- Tweets 2,007

- Following 29

- Followers 1,631

- Likes 634

ALT Quantillion Atlas — Researched Return (since inception, Jul 01, 2010 to May 19, 2026, 15.9 years) Return: 2842.94% Return YTD: 1.32% 1Y Return: 3Y Return: CAGR (since 2010): 23.73% Sharpe: 2.44 Volatility: 6.09% Max Drawdown: 7.79% See attached chart for performance details. This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

ALT Quantillion Atlas — Researched Return (Jan 01–Jun 11, 2026, YTD) Return: 0.89% Sharpe: 0.21 Volatility: 8.31% Max Drawdown: 5.89% See attached chart for performance details. This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

ALT Quantillion Atlas — Researched Return (Jan 01–Jun 09, 2026, YTD) Return: 1.24% Sharpe: 0.28 Volatility: 8.18% Max Drawdown: 5.89% See attached chart for performance details. This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

ALT Quantillion Atlas — Researched Return (Jan 01–Jun 05, 2026, YTD) Return: 0.98% Sharpe: 0.23 Volatility: 8.27% Max Drawdown: 5.89% See attached chart for performance details. This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

ALT Quantillion Atlas — Researched Return (Jan 01–Jun 03, 2026, YTD) Return: 1.53% Sharpe: 0.35 Volatility: 8.16% Max Drawdown: 5.89% See attached chart for performance details. This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

ALT Quantillion Atlas — Researched Return (Jan 01–Jun 01, 2026, YTD) Return: 2.09% Sharpe: 0.46 Volatility: 8.18% Max Drawdown: 5.89% See attached chart for performance details. This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

ALT Quantillion Atlas — Researched Return (Jan 01–May 28, 2026, YTD) Return: 1.59% Sharpe: 0.37 Volatility: 8.26% Max Drawdown: 5.89% See attached chart for performance details. This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

ALT Quantillion Atlas — Researched Return (Jan 01–May 26, 2026, YTD) Return: 1.67% Sharpe: 0.39 Volatility: 8.32% Max Drawdown: 5.89% See attached chart for performance details. This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

ALT Quantillion Atlas — Researched Return (Jan 01–May 26, 2026, YTD) Return: 1.67% Sharpe: 0.39 Volatility: 8.32% Max Drawdown: 5.89% See attached chart for performance details. This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

ALT Quantillion Atlas — Researched Return (Jan 01–May 22, 2026, YTD) Return: 1.29% Sharpe: 0.31 Volatility: 8.42% Max Drawdown: 5.89% See attached chart for performance details. This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

ALT Quantillion Atlas — Researched Return (Jan 01–May 22, 2026, YTD) Return: 1.29% Sharpe: 0.31 Volatility: 8.42% Max Drawdown: 5.89% See attached chart for performance details. This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

ALT Quantillion Atlas — Researched Return (Jan 01–May 21, 2026, YTD) Return: 1.43% Sharpe: 0.34 Volatility: 8.45% Max Drawdown: 5.89% See attached chart for performance details. This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

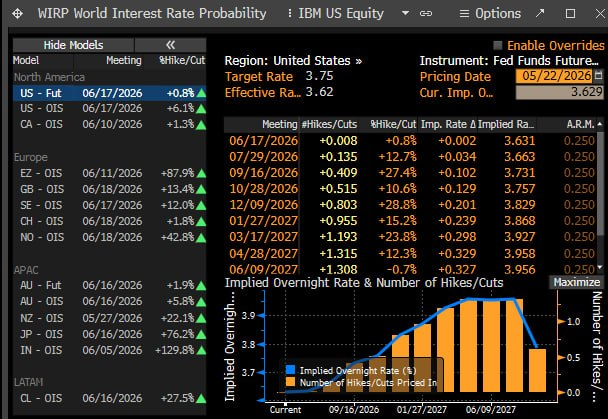

ALT Oil is still high, inflation pressure is not really gone, and WIRP is already showing that the market is no longer pricing only cuts. There is now a real probability of Fed hikes coming back into the curve for 2026–2027.