Just a nobody, passing through...

Joined June 2009

- Tweets 31,285

- Following 86

- Followers 2,236

- Likes 123,915

1,948 Photos and videos

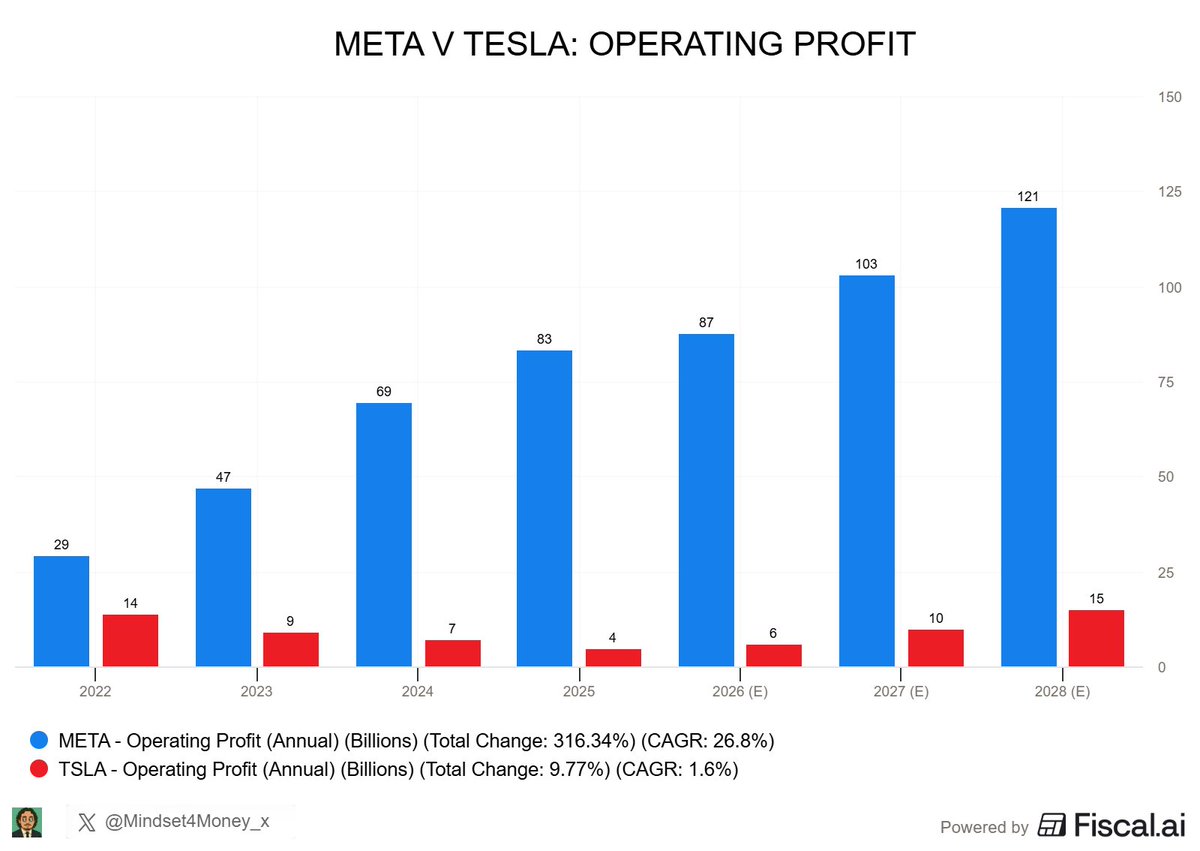

There were astronomically high expectations for Tesla’s profits promoted by ardent Tesla believers, aka (the cult), 5 years back.

Yet here we are today in Q1 2026 with Tesla posting $477 million in GAAP net income, yet with a $1.412 trillion market cap. Can’t make this stuff up.

14

17

208

8,526

Watuzzi retweeted

Apr 23

Last night was the biggest disaster in the history of Tesla.

Let me walk you through what actually happened on that earnings call, because the headlines are doing you a disservice:

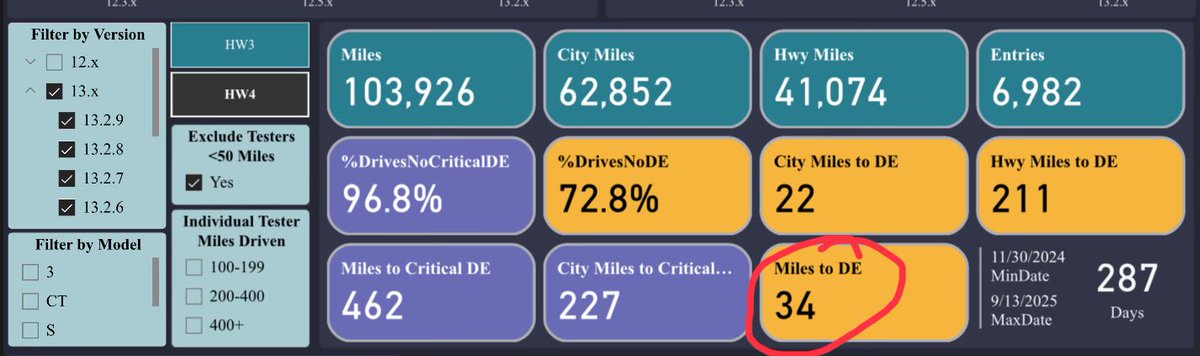

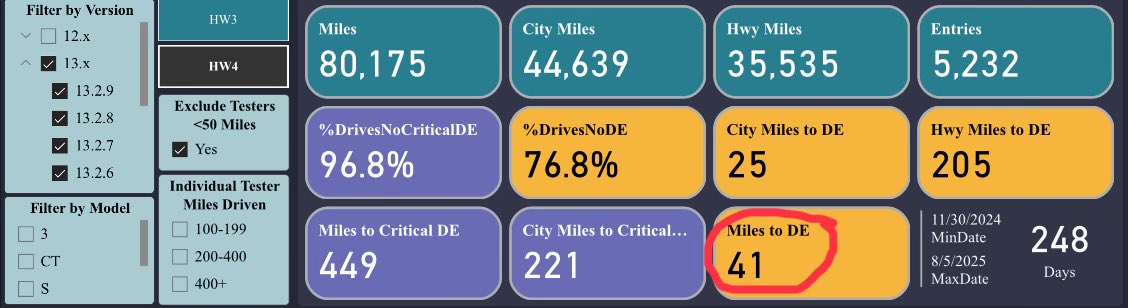

Elon Musk got on the call and admitted (his words) that Hardware 3 "simply does not have the capability to achieve unsupervised FSD."

He said he wished it were otherwise. He said the memory bandwidth is one-eighth of what Hardware 4 has. And that's the end of the conversation.

Approximately 4 million Tesla vehicles on the road right now have Hardware 3. Many of those owners paid $8,000 to $15,000 for Full Self-Driving capability based on Musk's repeated promises (going back to 2016) that the hardware was sufficient for full autonomy. As recently as 2022, Musk was publicly assuring owners that HW3 had the processing power to get it done.

BUT IT DIDN'T

Those promises are now officially broken.

The solution is a "discounted trade-in" toward a new car with Hardware 4.

Not a refund or a free upgrade...

A discount on buying ANOTHER Tesla.

Investor Ross Gerber said it too - all HW3 owners got screwed, and with roughly 285,000 FSD purchasers affected, the potential liability runs into the BILLIONS.

But that's not even the worst part.

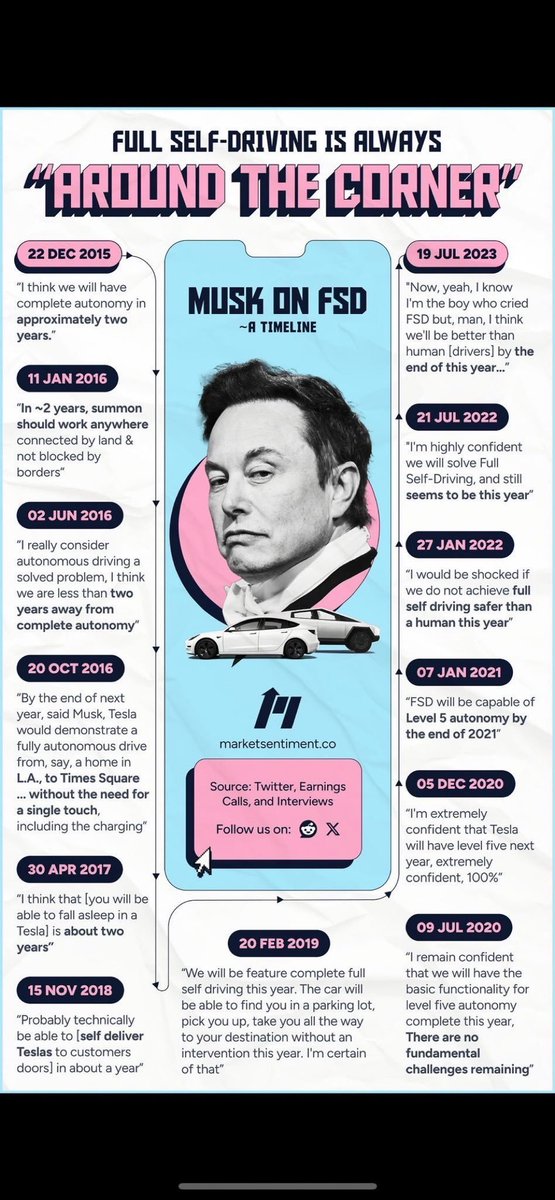

Musk was asked if the current FSD v14.3 was ready for unsupervised deployment. He said yes. Then immediately walked it back and admitted Tesla has "major architectural improvements" in the pipeline that would significantly improve safety.

What he really means: the software isn't SAFE ENOUGH to deploy without a human watching. Full unsupervised FSD for consumer cars is pushed to Q4 2026. At the earliest... Maybe.

How many times has this deadline been pushed? I've lost count. And trust me, I've seen a lot of broken promises. But this one takes the cake.

Now let's talk about the numbers everyone is celebrating:

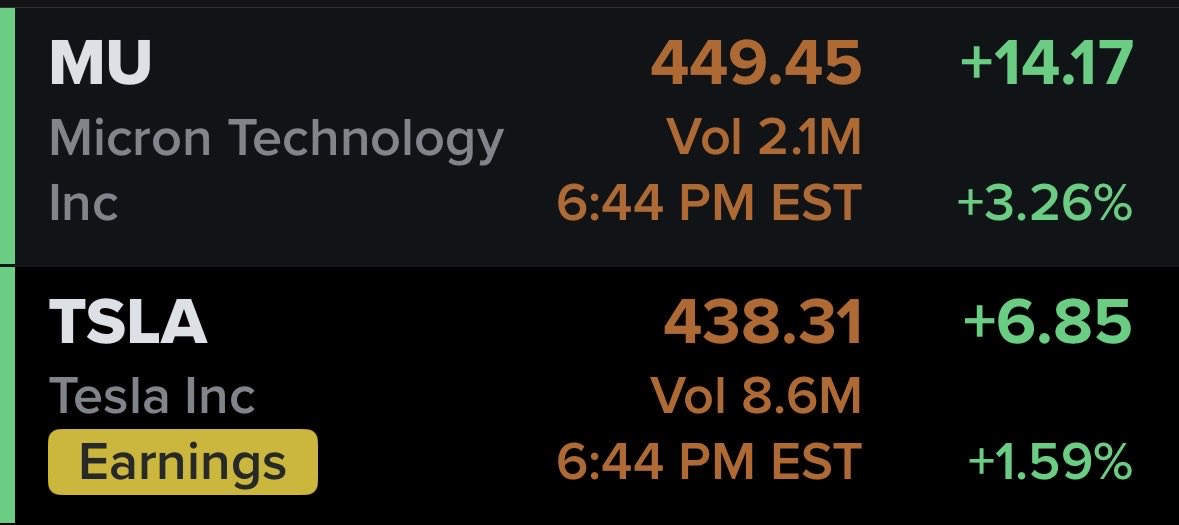

Tesla reported $22.4 billion in revenue and $0.41 in non-GAAP earnings. A "double beat." The stock popped 4% after hours. Victory, right?

WRONG

Dig into the actual filing:

The number one driver of operating income improvement wasn't cost reductions, wasn't volume growth, wasn't FSD revenue. It was - and Tesla listed this FIRST in their own shareholder letter - "one-time benefits related to warranty and tariffs."

They released warranty reserves. They booked tariff refund windfalls. They stretched supplier payments by 10 days. They took on billions in new debt. Then they presented everything through non-GAAP metrics that strip out over $1 billion in stock-based compensation.

GAAP net income was $477 million on $22.4 billion in revenue. That's a 2.1% net margin. On a $1.4 trillion market cap.

Let me put that in perspective:

3.75 billion shares outstanding. Annualize the Q1 GAAP profit and you get roughly $1.9 billion. That's a trailing P/E ratio north of 700. Use the adjusted number - strip out stock comp, which is a REAL cost to shareholders through dilution - and you're still at around 250x earnings.

All of this is extremely bad, but I didn't even talk about the CAPEX BOMB yet...

3 months ago, Tesla guided to "over $20 billion" in 2026 capital expenditure. Last night they raised it to over $25 billion. A $5 billion increase in a single quarter. That's 3x their historical annual capex run rate - $8.5 billion in 2025, $11.3 billion in 2024. The CFO confirmed on the call that Tesla expects NEGATIVE free cash flow for the rest of the year.

So you have a company generating roughly $6 billion in annual free cash flow on a good year, and they're about to spend $25 billion.

The math doesn't work.

They will almost certainly need to issue equity. Which means dilution. Which means the $1.9 billion in annual earnings gets spread across even MORE shares.

The core auto business is literally deteriorating in real time:

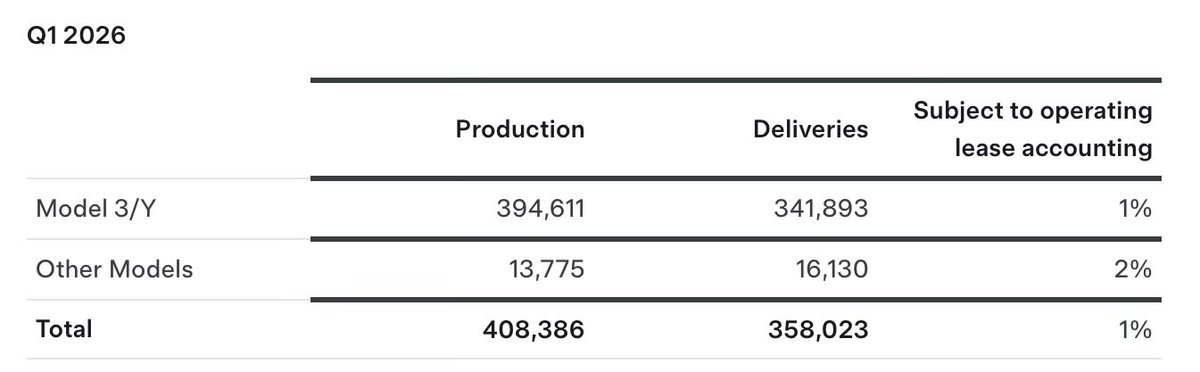

Tesla delivered 358,000 vehicles in Q1 (missed estimates again).

They produced 408,000. That's 50,000 cars sitting on lots that nobody bought.

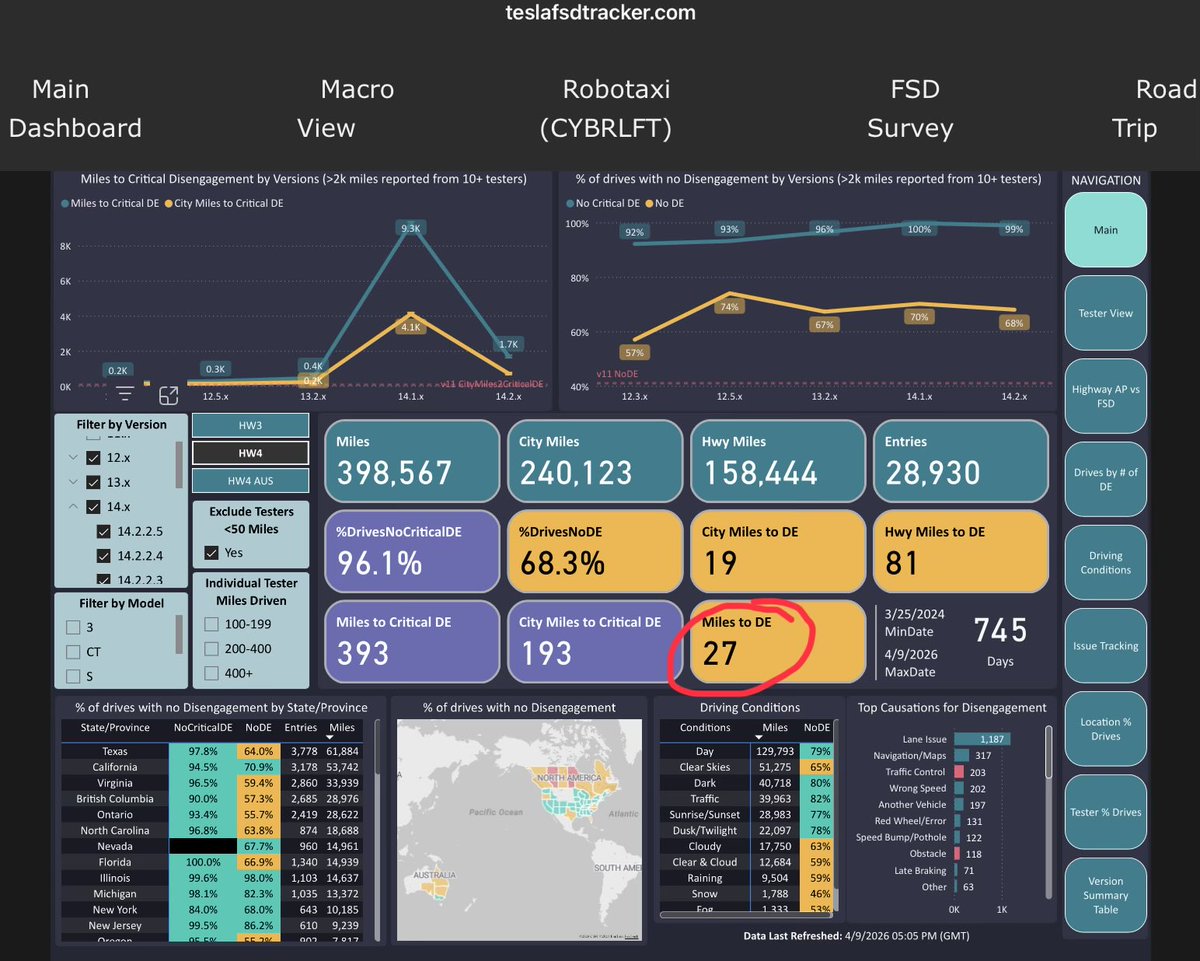

Inventory days jumped from 10 to 27 in just a few quarters. California (their most important US market) saw registrations crash 24% year over year.

Their market share in the state fell from 9.2% to 7.7%. That's on top of a Q1 2025 that was ALREADY weak from Model Y retooling. They're declining off a decline.

And here's what really kills the bull case...

The entire valuation rests on robotaxis, Optimus robots, and autonomy. So let's put numbers on it:

Waymo - the actual leader in autonomous driving with 15 million completed rides in 2025 alone, over 127 million autonomous miles driven, operating commercially across 6 US cities with plans to expand to 20 more - just raised $16 billion at a $126 billion valuation.

That's the market's verdict on what the LEADING robotaxi company is worth. $126 billion.

And Waymo is YEARS ahead of Tesla in actual deployment.

Tesla has 3.75 billion shares outstanding. So even if you assign $126 billion in robotaxi value (giving Tesla full credit for matching Waymo despite being nowhere close) that's $33 a share. Add the auto business at generous auto-industry multiples, maybe $20 a share. Throw in energy storage and services, $10-15.

Sum of the parts gets you to roughly $65-70 a share if you're feeling generous. Maybe $50 if you're not.

The stock is $387.

So what exactly are you paying for?

You're paying for a STORY. You're paying for PROMISES that keep getting pushed back, technology that keeps falling short, and a business plan that requires spending $25 billion a year while the core product sells fewer units at declining margins in a market where California sales just fell 24% and the federal EV tax credit is gone.

I managed the number one mutual fund in America. I founded two billion-dollar hedge funds. I've been doing this since 1981.

And I am telling you:

Tesla at $387 is one of the most egregious mispricings I have seen in my entire career.

THE CRASH WILL BE EPIC

1,184

2,556

10,386

1,220,078

$TSLA financial trajectory update through Q1 2026:

Operating income:

2022 - $13.7 Billion

2023 - $8.9 Billion

2024 - $7.1 Billion

2025 - $4.4 Billion

2026 - $0.9 Billion

Operating margin:

2022 - 16.8%

2023 - 9.2%

2024 - 7.2%

2025 - 4.4%

2026 - 4.2%

$TSLA financial trajectory update as of end of 2025:

Operating income:

2022 - $13.7 Billion

2023 - $8.9 Billion

2024 - $7.1 Billion

2025 - $4.4 Billion

Operating margin:

2022 - 16.8%

2023 - 9.2%

2024 - 7.2%

2025 - 4.4%

x.com/scidood/status/1948174…

14

46

231

27,656

Watuzzi retweeted

Apr 11

What stock would you not touch with a 10-foot pole?

Mine is $TSLA.

141

13

287

26,801

Tesla has been in business over 20 years. A decade ago their plan was to take over the vehicle market. Fast forward to 2026, what was propping their financial sheet up has entirely failed.

Unbelievably, $TSLA stock still garners a > $1 trillion market cap with a > 300 TTM P/E.

11

16

90

3,892

Even though all of this is very obvious to informed outsiders looking in, it’s not easy to short this type of a highly followed cult stock.

The high valuation will keep not making sense until the one day that sane investors become the majority.

7

5

43

3,481

Watuzzi retweeted

76

46

717

49,655

Nailed another one…

Say goodbye to the so called Tesla Model S and X “halo” cars. Never mind the Ciberturck never making it out of North America.

With combined worldwide sales dropping to just over 10k as of last quarter, production of these three may not last past 2026.

arenaev.com/tesla_pulls_the_…

2

3

19

2,001

With Tesla's decade old narrative of taking over the worlds auto market now obviously solidly obliterated, it was time for Tesla (Musk) to do what they're doing. That was to spitball a bunch of different company divisions and paths to keep the $TSLA stock fantasy alive.

5

3

32

1,145

$TSLA financial trajectory update as of end of 2025:

Operating income:

2022 - $13.7 Billion

2023 - $8.9 Billion

2024 - $7.1 Billion

2025 - $4.4 Billion

Operating margin:

2022 - 16.8%

2023 - 9.2%

2024 - 7.2%

2025 - 4.4%

x.com/scidood/status/1948174…

$TSLA financial trajectory update as of Q2 2025:

Tesla’s operating income:

2022 - $13.7 Billion

2023 - $8.9 Billion

2024 - $7.1 Billion

2025 H1 - $1.4 Billion

Tesla’s operating margin:

2022 - 16.8%

2023 - 9.2%

2024 - 7.2%

2025 H1 - 3.1%

77

109

1,255

326,089

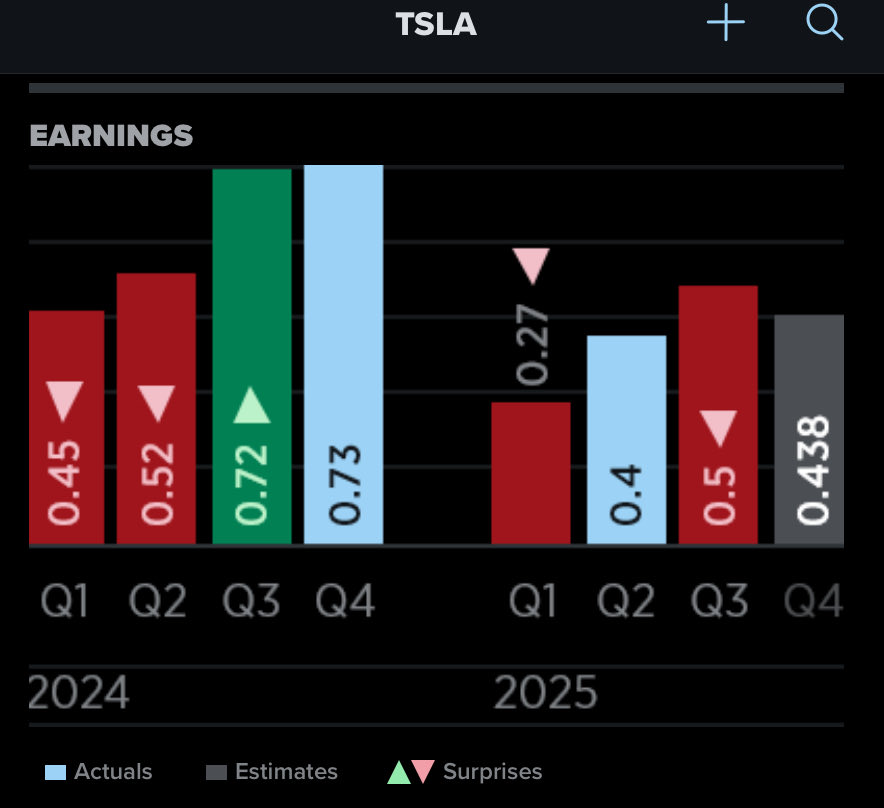

I don’t see how Tesla stays with a 4 handle in front of the stock for much longer if their earnings don’t stop dropping.

Their Q4 lowered EPS estimates now stand at $0.44 diluted. If they don’t at least meet this lower number, institutional investors may begin shedding shares.

13

6

79

6,557

It’s amazing how much a cult stock gets propped up for so long.

As Tesla vehicle sales continue their decline for a 3rd consecutive year, so do their profits. Let the Q4 EPS downgrades begin.

If $TSLA stays in the $400s through Q4 earnings release, their P/E may be in the 400s.

1

1

11

553