Joined April 2009

- Tweets 4,063

- Following 2,197

- Followers 835

- Likes 89,653

50 Photos and videos

Pinned Tweet

Jan 3

This is an efficient overview of @MyriadUranium as we begin 2026.

youtube.com/watch?v=7JrBNkHi…

5

23

3,907

Thomas Lamb retweeted

Myriad is advancing drill plans across multiple Copper Mountain targets while progressing toward full district ownership and a potential U.S. listing. Exploration and corporate milestones continue to align, building momentum at Copper Mountain.

Learn what's ahead: ow.ly/poTs50Z8NSa

CSE: $M.CN | OTC: $MYRUF | FRA: $C3Q

6

17

1,051

Thomas Lamb retweeted

Jun 12

Was an interesting road show - well (re) structured and recently financed for upcoming programs. Of the 3, I like the Mexican project. @tdlamb @J2Metals

linkedin.com/posts/natrinova…

3

5

629

Thomas Lamb retweeted

#uranium #nuclearenergy $M.CN $MYRUF

New @CruxInvestor interview with CEO @tdlamb & Senior Geologist George van der Walt👇🎞️

Made In America | Myriad Uranium (CSE:M) - America's Uranium Gap & The Wyoming Project Closing It

Watch here⬇️

youtu.be/w7MfBgJq6Ps?si=2bd0…

8

22

2,715

Jun 9

Thank you for this great overview of @MyriadUranium's new Arizona project next to Energy Fuels' Pinyon Plain Mine, Anders.

Jun 9

Today's news from Myriad #Uranium $M.CN looks like a very smart move, in my opinion.

Myriad acquired a large package of Arizona breccia pipe uranium targets without paying a third party acquisition cost, essentially securing the ground through leases and staking. Even better, Wedgemount will fund the initial exploration work, meaning no immediate dilution for Myriad shareholders, while Myriad retains the right to earn back up to a 50% interest in the project.

Under the agreement, Wedgemount will spend up to C$4 million on exploration while Myriad retains significant exposure to the upside, including the right to earn back up to a 50% interest in the project. In other words, shareholders gain exposure to a potentially high-impact uranium district without Myriad having to fund the early-stage work itself.

But what really caught my attention is the location.

The project sits in the same district as Energy Fuels' Pinyon Plain Mine. When I reviewed their drill results last year, I was genuinely impressed. Their May 1 release (see screenshot below) included intercepts grading over 20% U₃O₈. That's not a typo. Those are Athabasca-style grades and among the highest uranium grades ever reported in the United States.

In the uranium sector, major discoveries often trigger a staking rush. Companies move quickly to secure prospective ground around successful deposits, hoping to make the next discovery in the same geological trend. We saw that playbook in the Athabasca Basin after the Triple R discovery, where aggressive land consolidation ultimately led to discoveries such as Arrow.

No one can assume Myriad's targets will replicate Pinyon Plain. Exploration is exploration. But shareholders now have exposure to one of North America's highest-grade uranium districts, with another company paying the exploration bill.

That's a setup I like.

Disclosure: Paid partnership with Myriad Uranium. This is not financial advice. Please do your own due diligence.

1

1

7

312

Thomas Lamb retweeted

4

18

896

Thomas Lamb retweeted

Jun 3

J2 Metals $JTWO is starting to look seriously interesting here. 🔥 #silver #antimony #gold

Today’s update from J2 Metals confirms they are advancing TWO highly compelling discovery stories at the same time:

🇲🇽 Sierra Plata (Silver-Gold-Antimony)

🇨🇦 Miniac (Copper-Gold-Zinc VMS)

At Sierra Plata, the team is now ON THE GROUND mapping historical mines, workings, and vein systems in one of Mexico’s most prolific historic epithermal districts. This project has never been explored with modern methods despite 500 years of mining history.

Key points:

• 5 past-producing high-grade mines

• Waste dump samples up to 3,932 g/t AgEq

• Drill permitting underway

• Antimony exposure at exactly the right time

The antimony angle could become huge. Antimony is now one of the hottest critical minerals globally due to defense, flame retardants, and battery applications, while supply remains extremely constrained.

Meanwhile at Miniac in the Abitibi:

• 41 km OreVision IP survey completed

• Multiple chargeability/resistivity anomalies identified

• Coincident with previous EM targets

• 19 high-priority targets along a 7 km conductive horizon

• Phase II drilling up to 5,000m being planned

Disclosure: Paid partnership with J2 Metals. This is not financial advice. Please do your own due diligence.

#silver #gold #antimony

News🚨🧾

J2 Metals Inc.: Field Team Mobilized at Sierra Plata Silver-Gold-Antimony Project in Zacualpan to Map Historical Mines, Workings, Veins. 3D-IP Survey Completed at Miniac Project in the Abitibi.

Read here⬇️

j2metals.ca/field-team-mobil…

4

6

1,753

Thomas Lamb retweeted

BREAKING. The Russian government has just announced that I have been added to their sanctions list for my work exposing their sanctions evading cryptocurrency A7A5. In doing so, I have exposed their Achilles’ heel. Without A7A5 they would not be able to fund their war of aggression. I have been sanctioned alongside Washington Post reporter @catherinebelton and 3 other UK nationals. It’s a badge of honour.

tass.com/politics/2140481

284

1,324

5,901

228,163

Thomas Lamb retweeted

Myriad Commentary: The U.S. Nuclear Renaissance Accelerates After First Year of Executive Orders

One year after President Trump’s nuclear executive orders, the U.S. nuclear sector is moving from policy ambition to tangible deployment activity. The DOE recently outlined major progress across reactor licensing, fuel supply chains, plant restarts, SMR deployment, microreactors, and nuclear infrastructure investment.

Key developments over the past 12 months:

• DOE support for multiple new SMR deployments

• NRC approvals advancing new design advanced reactor projects

• Billions committed toward domestic uranium enrichment supply

• Restart financing for idle nuclear plants

• Expansion of reactor uprates and 80-year operating license extensions

• Deployment pathways for military, Ai data centers, and microreactors

• New federal initiatives targeting faster reactor testing and commercialization

Bottom line:

The U.S. nuclear sector is now entering a large-scale deployment phase supported by federal financing, regulatory acceleration, and supply chain investment.

Collectively, these developments reinforce long-term demand visibility for uranium and nuclear fuel through the coming decades.

energy.gov/ne/articles/one-y…

5

15

434

Thomas Lamb retweeted

Jun 2

What if the largest uranium discovery in the U.S. is already sitting in plain sight…

…and the company behind it is still valued like a tiny junior explorer? 👀☢️

New drill program starts THIS month.

Market cap still asleep.

Jun 1

The timing here is getting very interesting for Myriad Uranium $M.CN.

Long-term #uranium prices just hit new 18-year highs:

• UxC LT price: $93/lb

• TradeTech LT price: $95/lb

• SWU and conversion prices at or near all-time highs

• Production cost indicators continue rising

The market is starting to price in a world where future uranium supply may become increasingly difficult and expensive to develop.

And right as this is happening, Myriad is preparing to start Phase II drilling at Copper Mountain this month.

That connection matters.

Copper Mountain is not an early conceptual grassroots story:

- Historic resource base of 26.6M lbs

- Historic DOE Bendix work outlined exploration potential of up to 655M lbs across the broader district

- Multiple new geophysical targets

- Positive disequilibrium identified in Phase I

- Large portions of the district still untested with modern methods

- Potential expansion up to 10,000m in Phase II

If Phase II successfully validates and expands mineralization while uranium prices continue strengthening, I think Myriad will be completely re-rated.

Disclosure: Paid partnership with Myriad Uranium. This is not financial advice. Please do your own due diligence.

3

4

27

8,885

Thomas Lamb retweeted

Jun 1

The timing here is getting very interesting for Myriad Uranium $M.CN.

Long-term #uranium prices just hit new 18-year highs:

• UxC LT price: $93/lb

• TradeTech LT price: $95/lb

• SWU and conversion prices at or near all-time highs

• Production cost indicators continue rising

The market is starting to price in a world where future uranium supply may become increasingly difficult and expensive to develop.

And right as this is happening, Myriad is preparing to start Phase II drilling at Copper Mountain this month.

That connection matters.

Copper Mountain is not an early conceptual grassroots story:

- Historic resource base of 26.6M lbs

- Historic DOE Bendix work outlined exploration potential of up to 655M lbs across the broader district

- Multiple new geophysical targets

- Positive disequilibrium identified in Phase I

- Large portions of the district still untested with modern methods

- Potential expansion up to 10,000m in Phase II

If Phase II successfully validates and expands mineralization while uranium prices continue strengthening, I think Myriad will be completely re-rated.

Disclosure: Paid partnership with Myriad Uranium. This is not financial advice. Please do your own due diligence.

At Myriad, we're focused on execution.

✔️ Expanded Copper Mountain to district scale

✔️ Completed a successful maiden drill program

✔️ Confirmed #uranium mineralization and positive disequilibrium

✔️ Completed high-resolution geophysics and advanced targeting

✔️ Filed a comprehensive NI 43-101 Technical Report

✔️ Commenced Phase II drilling

With up to 10,000m planned, Phase II is designed to validate historic resources, expand known mineralization, test priority targets and advance Copper Mountain toward a maiden resource estimate.

We're building on momentum, achieving key milestones and working to unlock the full potential of Copper Mountain for our shareholders.

3

3

28

6,124

#gold #silver

The presence of multiple former mines within the project area provides clear evidence of a robust and repeatable mineralizing system, significantly reducing geological risk.

Historic workings, mine dumps, and underground development also offer valuable data points for modern exploration.

Learn more⬇️

j2metals.ca/projects/#_proje…

🇨🇦TSX.V: $JTWO

5

15

1,464

Thomas Lamb retweeted

May 28

Why I think now could be one of the most asymmetric entry points in Myriad #Uranium $M $M.CN ☢️🔥

The market still seems to view Copper Mountain as just an old historical uranium district.

I think that is about to change.

Phase II drilling starts in June, with potential expansion up to 10,000 meters — and this could become one of the most important U.S. uranium exploration stories of 2026.

Here’s what makes the setup so compelling:

• Existing historic resource base of 26.6M lbs

• DOE “Bendix Report” outlined exploration potential of up to 655M lbs across the district, but that is now old data since:

✅ Recent geophysics generated multiple new drill targets

✅ Phase I drilling showed positive disequilibrium, suggesting historical grades may materially underestimate the real uranium content

✅ Large parts of the system remain essentially untested with modern exploration methods

This is the kind of setup the market often misses early:

A known uranium district with historical resources modern targeting potential grade upgrades district-scale upside.

And importantly:

Copper Mountain is in the U.S.

In a world increasingly focused on domestic uranium supply chains, strategic projects in safe jurisdictions could become dramatically more valuable if uranium prices move where many bulls expect them to go.

The strategic alliance with Subatomic adds another layer of credibility here. Smart capital tends to position itself before the broader market fully understands the opportunity.

If uranium moves toward $150/lb in the coming years, utilities may not care nearly as much about “optionality” stories anymore — they will care about where future pounds can realistically come from.

That’s why I think Copper Mountain could become much more important than the market currently appreciates.

Disclosure: Paid partnership with Myriad Uranium. This is not financial advice. Please do your own due diligence.

$M.CN $MYRUF #uranium

Myriad Uranium advances at Copper Mountain: after a highly successful Phase I, Phase II kicks off with 4,500m of drilling (with expansion potential to 10,000m) targeting historic resources of 26.63 Mlbs plus major new upside. Phase III aims to build toward a maiden resource estimate and further test new targets.

Stay tuned for news and updates!

4

20

1,810

Thomas Lamb retweeted

May 26

J2 Metals $JTWO just became one of the most interesting junior #silver stories on the TSXV in my opinion.

The TSXV has now approved J2 Metals’ definitive agreement to acquire 100% of the Sierra Plata silver-gold-antimony project in Mexico’s historic Taxco district.

And this project looks STACKED:

✅ 2,203 hectares in one of Mexico’s premier silver camps

✅ FIVE past-producing silver mines

✅ Historic San Miguel Mine believed to extend onto JTWO ground

✅ Exposure to BOTH silver and critical mineral antimony

✅ Existing infrastructure local technical teams via Impact Silver

The grades are what really catch attention. A few examples:

• 3,868 g/t AgEq (👀 bonanza grades!)

• 845 g/t AgEq

• 659 g/t AgEq

• 489 g/t AgEq

These are not low-grade bulk-tonnage numbers. These are serious high-grade epithermal-style silver-gold results from waste rock sampling.

And the antimony angle could become HUGE.

Antimony is now officially classified as a critical mineral in both the US and EU due to:

⚡ energy storage

🛡️ defence applications

🏭 supply chain security

2026 could be a pivotal year for J2 Metals, with significant re-rating potential.

Disclosure: Paid partnership with J2 Metals. Not financial advice. Please do your own due diligence.

Yesterday we announced TSX-V approval of our definitive option agreement to acquire 100% of the past-producing Sierra Plata #Silver-#Gold-#Antimony Project in Taxco, Mexico. 🇲🇽

A large-scale opportunity in one of Mexico’s most historic silver camps:

🔹 2,203 hectares

🔹 5 past-producing silver mines

🔹 Strong silver-gold grades

🔹 Antimony exposure in a critical minerals market

With local infrastructure, experienced technical teams, and exploration already underway, we’re moving quickly.

More info: j2metals.ca/tsx-venture-exch…

3

5

1,195

Thomas Lamb retweeted

Yesterday we announced the commencement of Phase II drilling at Copper Mountain — and the scale matters.

🔹 Initial program: 4,500 metres (15,000 ft)

🔹 Fully scalable to 7,000–10,000 metres (23,000–33,000 ft) subject to results

🔹 Targets include both known mineralized zones AND new targets generated from recent geophysics historic Bendix data

After a maiden program that exceeded expectations, Phase II is about systematically unlocking district-scale uranium potential in Wyoming

Learn more⬇️

myriaduranium.com/myriad-ura…

1

7

31

1,810

Thomas Lamb retweeted

10

26

868

Thomas Lamb retweeted

May 18

Aside from my main commodities #uranium and #silver, I have started to look into fertilizers, and #potash in particular.

American Critical Minerals @MineralsCorp $KCLI is starting to look like one of very few emerging US potash development stories at exactly the right time.

The market is waking up to a major macro shift:

• Middle East tensions are adding volatility to global fertilizer markets

• The US remains heavily dependent on imported potash, with roughly 90–95% of supply coming from abroad

• Potash is now officially classified as a critical mineral in the US

• Washington is aggressively pushing domestic mineral security

Meanwhile, American Critical Minerals is sitting on a massive project in Utah’s Paradox Basin — the same basin hosting the long-running Moab potash operation.

What stands out to me:

✅ Exploration target of 600M–1B tonnes of sylvinite

✅ Grades ranging from 19–29% eKCl

✅ Existing infrastructure, roads, rail, power nearby

✅ Potential exposure not just to potash, but also lithium bromine

✅ A fully permitted maiden drill program is expected to advance in 2026

The strategic angle is becoming hard to ignore.

The US government is openly prioritizing domestic critical mineral supply chains, and multiple new American potash projects are now receiving regulatory support.

Tiny market cap.

Massive optionality.

Potash lithium US critical minerals theme all in one ticker.

Find out more here: acmineralscorp.com/projects/

Disclosure: I have a financial relationship with $KCLI.

3

7

31

6,365

Thomas Lamb retweeted

May 19

As Myriad $M.CN completes the sale of Red Basin Uranium project, this strategic alliance is what really makes me excited. Tech companies entering with capital and new exciting ideas is exactly what is needed to move the #uranium sector.

Disclosure: I have a commercial relationship with Myriad Uranium.

News Alert 🔔

Myriad Uranium Completes Sale of Red Basin Uranium Project to VC-Backed Subatomic, Retains 10% Free Carried Interest and Enters into Strategic Alliance

$M $M.CN $MYRUF #uranium

Read now⬇️

juniorminingnetwork.com/juni…

1

3

16

2,477

Thomas Lamb retweeted

DOE’s latest report highlights nuclear’s growing role in flexible, clean energy systems alongside renewables.

As nuclear deployment expands, secure uranium supply becomes increasingly strategic—supporting the outlook for Myriad’s U.S. assets.

ow.ly/7N8e50Z09q4

5

21

1,043

Thomas Lamb retweeted

#uranium $M $M.CN $MYRUF

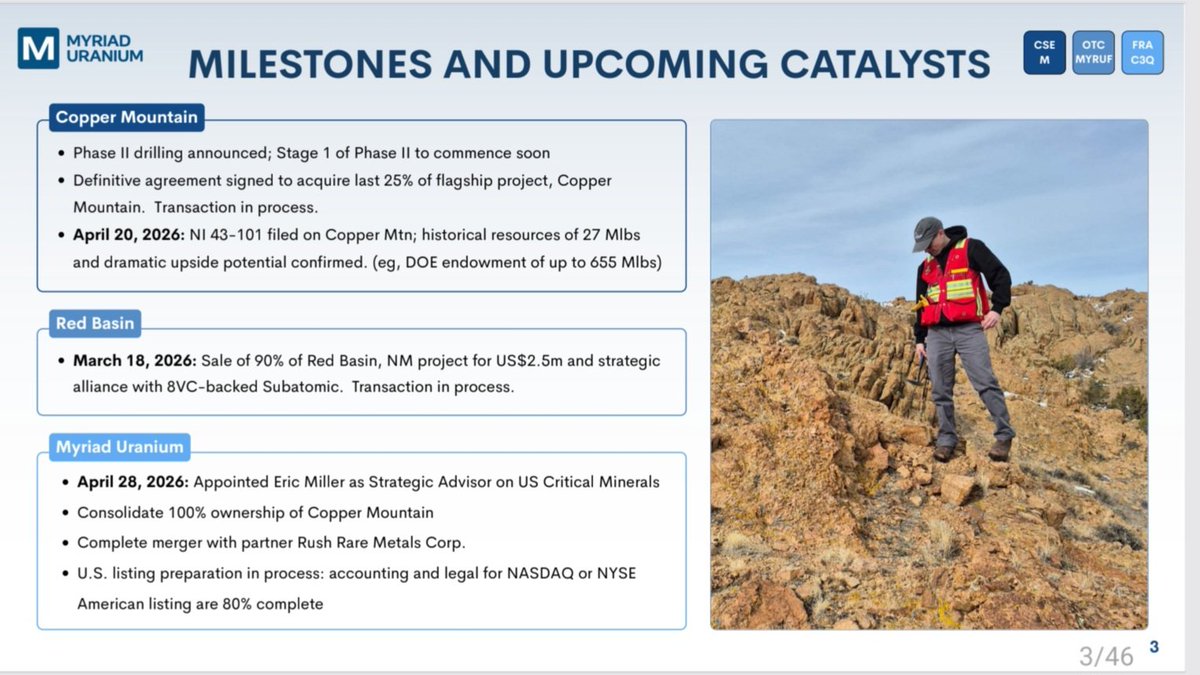

Multiple near-term catalysts for Myriad Uranium 👀

⛏️ Copper Mountain Phase II drilling soon

📈 100% ownership consolidation in progress

🤝 Red Basin strategic deal underway

🇺🇸 NASDAQ / NYSE American listing prep 80% complete

⚡ Rush Rare Metals merger progressing

11

32

2,333

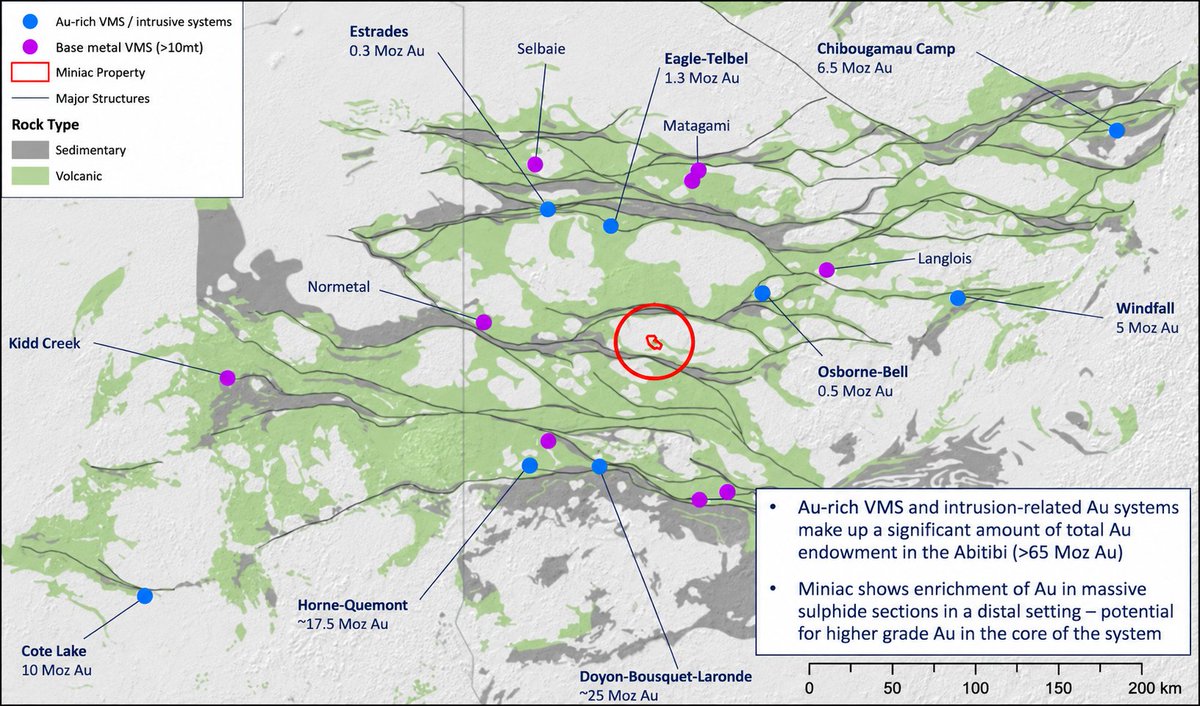

The Abitibi Greenstone Belt has produced 200M oz of #gold from 120 mines and remains one of the world’s premier jurisdictions for both orogenic gold and VMS discoveries.

That’s exactly why $JTWO’s 100%-owned Miniac Project matters.

📍 Northern Abitibi, Quebec

📍 Along the prolific Chicobi fault system

📍 Between past-producing Normétal & Osborne-Bell

📍 Polymetallic Au-Ag-Cu-Zn VMS target with historic gold/zinc hits

📍 19 high-priority targets identified across a 7km conductive trend

📍 41km IP survey completed to refine Phase II drill targeting

Tier-1 address. Strong geology. Systematic exploration.

Discovery leverage in the right postcode.

Learn more:j2metals.ca/projects/#projec…

#mining #exploration #VMS #Abitibi #Quebec #juniormining

1

6

13

2,332