Exploring the intersection of digital assets, tokenization and AI. 15 years in tech consulting and product leadership.

Joined December 2022

- Tweets 701

- Following 3,488

- Followers 264

- Likes 15,192

122 Photos and videos

Jun 12

One of the most common mistakes in discussions about stablecoins is focusing on the technology before understanding the problem that it is trying to solve.

For all the advances in technology over the past several decades, moving money across borders remains surprisingly inefficient. International payments often rely on multiple intermediaries, settlement can take several days, fees can be significant, transparency is limited, and access depends on banking infrastructure that was designed long before the internet became the foundation of global commerce (this was exactly how I discovered USDT myself 😎 ).

This issue is noticeable compared to how information moves today, almost instantly and globally with very little friction. Money, however, still largely depends on systems built around banks, correspondent banking relationships, business hours and jurisdictional boundaries.

Stablecoins emerged as an attempt to address this gap by combining the stability of traditional currencies with a digital infrastructure that allows value to move more efficiently. And they are not trying to replace existing currencies. The most successful stablecoins are denominated in the same currencies that already dominate the global financial system, primarily U.S. dollar and Euro. Their value is not in creating a new unit of account, but in creating a different way for that unit of account to move through the digital economy with low fees, global coverage and instant execution.

This distinction helps explain why stablecoins have succeeded where many other blockchain applications did not achieve meaningful adoption. Rather than asking users to accept an entirely new monetary system, stablecoins allow them to continue using familiar currencies while benefiting from a different settlement infrastructure.

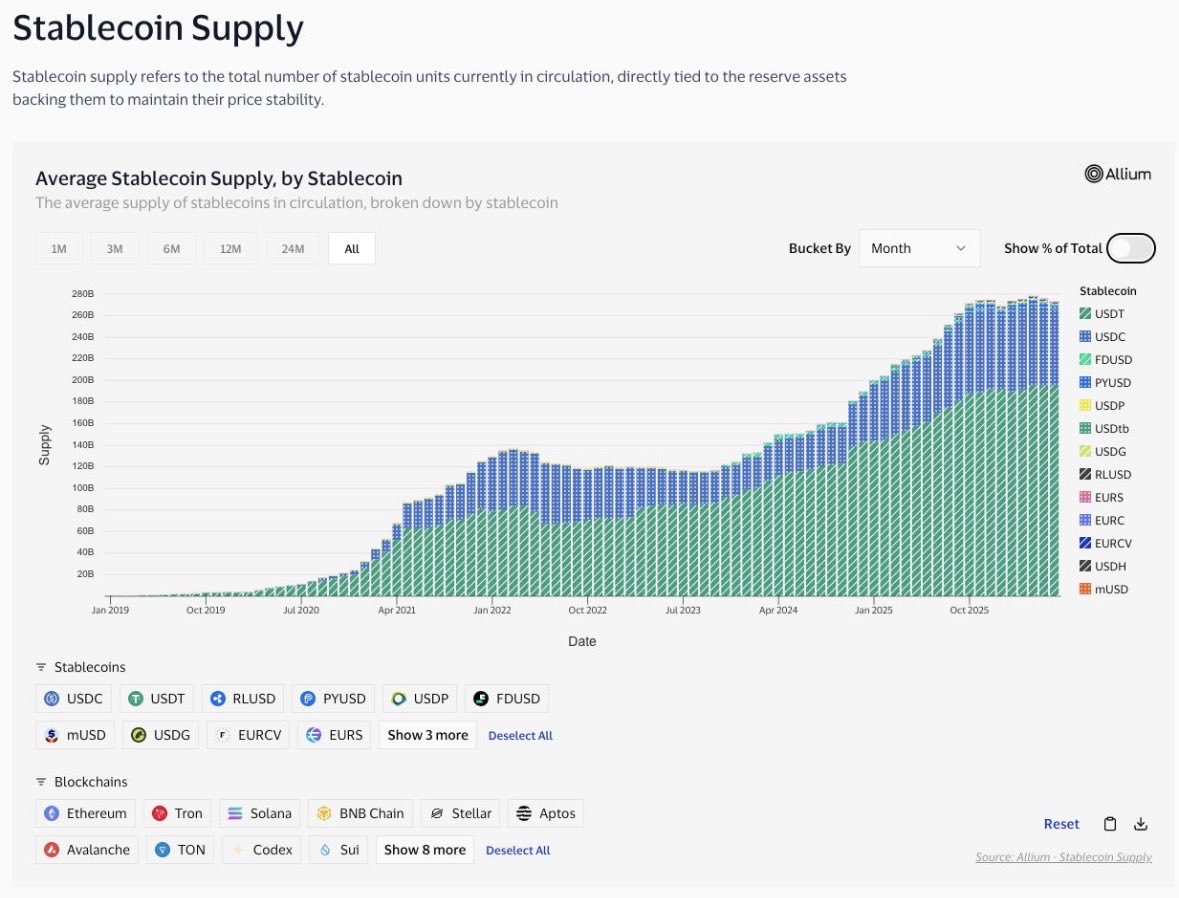

Stablecoin transaction volumes have grown rapidly. According to Visa's on-chain analytics, stablecoins processed more than $24.4 trillion in transaction volume since 2019. The total stablecoin marketcap has also grown to more than $160 billion, while major issuers such as @tether and @circle now serve tens of millions of users globally. Business adoption continues to increase, and nearly every major financial institution, including J.P. Morgan, PayPal, Visa, Mastercard, etc, is now exploring or actively developing stablecoin-related initiatives.

Stablecoins are often discussed as a separate category within digital assets, while in reality they are the first successful example of tokenization at scale. For major ones, like USDT and USDC, every token represents a claim on an underlying asset held outside the blockchain. In other words, stablecoins demonstrated that tokenized representations of real-world assets could attract users, liquidity and global adoption.

But the whole tokenization ecosystem is much broader than stablecoins, as we will see in the next parts of this series.

2

31

Jun 10

.@tether's recent win in Georgia highlights an interesting trend: 𝘀𝗺𝗮𝗹𝗹𝗲𝗿 𝗻𝗮𝘁𝗶𝗼𝗻𝘀 𝗺𝗮𝘆 𝗯𝗲 𝗯𝗲𝘁𝘁𝗲𝗿 𝗽𝗼𝘀𝗶𝘁𝗶𝗼𝗻𝗲𝗱 𝘁𝗵𝗮𝗻 𝗺𝗮𝗷𝗼𝗿 𝗲𝗰𝗼𝗻𝗼𝗺𝗶𝗲𝘀 𝘁𝗼 𝗹𝗮𝘂𝗻𝗰𝗵 𝗻𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝘀𝘁𝗮𝗯𝗹𝗲𝗰𝗼𝗶𝗻𝘀. The announcement of GEL₮, a stablecoin backed by the Georgian lari and developed in partnership with Tether, shows how countries can leverage existing private-sector infrastructure instead of spending years building a central bank digital currency from scratch.

When national stablecoins are discussed, most attention goes to the United States, EU, China, UK and Russia. Yet speed is an advantage that smaller countries often have over larger economies. They often face fewer layers of coordination, allowing them to move faster, create regulatory frameworks, partner with technology providers, and bring products to market more quickly. Many are also eager to 𝗰𝗮𝗽𝘁𝘂𝗿𝗲 𝗼𝗽𝗽𝗼𝗿𝘁𝘂𝗻𝗶𝘁𝗶𝗲𝘀 𝗶𝗻 𝗲𝗺𝗲𝗿𝗴𝗶𝗻𝗴 𝘀𝗲𝗰𝘁𝗼𝗿𝘀 𝗮𝘀 𝗮 𝘄𝗮𝘆 𝘁𝗼 𝘀𝘁𝗿𝗲𝗻𝗴𝘁𝗵𝗲𝗻 𝘁𝗵𝗲𝗶𝗿 𝗰𝗼𝗺𝗽𝗲𝘁𝗶𝘁𝗶𝘃𝗲𝗻𝗲𝘀𝘀 𝗮𝗻𝗱 𝗿𝗲𝗹𝗲𝘃𝗮𝗻𝗰𝗲 𝗶𝗻 𝘁𝗵𝗲 𝗴𝗹𝗼𝗯𝗮𝗹 𝗲𝗰𝗼𝗻𝗼𝗺𝘆, especially when positioned between larger economic powers.

Looking beyond payments, national stablecoins represent much more than a digital version of a local currency. They are:

- a way to make a national currency accessible within the global digital economy

- can reduce the cost and friction of cross-border payments

- can support international trade

- can become a foundation for entirely new financial services

For that reason, I believe the next few years will not only be about competition between USDT, USDC and other major stablecoins. We are also likely to see competition between jurisdictions seeking to become the most attractive home for digital representations of national currencies.

That is why I have decided to start a series focused on stablecoins, tokenization, as well as the overall growing intersection between digital assets and AI.

I invite you to join me as I explore this space, starting with the fundamentals, moving toward more advanced topics such as tokenization mechanics and beyond.

As always, the focus will be on practical aspects rather than abstract discussions.

3

69

May 18

This can be a great opportunity for government optimization done right.

Welcome to AI-based government.

Sensay Island 🏝️

3

48

May 11

The major local AI initiative in the market

Tether Launches Developer Grants Program to Fund Local-First AI and Payments Infrastructure

Read more:

tether.io/news/tether-launch…

4

48

May 8

The masterclass in hijacking the Google speaker’s stage, performed by @lunardragon420 at ETHPrague 😁👏

Brilliantly articulated the ‘beauties’ and benefits of CBDCs, centralized AI, and privacy-less networks.

1

3

99

Apr 30

It is now even more important to stick to privacy-oriented solutions in nowadays. Kudos to @Holepunch_to and @tether!

Apr 30

Tons of new users are joining Keet

1

65

Apr 29

This is 100% right. But especially in light of the recent AAVE and ZRO incidents, this whole area needs much stronger, more radical focus on SecOps and new insurance primitives. A single breach must not be able to push the entire DeFi sector to the edge of death.

1

131

Apr 18

AI is clearly here to stay and will reshape almost everything. But one topic that is still underestimated is - sovereignty.

And the world is moving toward a serious AI dependency trap:

Apr 17

Two futures. Only one is worth living in.

9

1

49

Apr 18

Which means more privacy, more resilience and less dependence on centralized infrastructure.

You should consider such an initiative in your AI strategy.

18

Apr 18

The company is shifted beyond stablecoins into AI, peer-to-peer infrastructure and other emerging technologies. Their on-device AI through the QVAC framework allows AI to run directly on the device (even modern smartphones!) itself instead of sending all data to external servers.

16

Apr 18

Also recent geopolitical developments have shown that the world is becoming more fragmented and dependence on foreign infrastructure became a strategic weakness.

>> That is why I would pay close attention to what Tether.io is doing <<

12

Apr 18

If those systems go offline and doctors have become too dependent on them over time, diagnoses may simply be delayed until the AI systems come back online. This creates a severe inability to execute without such systems.

12

Apr 18

If critical services become heavily dependent on AI, even a temporary outage can have serious consequences. Imagine hospitals relying on AI systems to analyze scans and identify illnesses.

10

Apr 18

In 2025 alone, AWS, Azure and Google Cloud had more than 100 service outages combined.

10

Apr 18

It is very similar to what happened with cloud computing where we have only AWS, Google and Microsoft and couple of small players. Such a centralization only becomes visible when we experience global outages.

Remember Cloudflare and CrowdStrike? There is even more!

16

Apr 18

B) The second level is the compute infrastructure centralization. Even if you build your own AI applications, you still rely on someone else’s compute, GPUs, cloud providers and data centers.

9

Apr 18

A) Most of the world consume AI from a very small number of AI providers such as OpenAI, Anthropic and Google. This creates the first level of vendor lock-in.

18

Apr 18

A) Most of the world consume AI from a 𝘃𝗲𝗿𝘆 𝘀𝗺𝗮𝗹𝗹 𝗻𝘂𝗺𝗯𝗲𝗿 𝗼𝗳 𝗔𝗜 𝗽𝗿𝗼𝘃𝗶𝗱𝗲𝗿𝘀 such as OpenAI, Anthropic and Google. This creates the first level of 𝘃𝗲𝗻𝗱𝗼𝗿 𝗹𝗼𝗰𝗸-𝗶𝗻.

9

Stan retweeted

Mar 30

If you care about financial privacy, then this is probably the most important research you will read all year.

The Dutch Court of Audits has released a paper on the effectiveness of AML measures, and lo-and-behold: it found that there is no evidence that AML actually works.

These laws are what are used to debank law-abiding citizens, throw developers in prison, surveil every transaction you make, and collect your identity in central databases that end up hacked.

Governments have built a complete and total surveillance dragnet around your finances under the guise of AML, and this Dutch Court just said the quiet part out loud:

AML is discriminatory, overly expensive, and we have no proof of it stopping crime.

Mar 30

🇪🇺🇳🇱 DUTCH COURT OF AUDITS FINDS "NO UNDERSTANDING" OF EFFECTIVENESS FOR AML APPROACH

The Dutch Court of Audits has published a paper on Anti-Money Laundering (AML) in banking, finding that "there is no understanding of the effectiveness of the anti-money laundering approach."

The paper states that "it is not clear whether the increasing controls by banks actually contribute to the prevention and detection of money laundering," while highlighting the significant costs imposed on banks.

According to the court, AML measures are discriminatory particularly towards people with foreign surnames, stating that the lack of proven effectiveness of the measures "does not establish that this distinction is justified."

The court plans to put its research into EU perspective later this year.

24

261

987

60,109