Investing and Trading. For information and education only, not investment advice.

Joined July 2022

- Tweets 741

- Following 796

- Followers 17,719

- Likes 971

309 Photos and videos

QuantSeeker retweeted

Jun 16

Should you build portfolios only from strongly statistically significant signals?

This recent paper suggests no.

"Out-of-sample information ratios are highest at p-value thresholds between 5% and 10%, well above levels typically advocated for false-discovery-controlled inference."

Paper by Goto and Yamada on the tension between strict significance-based selection and portfolio diversification (open access): sciencedirect.com/science/ar…

2

13

96

5,619

Jun 15

Does the Nikkei quanto spread contain a monetizable risk premium?

New paper by M. L. Tan: papers.ssrn.com/sol3/papers.…

1

7

52

3,908

Jun 14

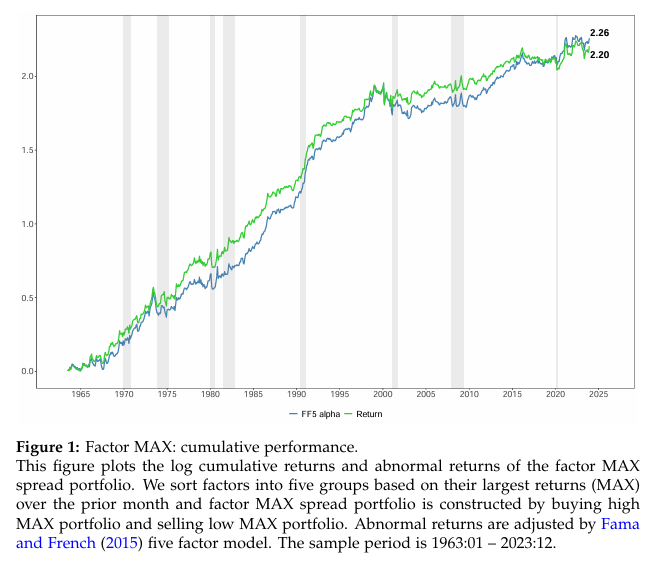

"Factors with the highest maximum daily returns in the past month outperform those with the lowest maximum returns by 0.32% per month..."

Paper by Wang and Zeng: papers.ssrn.com/sol3/papers.…

2

12

144

11,009

Jun 9

"Using S&P 500 index constituents, we construct a value-weighted Component CAPE ratio and find that it delivers economically and statistically significant improvements in long-horizon return forecasts."

Paper by Ma et al. papers.ssrn.com/sol3/papers.…

2

2

27

3,570

QuantSeeker retweeted

Mar 20

Previously, I shared Chuan Shi’s excellent lecture notes on factor investing.

Here are 4 more from the same series, covering ML, factor timing, and alternative data.

Great reading if you’re building factor strategies.

- Machine learning in factor investing

papers.ssrn.com/sol3/papers.…

- Factor timing and factor allocation

papers.ssrn.com/sol3/papers.…

- Alternative data

papers.ssrn.com/sol3/papers.…

- Behavioral finance and factor investing

papers.ssrn.com/sol3/papers.…

21 May 2025

Great lecture notes on Factor Investing by Chuan Shi:

- Intro to Factor Investing

papers.ssrn.com/sol3/papers.…

- Portfolio Sort Analysis

papers.ssrn.com/sol3/papers.…

- Regression-Based Tests

papers.ssrn.com/sol3/papers.…

- Multiple Hypothesis Testing

papers.ssrn.com/sol3/papers.…

- A Forward Looking View of Factor Investing

papers.ssrn.com/sol3/papers.…

- Factor Failure

papers.ssrn.com/sol3/papers.…

1

31

182

28,001

QuantSeeker retweeted

qoppac.blogspot.com/2026/06/… two blog posts today, going a bit hyper clearly...

2

2

31

6,281

Jun 5

"We introduce the Polymarket-v1 Database: the complete on-chain trade archive of Polymarket’s first-generation CTF Exchange on Polygon, spanning 2022-11-21 to 2026-04-28...The dataset comprises 1.20 billion trade records across 1.30 million markets..."

Paper: arxiv.org/abs/2606.04217

Dataset: huggingface.co/datasets/Time…

13

72

5,569

May 27

A new Research Recap is out. This week's topics include:

➢ Technical signals in crypto

➢ Selling vol around earnings

➢ Timing growth vs defensives

➢ Great blogs, industry research & podcasts

➢ ...and much more.

quantseeker.com/p/weekly-res…

3

1,268

May 22

Is there commodity alpha in public climate data?

Perhaps some.

Combining El Niño/La Niña signals with price-based features improves Sharpe in soft commodity futures, with the strongest predictability during major El Niño regimes.

New paper by Apte: papers.ssrn.com/sol3/papers.…

6

17

4,160

QuantSeeker retweeted

May 19

A new Research Recap is out. Topics include:

➢ Crypto options

➢ LEAPS

➢ Risk parity

➢ Predicting vol

➢ Great blogs, industry research & podcasts

➢ ...and much more.

quantseeker.com/p/weekly-res…

3

14

2,550

May 12

A new Research Recap is out. Topics include:

➢ Commodity momentum

➢ Market timing

➢ Predicting ETF returns with ML

➢ Vol scaling portfolios

➢ Great blogs, industry research & podcasts

➢ ...and much more.

quantseeker.com/p/weekly-res…

2

15

2,096

May 5

A new Research Recap is out. Topics include:

➢ Alpha in commodity markets

➢ Crypto arbitrage

➢ Do hedge-fund awards matter?

➢ LLMs for alpha discovery

➢ Great blogs, industry research & podcasts

➢ ...and much more.

quantseeker.com/p/weekly-res…

1

6

1,804

Apr 28

A new Research Recap is out. Topics include:

➢ Diversifying across commodity factors

➢ Size and momentum in crypto

➢ Short-term mean reversion

➢ Event-driven alpha

➢ Great blogs, industry research & podcasts

➢ ...and much more.

quantseeker.com/p/weekly-res…

1

9

2,004

Apr 21

A new Research Recap is out. Topics include:

➢ An improved commodity carry signal

➢ Long-short equity strategies

➢ Trading the EIA report with LLMs

➢ Predicting option returns with LLMs

➢ Trading on inflation betas

➢ Great blogs, industry research & podcasts

➢ ...and much more.

quantseeker.com/p/weekly-res…

1

4

19

4,259

Mar 24

Having a spouse in a C-suite or executive role can create a real information edge. In spouse-linked industries, these fund managers’ buys outperform peers by 4% per quarter, and their trades anticipate earnings surprises and corporate events. Alpha isn’t just skill, it’s who you’re connected to.

Paper: papers.ssrn.com/sol3/papers.…

2

5

34

4,217