set to open as the 6th largest public company in the world

Turn on our post notifications at @KobeissiLetter for real time analysis as the SpaceX IPO launches.

194

380

4,545

751,637

Jun 12

✂️ SpaceX PreStocks now reflects the 5-for-1 stock split.

If you hold $SPACEX, supported apps should now show your balance multiplied by 5 and price divided by 5. This is purely a cosmetic UI update to reduce confusion. Your raw balance is unchanged.

This is achieved through @Solana’s SPL-22 scaled UI amount extension, which instructs apps to display scaled balances and prices without changing the raw balances.

If an app has integrated $SPACEX but still shows unscaled prices and/or balances, please tag them below so we can help get them to support the extension.

39

5

39

8,015

PreStocks retweeted

Jun 11

- @PreStocks hits 25,000 holders.

Pre-IPO stocks on @solana.

13

10

59

5,088

PreStocks retweeted

May 22

Stocks tab is live on Lavarage v2. No need to be sidelined for one of the largest IPO upcoming.

Margin trade curated SPL tokens from @PreStocks and @xStocksFi. Backed by issuer SPV (their claim, not ours). DYOR.

Try it here: v2.lavarage.xyz/#xstocks

1

5

19

4,560

PreStocks retweeted

May 22

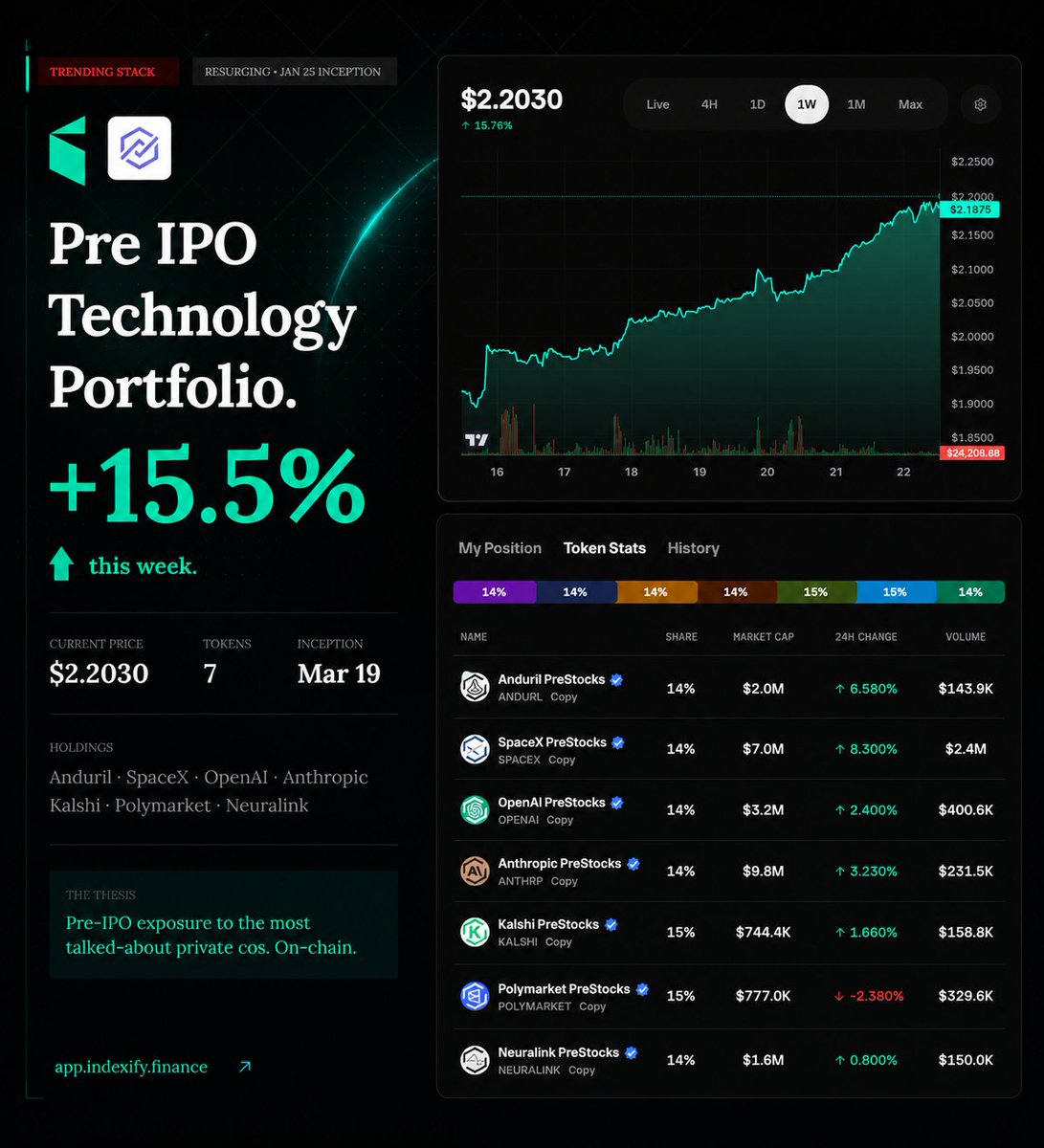

Pre IPO Technology Portfolio just bounced hard.

Took a haircut. Now up 15.5% this week.

Dips on solid theses are often the opportunity.

All on-chain. All public. All on @PreStocks & @solana

solana:PresTj4Yc2bAR197Er7wz4UUKSfqt6FryBEdAriBoQB · solana:PreANxuXjsy2pvisWWMNB6YaJNzr7681wJJr2rHsfTh · solana:PreweJYECqtQwBtpxHL171nL2K6umo692gTm7Q3rpgF · solana:Pren1FvFX6J3E4kXhJuCiAD5aDmGEb7qJRncwA8Lkhw · solana:PreLWGkkeqG1s4HEfFZSy9moCrJ7btsHuUtfcCeoRua · solana:Pre8AREmFPtoJFT8mQSXQLh56cwJmM7CFDRuoGBZiUP · $Neuralink

1

5

16

3,757

PreStocks retweeted

May 20

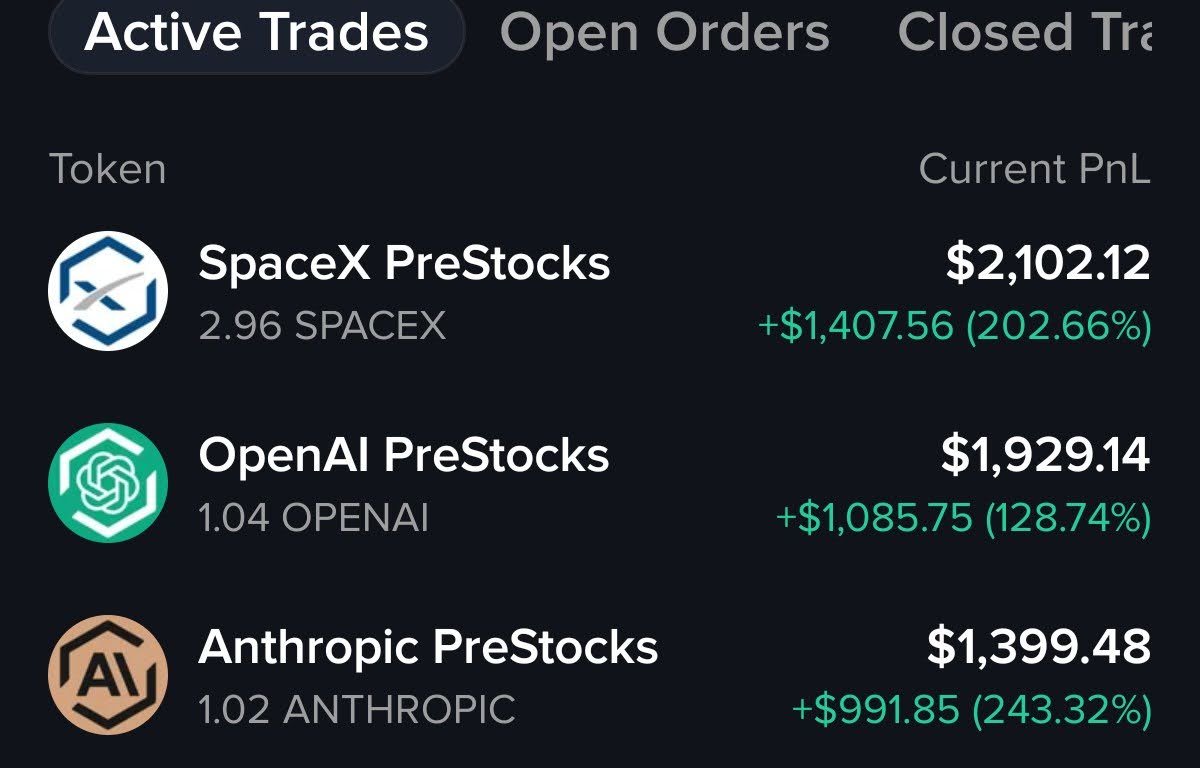

Access the world’s greatest private companies through tokenized pre-IPO stocks.

@PreStocks brings 24/7, permissionless trading of companies like SpaceX, OpenAI, and Anthropic onchain.

Powered by Meteora.

4

9

31

4,933

PreStocks retweeted

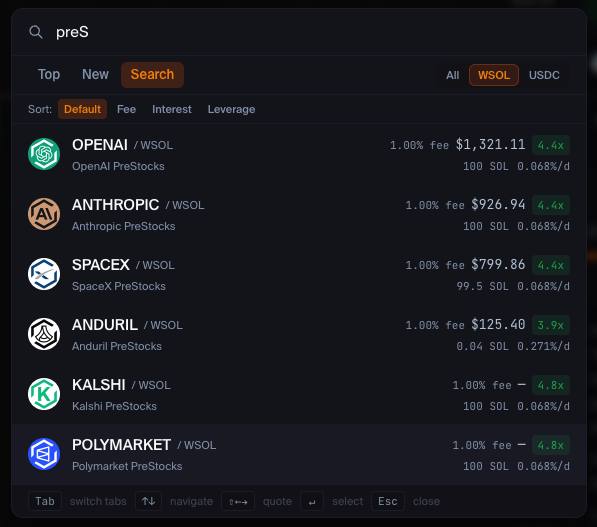

May 19

SpaceX IPO drops June 12. @anduriltech, @Kalshi, @Polymarket queued behind it.

All tradable on @solana via @PreStocks — now with up to 4.8× spot margin on Lavarage.

Real PreStocks tokens back every position. Repay anytime to claim them.

4

4

25

3,873

PreStocks retweeted

May 18

ALERT: $SPACEX onchain volume has surged to $15.2M ( 430%) in the last 24 hours ahead of the June IPO, now trading at a $2.1T implied FDV.

Live on Solana via @PreStocks.

tokens.xyz/spacex

3

7

28

3,500

PreStocks retweeted

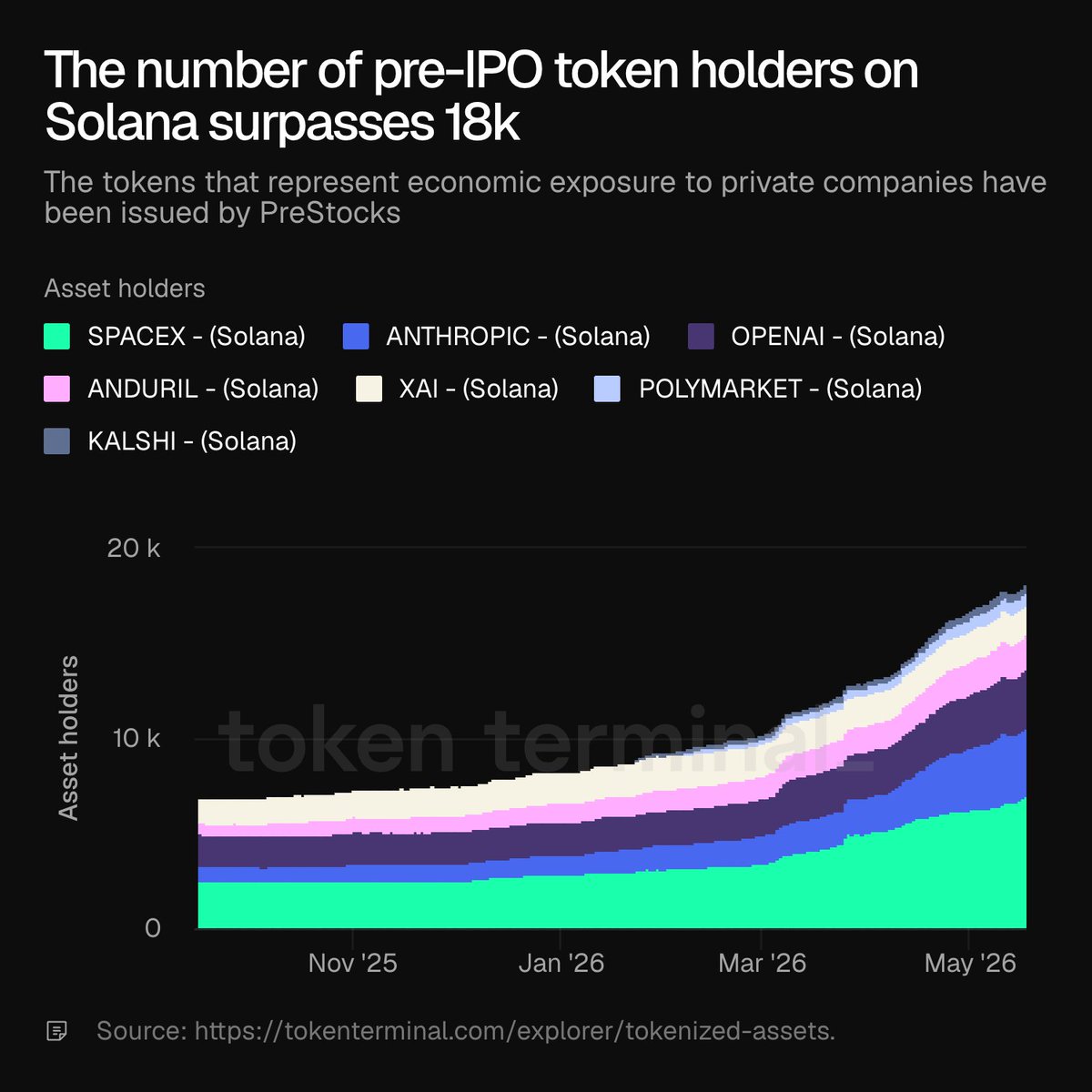

May 18

The line between public and private markets is blurring.

More than 18k wallets on @solana now hold tokenized exposure to private companies.

These assets, issued by @PreStocks, provide onchain economic exposure to companies like @SpaceX, @OpenAI, @AnthropicAI, and more.

16

17

88

18,489

PreStocks retweeted

May 18

JUST IN: SpaceX @PreStocks volume on @Solana has surged to $11.9M in the last 24 hours as IPO speculation builds, with the market now trading at a $2.08T implied FDV.

28

15

98

18,663

May 15

Recent headlines do not change the reality of pre-IPO markets.

SPVs have been a dominant part of pre-IPO secondaries for over a decade. SPV and counterparty risks are not new. Private companies have long been aware of, relied on, and benefited from secondary markets, even while publicly disavowing them. SPVs and secondaries help these private companies broaden investor demand, provide liquidity to employees and early investors, and support price discovery.

At PreStocks, we mitigate counterparty risk by avoiding 3rd or lower layer SPVs, verifying actual ownership up to the cap table, and vetting and reference checking fund managers before tokenization.

PreStocks tokens are Reg S debt instruments issued outside the U.S. and available only to eligible non-U.S. users. They provide economic exposure without placing tokenholders on private-company cap tables. Minting and redemption require eligibility verification and KYC. Settlement on redemption or exit is made in stablecoins or tokenized public equity after IPO, not via direct equity transfer.

As PreStocks scales, we further diversify backing across more SPVs, negotiate better terms, and progressively upgrade to higher quality exposure.

PreStocks benefits from and advocates for stronger private-market standards, including greater accountability from larger private companies that benefit from secondary markets, stronger protections for secondary-market investors, clearer ownership-chain reporting, stronger rules for SPV fund managers, and improved reporting by token issuers (including PreStocks).

All live PreStocks tokens remain fully backed in accordance with our terms, and PreStocks continues to operate normally.

As long as a secondary market exists, PreStocks exists.

Thank you for your attention to this matter.

18

28

124

11,639

PreStocks retweeted

May 10

Crazy, you can just buy the token instead and not pay funding for exposure.

@PreStocks is a killer product.

tokens.xyz/anthropic

If you ever feel dumb just remember people are PAYING 8,700% in funding to have pre-IPO exposure to Anthropic at a $1T valuation

12

4

78

16,219

PreStocks retweeted

May 6

Insanely bullish @PreStocks on @solana

Imo if you solve a real access problem - pmf follows

Prestocks are solving a real access problem today. People want exposure to these assets and they can get them on Solana right now!

May 6

PreStocks volume just crossed $1 billion! 📈🎉

This is what happens when pre-IPO stocks finally trade like liquid assets. You get permissionless, instant exposure to Anthropic, SpaceX, Anduril and more - before they go public.

Only possible on @Solana.

5

5

59

7,244

PreStocks retweeted

May 6

PreStocks volume just crossed $1 billion! 📈🎉

This is what happens when pre-IPO stocks finally trade like liquid assets. You get permissionless, instant exposure to Anthropic, SpaceX, Anduril and more - before they go public.

Only possible on @Solana.

52

35

200

47,717

Anthropic, OpenAI, SpaceX holders are up $4 MILLION on Solana

VCs took your dreams of buying your favorite companies at FAIR valuations

They will IPO at TRILLIONS, leaving ZERO upside to retail

So I made this website that shows you how to buy them on Solana

🔗 iposolana.com

4

5

67

8,632

PreStocks retweeted

May 4

Time to close out these @PreStocks and have some fun. But it's been a great ride with @mobyagent 🫶

8

7

51

6,006