Delivering multi-asset research & strategy | Provided 800 actionable trade ideas at rationaletrading.com/

Joined November 2012

- Tweets 2,392

- Following 185

- Followers 1,421

- Likes 2,080

1,514 Photos and videos

Pinned Tweet

4 Oct 2024

Rationale is my research service that provides actionable trade ideas and in-depth market analysis across equities, FX, futures, ETFs, and crypto.📊📉

Subscribe now for exclusive trade ideas👇

rationaletrading.com/

4

16

6,321

Jun 13

Trade Ideas Equities: TBBB(NYSE), BROS(NYSE), INTC(NASDAQ), AMT(NYSE), AKSA(BIST), MTY(TSX), MAU(TSX), 8316(TSE)

rationaletrading.com/p/trade…

1

1

10

331

Jun 11

$IBB - Biotech ETF is forming a symmetrical triangle just above the 200-day EMA(yellow line), with price action tightening. Monitoring the direction of the breakout.

10

663

Jun 11

The $XOM / $CVX ratio is forming a symmetrical triangle following a strong uptrend, with price compressing toward the lower boundary. A breakdown from this structure would favor $CVX over $XOM on a relative basis.

The technical setup is clear. What is driving the divergence within the same sector is the more interesting question.

4

431

Jun 9

1

4

45

10,050

Jun 8

$MS - Cup & Handle chart pattern formation breakout then moved well. Monitoring the 10-day EMA(yellow line) as it managed to act as a support along the recent run up.

May 2

Trade Ideas Equities: CMP(NYSE), TAL(NYSE), FTNT(NASDAQ), CNOB(NASDAQ), MS(NYSE)

rationaletrading.com/p/trade…

1

3

508

Jun 8

Trade Ideas Fx-Futures-Etf-Crypto: EURGBP, XPDUSD, XPTUSD, ITA(CBOE), UK100

rationaletrading.com/p/trade…

4

405

Jun 8

Yes, that is exactly the tricky part. Yields and equities do not maintain a simple inverse relationship at all times.

When yields are rising on the back of structural growth, both can move higher simultaneously. However, the relationship becomes more complex when you decompose what is actually driving yields.

Nominal bond yields reflect three components: growth expectations, inflation expectations, and term premium. If the move is growth-driven, equities can continue to perform. The concern arises when rising yields are driven by term premium or persistent inflation expectations rather than growth. In that scenario, the discount rate applied to future earnings rises without a corresponding improvement in the earnings outlook, creating a genuine headwind for equity valuations regardless of near-term earnings momentum. This is why understanding what is behind a yield move matters as much as the move itself.

Jun 7

strong growth and earnings can still push stocks up even if this breaks to the upside

1

3

1,790

Jun 7

The US10Y real rate is forming a symmetrical triangle on the weekly chart, approaching a potential breakout.

Real rates are one of the most important macro variables to monitor. They represent the return an investor actually receives after adjusting for inflation, making them the primary driver of capital allocation decisions across asset classes.

5

12

107

17,117

Jun 7

Real rates are calculated as follows:

10Y Breakeven Rate = 10Y Nominal Yield -TIPS Yield

The breakeven rate reflects market inflation expectations. When investors anticipate higher inflation, demand for TIPS increases, pushing TIPS yields lower. A declining TIPS yield mechanically widens the breakeven rate, embedding higher inflation expectations directly into the calculation.

This is why the real rate, and any directional shift in it, carries significant implications for how capital moves across equities, fixed income, commodities, and currencies.

Worth monitoring closely.

2

42

18,157

Jun 7

RATIONALE watchlist is updated!

Whether you’re tracking new trade setups or revisiting existing ones, the watchlist simplifies the process by putting all ideas in one place.

rationaletrading.com/p/watch…

3

342

Jun 6

Trade Ideas Equities: NSSC(NASDAQ), ULTA(NASDAQ), PLTR(NASDAQ), TEX(NYSE)

open.substack.com/pub/roygul…

1

4

441

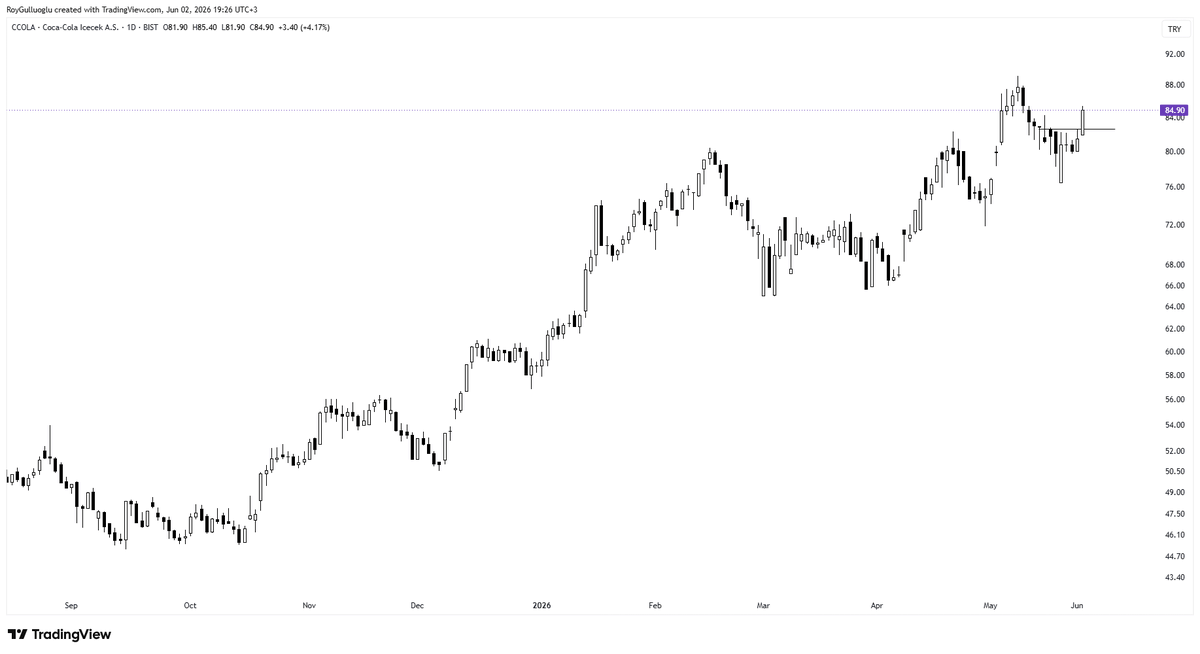

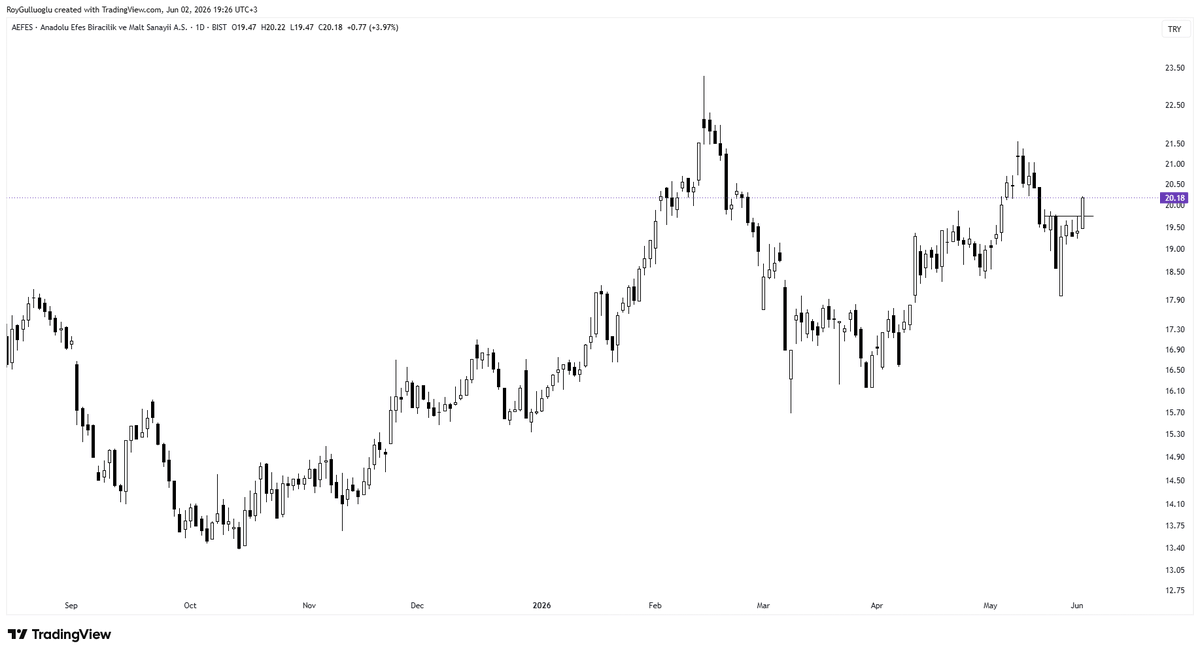

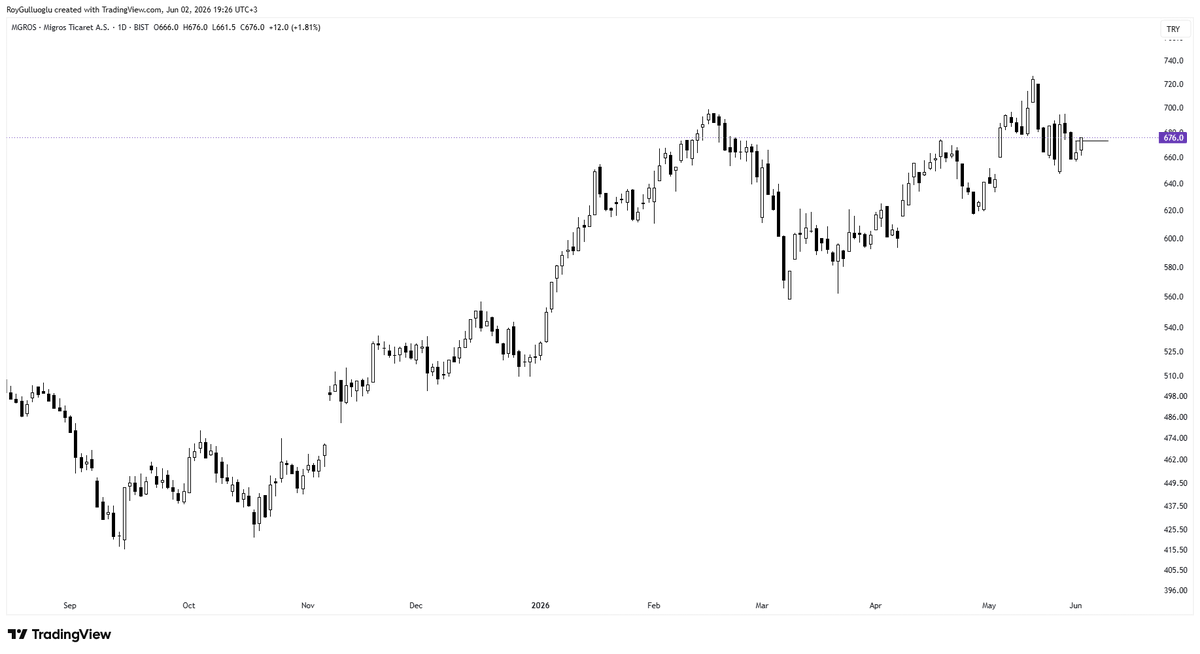

Jun 2

10

670

May 30

Trade Ideas Equities: HBM(NYSE), ATI(NYSE), ATKR(NYSE), NVAX(NASDAQ), CRDO(NASDAQ), 8795(TSE)

rationaletrading.com/p/trade…

5

360

May 23

Trade Ideas Equities: GDDY(NYSE), MNDY(NASDAQ), ATRO(NASDAQ), 8334(TSE)

rationaletrading.com/p/trade…

3

302