Quantpedia - The Encyclopedia of Quantitative&Algo Trading Strategies - we process academic research into trading ideas ... Risk Disclosure: quantpedia.com/risk

Joined April 2018

- Tweets 755

- Following 415

- Followers 5,554

- Likes 344

592 Photos and videos

Quantpedia in May 2026

– Quantpedia Awards 2026 Winners Announcement

– A new Dual Momentum report

– QuantBeats Episode 09

– Invitation to Uncorrelated Newport

– 11 new Quantpedia Premium strategies

– 9 new related research papers

– 7 new backtests

– and finally, 8 new posts on our Quantpedia blog

quantpedia.com/quantpedia-in…

#algo #trading #strategies #quantitative #finance #research

1

2

13

1,032

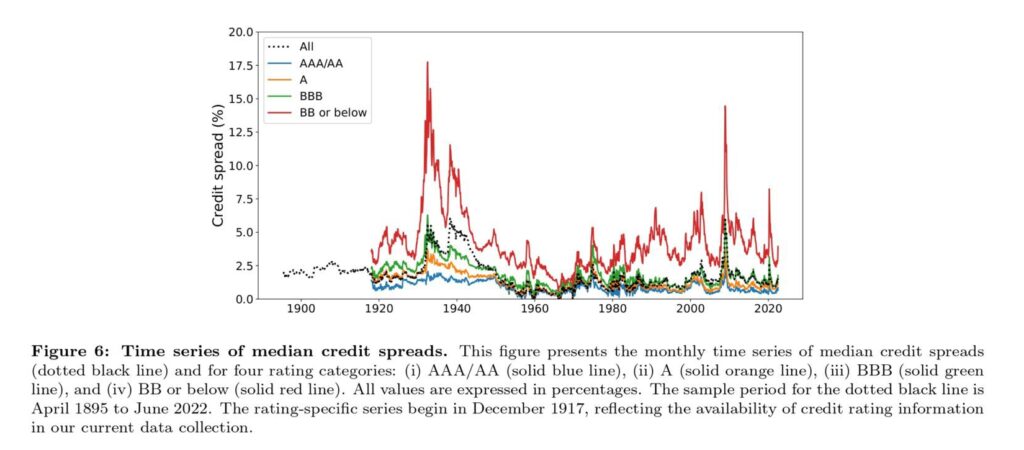

Reconstructing a Century of U.S. Corporate Bonds

How much do we really know about corporate bond returns before the modern data era? Until recently, the answer was: not enough. Most empirical work in corporate bond pricing has relied on relatively short samples, especially the post-2002 TRACE period, leaving open the question of whether observed risk premia are robust over longer horizons. Ghaderi, Plante, Roussanov, and Seo (2026) address this limitation by constructing a historical database of U.S. corporate bond returns from 1895 to 2022. Using hand-collected monthly bond quotes from sources such as the Commercial and Financial Chronicle, Standard & Poor’s Bond Guide, and Mergent/Moody’s Bond Record, they assemble a large panel of corporate bonds that allows for a much longer view of credit risk, return predictability, and factor pricing in fixed income.

quantpedia.com/reconstructin…

#credit #bonds #historical #data #spread #quant

2

15

1,620

QuantBeats Episode 09 - David Kaiser: The Process of Quant Value Investing

What happens when markets become unpredictable? David Kaiser breaks down how quantitative value investors rely on data, liquidity, and disciplined portfolio construction instead of reacting to every headline. Discover why a repeatable process, long-term conviction, and systematic decision-making can be powerful advantages in uncertain markets.

youtube.com/watch?v=XLozAKuQ…

#quant #podcast #quantbeats #value #investing

4

7

1,860

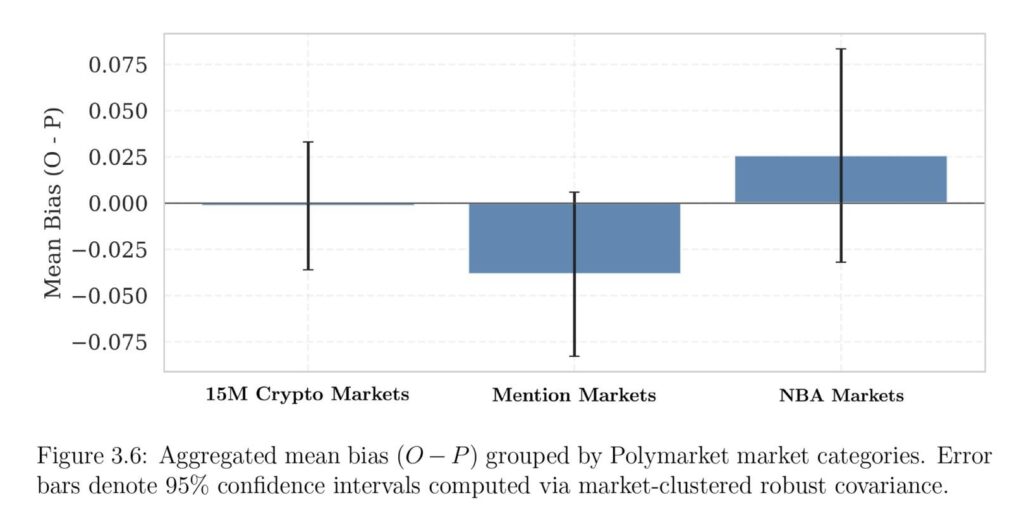

How Wise is the Crowd in Prediction Markets

If you’ve ever scrolled through Polymarket or Kalshi wondering whether the “wisdom of crowds” is actually wisdom—or just organized noise—you’re not alone. A new paper, “How Wise is the Crowd? Bias and Edge in Prediction Markets,” tears into the microstructure of modern prediction markets to ask a practical question: Who’s actually making money, and who’s just paying for the privilege of being loud? By engineering a high-frequency data pipeline that ingests tick-level order flow, on-chain wallet histories, and social commentary across decentralized finance and regulated venues, the authors expose structural inefficiencies that most traders overlook. The verdict? Market efficiency in Web3 betting isn’t dead—but it’s wearing a very clever disguise.

quantpedia.com/how-wise-is-t…

#quant #polymarket #kalshi #wisdom #crowd

2

309

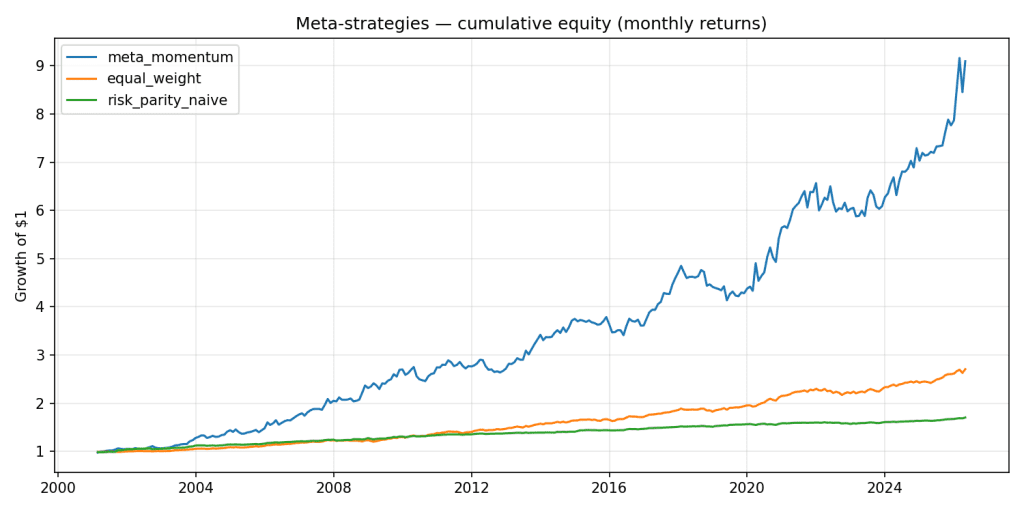

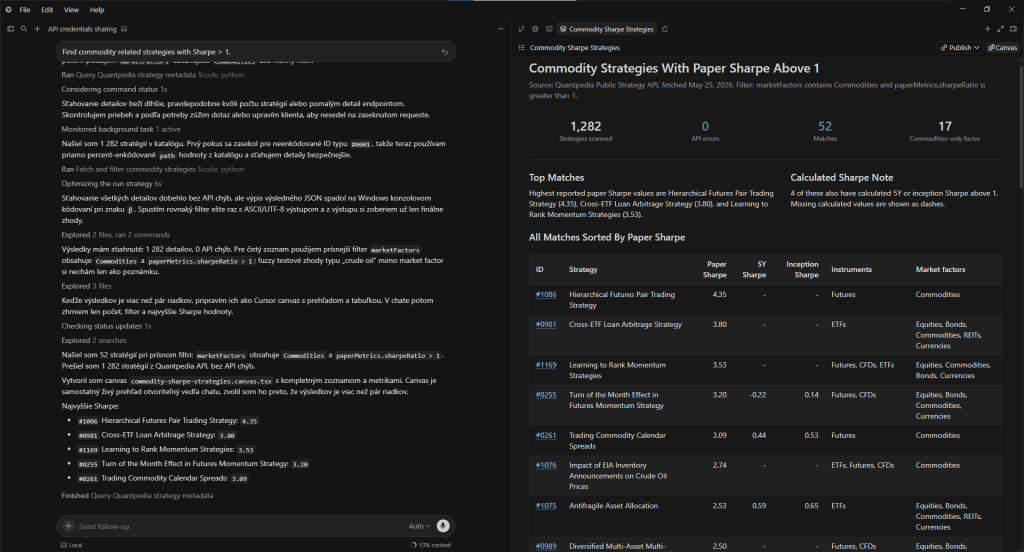

Building Meta-Strategies with Quantpedia API

Quantitative investors usually start their research by analyzing individual trading strategies. They compare performance, risk, implementation complexity, market exposure, and the economic intuition behind each anomaly. However, once historical equity curves of individual strategies are available, a different research question becomes possible. Instead of asking only which individual strategy looks attractive, we can ask how to allocate capital across a broad universe of strategies.

This is where meta-strategies become useful. A meta-strategy does not invest directly in stocks, ETFs, futures, or other financial instruments. Instead, it invests in underlying trading strategies. These strategies become portfolio building blocks, and the researcher can apply allocation rules such as momentum, risk parity, volatility targeting, or mean-variance optimization directly to their return streams.

The Quantpedia API makes this type of analysis practical. It provides access not only to strategy metadata, but also to historical strategy equity curves. Therefore, users can move from strategy discovery to systematic strategy portfolio construction.

quantpedia.com/building-meta…

#quant #api #trading #strategies

3

49

3,238

Building an AI Powered Quant Research Assistant with Quantpedia API

Artificial intelligence is gradually changing the way quantitative researchers interact with financial data. Instead of manually browsing databases, comparing strategies one by one and filtering spreadsheets, modern research workflows increasingly rely on conversational systems capable of retrieving and summarizing structured information automatically.

One practical application is combining the Quantpedia API with an LLM such as ChatGPT, Claude or Cursor AI to create a lightweight quant research assistant. In this setup, Quantpedia API provides structured access to quantitative trading strategies, performance metrics, classifications, equity curves, trading codes, and related research metadata through the official Quantpedia API, while the LLM acts as a conversational layer capable of interpreting the retrieved data and transforming it into readable research outputs.

quantpedia.com/building-an-a…

#ai #agents #algo #trading #strategies #quant #research

1

6

736

Quantpedia Days 2026 Bring Again 1 1 Special Offer

– Celebrate with us the relentless pursuit of knowledge and ingenuity

– You can now subscribe to any of our services, be it 3-, 12- or 36-months Quantpedia Prime, Premium, or Pro subscription, and get the same 2nd subscription for your co-worker or fellow researcher for free – an offer valid between 28th May and 5th June 2026

quantpedia.com/quantpedia-da…

#quantpedia #days #quant #research #algo #trading #strategies

401

Quantpedia Awards 2026 – Winners Announcement

Welcome to the Quantpedia Awards 2026 winners announcement. For the third time, we are proud to celebrate excellence in quantitative research and recognize the researchers behind innovative studies in quantitative trading. We are also pleased to see that the Quantpedia Awards have become an established and recognized brand within the quant community. This is the moment we have all been waiting for: who made it into the top five, and what will the authors of the winning papers receive?

quantpedia.com/quantpedia-aw…

#quantpedia #awards #2026 #quant #competition #trading #strategy #research #papers

2

509

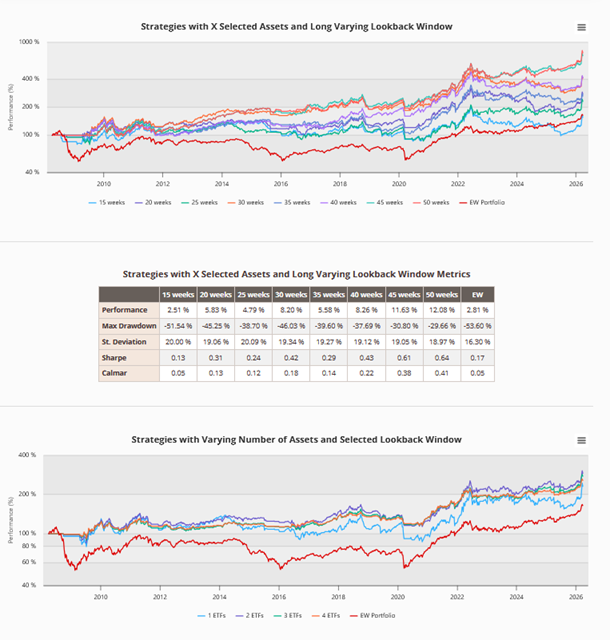

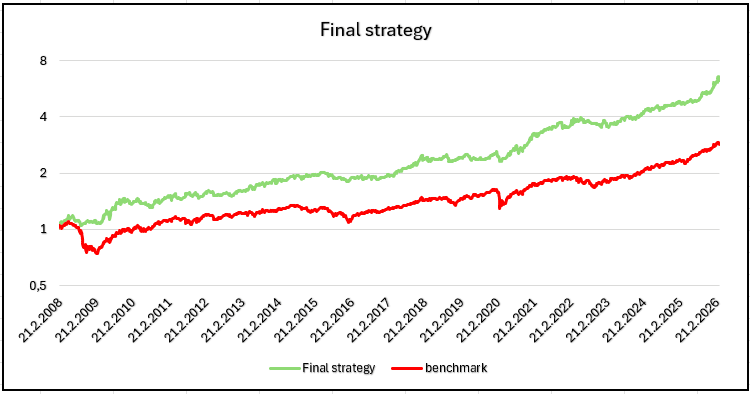

Active Dual Momentum GTAA Strategy

Our study explores a weekly-rebalanced dual-momentum-based Global Tactical Asset Allocation (GTAA) strategy applied to a diversified set of ETFs. The strategy selects assets based on relative momentum and applies an absolute momentum filter to avoid declining investments. Ultimately, a single combined strategy was created by merging two sub-strategies, incorporating both shorter- and longer-term momentum signals. Backtesting over an extended period demonstrates that this approach delivers attractive risk-adjusted returns, achieving attractive Sharpe and Calmar ratios, while maintaining lower drawdowns compared to a simple equally weighted benchmark.

quantpedia.com/active-dual-m…

1

2

36

1,775

A Century Without Data: Reconstructing Emerging Markets Equity History

For U.S. equities, fixed income, and commodities, reconstructing long-term historical datasets is relatively straightforward, and we have already explored these challenges in several previous studies. Emerging markets, however, represent a particularly interesting opportunity for historical reconstruction, as reliable long-term data is often unavailable for much of the 20th century despite the growing importance of these markets in modern portfolio construction and asset allocation. In this article, we present the framework we developed to extend emerging market histories in a consistent and economically meaningful way, enabling more robust long-term quantitative research and modelling.

quantpedia.com/a-century-wit…

#emerging #markets #eem #vwo #etf #replication #historical #data

2

13

908

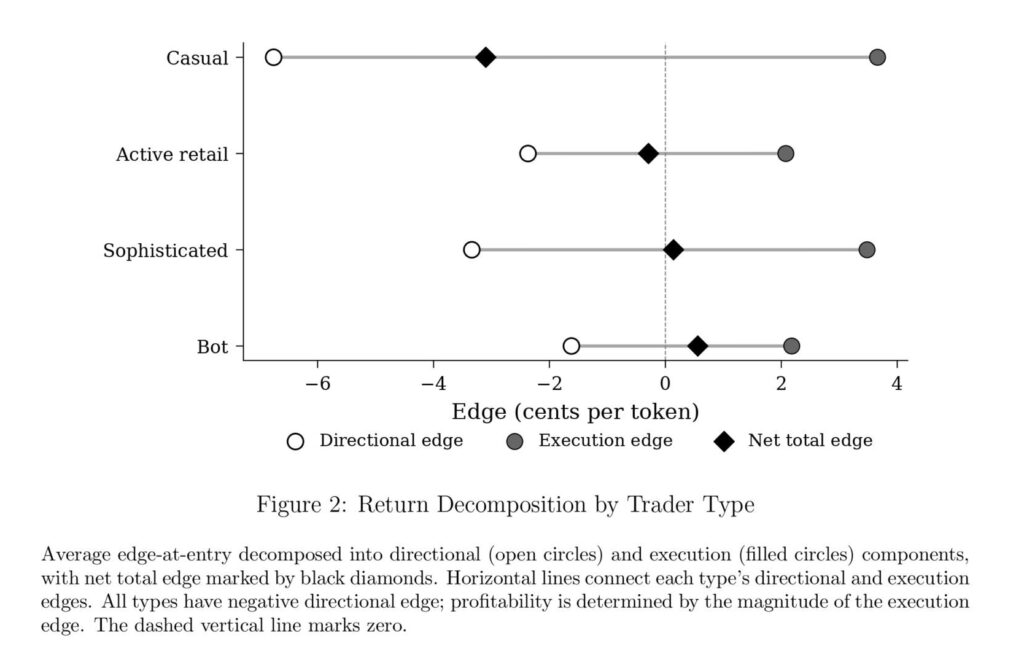

Who Profits from Prediction Markets?

In the high-stakes arena of prediction markets, a counterintuitive pattern emerges: retail traders who correctly pick winners more than half the time still lose money, while automated traders with coin-flip accuracy pocket nine-figure profits. Using 222 million prediction market trades with directly observable terminal payoffs, the paper “Who Profits from Prediction? Execution, Not Information” presents a clean answer to why it is so. The authors decompose trader returns into a directional component and an execution component, revealing that the execution component, not the directional component, determines which trader types earn positive returns.

quantpedia.com/who-profits-f…

#prediction #markets #kalshi #polymarket #trading

1

1

11

1,040

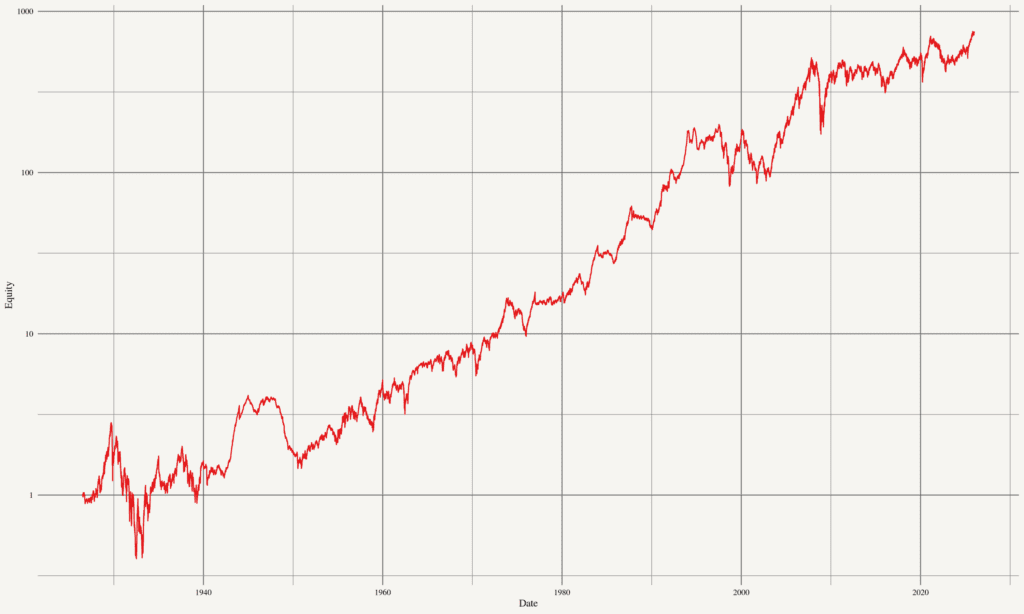

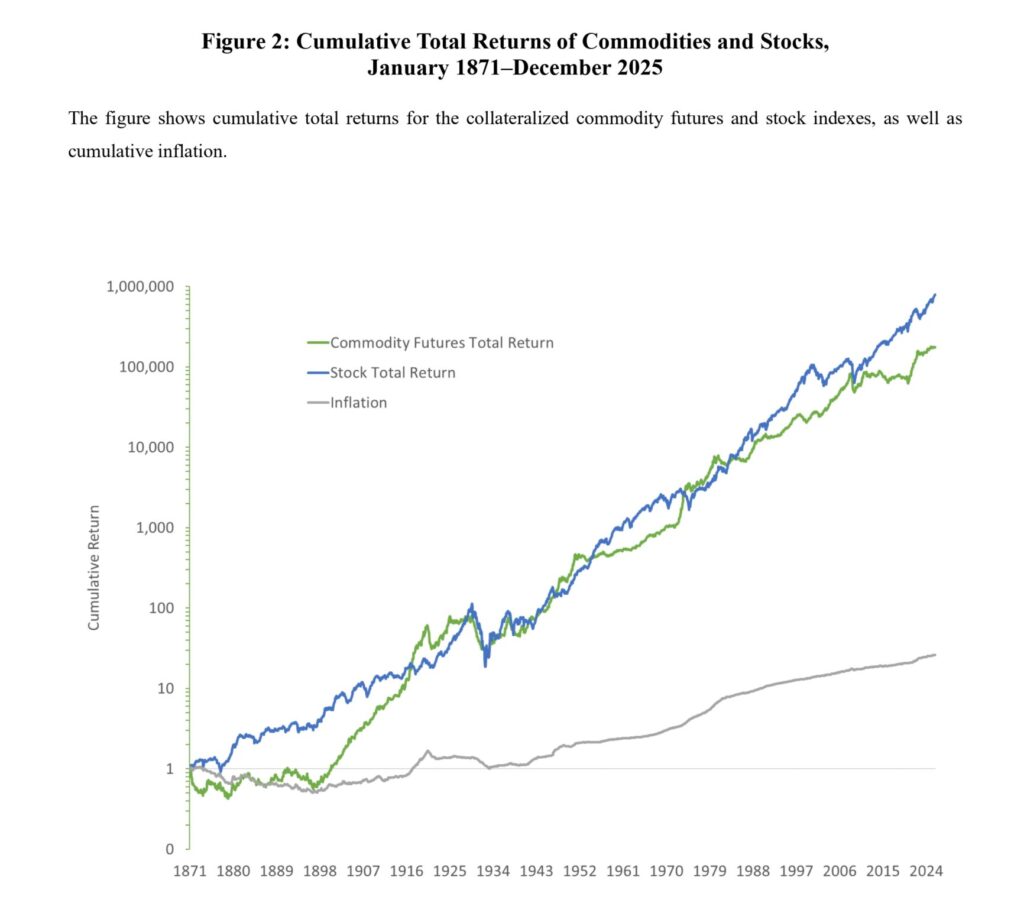

An Index of Commodity Futures Returns Since 1871

Commodity markets are back in investors’ focus. After years in which equities and growth assets dominated portfolios, the recent rise in geopolitical tensions, inflation uncertainty, supply-chain fragmentation, and renewed resource nationalism has reminded allocators that commodities remain a critical macro asset class. That is why a newly released research paper, An Index of Commodity Futures Returns Since 1871, is particularly timely. Using a hand-collected database covering more than 150 years of U.S. commodity futures history, the authors provide one of the most comprehensive long-term perspectives yet on commodity investing — showing not only that diversified commodity futures historically delivered equity-like risk premia, but also that their return drivers were meaningfully different from stocks, offering valuable diversification across economic regimes.

quantpedia.com/an-index-of-c…

#commodity #futures #investing #oil #gold #silver #copper #corn #wheat

4

24

2,608

Quantpedia in April 2026

– Expansion of Quantpedia’s API

– Introduction of Bookmarks

– Quantpedia Awards 2026 Top 10 papers

– 12 new Quantpedia Premium strategies

– 7 new related research papers

– 8 new backtests

– and finally, 8 new posts on our Quantpedia blog

quantpedia.com/quantpedia-in…

#quant #trading #strategies #quantpedia

13

1,071

Dual Momentum Allocation Between Physical Gold and Bitcoin (Digital Gold)

From the trading desk to the portfolio committee, investors face a familiar question: how should alternative stores of value fit into a diversified portfolio? This research explores that question through a systematic dual-momentum framework comparing Bitcoin and physical gold in a rules-based tactical allocation model. Rather than debating ideology, we focus on practical portfolio construction and risk-adjusted returns. The goal is to examine whether “digital gold” can complement its physical counterpart within a disciplined investment process, and whether the distinct behavior of these assets can be used to build a more effective systematic strategy.

quantpedia.com/dual-momentum…

#gold #bitcoin #dual #momentum #trading #strategy

1

3

41

3,277

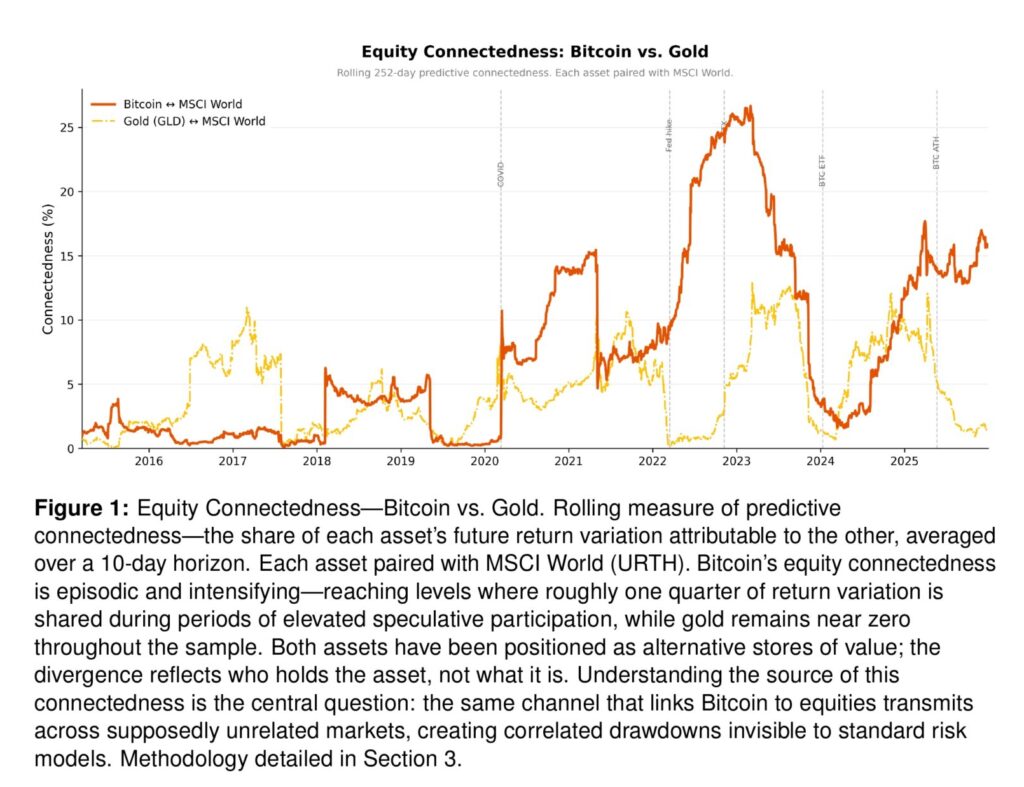

The Attention Factor: The Link That Connects Crypto and Public Equity Markets

In an era of increasingly fragmented market microstructure, the emergence of cross-asset connectedness between Crypto and public equity markets presents a critical challenge for modern portfolio construction. This blog post examines the recent working paper by Harin de Silva, “The Attention Factor: The Speculative Risk You May Already Own,” which identifies a previously underappreciated transmission channel: a speculative cohort of marginal investors whose sentiment shifts propagate correlated price movements across BTC, zero-day-to-expiration (0DTE) options, commission-free brokerages, and social-sentiment-driven equities. The author introduces the Attention factor—a capital-backed measure of collective conviction—as a systematic risk driver that persists after controlling for traditional macro factors, fundamentally reshaping how we model Equity Risk in multi-asset portfolios. For quantitative practitioners, this work underscores the need to augment conventional Risk Models with sentiment-aware factors to capture residual connectedness that standard factor frameworks may overlook.

quantpedia.com/the-attention…

#0DTE #options #crypto #bitcoin #trading

1

12

1,365

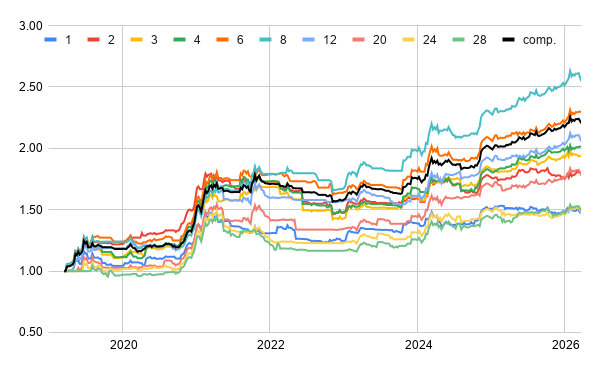

Commodity Portfolio Strategy for a Potential 2026 Inflationary and Supply Shock Regime

Commodity markets are in the spotlight. Two factors currently stand out. Firstly, the geopolitical tensions, as ongoing instability in the Middle East continues to create uncertainty in energy markets, particularly on the supply side. Secondly, less discussed are climate conditions, as the El Niño–Southern Oscillation (ENSO) is a recurring climate cycle that affects temperature and precipitation patterns globally and has historically influenced agricultural yields and supply dynamics.

Together, these forces create a plausible environment for stronger commodity performance, or at least increased dispersion across individual commodities. Instead of expressing this view through a simple buy-and-hold allocation, we approach the problem as a systematic portfolio construction task.

quantpedia.com/commodity-por…

#commodity #momentum #trading #strategy #trump #IranWar #oil

1

2

18

1,194

When Big Gets Small: Trading the Lower Tier of Large Caps and Upper Mid Caps

The growing dominance of passive investing has fundamentally altered the dynamics of equity markets. A substantial share of trading volume is now driven by index-tracking strategies, which mechanically allocate capital based on index membership rather than company-specific fundamentals. This raises an important question: can predictable flows associated with index rebalancing be systematically exploited?

quantpedia.com/when-big-gets…

#SP500 #Index #additions #deletions #stockpicking #trading #strategy

4

632

How to Analyze Individual Equity Curves

One of the advantages of the Quantpedia Pro platform and its Portfolio Analysis toolkit is the ability to analyze not only multi-asset and multi-strategy portfolios but also individual equity curves. Users can upload virtually any return series or analyze assets already present in the database. The same analytical tools used for portfolio construction can therefore also be applied to single assets.

Given the current macro-driven environment, commodity markets—particularly crude oil—offer a relevant case study. The United States Oil Fund (USO) ETF serves as a practical proxy for oil price dynamics. By analyzing its equity curve through Quantpedia Pro, we can explore whether persistent patterns, behavioral effects, or structural inefficiencies exist and whether they can be transformed into systematic trading strategies.

quantpedia.com/how-to-analyz…

#oil #trading #strategy

12

875

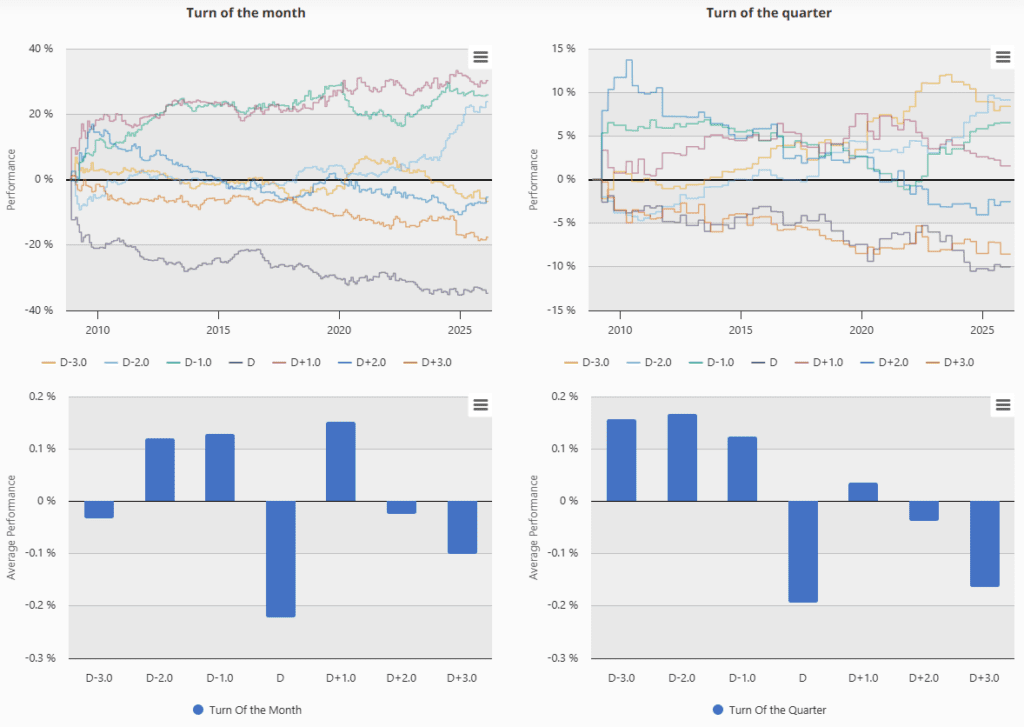

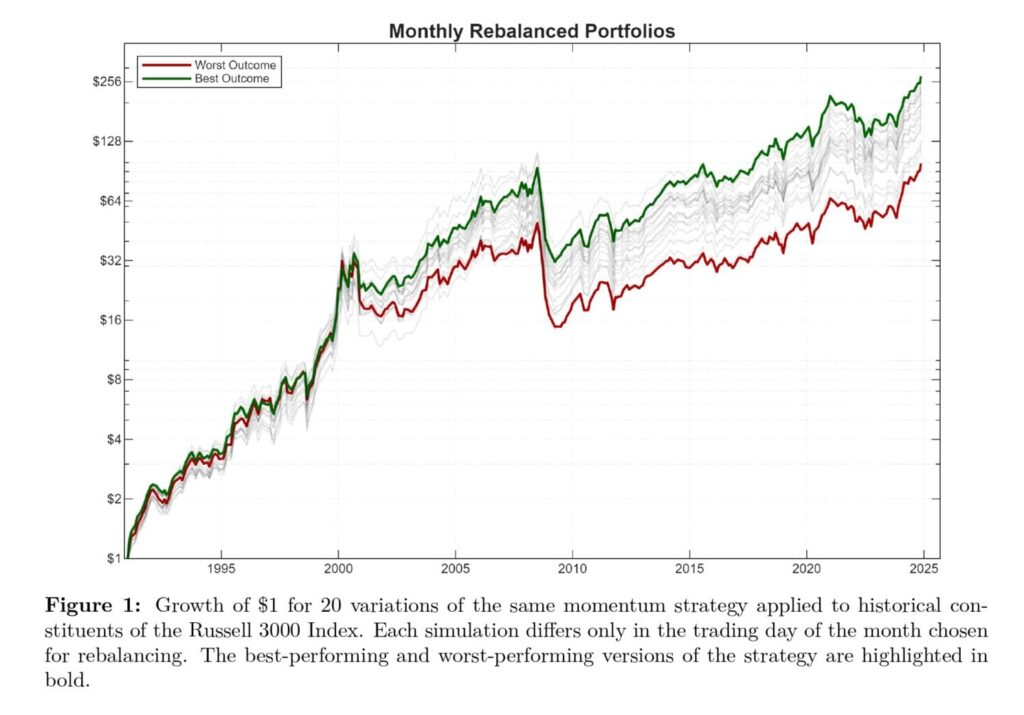

The Tranching Dilemma

What if a meaningful part of usual trading strategy’s performance has nothing to do with your signal—but simply when you rebalance? A recent paper written by Carlo Zarattini & Alberto Pagani highlights a largely underestimated risk in systematic investing: rebalance timing luck (RTL). For practitioners running rotation or factor strategies, this is not noise—it’s a structural source of dispersion. Using a concentrated U.S. equity momentum strategy, the authors show that identical portfolios differing only by rebalance day can diverge by as much as ~350 bps in annual returns, compounding into dramatically different terminal wealth outcomes.

quantpedia.com/the-tranching…

#tranching #trading #strategy #diversification

1

5

50

2,859

Exploiting Mean-Reversion in Decentralized Prediction Markets: Evidence from Polymarket Binary Contracts

This study examines the profitability of mean-reversion trading strategies applied to binary outcome contracts on Polymarket, the world's largest decentralized prediction market platform. We analyze three distinct contracts representing varying risk profiles: a quasi-risk-free instrument (No to "Will Jesus Christ return in 2025?") and two high-yield speculative contracts (No to "Will China invade Taiwan in 2025?" and "Will the US confirm that aliens exist in 2025?"). Using high-frequency price data sampled at 10-minute intervals over approximately one year, we implement a parameterized mean-reversion framework across twelve strategy variants, testing robustness under varying liquidity constraints and transaction cost assumptions. Our findings reveal that while mean-reversion signals generate substantial alpha under passive limit-order execution (zero-spread scenario), strategy performance degrades significantly when more aggressive market orders are accounted for.

quantpedia.com/exploiting-me…

#polymarket #kalshi #prediction #markets #trading #strategy

1

5

58

4,990