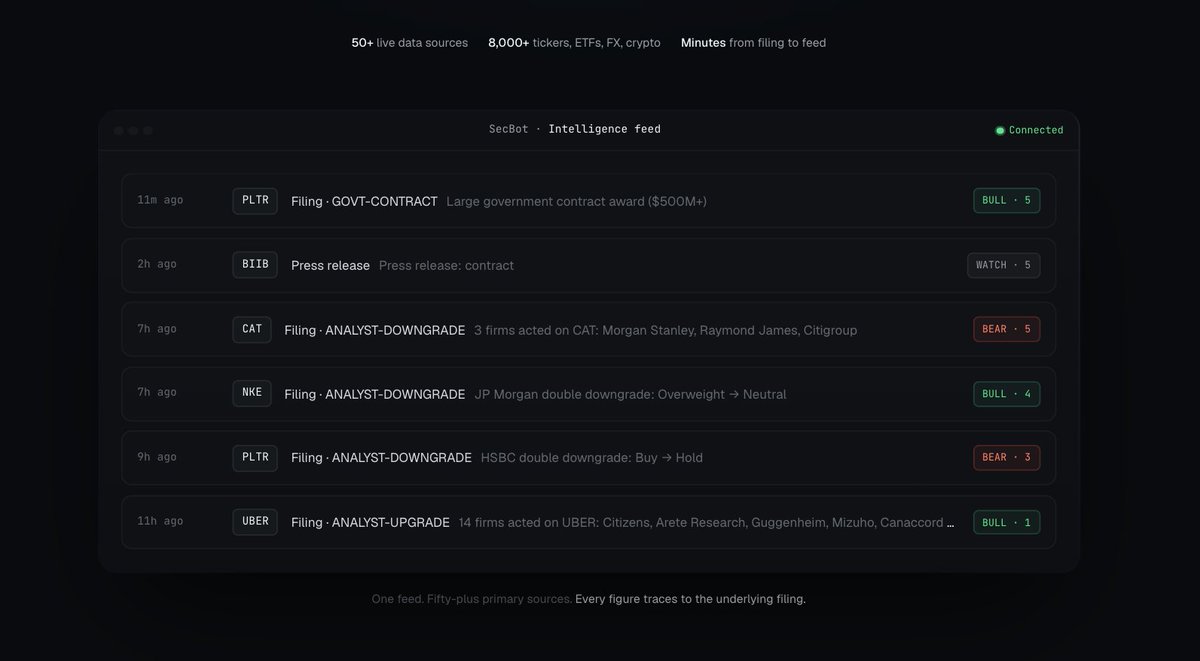

Insider clusters. Congressional trades. FDA catalysts. Regime shifts. Surfaced within minutes — grounded in primary sources, built for retail.

Joined May 2026

- Tweets 64

- Following 20

- Followers 70

- Likes 12

4 Photos and videos

Not selling a course. Not selling signals. AI that reads every filing, insider trade, analyst call, congressional trade, and FDA decision the moment it drops — and tells you which ones actually matter.

Like, follow, retweet and drop your email in the waitlist at secbot.trade for a free 14-day trial.

2

18

SpaceX went public Friday at a $2 TRILLION valuation - the biggest IPO in history, bigger than Tesla on day one.

Morningstar says it's worth $63 a share. It's trading near $178.

And thanks to automatic index inclusion, an estimated $15–20 trillion in passive funds now have to buy it, with only ~4% of shares available.

A forced squeeze on the most overvalued stock on Earth. $SPCX

2

89

Biotech didn't take the weekend off. EHA, EAACI, ENDO and ESMO gynae all ran through saturday and sunday, and the data came out in waves. Three things actually mattered.

Hereditary angioedema turned into a philosophy fight. Two companies reported within a day of each other, going at the same disease from opposite ends. Pharvaris $PHVS dropped phase 3 RAPIDe-3 on its oral pill deucrictibant — median symptom relief in 1.28 hours vs twelve-plus for placebo, 83% of attacks handled with a single capsule, 93% needing no rescue. Then intellia $NTLA put out HAELO, a one-time crispr gene edit, 89% fewer attacks that need on-demand treatment, and walked it straight into the new england journal. One bet is a pill you take when an attack hits. The other is a single dose meant to end the attacks entirely. Both worked. The market eventually has to price which model wins, and they don't both win the same patient.

Platinum-resistant ovarian cancer got crowded overnight. It's the indication that's broken a long line of programs, and this weekend two more showed up with real numbers. Zymeworks $ZYME phase 1 on its FRα adc ZW191 — 78.6% confirmed response in FRα-positive patients, still 47.4% in the FRα-negative ones, 7.6 month median pfs. Context $CNTX came in lighter, 29% response with its CLDN6 bispecific, but in heavily pretreated patients and with fast track already in hand. Early data, small numbers, but the space went from empty to contested in 48 hours.

And the one to actually slow down on: agios $AGIO. The sickle cell headline looked clean — hemoglobin response 40.6% vs 2.9% placebo, transfusion burden down 41%. But the primary endpoint, the one the trial was actually powered on, was reduction in pain crises, and it missed significance. Fatigue showed no difference either. The sNDA's already filed for accelerated approval. So the question isn't whether the data's good. It's whether the fda cares more about the endpoint that hit or the one that didn't.

A loud weekend. Monday sorts the ones that hold.

3

110

Next week has one number that matters: wednesday, the Fed and it's Kevin Warsh's first meeting as chair.

Rates almost certainly hold, so it's not the decision. It's how the new chair talks. Tone, the dot plot, the press conference. The whole "cuts are coming" trade rides on the read. Retail sales tuesday, housing wednesday. everything orbits 2pm wednesday.

2

63

How to read an insider trade (and why 90% of them are noise) 🧵:

Every week someone posts a screenshot, "INSIDER DUMPS $40M IN STOCK!", and the replies panic. Most of the time, nothing happened. The executive didn't sell a thing. Learning to tell the difference is one of the highest-value skills in markets, and it takes about ten minutes to learn.

Here's the foundation. Every officer, director, and big shareholder has to report their trades to the SEC on a Form 4, usually within two business days. It's public, free, and fast. The catch is that the filing buries the one field that matters under a pile of stuff that doesn't.

That field is the transaction code. Get it right and everything else falls into place:

P is an open-market purchase. The insider spent their own cash to buy shares in the open market. This is the signal. It's the one code that's genuinely hard to fake, because nobody writes a personal check for stock they think is going down.

S is an open-market sale. Weak signal on its own. People sell for a thousand reasons that have nothing to do with the company: taxes, a divorce, a house, diversification.A is a grant, F is shares withheld for taxes, G is a gift, M is an option exercise. These four are where the fake "insider selling" headlines come from. When an exec's RSUs vest, the company automatically holds back a chunk of shares to cover the tax bill. That shows up as code F, and a careless headline calls it a "sale." It isn't. The exec didn't decide anything. Same with gifts (estate planning) and grants (just compensation landing).

So that "$40M dump"? Pull the filing. Nine times out of ten it's a wall of F and G codes, vesting mechanics and a trust transfer, not a single dollar of conviction.

Now the second filter, and this is the one even semi-pros miss: was the trade pre-scheduled? There's a thing called a 10b5-1 plan, a program an insider sets up months in advance to buy or sell automatically, specifically so they can't be accused of trading on inside information. A sale under a 10b5-1 plan was decided long ago and tells you nothing about today. A purchase made outside any plan, the insider choosing, right now, to buy, is the version with information in it. The filing flags which is which. Always check.

Then there's the part that separates a casual reader from someone with an edge: a single buy can be random, but a cluster isn't. When two co-CEOs and a CFO all buy on the same day, with their own money, no plan, that's not three coincidences. That's a shared view forming inside the company at the moment it matters. Clusters are the highest-conviction insider signal there is, and they're invisible if you're only looking at one filing at a time.

One more layer, because not all P-codes are equal either. An insider "buying" by converting debt they were already owed into equity will still show up as a purchase, but it's a restructuring, not a bet. A founder writing a fresh personal check is a different animal entirely. The footnotes tell you which one you're looking at. Read them.

Put it together and you have a filter most of the market doesn't use: ignore the S, A, F, G, M noise, weight the discretionary, non-plan P buys, prize the clusters, read the footnotes for what kind of buy it really is. Do that and "insider selling" headlines stop scaring you, and the rare, real conviction buys start standing out.

The honest problem is scale. Doing this by hand means reading thousands of filings a week, decoding codes and plan flags and footnotes on every one. No human keeps up. That's the entire reason SecBot exists. It reads every Form 4 across 8,000 tickers, filters the noise, scores the clusters, and surfaces the handful that actually mean something. But even if you never touch the tool: now you can read the filing yourself. That's the part nobody teaches.

2

5

227

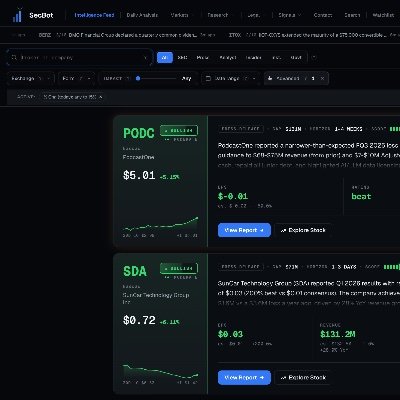

$ZCMD, $NUWE, $QTEXW - never heard of them? neither had we. All three filed dilutive offerings in the last 2 weeks. The system flagged all three as shorts. All three printed 100% or more within days. The fine print in SEC filings is a goldmine if someone actually reads it. Secbot does, every day.

3

348

CAR-T's biggest problem has always been logistics — harvesting your own cells, weeks of manufacturing. $CRBU's answer is off-the-shelf, and the new myeloma data landed: 92% response, 91% MRD-negative, half the cohort still in deep remission at 15 months. Small trial (n=12), but if allogeneic works, the whole field changes. Full data Sunday.

1

7

492