Joined February 2023

- Tweets 3,717

- Following 122

- Followers 69,581

- Likes 5,385

1,087 Photos and videos

Pinned Tweet

May 14

Inside Spark’s loss absorption & risk frameworks.

Spark’s security architecture is designed around:

• bounded capital movement

• explicit loss absorption layers

• coordinated liquidity management

• multi-layered oracle systems

• constrained automation under governance-defined limits

This deep dive breaks down how Spark structures risk, liquidity, and loss absorption across Spark Savings, SparkLend, and the Spark Liquidity Layer before losses propagate toward user deposits.

Including:

• updated loss absorption waterfall

• Prime Agent risk capital

• Genesis Capital Backstop

• oracle and killswitch architecture

• programmatic liquidity coordination

• constrained allocation design under stress

Security by design.

Resilience by architecture.

See what sits between losses and user deposits: paragraph.com/@spark-11/spar…

13

19

81

28,400

Jun 12

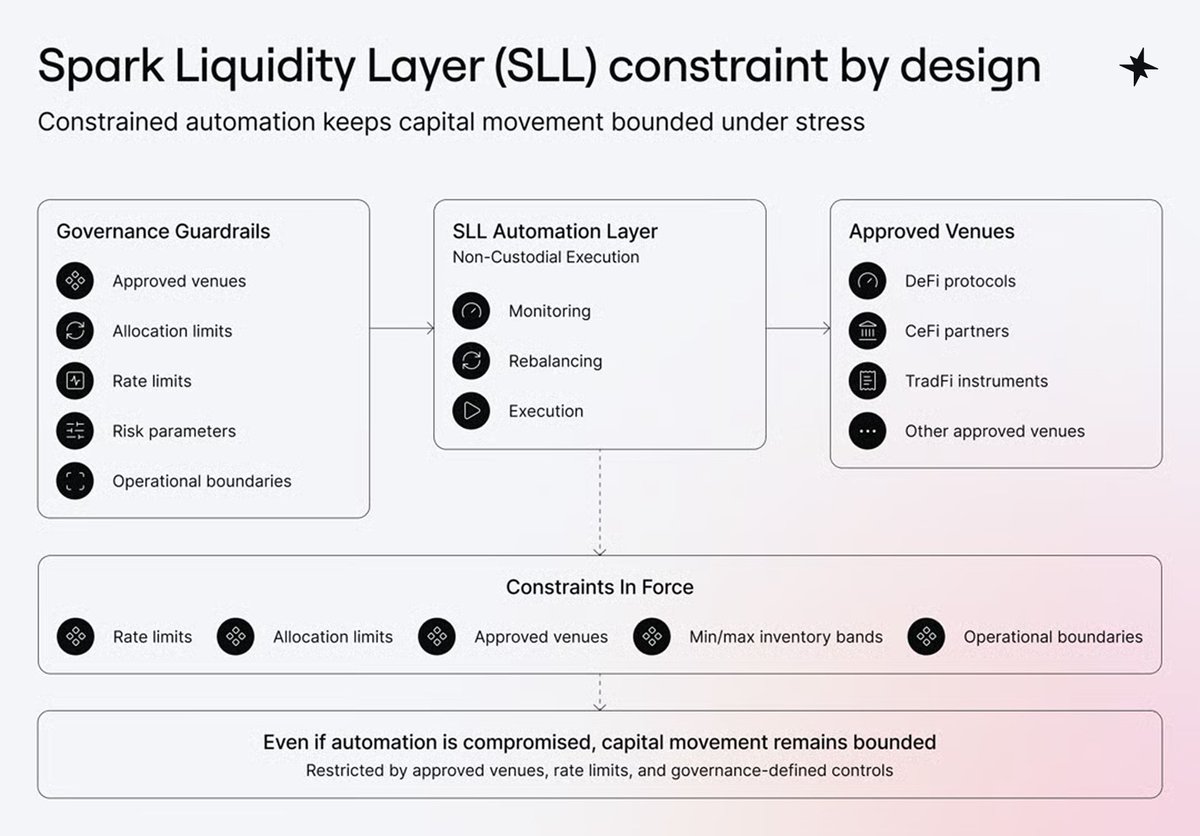

Automation creates value only when its range of motion is bounded.

Liquidity orchestration faces exactly this design problem. Capital needs to move quickly across venues, but speed should never become unbounded exposure.

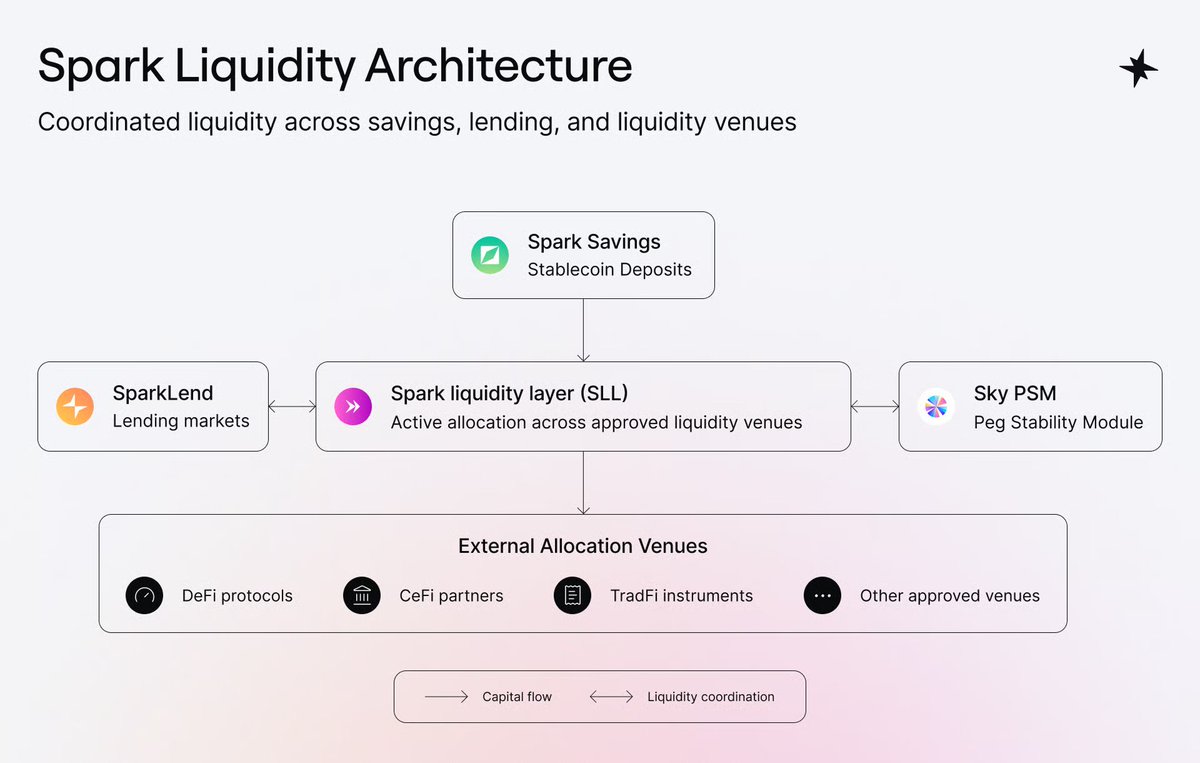

Spark Liquidity Layer handles it through governance-defined constraints.

Approved venues define where capital can move. Allocation limits and rate limits define how much can move, and how quickly. Min/max inventory bands cap how much can sit in any single venue.

The automation layer still monitors, rebalances, and executes, all inside constraints already in force before execution begins.

That is the security property. Even if automation is compromised, capital movement stays bounded.

For institutional liquidity infrastructure, automation is not the trust assumption. The constraint system is.

Read the full security framework here:

paragraph.com/@spark-11/spar…

2

5

28

2,096

Jun 12

Spark Savings is now native inside @Rabby_io ⚡️

️

This is more than an integration.

It’s a glimpse of where wallets are going: from holding assets → helping users put idle capital to work safely, instantly, and without leaving the wallet.

With Spark x Rabby, users can now earn on USDS, USDC, USDT, and ETH directly inside Rabby.

No bridges.

No extra steps.

No fragmented UX.

For Rabby users, this means idle assets can now earn directly from the wallet they already trust.

This trust is now reinforced by the Spark Savings Risk Framework, with its risk absorption layers which means SAFETY FIRST INSTANT REDEMPTION.

4

5

51

2,610

Jun 11

One of the hardest problems in credit markets is balancing liquidity and deployment.

Hold too much capital in reserve and returns suffer.

Deploy too much capital and liquidity suffers.

Spark's Liquidity Layer holds $1.11B of USDT across two roles.

$571M sits as plain USDT in the ALM proxy. That's the idle liquidity buffer. Most withdrawals clear instantly against it. Larger exits go through a request flow.

$545M is deployed into SparkLend's USDT pool as spUSDT, earning the benchmark rate.

Same asset, two different jobs. The split is what lets Spark Savings USDT offer real liquidity depth and a competitive return at the same time.

Deposit USDT: app.spark.fi/savings/mainnet…

5

9

34

2,229

Spark retweeted

Jun 11

While Mythos is changing the security threat model in some ways, I am not particularly concerned about exploits being found in blue-chip smart contracts.

If the code base is small and important enough (most SC code is), then traditional methods are sufficient to achieve high confidence in security.

What's changing is the cost of searching for exploits in large codebases. These bugs were always there, but we are compressing the time to discover them.

This is largely what is driving the recent infrastructure compromises affecting everyone. With smart contracts, this can be protected against using rate limits and timelocks, limiting the damage that can be done if an off-chain system is hacked.

Overall, this is a period of understandable apprehension, but I'm confident that by following best practises we can make it to the other side stronger than before.

9

6

61

6,055

Jun 9

Institutional capital held in custody can now now access on-chain credit markets through structured allocation via Spark.

Through BitGo, capital can be deployed into Spark Savings vaults, where it is allocated across multiple credit venues within a single, structured system.

Most on-chain lending requires selecting a single market or pool.

Spark takes a different approach:

Capital is deployed across venues based on predefined liquidity, exposure, and allocation parameters, rather than remaining fixed within one market.

Reducing exposure to high-utilisation conditions where liquidity becomes constrained.

This is a new path for institutional capital into on-chain credit markets.

Spark is now available via @BitGo institutional wallets.

26

16

77

28,116

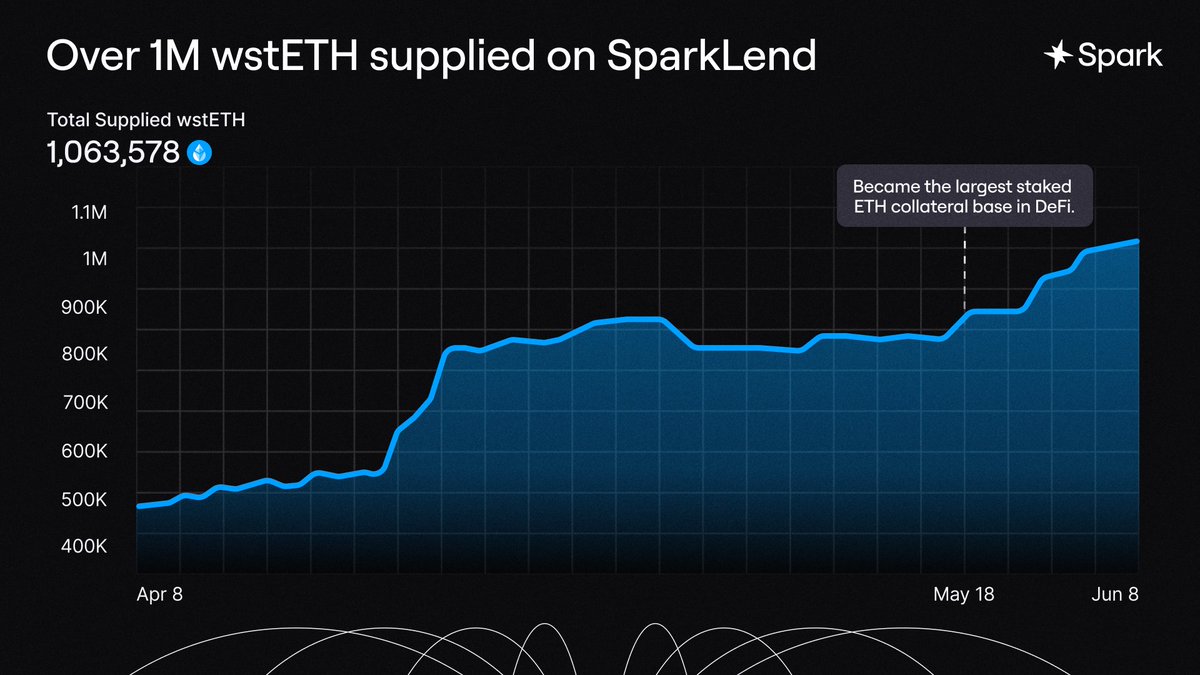

Jun 8

1M wstETH now backs SparkLend credit.

Over the past week, more than 228K wstETH was added to SparkLend.

The total supplied is now over 1M making Spark the largest wstETH collateral venue in DeFi.

Today, roughly 44% of all supplied collateral on SparkLend is wstETH.

Using staked ETH as collateral is common across DeFi lending.

SparkLend's distinction is scale.

The growth reflects a broader trend:

More ETH holders are seeking liquidity without giving up staking exposure, making staked ETH an increasingly important source of collateral across onchain credit markets.

Explore the market: app.spark.fi/markets

11

7

50

7,206

Jun 5

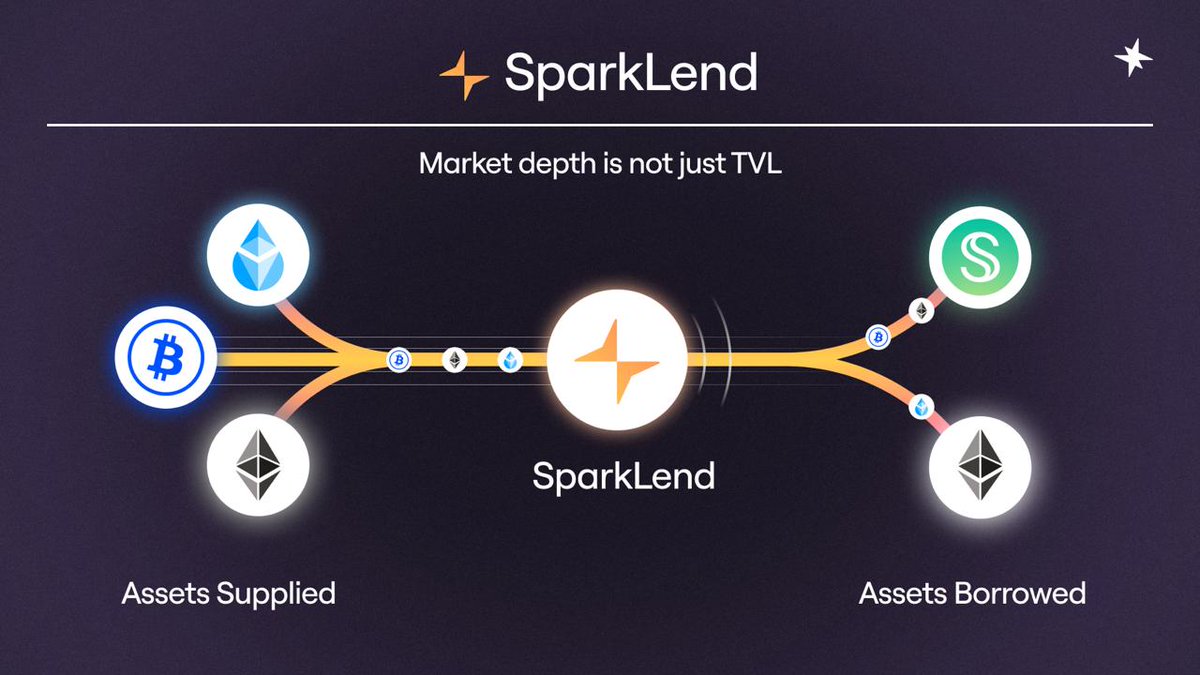

Most lending markets end up dominated by a single trade.

BTC holders borrowing stablecoins.

ETH loopers leveraging exposure.

Stablecoin borrowers chasing liquidity.

This week on SparkLend, all three were active at the same time:

→ ~$44M cbBTC supplied, $17M USDS borrowed

→ ~$34M WETH supplied, $25M USDS borrowed

→ ~$16M wstETH supplied, $15M WETH borrowed

Different collateral. Different strategies. Different market views.

More than $120M in combined collateral activity moved through the market, yet rates remained stable and no single cohort crowded out another.

That's what market depth actually looks like.

Not just TVL.

A market that can support multiple large borrower profiles simultaneously without breaking price efficiency.

Visit SparkLend: app.spark.fi/borrow

5

10

52

2,875

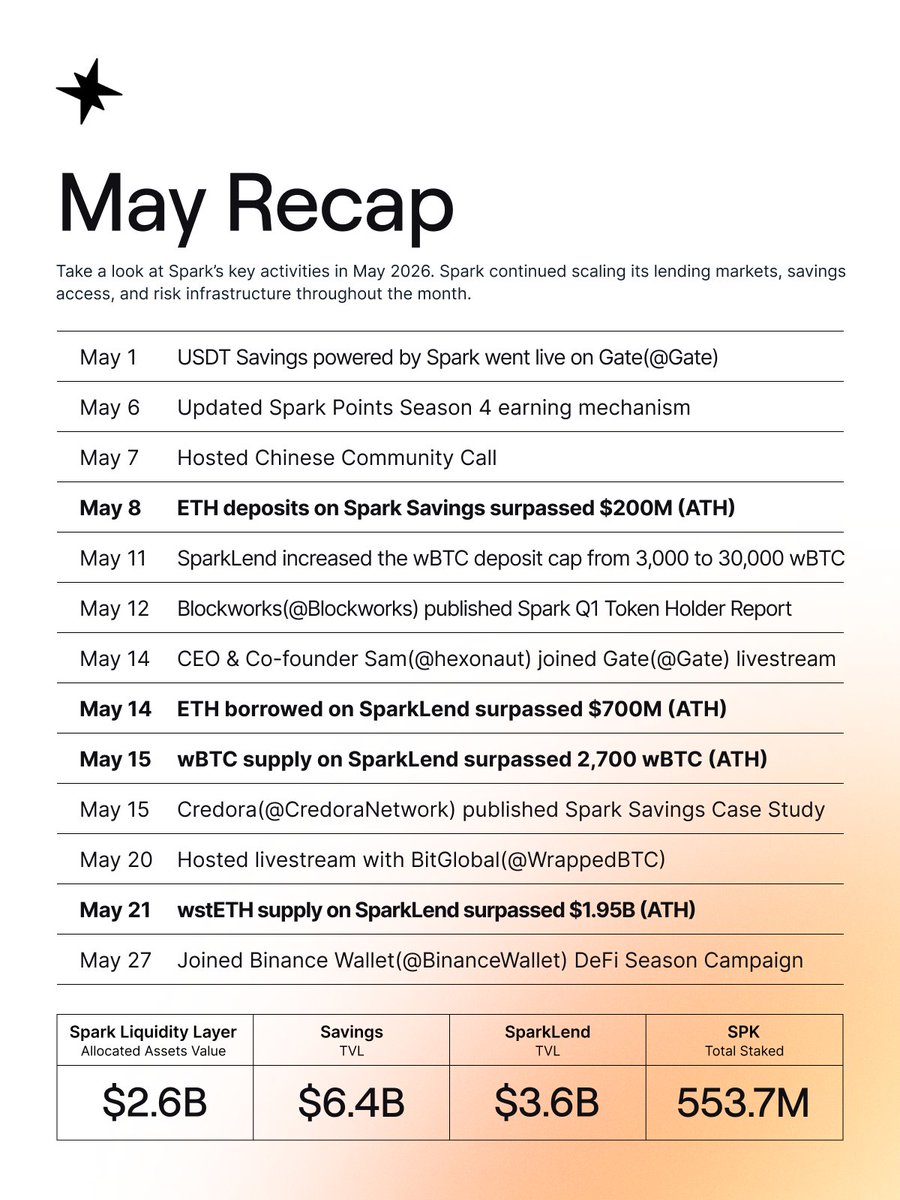

Jun 4

Spark closed May with $6.4B in Savings TVL, $3.6B in SparkLend TVL, and $2.6B deployed through the Spark Liquidity Layer.

Behind those numbers: four new ATHs, new integrations with @Gate and @BinanceWallet, and wBTC supply limits expanded 10x.

Here's the month in full. ⚡️

10

8

40

2,502

Jun 3

Most institutional strategies don't operate in a single venue.

Collateral sits with custodians. Execution spans exchanges. Exposure can extend across both DeFi and CeFi simultaneously.

Spark Prime extends overcollateralized lending across those environments under a unified risk framework.

A deep dive from @hexonaut on the future of prime financing and how M1 Capital is using the infrastructure today.

6

16

49

7,857

Jun 3

A portfolio is not a collection of isolated positions.

Yet much of crypto credit infrastructure still treats it that way.

Institutional trading firms manage exposure across exchanges, venues, and strategies simultaneously.

Evaluating each position independently can overstate the risk that actually matters: the portfolio as a whole.

That's why portfolio-based margining matters.

Spark Prime uses @ArkisXYZ technology to evaluate exposure across DeFi and CeFi venues, allowing financing decisions to reflect net portfolio risk rather than treating each position in isolation.

Read more about Spark Prime👇

paragraph.com/@spark-11/spar…

3

44

54

15,138

Spark retweeted

Jun 2

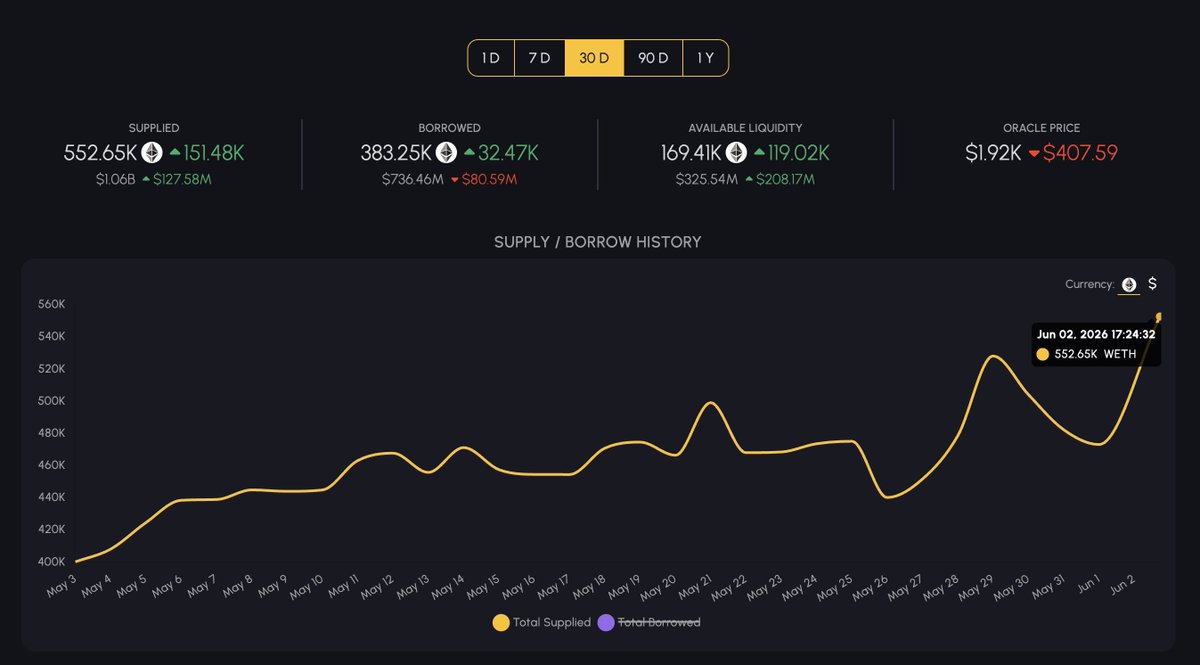

ETH deposits on SparkLend hit a new ATH of 552k.

Up 38% in the past month.

5

1

45

3,371

Jun 2

Spark Savings is not designed around static idle liquidity alone.

Vaults maintain liquidity buffers for standard withdrawals. Larger requests can be handled through signed withdrawal intents, with liquidity coordinated across the broader Spark and Sky system.

For USDT, the vault maintains an immediately available redemption buffer exceeding $10M.

For USDC, Spark Savings has access to billions in redemption capacity through the Sky PSM.

The point is coordinated redemption capacity, not idle liquidity alone.

Read the full security framework here:

paragraph.com/@spark-11/spar…

4

5

30

2,720

Jun 1

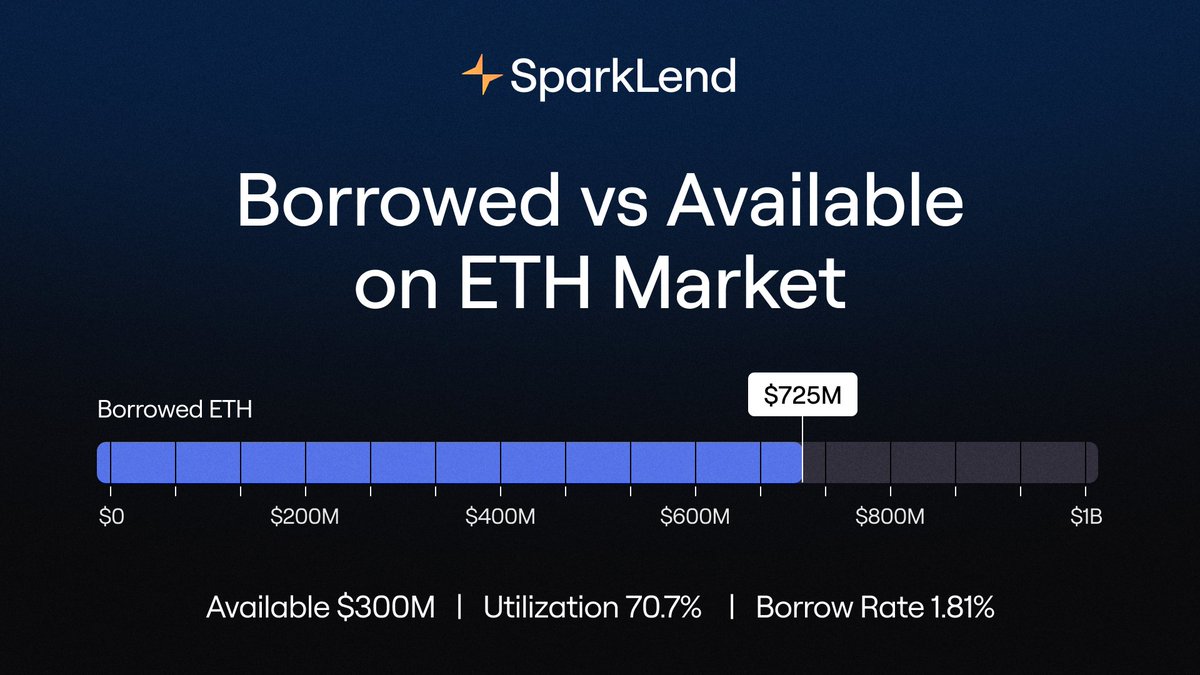

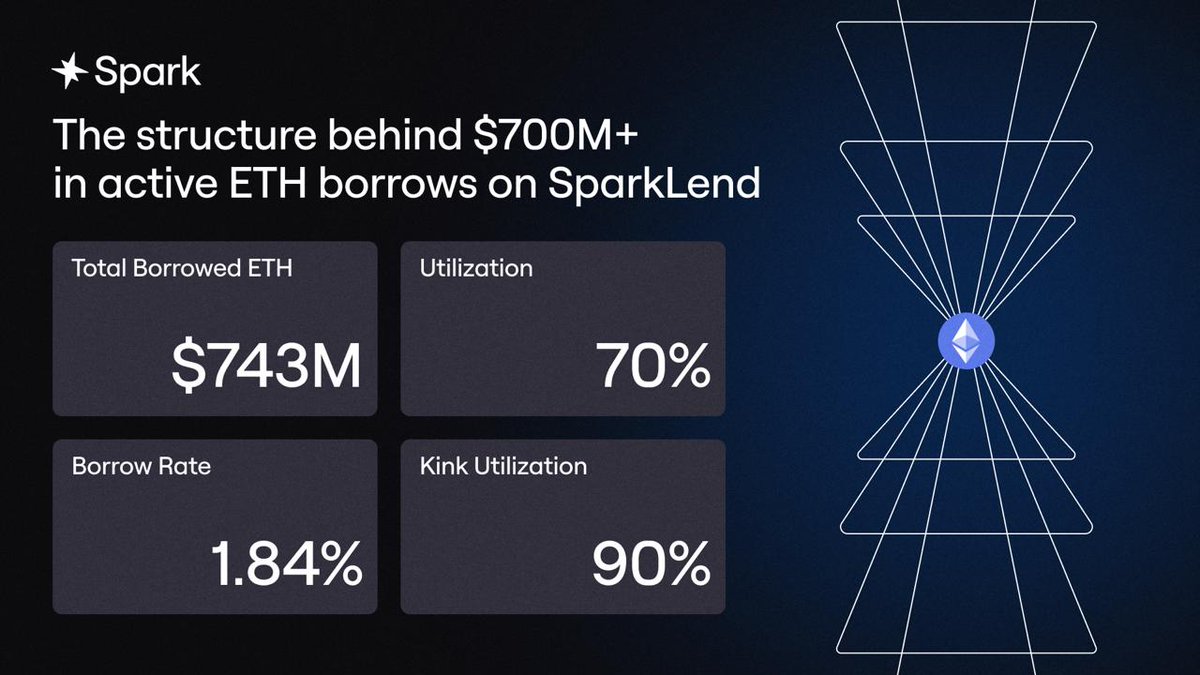

Over $725M of WETH is currently borrowed from SparkLend.

Current market conditions:

• $725M WETH borrowed

• 70.7% utilization

• 1.81% WETH borrow rate

The interesting part isn't the borrow volume.

It's that borrowing costs remain below 2% even with hundreds of millions of dollars of active demand.

As utilization rises, many lending markets rely on sharply increasing rates to balance supply and demand.

SparkLend's ETH market is designed differently.

The variable borrow rate at the optimal utilization threshold tracks the 2-day average stETH yield minus 10bps, aligning borrowing conditions more closely with ETH staking economics.

The result is a market that continues to support significant ETH borrowing activity without immediately entering a high-rate environment.

Structure matters.

Visit SparkLend: app.spark.fi/borrow

37

8

37

1,917

Jun 1

Spark isn't a trading desk.

It's financing infrastructure for professional trading firms.

Prime expands the range of financing opportunities available to the Spark Liquidity Layer while maintaining strict risk controls, capital limits, and portfolio diversification.

That's the difference between operating a strategy and financing one.

Spark is updating the scope of the Arkis partnership with a recent proposal.

The goal is to capture funding rates yield when leverage will come back in the market.

Let's unpack its significance and risks management.

Arkis provides borrowers with a single margin account that can be used to interact with multiple venues in DeFi and Tradfi.

Via the Arkis integration, @sparkdotfi can lend liquidity to delta neutral borrowers and carry traders, therefore getting exposure to funding rates without needing active management and a trading team.

While the Arkis integration has launched in q1 2026, it is about to scale meaningfully in the next months. A recent proposal expands the asset universe, including commodities (oil) metals (gold, silvers) and venue like Aster and Lighter.

The risk parameters are still tight, with $0.5 of required risk capital for every dollar allocated into Arkis, with a $5m max daily inflow. As more track record is built, this constraint will be relaxed. Current exposure is around $17m.

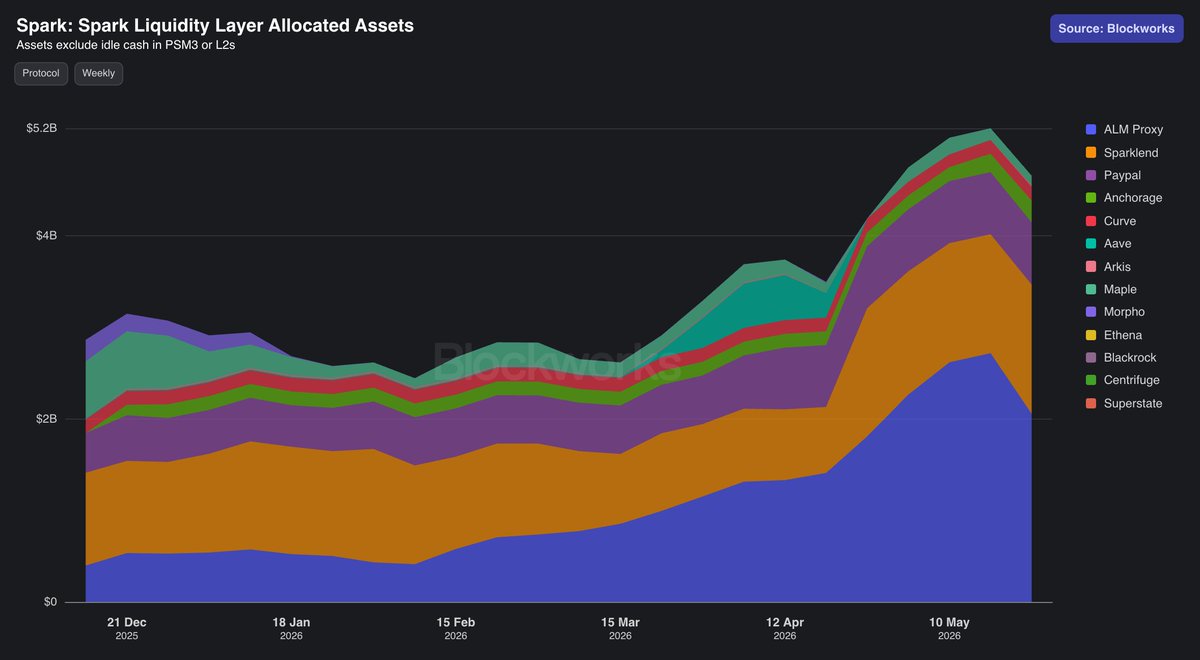

Spark has already exposure to onchain lending (via Sparklend), stablecoin liquidity (via pyUSD), institutional lending (via Anchorage). The addition of Arkis makes it even more diversified, allowing the Spark Liquidity Layer (picture) to select a better risk return in different market environments.

read the full risk council assessment:

forum.skyeco.com/t/saep-15-u…

4

6

33

3,222

May 29

Reminder for SparkLend users with BTC efficiency mode positions.

Spark will deprecate BTC efficiency mode as part of ongoing risk management.

This update only applies to positions borrowing cbBTC with LBTC or cbBTC as collateral.

Deprecation timeline:

June 4 — BTC efficiency mode deprecated

June 7 — Affected users should close open BTC efficiency mode positions

June 8 — Remaining affected positions will be subject to forced liquidation

All other SparkLend markets and positions are unaffected.

May 8

Notice on SparkLend: BTC efficiency mode will be deprecated.

Spark will deprecate BTC efficiency mode on SparkLend as part of ongoing risk management.

The change is expected to take effect on June 4. Any positions borrowing cbBTC using LBTC or cbBTC as collateral that remain open after that point will be subject to forced liquidation on June 8.

If you have an open BTC efficiency mode position on SparkLend, please close it by June 7.

This notice applies to BTC efficiency mode only. All other SparkLend markets and positions are unaffected by this change.

BTC efficiency mode deprecation timeline:

June 4 — BTC efficiency mode deprecated

June 8 — Remaining positions liquidated

This notice is issued in advance to give all affected users time to act.

13

10

30

3,532

May 28

x.com/BinanceWallet/status/2…

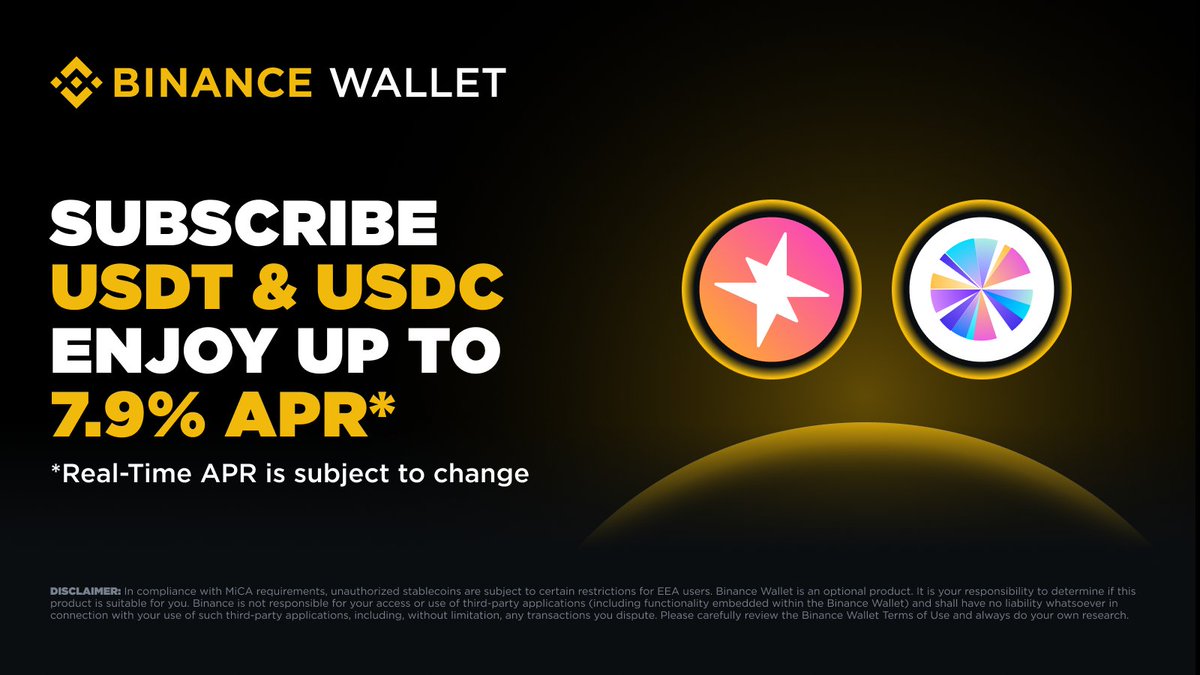

Now live on @BinanceWallet.

Access Spark USDT and USDS savings products and campaign rewards in Binance Wallet’s new Earn section.

Available now:

• Up to 6.1% APR & $200K USDS rewards

• Up to 5.3% APR & 5.5M SPK rewards

APR is dynamic and shown in-app.

Explore the vaults @BinanceWallet ↓

binance.onelink.me/mL1z/wu4i…

May 28

⏳ Access Rewards with Spark & Sky on #Binance Wallet.

🔥 Subscribe ≥100 USDT or ≥100 USDS into @sparkdotfi @SkyEcosystem through #BinanceWallet and secure up to 7.9% APR*

*Real-time APR is subject to change.

👉 Join and amplify your rewards:

binance.onelink.me/mL1z/wu4i…

4

6

31

3,114

Spark retweeted

May 27

Great article on the subDAO model!

2

2

31

4,983

May 26

Relook: Spark Prime is CeDeFi margin lending for institutional borrowers.

Most institutional strategies do not operate in one venue. Collateral sits with custodians, execution moves across exchanges, and exposure runs through DeFi protocols and traditional market infrastructure.

Spark Prime extends overcollateralized lending across these environments. Powered by @ArkisXYZ margin technology, it operates within a defined risk framework, with positions visible in real time.

The result is institutional financing infrastructure built around the full position, not one venue.

Read more about Spark Prime👇

paragraph.com/@spark-11/spar…

7

5

42

3,955

May 25

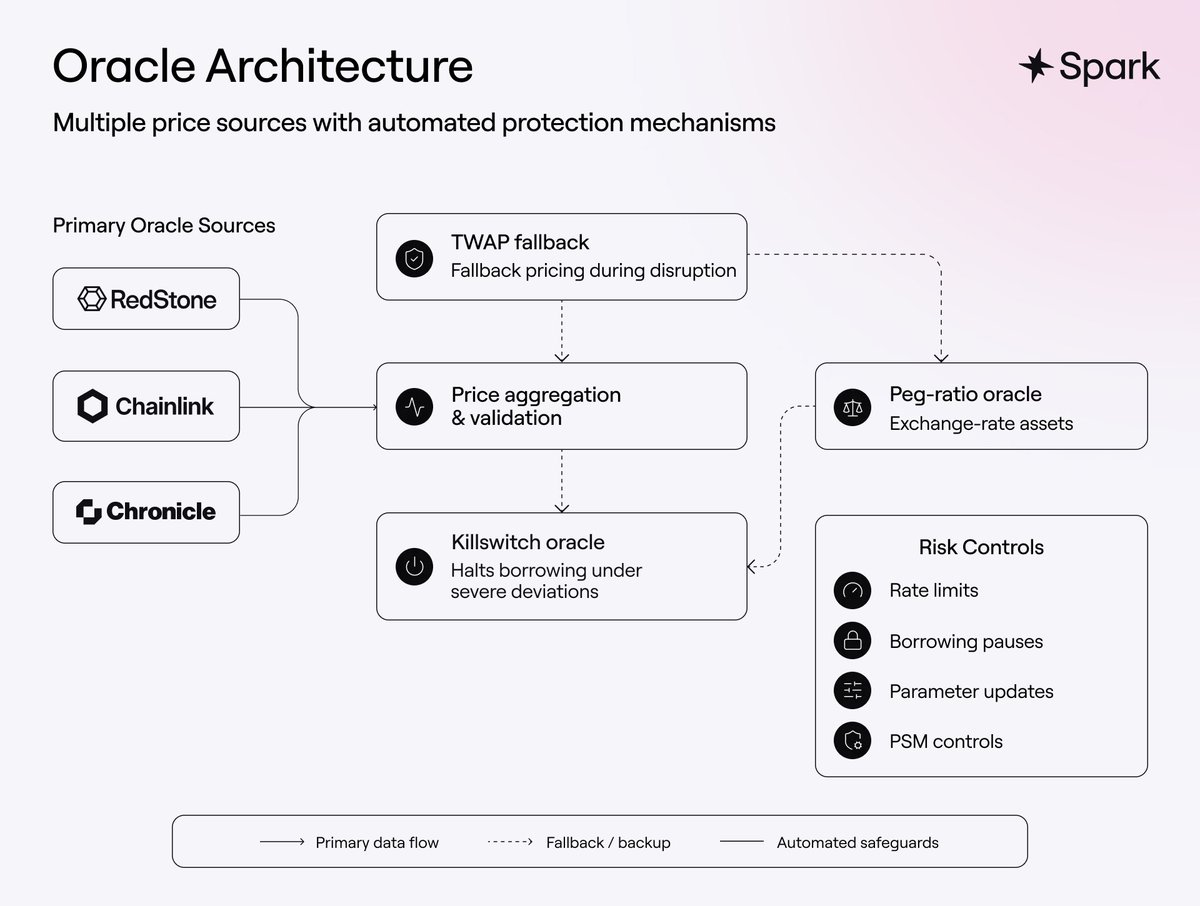

How SparkLend handles oracle disruption.

Pricing uses multiple independent oracle providers with aggregation, fallback logic, and automated safeguards designed to reduce reliance on any single price source.

Additional protection layers can restrict new borrowing when severe deviations are detected.

Read the full security framework here: paragraph.com/@spark-11/spar…

24

11

45

3,021