Bruce Lindsay Professor of Economics and Public Policy at Chicago Booth

Joined October 2012

- Tweets 3,838

- Following 590

- Followers 25,611

- Likes 15

251 Photos and videos

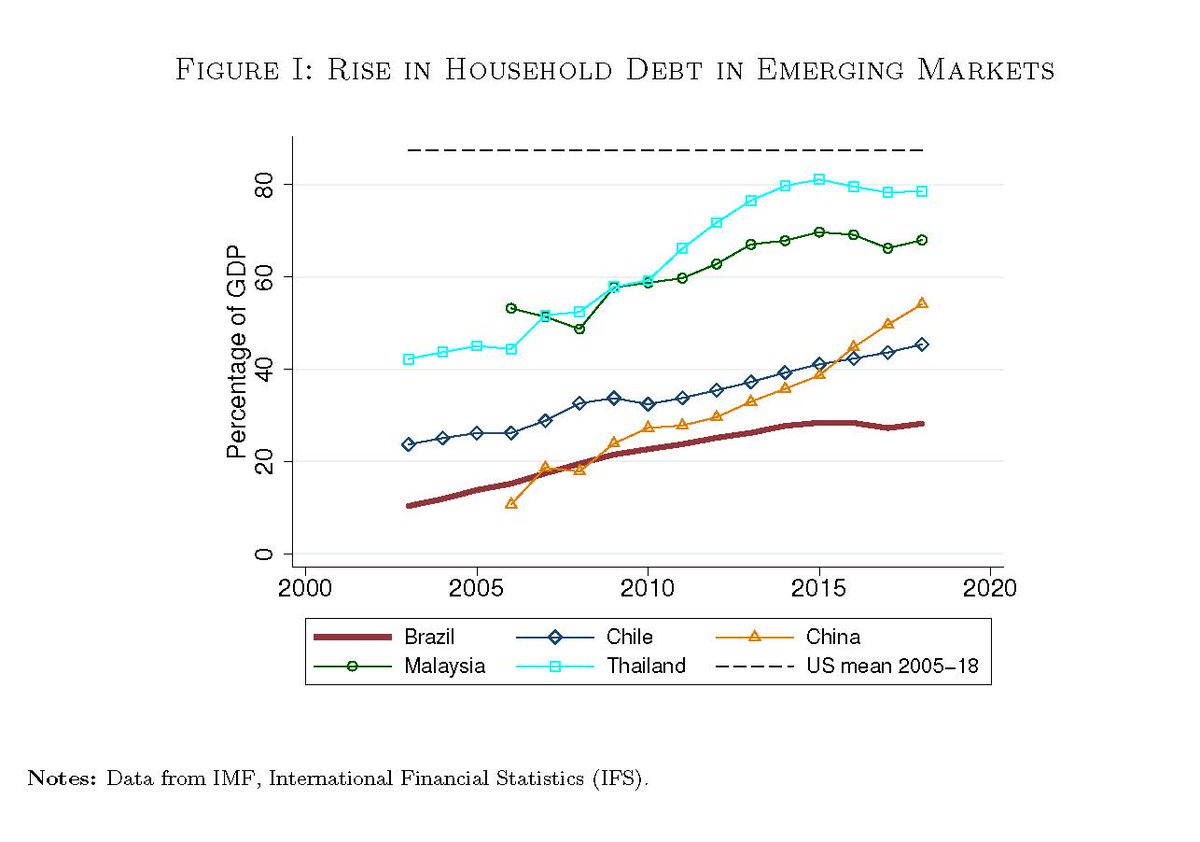

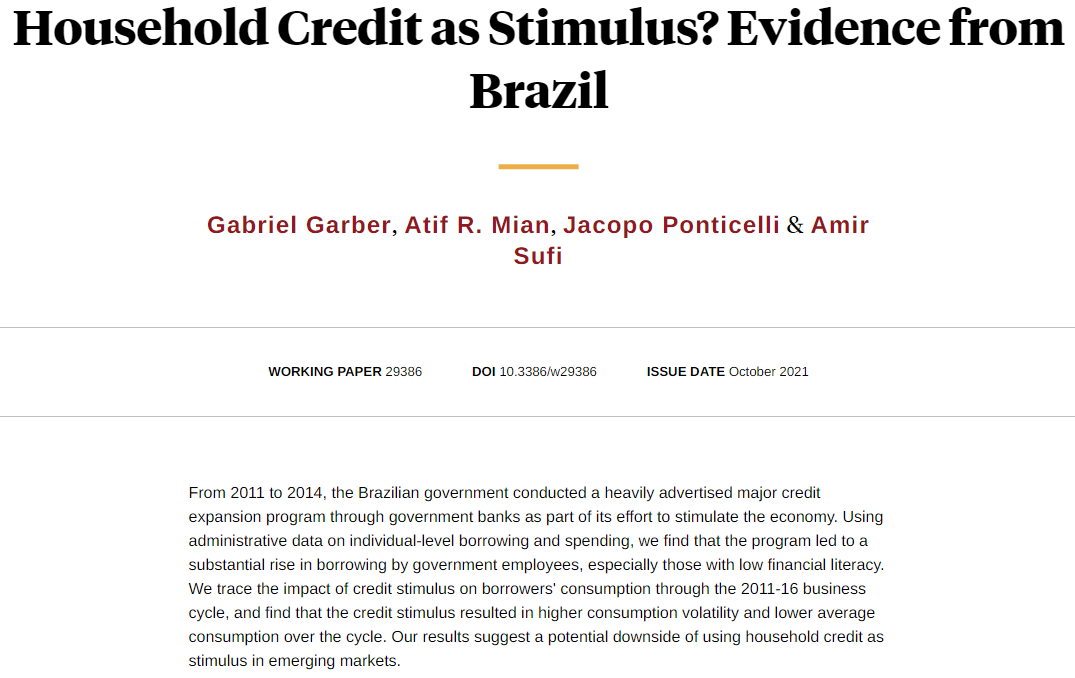

Starting in 2011, the Brazilian government tried to boost economic activity through aggressive household lending through government-owned banks. Is "household credit as stimulus" a good idea? A new paper with Gabriel Garber, @AtifRMian, and @jacopont (1/N)

nber.org/system/files/workin…

4

45

163

There may be an important role for governments in developing household credit markets to help with risk-sharing, house purchases, and education financing. But the Brazilian example suggests that using household credit to juice economic activity can end badly (5/N)

2

3

24

A major government credit program in Brazil resulted in higher borrowing by public sector employees with low financial literacy at the expense of higher volatility and lower average consumption, from Gabriel Garber, @atifrmian, @jacopont, and @profsufi nber.org/papers/w29386

23

52

We live in an extremely low interest rate environment. What are the consequences for industry competition and market structure? This is the focus of the recent study we released (joint with Thomas Kroen @ErnestLiuEcon @AtifRMian). A thread (1/N)

bfi.uchicago.edu/wp-content/…

1

23

91

Falling interest rates disproportionately benefit industry leaders, especially when rates are already low, from Thomas Kroen, @ErnestLiuEcon, @atifrmian, and @profsufi nber.org/papers/w29368

2

26

49

Amir Sufi retweeted

18 Oct 2021

Are very low interest rates market neutral?

Or do low rates tend to tilt the scale in favor of market leaders, thus reducing competition?

We have a new empirical paper out that suggests falling rates help the rise of superstars

A short thread ...

nber.org/papers/w29368?utm_c…

6

44

114

Amir Sufi retweeted

18 Oct 2021

New paper by @ErnestLiuEcon @AtifRMian @profsufi & Tom Kroen shows that lower rates benefit industry leaders; more so as r➡️0. Links low r and high concentration as in earlier theory paper: scholar.princeton.edu/sites/…

Falling Rates and Rising Superstars nber.org/papers/w29368#.YW10…

4

19

Amir Sufi retweeted

11 Oct 2021

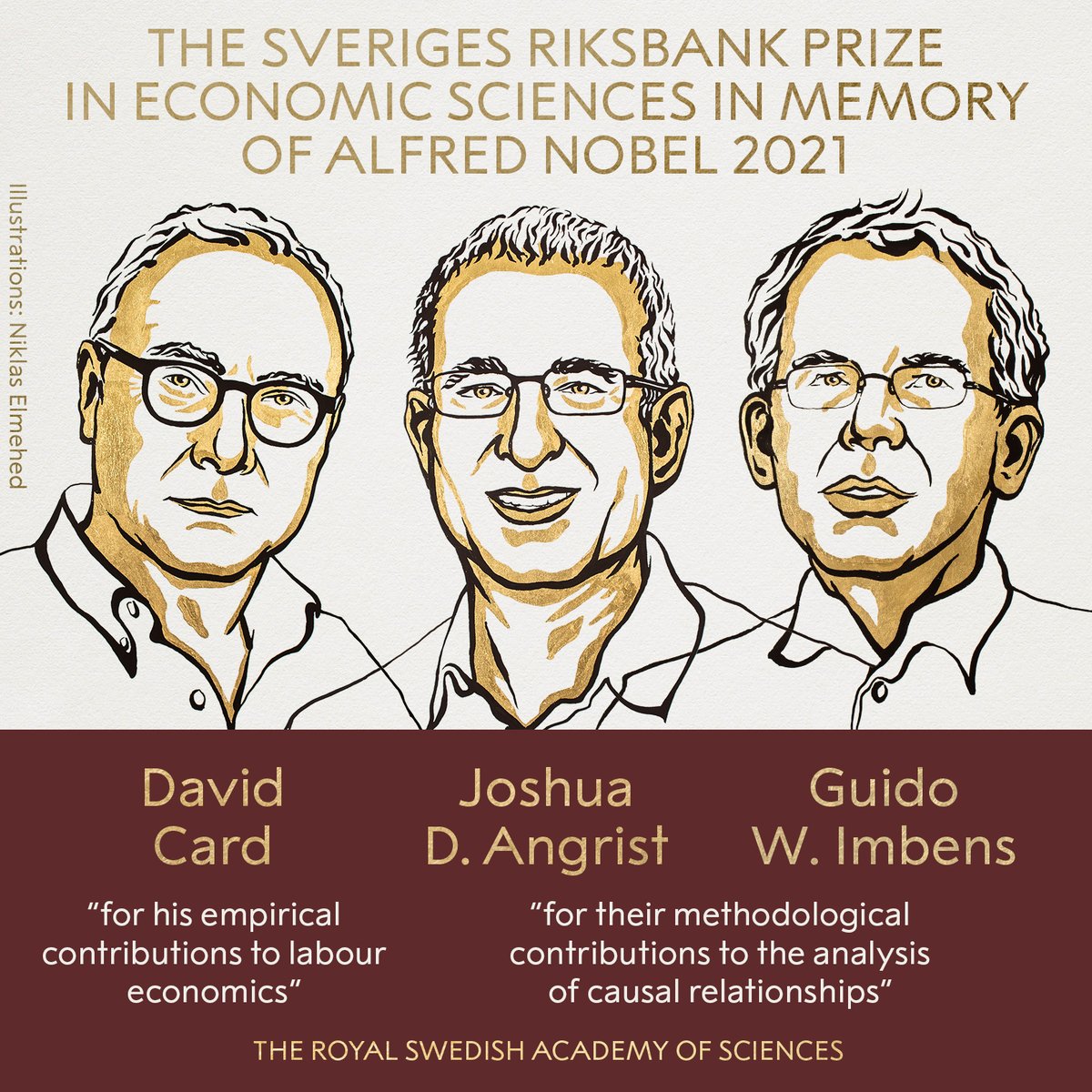

Can’t even explain yet to my non-Econ friends just what a revolutionary force these three economists who just won the Nobel created. My book on causal inference has a blurb by Guido on the back and I sent one to Angrist with the inscription “thank you for inspiring a generation”

3

50

568

Amir Sufi retweeted

11 Oct 2021

Uncorking the Champagne here!

This is a win for labor economics, modern empirical microeconomics, and three economists who were at the center of a revolution.

11 Oct 2021

BREAKING NEWS:

The 2021 Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel has been awarded with one half to David Card and the other half jointly to Joshua D. Angrist and Guido W. Imbens.

#NobelPrize

1

29

260

Amir Sufi retweeted

11 Oct 2021

Congrats on a well-deserved Nobel Prize for @metrics52, a fantastic advisor, scholar, and teacher. Rock on, Josh!

(screenshots courtesy of his sneaky metrics TA in March 2020)

8

74

1,067