Every claim includes a direct link to the exact highlighted paragraph on SEC EDGAR

Joined April 2026

- Tweets 85

- Following 57

- Followers 22

- Likes 57

7 Photos and videos

Pinned Tweet

May 10

Hey, I'm Will, a solo founder from Sydney.

If you're like me, you like to do your due diligence before buying a stock. The problem is SEC filings are 200 pages of legal language designed to obscure as much as it reveals.

1

2

227

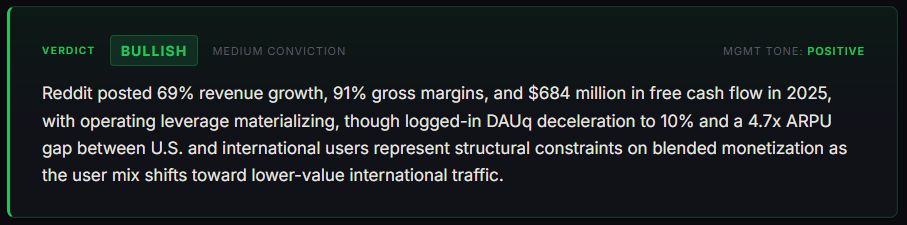

$RDDT — the 10-K verdict is BULLISH. The filing also shows this.

31% → 27% → 27% → 23% → 17% → 14% → 10% → 7%

Nine quarters of logged-in user deceleration. In Q3 2026 they're retiring the metric entirely.

The filing said it first.

1

44

Full teardown, verbatim SEC evidence throughout: sharpread.substack.com/p/wha…

7

May 26

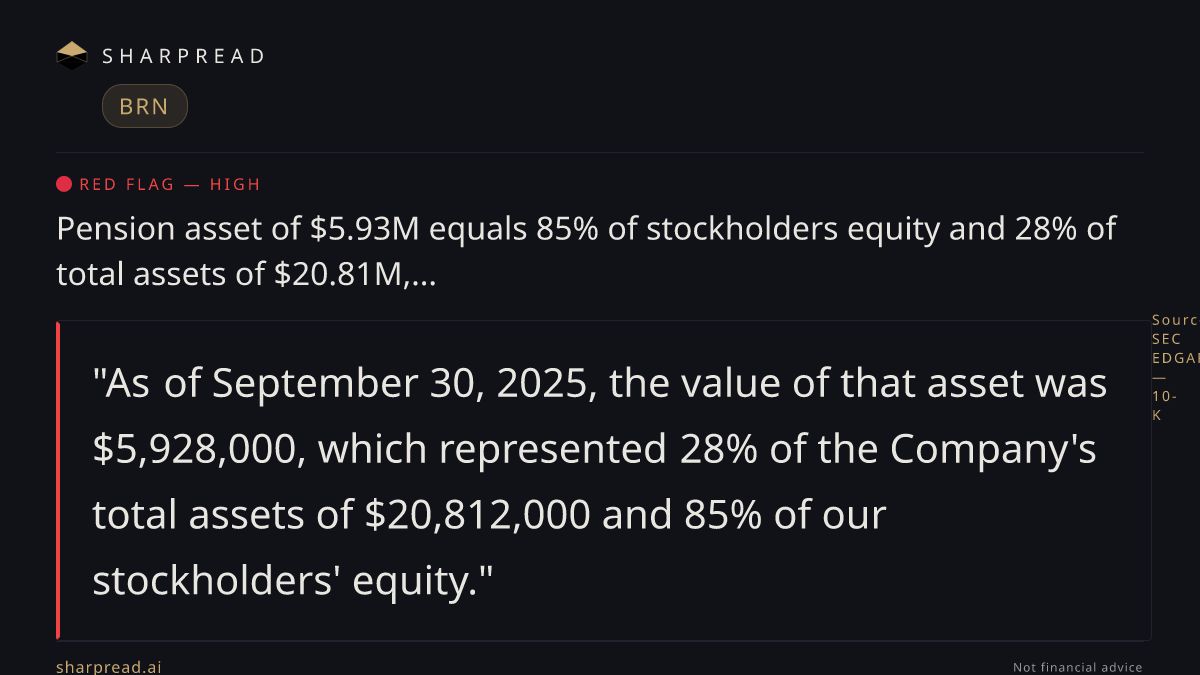

$BRN filed with $0 total debt, which sounds fine until you see a single pension asset representing 85% of stockholders equity. One actuarial swing could wipe out most of the book.

sharpread.ai/analysis/c40682…

15

May 21

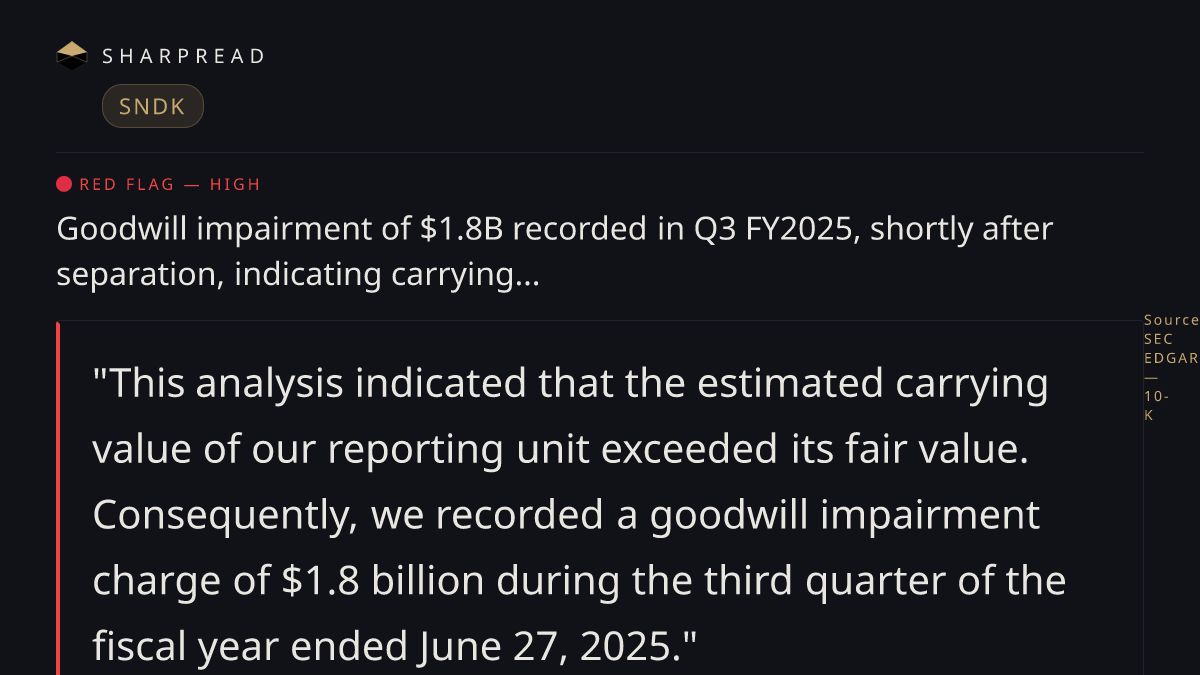

$SNDK recorded a $1.8B goodwill impairment in Q3, shortly after separation, meaning the business was worth less than its books said almost immediately after the split.

sharpread.ai/analysis/871231…

1

64

May 14

Everyone's building AI to try and predict the casino.

We took another path. Sharpread doesn't predict stock prices. It reads SEC filings and extracts exactly what management signed under penalty of perjury. We look at facts, not forecasts. The 10-K said

$BYND was in trouble months before the price reflected it. Not because our AI guessed it. Because their lawyers wrote it down.

Run your own analysis free at: sharpread.ai

2

803

May 12

$HIMS is down 15% in pre-market today on weak EBITDA guidance. The 10-K filed in February was already flagging the pressure points.

Subscriber growth decelerated 59% year-over-year while over 70% of US revenue now depends on compounded GLP-1 formulations that could disappear if the FDA removes the drug shortage designation.

At the same time, the Eucalyptus acquisition brings up to $910M in deferred obligations payable within 18 months of a mid-2026 close.

Slowing growth, concentrated revenue, and a large near-term cash obligation. The filing said this before today's call did.

What needs to be true for the bull case to hold from here?

Full filing breakdown: sharpread.ai/analysis/4b3d41…

157

May 11

$FLNC is up big. The 10-K tells a more complicated story.

New product order intake fell 34.6% in FY2025. 5.2 GW signed in 2024. 3.4 GW in 2025. That is 1.8 GW of demand that did not show up.

Management leads with pipeline growth. The filing leads with a collapsing book-to-bill.

OBBBA PFE restrictions add another layer. Treasury implementing regulations are not due until December 2026. Management explicitly acknowledges historical business impact from this kind of contracting uncertainty.

Is the backlog deep enough to carry the business while new orders recover?

sharpread.ai/analysis/956989…

101

May 11

The best thing about SEC filings is that management can’t lie in them. The worst thing about them is nobody reads them.

130

May 10

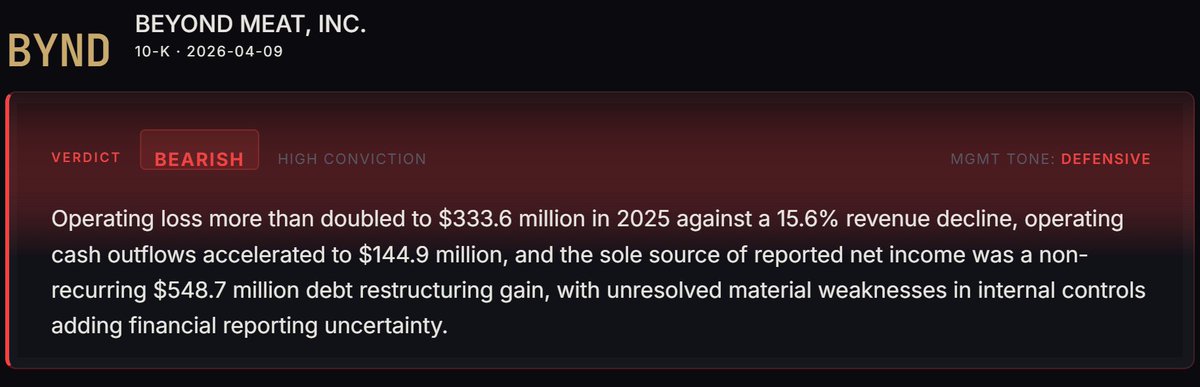

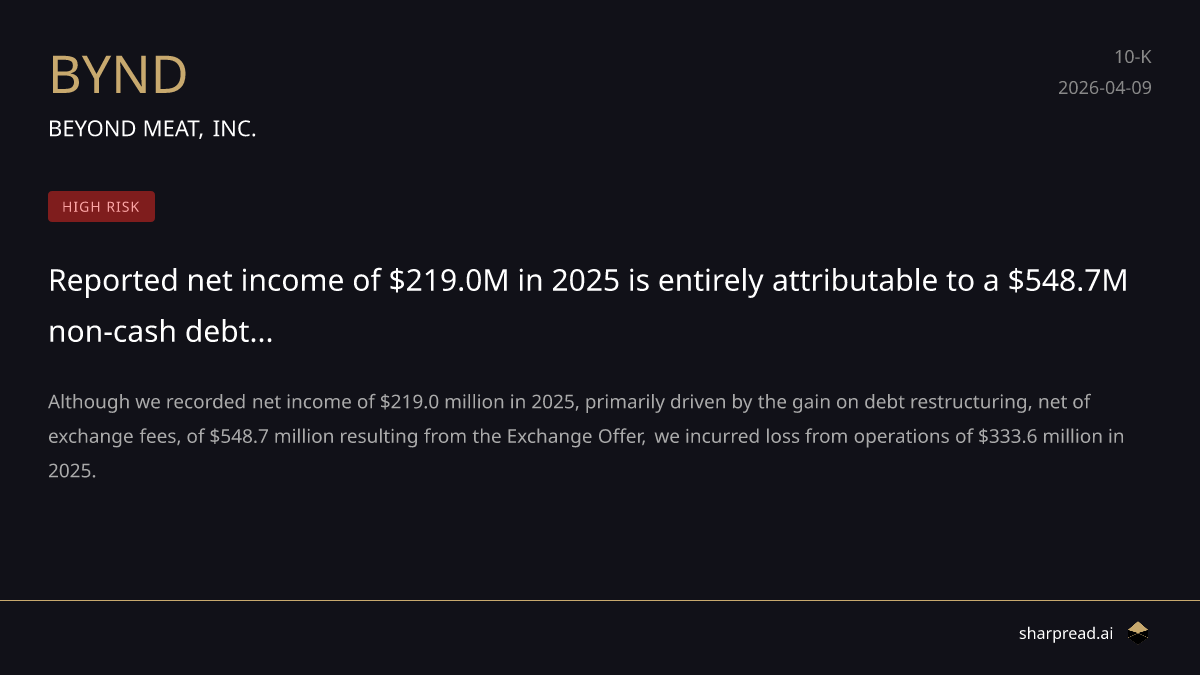

Spent some time this week going through the $BYND 10-K.

The net income line stopped me in my tracks. $219M reported profit on a company with a $333M operating loss. Same filing, same year.

Wrote up everything the filing actually said -- first Sharpread teardown, verbatim SEC evidence throughout.

sharpread.substack.com/p/wha…

6

2,598

May 10

$PLTR just posted 85% revenue growth. Rule of 40 at 145%. The earnings release reads like a victory lap.

The 10-K is a bit more measured.

A meaningful chunk of that revenue sits on contracts the customer can terminate at any time, no penalty.

Management also put in writing that they cannot guarantee profitability going forward – unusual language for a company trading at these multiples.

Not saying the bull case is wrong. Just worth knowing what the lawyers wrote down alongside what Alex Karp said on the call.

Full filing breakdown with verbatim SEC evidence:

sharpread.ai/analysis/29d8b2…

1

202

May 10

Hey, I'm Will, a solo founder from Sydney.

If you're like me, you like to do your due diligence before buying a stock. The problem is SEC filings are 200 pages of legal language designed to obscure as much as it reveals.

1

2

227

May 10

Here is what that looks like in practice.

$NOW trades at a massive premium. But their 10-K shows GAAP operating income of $1.8B against a reported Non-GAAP of $4.1B. That $2.3B gap is almost entirely stock-based compensation.

The filing was right there. Most people just never read it.

sharpread.ai/analysis/b476c6…

1

2

97

May 10

Run any ticker free at sharpread.ai

No credit card. No AI-guessed numbers. Just the actual filing.

sharpread.ai

1

57

May 9

$INOD is up 48% on "AI growth." The 10-K tells a different story.

One customer = 58% of all revenue. 30 to 90 day cancellation notice. Zero binding purchase commitments.

Stock-based comp tripled while headline earnings looked clean.

One-client consulting firm. Trading like an AI monopoly.

sharpread.ai/analysis/19f3af…

140