MFT & HFT | Views my own. Not financial advice.

Joined November 2019

- Tweets 14,997

- Following 1,620

- Followers 70,121

- Likes 10,605

1,323 Photos and videos

23h

i smell an arb

Jun 12

If you're wondering what happened to Solana @PreStocks SpaceX, they got absolutely crushed and are now trading around ~$112 (after 5:1 split), implying a ~40% discount to the underlying shares.

Turns out there's a 180-day lockup before preStocks can be converted into real shares (I suspect very few people were aware of this). So holders have two choices: dump into a thin-liquidity market at a steep discount today, or wait 180 days and convert at full value. Looks like many crypto degens are choosing the former.

Interestingly, this issue doesn't exist (and couldn't exist) in the $SPCX perp market.

Pre-IPO markets only make sense to trade via perps.

Hyperliquid.

4

2

78

31,618

Jun 9

Forecasting:

5min and below - XGBoost

15min and above - Ridge

You can enhance ridge by fitting non parametric regressions per feature as an in-between. To reduce fitting you can add a hypothesis, and only fit if it validates.

This is typically the optimal model by horizon.

18

14

309

23,690

Jun 8

I remember I went to a conference once and a quant fund exec (non technical) told me the full list of all the alt datasets they used.

He obviously had no idea that probably should’ve stayed confidential as testing datasets is a lot of work and many of them were niche, but it saved me testing 20 something datasets!

5

2

252

39,584

Jun 8

New article where we test various HFT features, resulting in 7x 5s features and 5x 15s features.

This is the first part in a 5-part series on how to go from feature ideas to a final production ready HFT forecast.

7

125

11,144

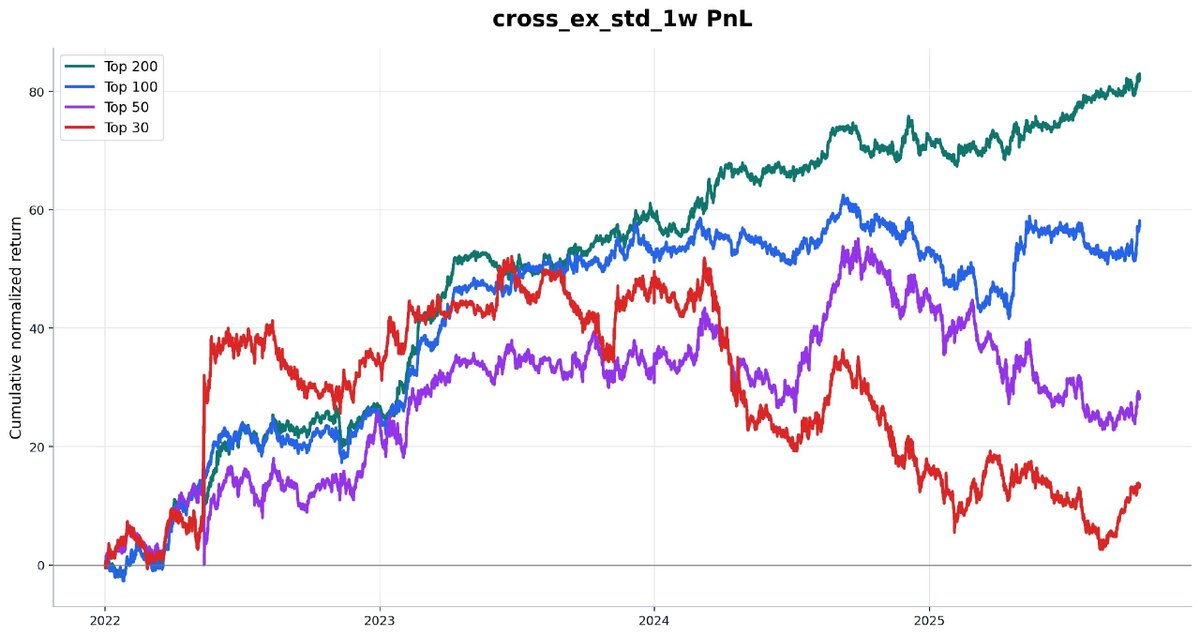

Jun 3

Here's an example of how an alpha decays as we trade less and less liquid assets. This the pre-fees performance of an alpha `cross_ex_std_1w`.

It is the standard deviation of volume across exchanges for a given timestamp, and then averaged over the past week. Basically how well do exchanges agree, you can also use OI it is about 0.86 correlation if you swap it out for OI.

It is very clear that as we trade less liquid and higher spread assets where it becomes increasingly harder and harder to monetise the signal gets worse.

It starts out at 2 sharpe and ends off at 0.3 Sharpe for top 30 (by marketcap). An example of efficiency of alphas.

2

6

132

12,258

Jun 2

This is a great read for active HFT researchers and breaks down research steps I use regularly in my own processes

Jun 2

In the latest article we break down exactly how to research and evaluate HFT alphas, and explain advanced techniques used by top trading firms.

6

151

21,439

Jun 2

In the latest article we break down exactly how to research and evaluate HFT alphas, and explain advanced techniques used by top trading firms.

12

233

79,243

May 29

I find HPCA is a v useful tool for feature selection. Makes the clusters where you need to choose between features much more clear than a correlation grid

7

1

37

6,911

Stat Arb retweeted

May 27

A top quant lost his job due to an AI reasoning model replacing him at his company. He kept applying to different companies and tried his hand at macro writing but to no avail.

Eventually he swallows his pride and talks to his school friend who is now a plumber.

"I understand your old position was a finance maths guy. Why don't you come to our company and apply for a plumber position? You will earn half your old salary but the overtime and the union benefits make up for the rest. But remember, when you apply, tell them that you completed only seven elementary classes. They don't like educated people."

So it happened. The quant got a job as a plumber and his life significantly improved. He just had to seal a screw or two occasionally, and his salary was good enough and he had zero stress.

One day, the board of the plumbing company decided that every plumber had to go to evening classes to complete "basic financial literacy" certification. So, our quant had to go there too. It just happened that the first class was retirement planning. The evening teacher, to check students' knowledge, asked

“If you invest half your money in stocks and half in bonds, how do you calculate the portfolio return?”

The person asked was the quant. He jumped to the board, and then he realized that he had forgotten the formula. He started to reason it, and he filled the white board with He defined a filtered probability space (Ω, ℱ, {ℱ_t}, ℙ) and posited two correlated geometric Brownian motions for the risky and “risk-free” assets. He invoked the Radon-Nikodym derivative to switch to the risk-neutral measure ℚ, then switched back because the question was about realized returns, not prices.

He filled the whiteboard with stochastic discount factors, covariance matrices, CRRA utility functions, and pages of Itô calculus. He derived the wealth process under a self-financing strategy:

dW_t = W_t[(w R_s (1−w) R_b) dt w σ_s dB_t^s (1−w) σ_b dB_t^b]

Then he solved the HJB equation for the optimal allocation, noted that Merton’s solution collapses to a constant weight under log utility, and circled w = ½ as the given constraint.

He invoked the linearity of expectation. He cited Markowitz (1952). He drew a small efficient frontier in the corner for context.

Finally, exhausted, chalk-dusted, eyes wild, he arrived at:

R_p = ½ R_s ½ R_b

Then forty plumbers, in perfect unison, slammed their wrenches on the desks and roared:

“YOU FORGOT THE VOLATILITY DRAG, YOU FUCKING TOURIST!!”

34

128

2,364

211,914

May 23

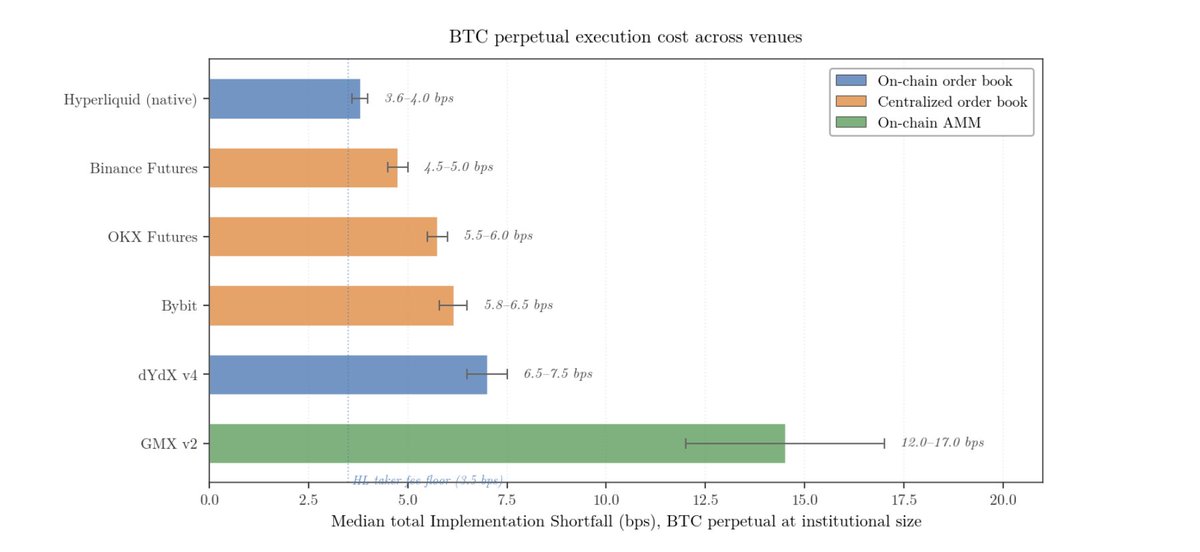

Who is paying >3.6 bps to trade BTC 🤣

May 23

Currently deep in the full history of Hyperliquid order book data, reconstructing Implementation Shortfall costs (the true cost of trading — the gap between the price you decided to execute at and the price you actually got, capturing every basis point lost to spread, market impact, and delay) — and the early findings are genuinely striking

4

2

65

23,815

May 23

Unit tests are an admission that your code might have errors. Real manual HFT developers don’t use them

7

1

134

13,893

May 23

ChatGPT has allowed otherwise incapable people to generate pretty graphs and this has revolutionised the quant slop space

13

7

256

12,664

May 23

None of you are going to make it if you think these ChatGPT renders of some bs no one uses is citadels alpha.

None of this is true

a citadel quant told me something that broke my entire trading framework

"we don't predict markets. we model the state machine"

he explained markov chains in 90 seconds

the market is never random - it always exists in one of three states

trending up, trending down, ranging - each has a fixed probability of shifting to another

build the transition matrix from real price data:

> trending up -> 68% stays trending, 21% flips to range, 11% reverses

> ranging -> 54% stays range, 28% breaks up, 18% breaks down

> trending down -> 61% stays falling, 24% flips to range, 15% reverses

now you're not guessing, you're playing probability

identify current state, enter with the 68% edge, size with kelly criterion based on that probability

the formula is public - markov published it in 1906

hedge funds use it, the math costs nothing

what costs you is asking the wrong question

"where is price going?" is random

"what state am I in right now?" has an answer

transition matrix built from 10 years of data is your edge

Bookmark it

not a signal, not an indicator - just conditional probability that compounds every single trade

14

7

246

36,669