Director of Policy and Research @restate_thinks. PhD from @kingspol_econ. Govt reform, localism, political econ, democratic theory. Tsundoku art. Ostrom stan.

Joined April 2009

- Tweets 9,033

- Following 4,474

- Followers 2,338

- Likes 5,789

641 Photos and videos

Pinned Tweet

Feb 5

ICYMI - here's me being interviewed about our 'Capital at risk' report by Jane Garvey on @TimesRadio....

youtube.com/watch?v=Z6KEpPY9…

1

2

666

The Re:View is out! Fantastic read on the challenges facing DWP’s new Perm Sec from our own @stkaye

Jun 12

The Re:View is out 🥳

While Westminster chased the headlines, @stkaye looked elsewhere: the DWP.

With backlogs growing and a new Permanent Secretary taking charge, is this a welfare system under strain, or a State in need of reform?

Read more 👇

open.substack.com/pub/restat…

1

2

543

Local government, from the smallest council up to the mightiest combined authority, has almost zero incentive to permit businesses in their area to grow and thrive. The only way they do is if the Treasury decides from its own goodwill to give them another little grant. So we shouldn't be surprised when they don't prioritise growth!

The local costs to them (e.g. from vocal opponents of business) are high, and the benefits in tax revenue all accumulates to Westminster.

Good fiscal devolution policy can change that - giving local government a stake in growth by letting them share in the proceeds, while making it harder to free-ride on revenue generated by other regions.

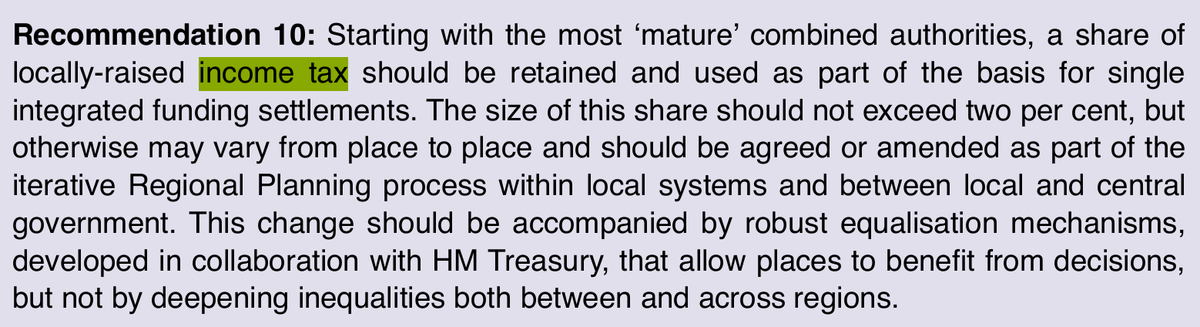

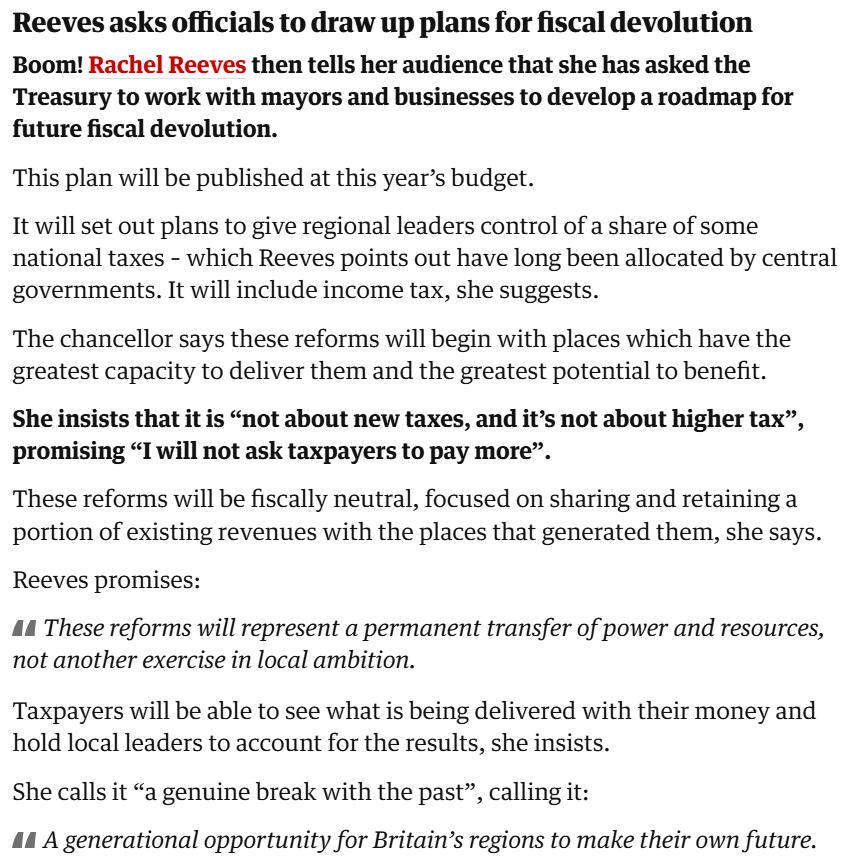

Great post this morning from @stkaye and @alwalks96 on the path to fiscal devolution.

restate.substack.com/p/how-t…

1

6

26

2,017

Jun 10

Amazing line up in store for our big annual conference, now just a few weeks away!

Particularly chuffed to have added massive voices on the localism and devolution policy debate, including MHCLG Secretary of State @SteveReedMP and the excellent Amy Harhoff from @EastMidsCCA.

1

190

Simon Kaye retweeted

Jun 8

🚨 NEW FROM THE DEVO NEXT INITIATIVE 🚨

The Chancellor’s commitment to develop a fiscal devolution roadmap represents a significant opportunity.

Re:State's Devo Next Initiative today publishes a set of design principles to realise the full potential of fiscal devolution.

1

2

12

6,449

Simon Kaye retweeted

Jun 5

Flood risk does not stop at boundaries.

We have sponsored a new report by @restate_thinks exploring how flood infrastructure can be planned and delivered more effectively as devolution evolves.

Read the full report here: bit.ly/3RN5a69

#BalfourBeatty #ExpertEngineers #BuildingNewFutures

1

1

3

382

Simon Kaye retweeted

Jun 5

NEW PAPER: 'Building in the Balance'

Infrastructure policy is in flux. Government wants faster delivery, stronger resilience, planning reform and more devolution. But the institutions expected to deliver this remain fragmented, while public expectations are often contradictory.

1

3

2

688

Jun 4

Spot on.

But also, since when do you "hate to sound like a Treasury guy"

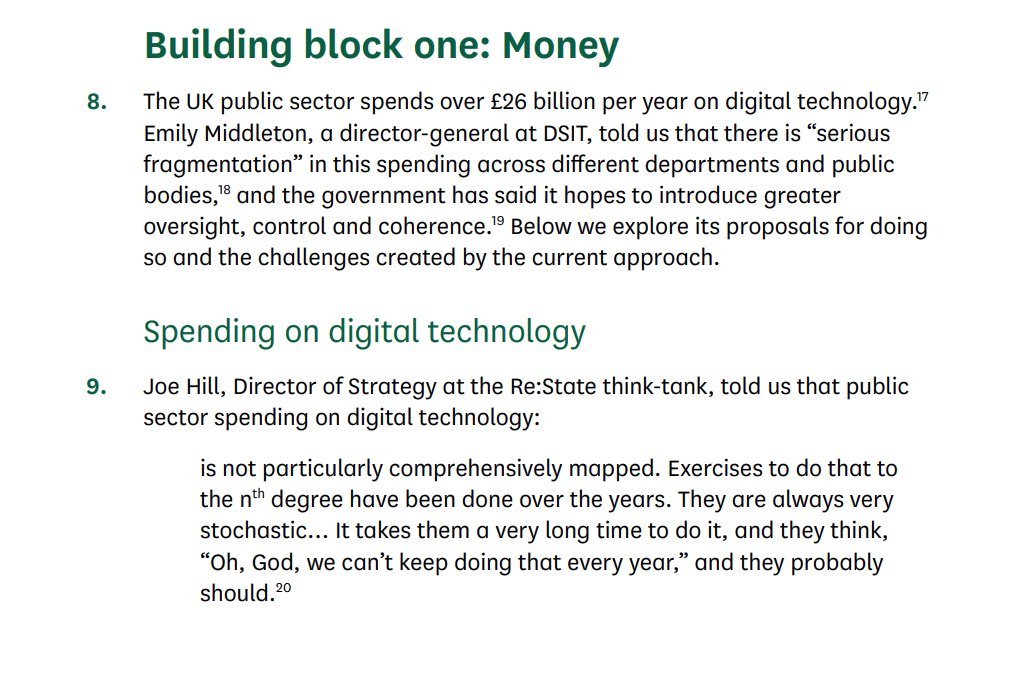

Great to see some of our work @restate_thinks feature in the Science, Innovation and Technology Committee's latest report on 'Rewiring the State'.

I hate to sound like a Treasury guy, but government should be able to answer basic questions about how much it spends on tech

3

160

May 19

Re:State: Year One.

It's been exactly a year since the rebrand. Every paper in the picture below has been published in that time (and there's a few I haven't squeezed into the pic!)

Immensely proud of the @restate_thinks team.

2

6

582

Simon Kaye retweeted

May 12

Today Re:State are launching our first flagship annual conference, 'Remaking the State', happening in London on 1 July 2026.

Agenda and speakers will be confirmed over the coming weeks.

2

10

819

Simon Kaye retweeted

May 8

The Re:View is out! 🥳

This week our Director of Policy & Research @stkaye writes about the implication of the local election results for the future of devolution.

restate.substack.com/p/the-r…

1

1

919

May 6

A new civil service code, ready to replace the old one, courtesy of @M_feeney, @ce_pickles, and @jo3hill.

re-state.co.uk/publications/…

1

4

942

Simon Kaye retweeted

Apr 30

More holes in the patchwork of English devolution.

In our first new Re:Act @stkaye shares his analysis of the latest developments in the English devolution following the bill gaining Royal Assent yesterday.

restate.substack.com/p/the-e…

1

2

3

526

Simon Kaye retweeted

Apr 17

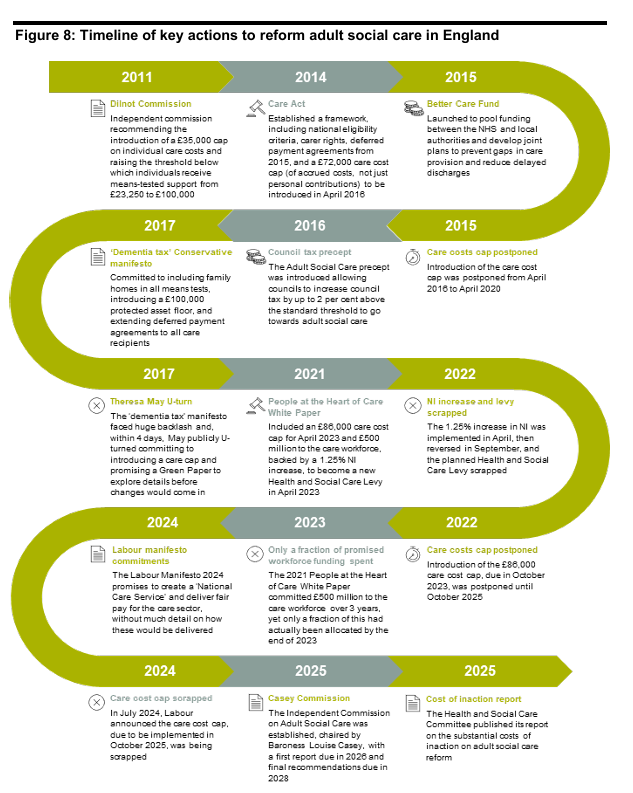

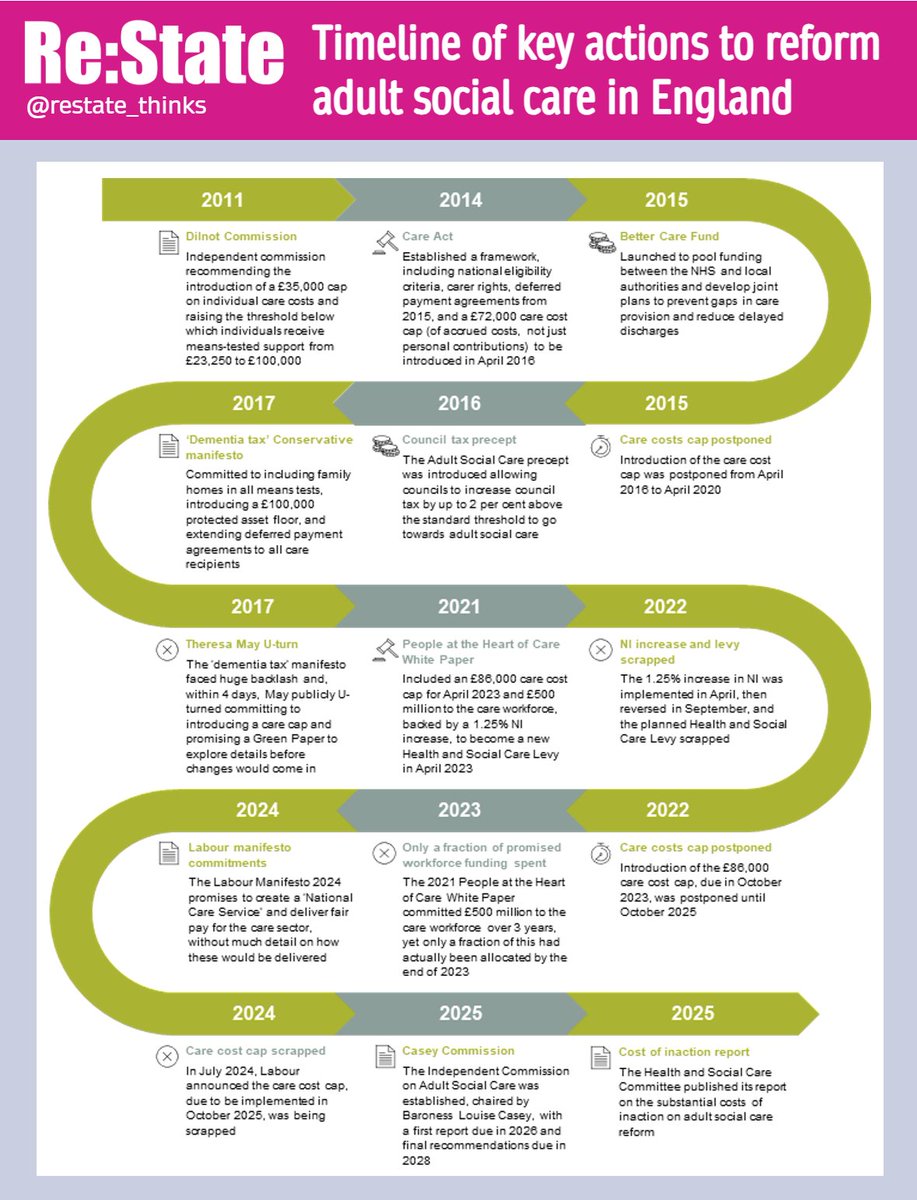

There are two things which essentially every review of care (inc ours) has recommended - separate elderly social care from council budgets and get people to contribute via insurance, salary contributions and/or slice of equity wealth. Tumbleweed in Whitehall.

In some policy areas, there really is nothing new under the sun. But social care really is an example of what Tolkein called "fighting the long defeat".

Fifteen years of failure by the policy community to realise that the Dilnot Commission's recommendations are a bogus consensus, and take a different approach.

Today we've called for a change, and a move to a Later Life Care Fund model - read more in @restate_thinks paper 'Beyond caring'.

re-state.co.uk/publications/…

7

22

113

16,873

Simon Kaye retweeted

Apr 16

For decades, governments have promised to “fix” adult social care — commissioning reports, launching independent reviews, and announcing new policies. Yet time and again, these reforms have been delayed, diluted, and abandoned, leaving an ever more dysfunctional system.

1

2

3

296

The social care funding crisis isn't up for debate. But the debate hasn't moved forward in fifteen years. @stkaye has written about why we're taking a different approach to the funding of care, and publishing a roadmap to create a dedicated Later Life Care Fund. Read it on our Substack!

restate.substack.com/p/the-c…

1

3

4

358

Simon Kaye retweeted

Apr 16

The third rail of British politics: social care

The utter failure of successive govs to act is a stain on our political class

The most recent 'consensus', Dilnot, hasn't been implemented because its the not the answer - its not affordable & fails to address fairness

🧵

1

4

3

985

Simon Kaye retweeted

Apr 16

This looks very promising. That's Re:State, Labour Together and SMF all arguing for the end of council tax as the means to fund social care. This is becoming one of those things (like weening off the triple lock) that every policy expert agrees with but no politician dares admit.

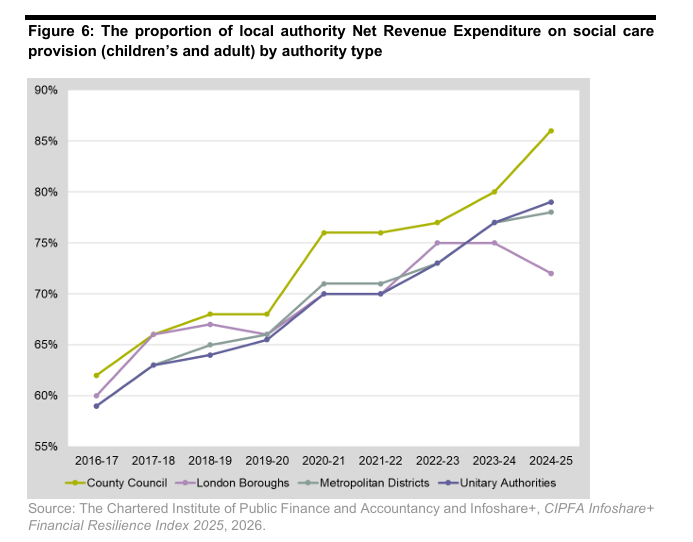

Care costs are bankrupting local government. What should we do about them?

One of the main reasons people are frustrated with the State is that they pay more and more Council Tax each year for worse and worse services. They don't understand where the money is going, and few realise it's mostly going to pay for their neighbours’ later-life care.

For years the Treasury has ducked the question of how to pay for care by shunting the problem onto local government's budgets, letting them take the blame for raising taxes. Meanwhile it has given the public the illusion that people are "paying in" today to a pot (through National Insurance and Income Tax) which will cover their care costs when they retire. This is false - that revenue just goes into general taxation and covers the cost of existing services, including care for those who are currently using it.

That Council Tax is a regressive way of raising revenue, which disproportionately affects lower earners, only exacerbates how unfair the system is. Because the costs of older and (relatively) wealthy retirees are being funded by younger and poorer workers through high taxes. Taxes which also make it harder to get on the housing ladder, while most housing assets owned by later-life care users are shielded from being used to pay for their care costs.

By stealth and fiscal slight-of-hand this has undermined:

1. The social contract of care ("I paid in, so I should get back what I paid").

2. The legitimacy of local government to raise taxes.

3. The prospect of lower taxes for future generations.

Other countries pre-fund social care through different mechanisms - mostly mandatory lifetime contributions into a social insurance fund, which is separate from their general taxation revenue. This is invested for profit over time, and covers the cost of care when needed - meaning that by the time each cohort reaches the point of needing care, the money they contributed pays for their needs.

Today we at @restate_thinks have published a paper arguing that Britain should adopt this model, creating a Later Life Care Fund through a 1.8% mandatory contribution on the pre-tax incomes of people from the age of 34 to 68. This would be invested over time in schemes which yield high returns, and pay out based on need - supported by a system of individual personal allowances, co-payments and a protected-asset floor.

It would be a more sustainable, fairer and more generous system than we can afford in today’s model of paying through taxes. The hardest part will always be transition - where current older generations will need to pay more through temporary transition-funding or levies. For example, expanding personal National Insurance Contributions to the incomes of pensioners.

Huge credit to @stkaye and @AliceKSemark for their hard work.

re-state.co.uk/publications/…

4

11

54

6,142

Simon Kaye retweeted

Apr 16

There are no easy answers to the social care dilemma. But what should be clear is that we cannot continue to muddle through as we are. The current situation is utterly destroying local government while still not providing adequate funding.

This is a really valuable paper from @restate_thinks setting out how a dedicated social insurance model could work (which to me feels preferable to sticking the bill on general taxation, for example, or the lottery of unlucky people having to sell their home to pay for care).

We cannot continue to duck this. Government must *choose*, and soon - and all parties have a responsibility to do the same.

Care costs are bankrupting local government. What should we do about them?

One of the main reasons people are frustrated with the State is that they pay more and more Council Tax each year for worse and worse services. They don't understand where the money is going, and few realise it's mostly going to pay for their neighbours’ later-life care.

For years the Treasury has ducked the question of how to pay for care by shunting the problem onto local government's budgets, letting them take the blame for raising taxes. Meanwhile it has given the public the illusion that people are "paying in" today to a pot (through National Insurance and Income Tax) which will cover their care costs when they retire. This is false - that revenue just goes into general taxation and covers the cost of existing services, including care for those who are currently using it.

That Council Tax is a regressive way of raising revenue, which disproportionately affects lower earners, only exacerbates how unfair the system is. Because the costs of older and (relatively) wealthy retirees are being funded by younger and poorer workers through high taxes. Taxes which also make it harder to get on the housing ladder, while most housing assets owned by later-life care users are shielded from being used to pay for their care costs.

By stealth and fiscal slight-of-hand this has undermined:

1. The social contract of care ("I paid in, so I should get back what I paid").

2. The legitimacy of local government to raise taxes.

3. The prospect of lower taxes for future generations.

Other countries pre-fund social care through different mechanisms - mostly mandatory lifetime contributions into a social insurance fund, which is separate from their general taxation revenue. This is invested for profit over time, and covers the cost of care when needed - meaning that by the time each cohort reaches the point of needing care, the money they contributed pays for their needs.

Today we at @restate_thinks have published a paper arguing that Britain should adopt this model, creating a Later Life Care Fund through a 1.8% mandatory contribution on the pre-tax incomes of people from the age of 34 to 68. This would be invested over time in schemes which yield high returns, and pay out based on need - supported by a system of individual personal allowances, co-payments and a protected-asset floor.

It would be a more sustainable, fairer and more generous system than we can afford in today’s model of paying through taxes. The hardest part will always be transition - where current older generations will need to pay more through temporary transition-funding or levies. For example, expanding personal National Insurance Contributions to the incomes of pensioners.

Huge credit to @stkaye and @AliceKSemark for their hard work.

re-state.co.uk/publications/…

3

7

42

6,086

Simon Kaye retweeted

Apr 16

England's current model of funding adult social care leaves many people facing unmanageable costs, and has resulted in soaring unmet need, estimated at over 3.5 million adults.

In 'Beyond Caring', we propose a new funding model, offering far more generous personal protections.

1

2

4

217

Apr 16

Great to have coverage of our report today in @room_151.

CCN: two-thirds of councils’ budgets spend on care services: Local authorities in England spend around two-thirds of their budget on adults’ and children’s social care, a new analysis has revealed. The research by Pixel Financial Management for the… dlvr.it/T4FZ4N

71