Finance prof co-director PE Program @Columbia_Biz. RA @nberpubs. Quant. Advisor @correlationvc. Co-organizer @workshopefi. Code: github.com/michaelewens

Joined April 2010

- Tweets 1,415

- Following 654

- Followers 2,010

- Likes 2,982

284 Photos and videos

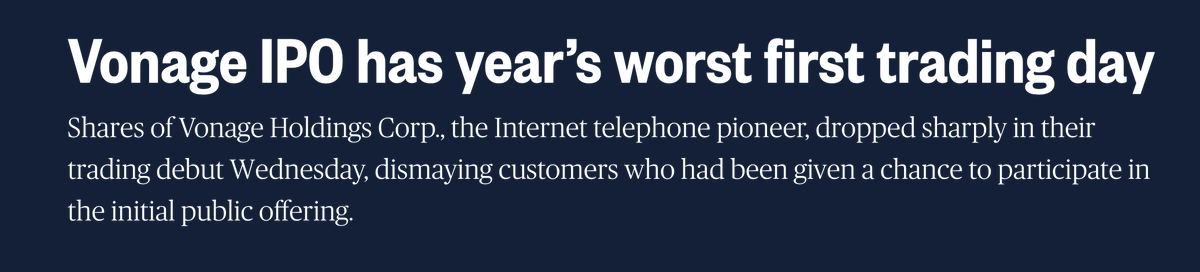

Reminds me of the 1st time I earned something from my economics training. Vonage (VoIP provider) offered me, a customer and 4th-year college student earning <$15K/year, shares in its IPO. It was a clear signal that smart $ was not interested. Then this happened:

Jun 4

NEW: Fidelity lowers the minimum account requirement for the SpaceX IPO from as high as $500,000 to just $2,000.

1

5

18

3,657

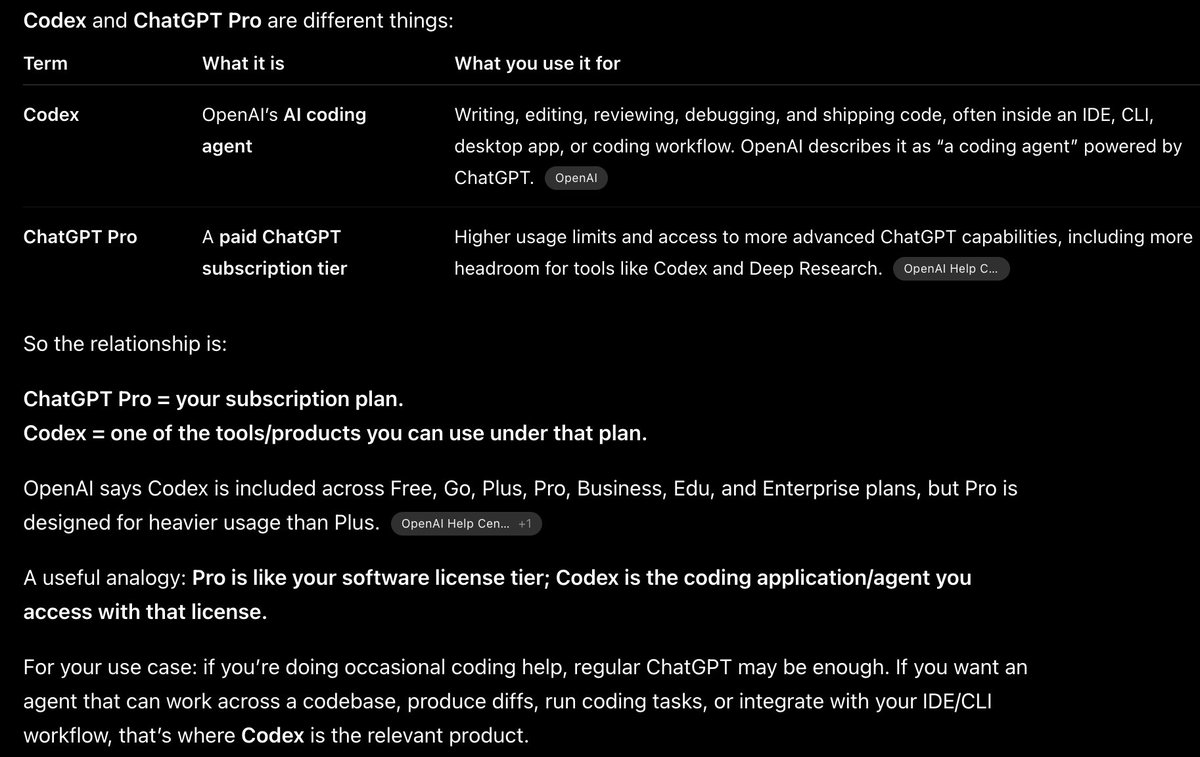

Amazing multiple AIs use case: Claude talks to Codex about a plan.

I'm rebuilding complex data and often send plans b/t the AIs. In Cmux (see below), instead tell Claude, "Ask Codex next to you for feedback". You can tell Claude to just check every 2 minutes, w/o pasting

1

1

10

1,639

I'm pleased to announce the 2nd American Finance Association Junior Faculty Mentoring Program (JFMP) event, which I am co-organizing with Audra Boone.

The program provides mentorship, research feedback, and professional development to junior faculty in finance. 🧵

1

8

702

Sessions cover research development, publishing strategy, tenure navigation, and the broader challenges of an academic career in finance. Beyond the workshop itself, participants join an ongoing cohort network that continues after the meeting. 3/N

1

1

183

This event follows the inaugural event in January '26, The 2027 workshop will be held on Saturday, January 2, 2027, in Washington, DC, with 20 senior scholars serving as mentors.

Info: afajof.org/junior-faculty-me…

Apply: afajof.org/management/mentor…

53

May 29

Join us in March!

May 28

📢Call for papers for the ESADE Entrepreneurial Finance Conference, organized by Vicente Bermejo, Martí Guasch, and me in Barcelona on March 11–12, 2027.

Confirmed speakers: Michael Ewens, Sabrina Howell, Ramana Nanda & David Robinson.

Submit by June 30: form.jotform.com/26137371121…

198

Michael Ewens retweeted

May 15

An Econ PhD student at the 20th ranked program who is working on stuff they are passionate about will have a better job market than one at MIT who's been doing nothing but phd-app-maxxing since undergrad.

People get confused by this because they don't observe *how* successful people came about their insane knowledge bases. It wasn't by relentlessly grinding away at stuff because they had to.

They look at Scott Kominers and say "if i grind and learn as much math as he did, i will be successful." You can't! *You* can't learn as much math as Kominers because he gets energized by configuration results for type ii lattices. You will burn out if you try to do it this way.

You cannot, through grind alone, learn more about the economics of cities than Glaeser, or about how to maximize a value function than Acemoglu.

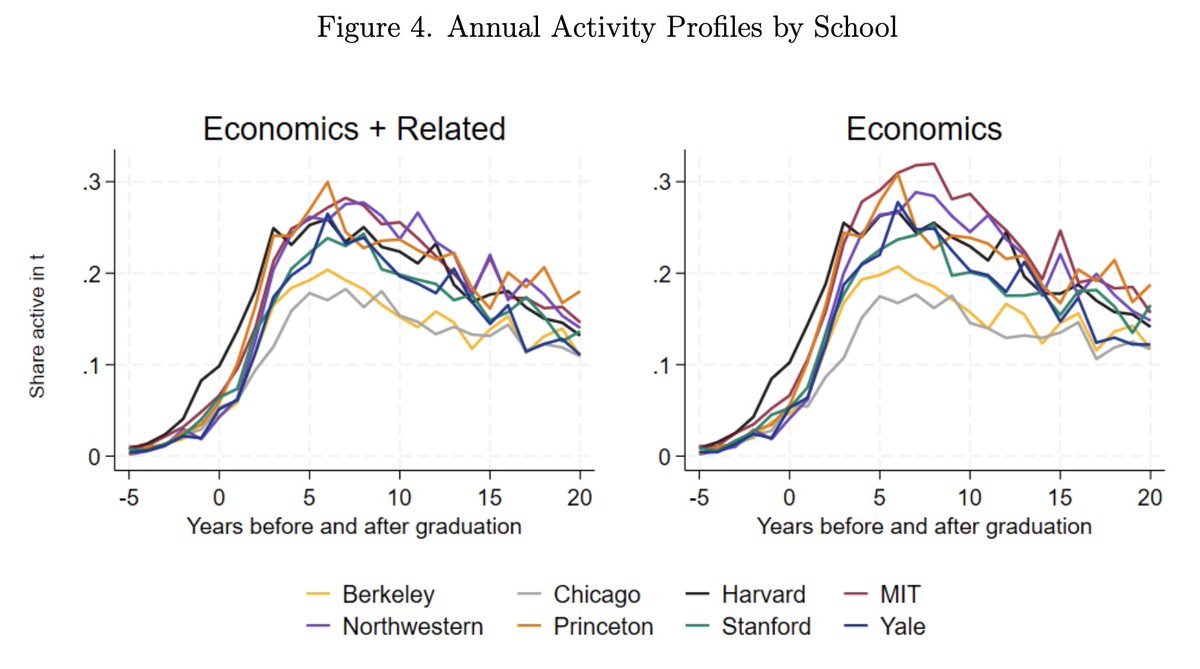

Research careers are long. Most people give up and stop working on research (graph is share of elite PhD graduates with at least one publication in year X after graduation).

If you're starting a PhD, you're presumably doing it to have a successful 40-year research career. The number one factor in whether that happens is not which program you get into, it's whether you find a research angle that energizes you enough to push through the endless barriers an academic career throws in your path.

This is why a lot of the received wisdom around PhD applications is wrong. If you're 100% consumed by the predoc rat race already, it's going to be a long, hard road ahead.

Obv you still have to do admissions, you should study a lot for the GRE, sigh it seems like taking real analysis is probably worth it.

But spending time on the things that energize you about economics is a no-brainer, whether it's policy, or blogging, or whatever, you gotta do the things that light your fire and make you want to be on this road.

32

191

1,601

347,735

May 12

The @workshopefi Fellows program is accepting pre-applications for the 2026 cohort. Deadline is June 1.

We support 10 PhDs working in entrepreneurship, entrepreneurial finance, and innovation. 🧵

1

11

9

1,136

May 12

We meet bi-weekly for presentations of new ideas, practice job talks, mock interviews, and idea pitches.

Our graduating fellows landed at IE Univ. (Yangyang Cheng), Univ. Arkansas (Melissa Crumling), OSU (Blake Jackson), Univ. Amsterdam (Roham Rezaei) 2/3

1

1

215

May 12

Eligibility:

- PhD students in economics, finance, strategy, or management

- 3rd year or later, ideally with a 2nd or 3rd-year paper

Pre-application form: columbia.qualtrics.com/jfe/f…

Info: workshop-efi.com/wefi-fellow…

Please pass this along!

1

131

Michael Ewens retweeted

May 5

Today, the @SECGov proposed amendments to provide public companies with the option of filing one semiannual report, on a new Form 10-S, in lieu of three quarterly reports on Form 10-Q.

Here's why it matters. ⬇️

Public companies have an obligation under the federal securities laws to provide information that is material to investors. Yet, the rigidity of the SEC’s rules has prevented companies and their investors from determining for themselves the interim reporting frequency that best serves their business needs and investors. Today’s proposed amendments, if ultimately adopted, would provide companies with increased regulatory flexibility in this regard.

In determining a company’s reporting cadence, a company might consider factors such as the costs and management time of preparing quarterly reports versus semiannual reports, expectations of its investors, potential effects on its cost of capital, the stage of its business development, the nature of its business model, other avenues of disclosure including earnings calls[2] and current reports on Form 8-K, and prospects of increased research coverage, all without undermining fundamental investor protections. Ultimately, this flexibility might reduce some of the burdens of being a public company and potentially influence a company’s decision to become or remain public. The proposal seeks public input on the optional semiannual reporting framework, and I look forward to the public feedback.

Of course, the frequency of regulatory reporting is only part of the equation for incentivizing companies to go and stay public. Another significant part is ensuring that the disclosure—both financial and non-financial—mandated in interim reports, whether filed quarterly or semiannually, is guided by materiality as the north star. At the SEC, the Commission staff is well underway in exploring potential amendments to Regulation S-K,[3] generally and including the parts implicated by interim reports.[4] With respect to the financial statements required in interim reports, I also encourage the Financial Accounting Standards Board to evaluate potential amendments to its accounting standards, with the same goal of eliciting disclosure of material information and avoid compelling the disclosure of immaterial information.

Today’s proposal is just the first step of the larger, comprehensive effort to review and reshape the current SEC rules governing public companies with respect to their ongoing reporting obligations and their ability to raise capital in the public markets.

Over the next few months, I expect that the Commission will be considering a series of proposals that, if adopted, will not only redefine what it means to be a public company, but will make being public attractive again.

48

20

163

32,921

Michael Ewens retweeted

Apr 24

Here is a puzzle. On the days when major AI labs release new frontier models — the kind of news that presumably raises expectations about future productivity growth — nominal and real Treasury yields fall. Andrews and Farboodi (2025) document this pattern across 17 model releases in a fascinating paper. Standard theory predicts that risk-free real rates increase when we expect higher economic growth as some of us try to consume some of that extra future income today by borrowing, thus pushing up rates. The conventional interpretation of these findings is that markets are revising growth expectations down, not up: bad news for AI optimism.

What's going on? U.S. Treasury Investors' Massive Bet on AI (post with James Paron and Howard Kung)

thetwocents.substack.com/p/u…

11

51

258

62,358

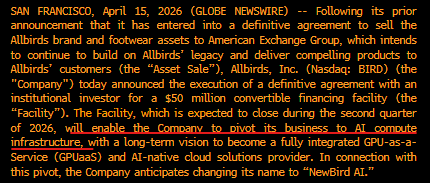

Apr 15

So they paid for a public company shell rather than do a SPAC...

223

Feb 17

Claude Code or Codex in Zed (multiple projects in one window)

Feb 16

Claude code or Cursor?

1

799

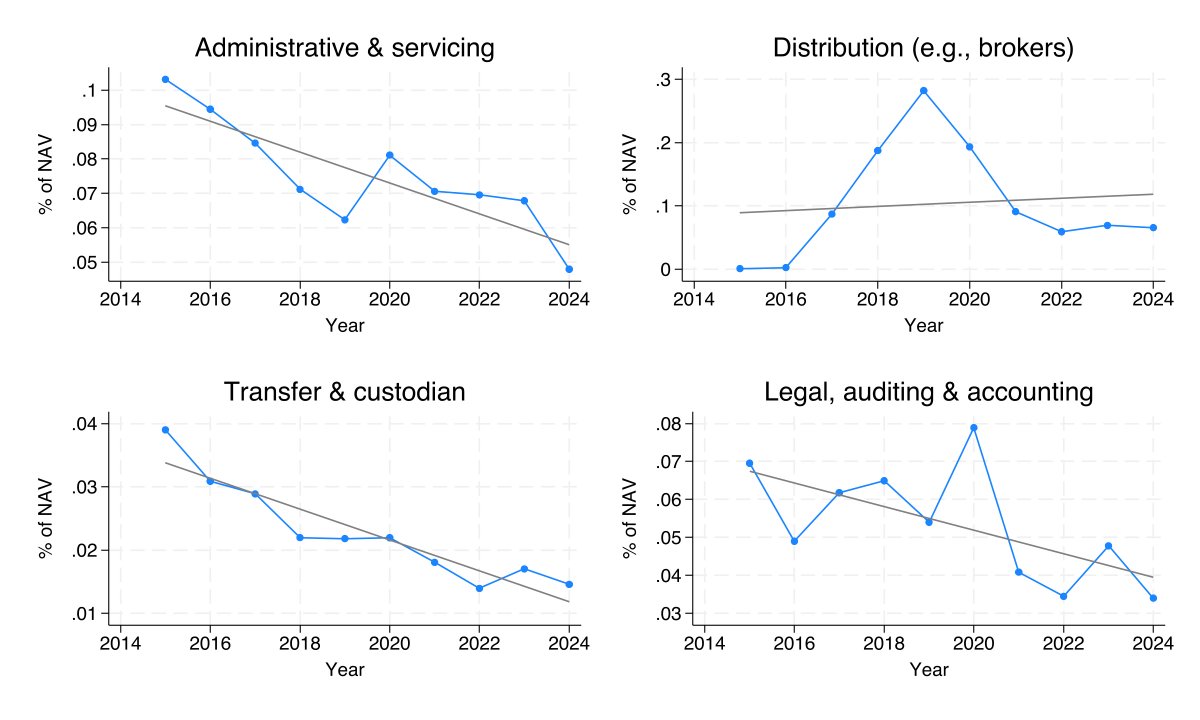

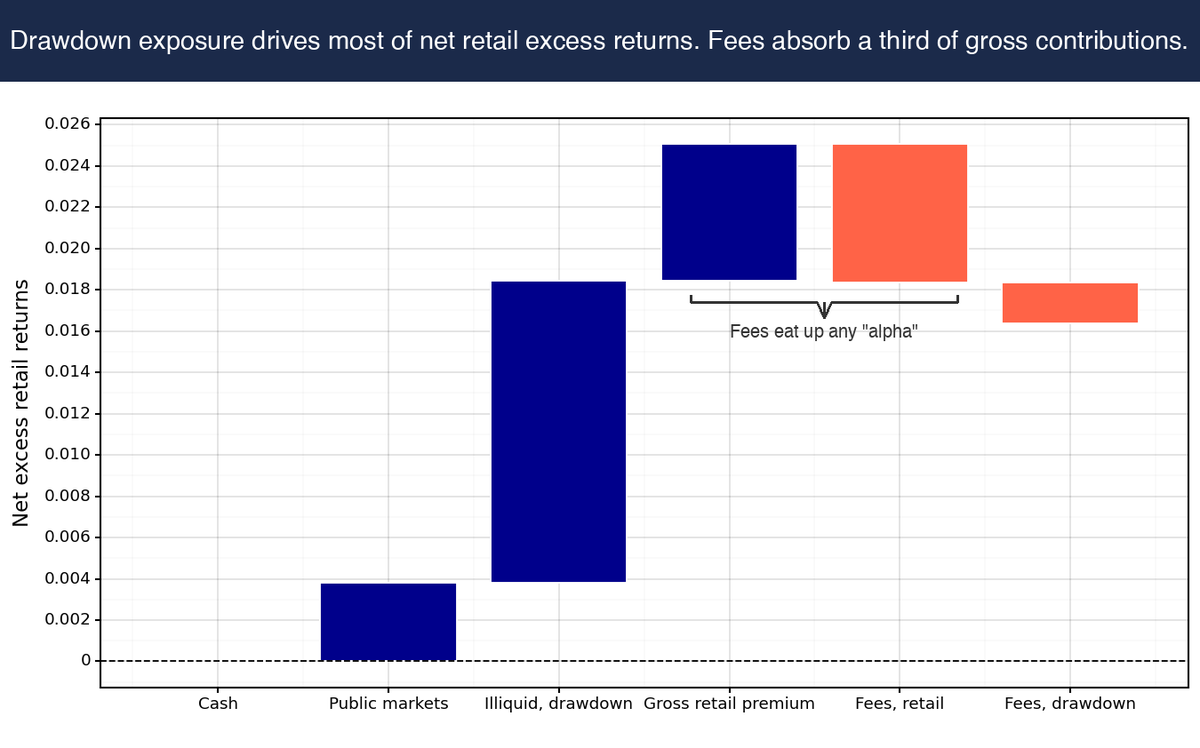

Many major PE firms are building a retail wealth channel. With Jacob Faber, we built a dataset of 114 registered funds (totaling $115B ) that offer access to private assets.

The findings are nuanced for the 401 (k) retirement expansion case. New paper: unlockingalts.com

1

5

405

Some interesting implications for major investors (e.g., pension funds, endowments): if retail capital grows as a share of AUM, expect strategy drift toward distribution-friendly, shorter-duration assets. The selection evidence already points in that direction.

1

1

1

149