Quantitative Researcher & Dev. | Financial Data Scientist | Machine Learning Engineer | Mathematical Research | Algorithmic Trading Systems

Joined July 2019

- Tweets 3,666

- Following 0

- Followers 12,202

- Likes 843

1,355 Photos and videos

Pinned Tweet

Apr 23

Hey guys! I’ve just released a refined, compact edition of one of my newsletter series on the foundations of quantitative trading. It is a theoretical introduction designed for aspiring quants who are beginning to explore the field. The focus is on first principles, method, and the conceptual framework behind quantitative trading.

Link in the comments. I hope you enjoy it.

11

46

502

24,843

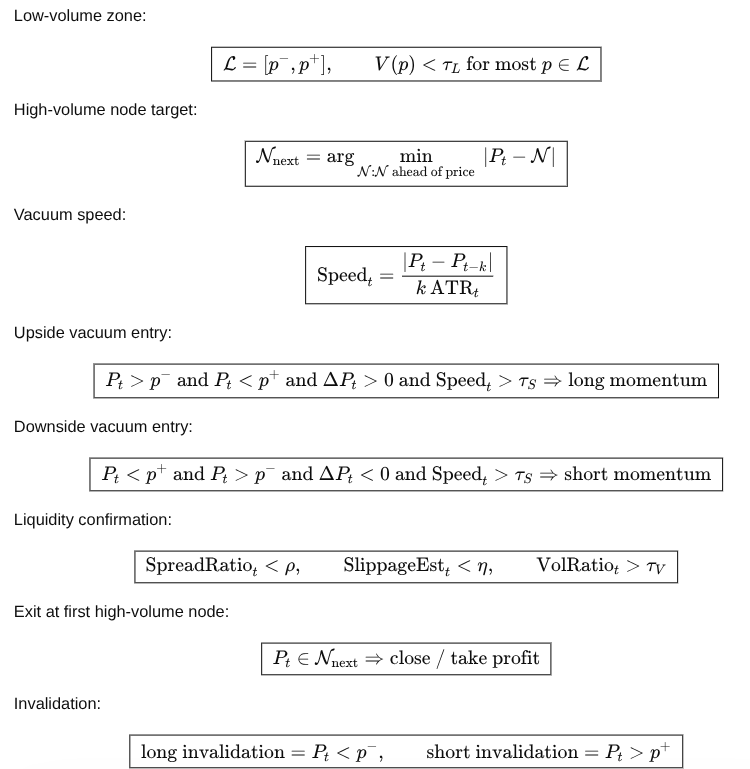

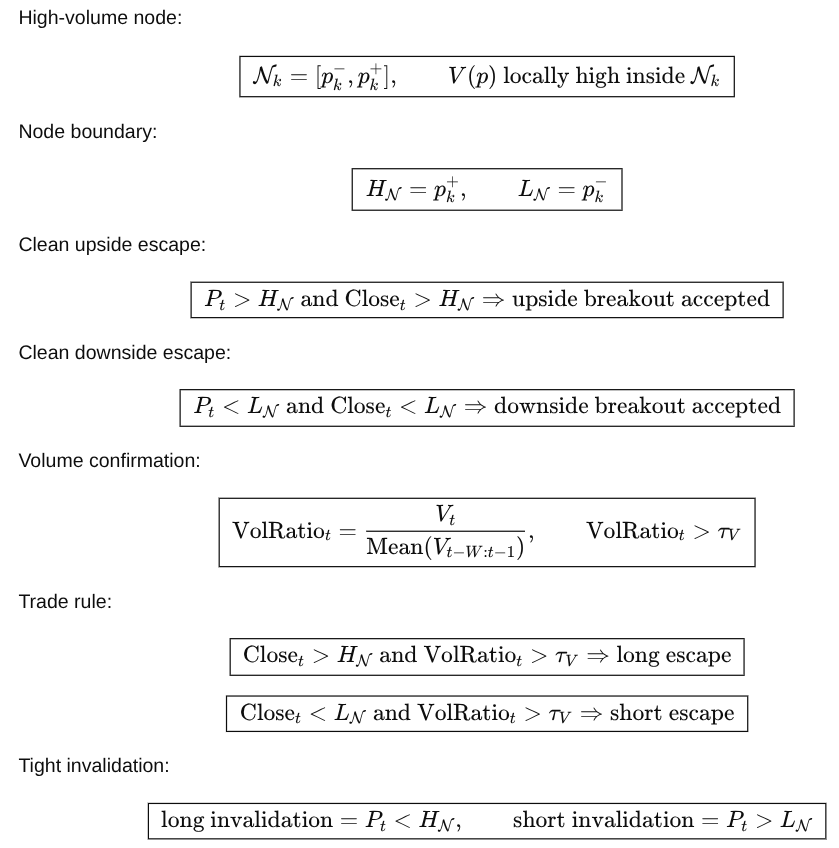

Some price zones contain little historical volume, so once price enters them, there is less resting interest to slow the move. This creates a liquidity vacuum where momentum can accelerate until price reaches the next high-volume node.

44

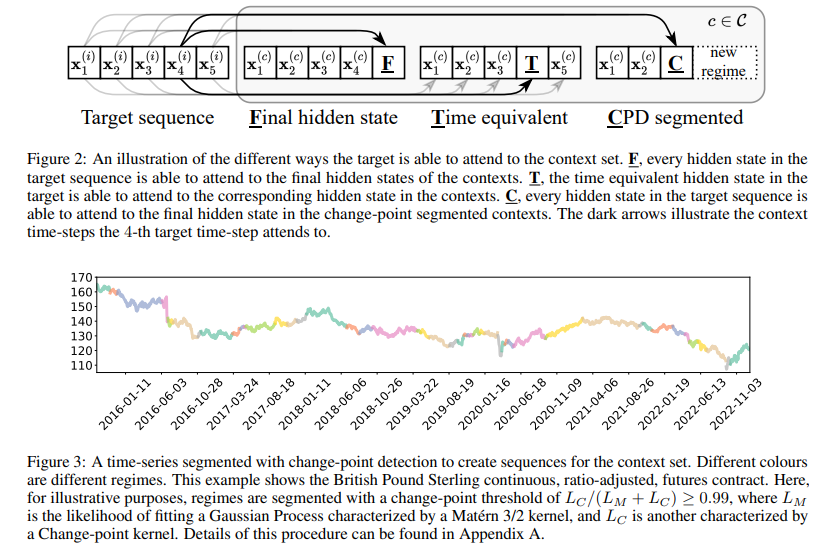

The inputs are normalized returns and MACD-style momentum features. That keeps the experiment clean, but it also means the paper is mostly testing whether attention over historical trend regimes improves trend-following, not whether the model discovers a broad transferable market structure.

1

28

1,624

The trading signal you research is never isolated. It is always linked to a specific context. The same signal can be valuable in one context and useless in another. Researching a signal means researching the conditions under which that signal expresses an edge.

1

2

26

1,033

Jun 13

These nodes often act as temporary balance areas because buyers and sellers previously agreed there. Trade the first clean escape from the node only when price leaves with acceptance, not just a wick.

1

20

1,124

Jun 13

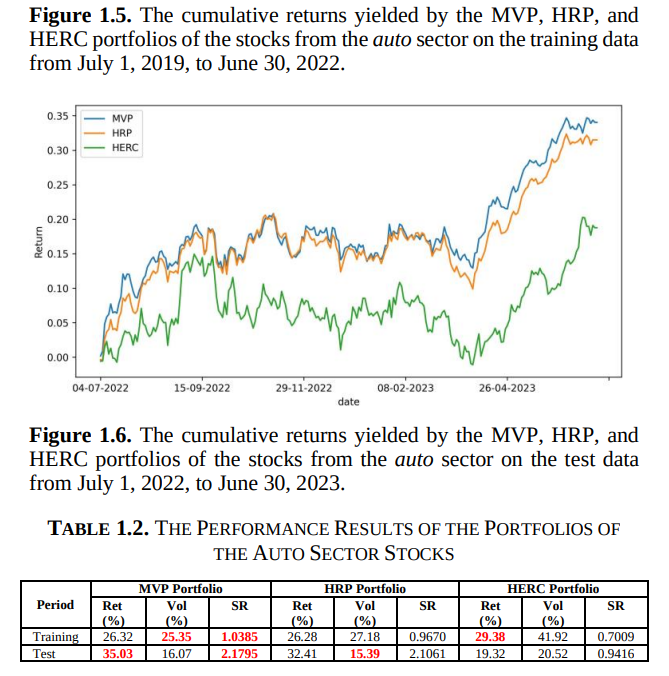

Although the paper has several obvious flaws, including look-ahead bias, survivorship bias, and an excessively short out-of-sample period, it still provides an interesting comparison of portfolio construction methods such as MVP, HRP, and HERC. However, the key issue is the results themselves, they are mediocre.

2

6

47

2,930

Jun 12

One of the strongest biases a data scientist might bring to the industry is the belief that they need hundreds of features to predict something, when in reality they only need one (but a useful one). That's where research begins and nonsense ends.

2

4

32

1,141

Jun 12

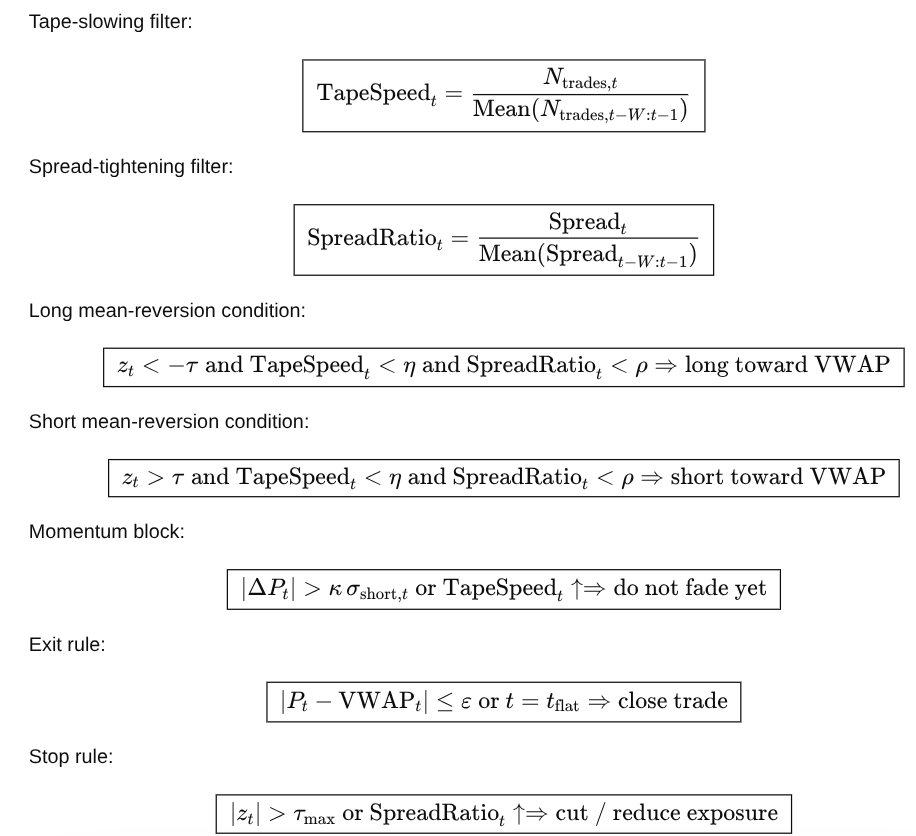

Large deviations from VWAP are faded only when the tape slows, spreads tighten, and immediate momentum weakens. This avoids shorting strength or buying weakness while the move is still being driven. The trade targets reversion back toward VWAP, not a full trend reversal.

2

21

162

6,532

Jun 12

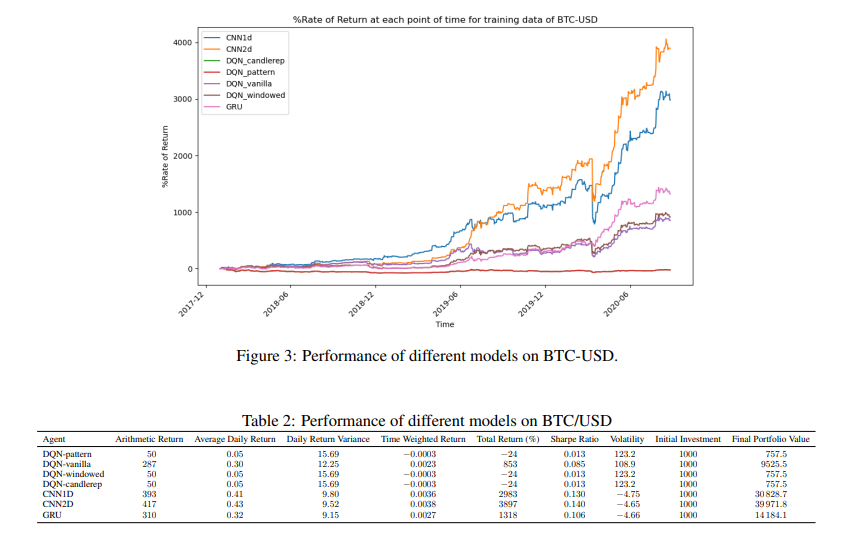

The biggest pitfall is that the paper treats higher backtest returns as evidence of model improvement. It stacks several DQN extensions, tests them on a very small number of assets, and then reports large returns without enough controls to separate real edge from overfitting.

4

4

44

2,639

Jun 11

I like this definition of trading inefficiencies because it connects more directly to dependence relationships.

1

2

13

813

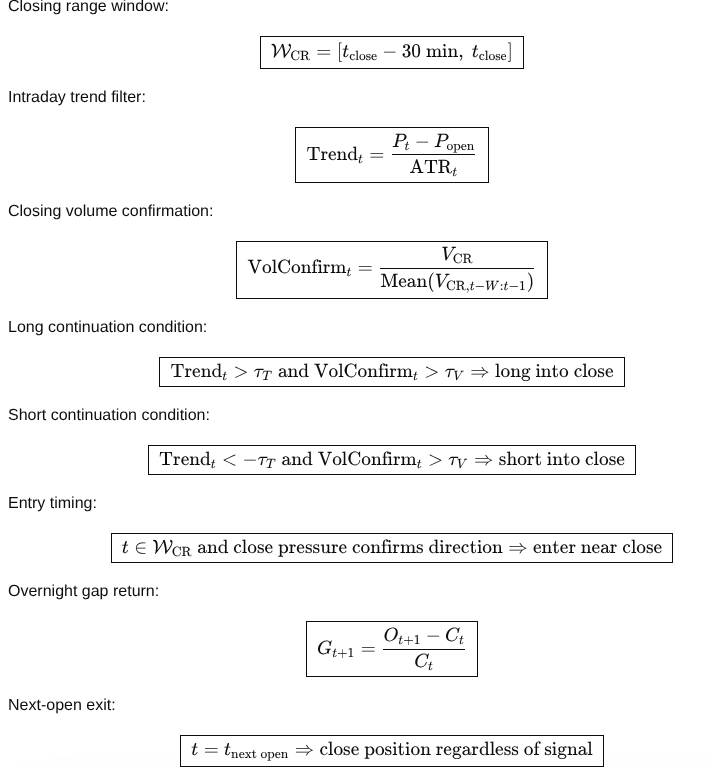

Jun 11

The last period of the session could reveal institutional positioning or rebalance pressure. If price is already trending and volume expands into the close, the move can carry into the next open. Enter only when trend and volume confirm during the closing window. Exit at the next open to capture overnight continuation without turning it into a longer swing trade.

1

3

47

1,978

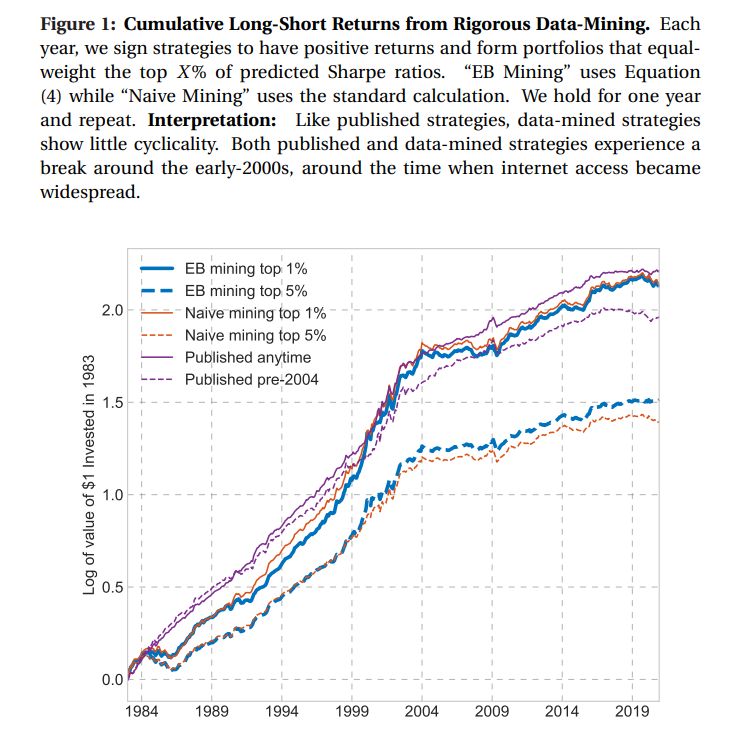

Jun 11

The authors admit that post-2004 EB predictions are less accurate because the 20-year rolling window fails to adapt to the market regime shift caused by information technology. EB could be interesting under a stable data-generating process, but markets are not stable

4

4

37

2,426

Jun 10

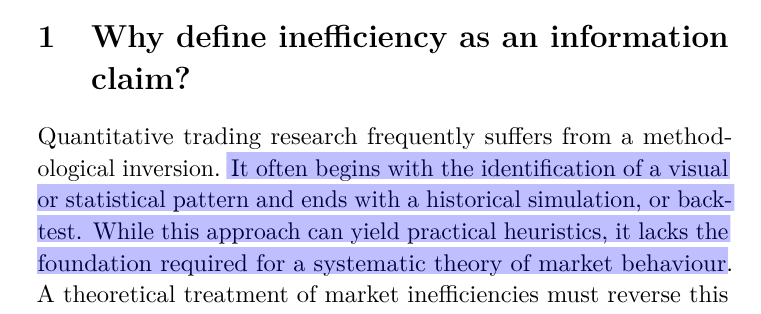

Visual or statistical trading pattern ⟺ Theory-first approach

1

1

18

825

Jun 10

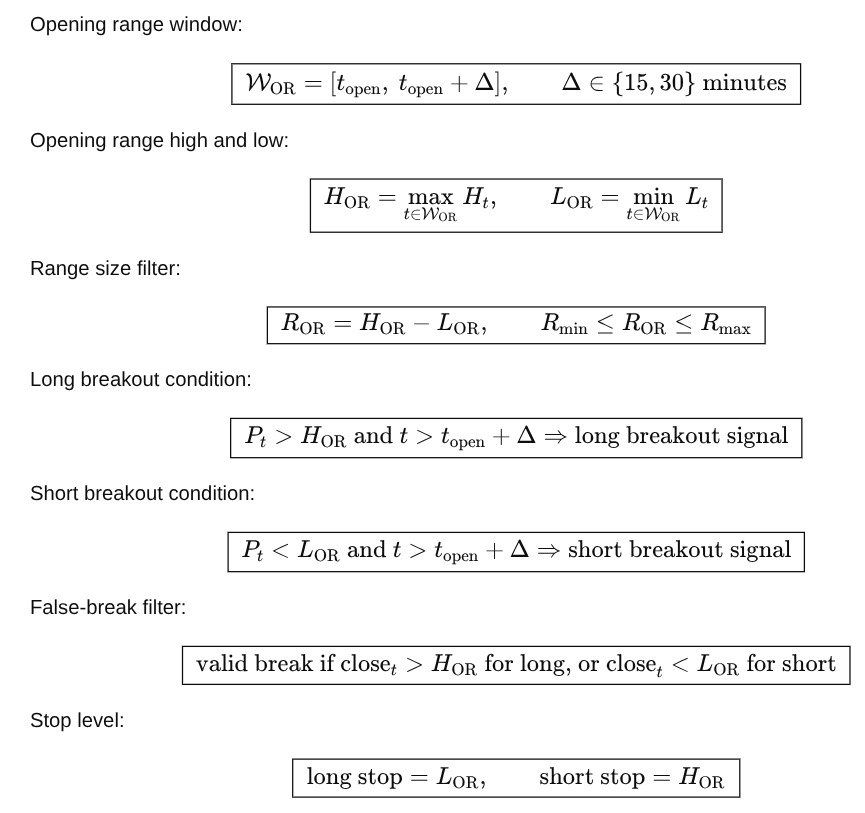

I would say that more and more people are alredy using this. Define the first 15–30 minutes as the opening range, where early liquidity sets the session reference zone. Trade only when price breaks above the range high or below the range low after the range is completed. The setup assumes that a clean break can trigger intraday continuation from trapped liquidity and early imbalance. Exit by time, not prediction, so the trade does not become an uncontrolled all-day position.

3

7

55

2,615

Jun 10

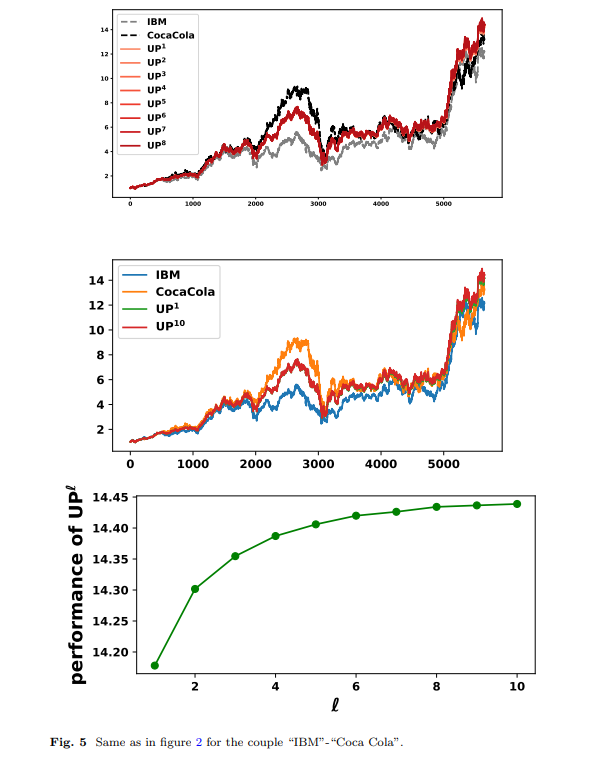

The paper itself admits that HOUPs can sometimes perform worse than the standard Cover UP. The conclusion says that empirical results are not guaranteed 😅

2

3

41

2,541