1,620 Photos and videos

Pinned Tweet

F1 Barcelona Grand Prix Weekend 🇪🇸🏎️

Nothing like the sound of these machines live 🔥Thanks to @OKXFrench @okx for the invite

2

7

102

That's My Quant 🤖🧠 retweeted

No TA. No indicators. Just order flow.

@thatismyquant scalping the market : comment “Order Flow” for the private live of the last trading session👇

6

5

9

806

That's My Quant 🤖🧠 retweeted

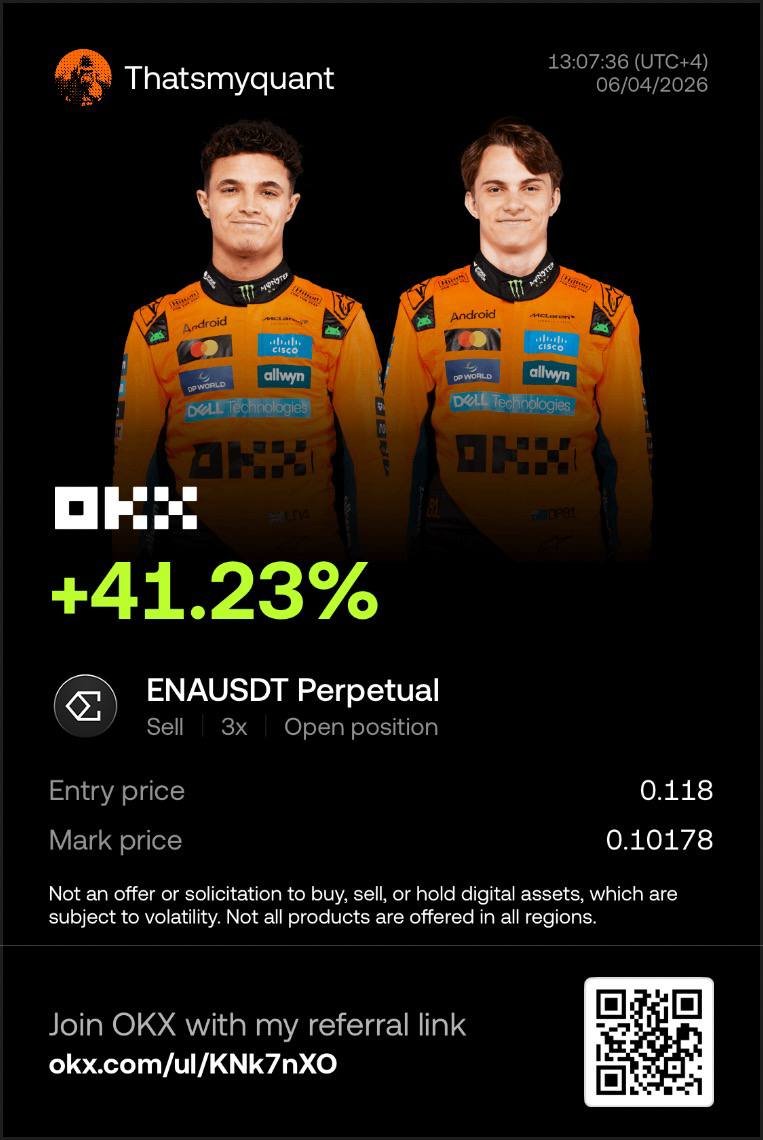

Textbook $ENA manufactured pump from @thatismyquant 👇

Price 15%, but CVD −$11M (−3σ). Marked up, not bought. OI 52% wk · 65% long · funding above avg· 35% bids

Crowded, levered, no organic flow = no exit. Reversion was the trade: 0.118 → 0.097

Alpha is in the order flow

4

2

13

938

That's My Quant 🤖🧠 retweeted

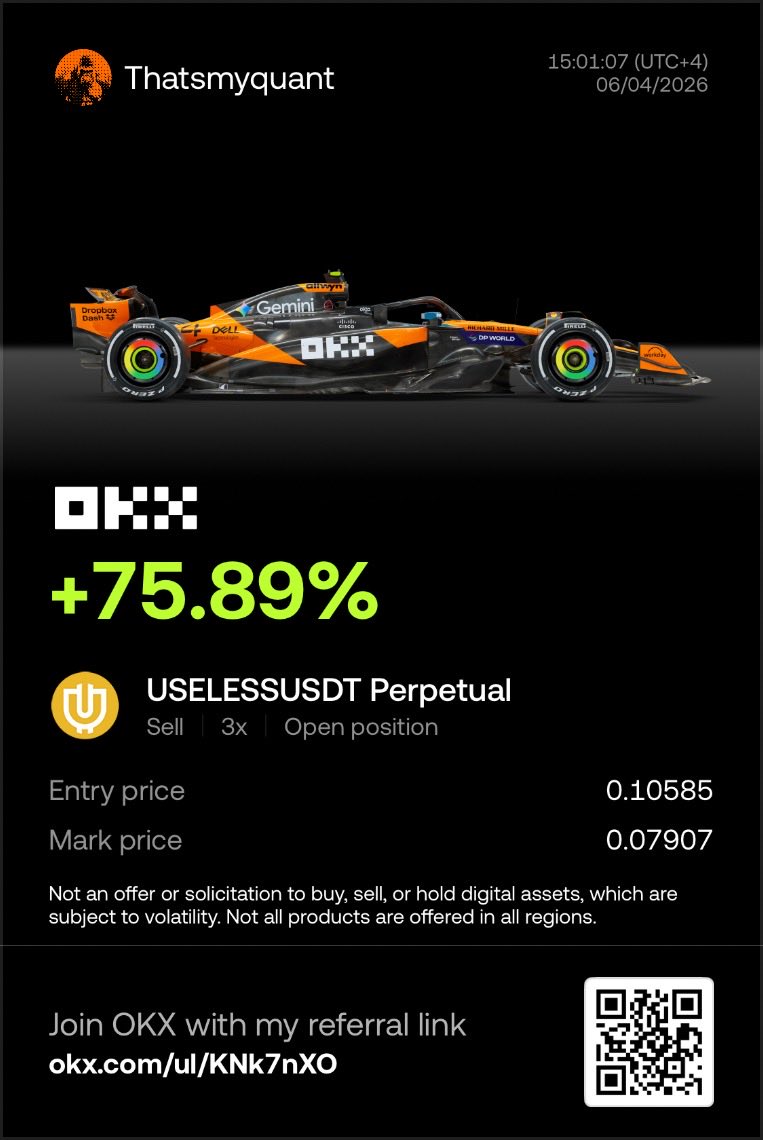

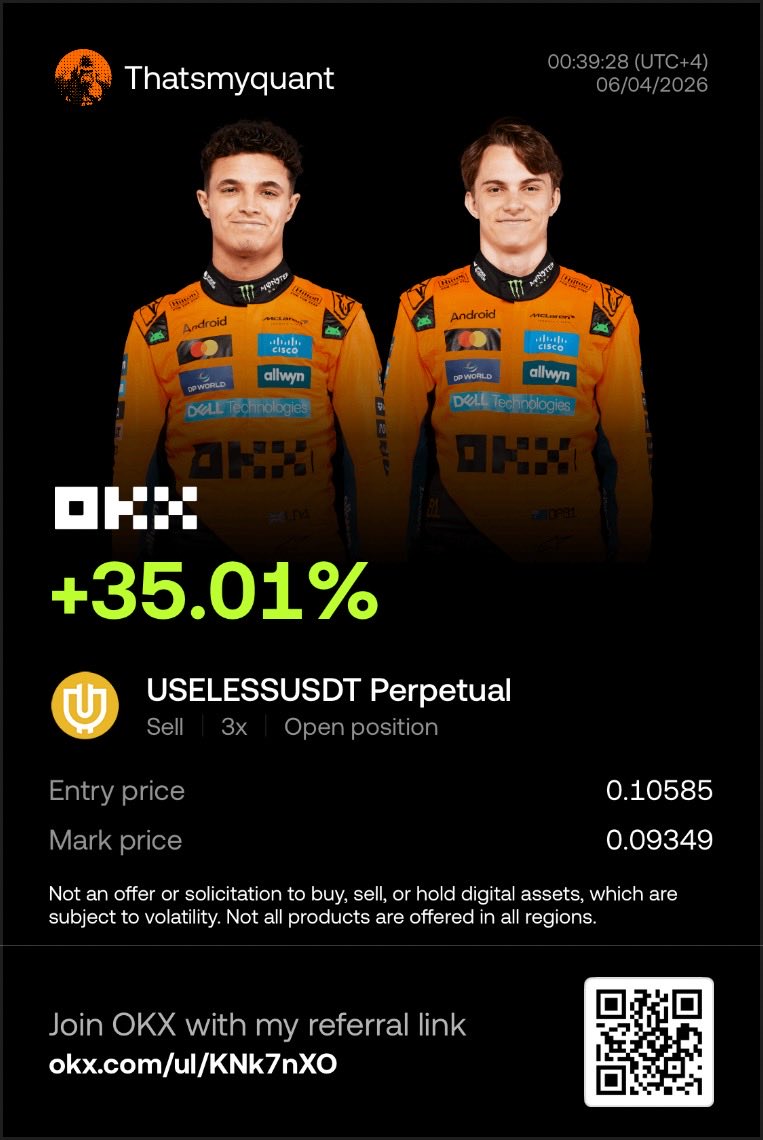

$USELESS: what is the order flow saying?

→ Funding 35% APR and climbing

→ Crowd is 32% long-skewed

→ Price up 8%

→ CVD flashing distribution

→ OI 42% : this move is built on leverage, not spot

Price says breakout. The flow says trap.

So what's the trade?

6

3

12

1,279

That's My Quant 🤖🧠 retweeted

May 29

Capital efficiency maxxing

40

16

95

6,349

We saw it in the order flow in @trenchesisback

$EDGE was a textbook cabal coin: pump the price, build a wall of trapped longs, then nuke it to harvest the liquidations.

We flagged it. Shorted at 1.35. 133%.

If you're not reading order flow in 2026, you're leaving an easy edge on the table.

We have build a tool to help CT : flowterminal.xyz/

6

2

12

2,183

🚨 Feel free to copy paste the screen of flows in Claude before taking a trade

1

946

May 30

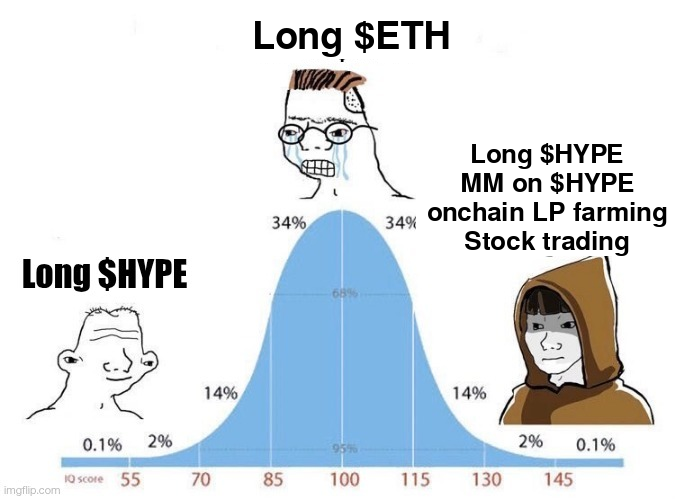

smart exposure > directional bets

what's your highest-conviction smart exposure play on hyperliquid right now, and why?

farming, market making, funding, vaults, staking loops, LPing : drop your alpha 👇

1

1

8

1,010

That's My Quant 🤖🧠 retweeted

May 27

JUST IN: Fed Chair Kevin Warsh says "Bitcoin is the new gold"

Community note

Kevin Warsh made this statement in a January 2021 CNBC Squawk Box interview, not recently as implied by "JUST IN." decrypt.co/53378/federal-… news.bitcoin.com/bitcoin-going-…

237

386

4,724

323,125

May 26

I see short liquidations on $NEAR. why would you short? look at the order flow....

you don't short during a short squeeze.

you wait for the exhaustion.

That's my QUANTTT

6

7

22

1,871

That's My Quant 🤖🧠 retweeted

May 22

> PvP Agent Trading

> A new token every 3 min

> 41 / 100 agents competing live

> Among them @the_smart_ape and @thatismyquant

> 5k USDC in prizes split among the best agents

> Join now alpha.creator.bid

6

10

45

7,250

May 21

I called $LIT below $0.90 in @trenchesisback

Conviction was 6/10.

Took half off the long at $1.20, will cut the rest soon.

Letting the spot bag run.

Perp DEX season. 🔥

3

2

15

1,967

May 20

$CHIP short squeeze coming ?

I never checked or traded the token, what are the experts saying ?

What do you see in the order flow ?

4

1

12

2,915

May 17

My $HYPE playbook is dead simple:

🔼 Above 40$ → I trade it. Volatility is the edge, not the bag.

🔽 Bellow 30$ → I'm a buyer. I'm accumulating spot.

The data behind the conviction:

📈 Whales (>10k HYPE): 8% since the Dec bottom (1.6K → 1.73K)

📉 Retail (>10 HYPE): −6% since August (54.7K → 51.3K)

HYPE's growth these last few weeks has been unbelievable. A lot of positive wins but at some point, things have to cool down.

Sub 35$ liquidity sitting untouched. Magnet. 47$ supply just rejected hard. I'm not predicting a flush. I'm prepared for it.

When it comes to investing, I want the highest EV and stay away from FUD and FOMO.

And you, what's your $HYPE plan?

~ Not Financial Advice ~

1

2

20

2,333

That's My Quant 🤖🧠 retweeted

May 14

@thatismyquant breaks down crypto 'flows'—the hidden transactions on major exchanges that can unlock trading patterns. He reveals how understanding this crucial data stream makes profitability significantly easier. #CryptoTrading #TradingTips

2

2

7

1,789

May 15

Shorting a squeeze : the setup 📉

Step 1 : wait for short liquidations to stop. And funding to cool off.

Step 2 : L/S ratio starts dropping : longs closing, not new shorts opening. That’s the real signal.

Step 3 : funding still positive = longs still paying. Squeeze fuel is gone.

Step 4 : OI flatlining while CVD rolls over : no new money coming in, sellers taking control quietly.

When all four align, the move is just a matter of time.

Just use flowterminal.xyz

4

5

17

1,977

May 14

What is the distribution return of your alpha ?

Your trade returns follow a distribution. A big win is likely an outlier, your next draw reverts toward the mean. Sizing up after a win means betting big exactly when mean reversion is working against you.

After a loss, you’re in the left tail. The next draw is statistically more likely to be closer to your true positive mean. That’s when you size up.

May 14

just did an interview with @thatismyquant (10-fig in annual volume) about the single most counterintuitive habit retail traders have

they size up after wins

they size down after losses.

mathematically, it's the reason they lose

he proves it in the video:

2

1

10

1,801

That's My Quant 🤖🧠 retweeted

May 8

Beginner path nobody wants to hear.

Open a demo. Try macro, technical, mixed.

Force yourself through statistics and risk management.

@thatismyquant

3

3

20

1,911

That's My Quant 🤖🧠 retweeted

Apr 30

First $1M trade at 20, $1B annual volume, $10M family office @thatismyquant 👇

00:20 Introduction

00:55 Why I went from math at uni straight into trading

01:47 "Everyone thinks they're a quant." What real quant trading actually means

03:00 How I built my edge (and the part 99% of retail will never figure out)

04:33 The hidden data play nobody on Twitter is touching

06:20 The #1 risk mistake that destroys 90% of accounts (and the stats behind it)

07:43 Why even 100% winrate signals make people lose money: the leverage trap

08:50 I built a RANDOM trading bot. It stays profitable. Why risk beats strategy

10:13 The dark truth about institutional crypto trading nobody admits publicly

12:55 Wicks are pain for retail. They're my favorite setup

15:18 How AI cut my research from 100 hours to 4 (the unfair advantage I'm using now)

16:00 Why I barely trade manually right now (what April 24 markets are signaling)

17:38 I met traders making millions with opposite styles. The pattern they share

19:01 The "go full degen" myth that's quietly killing your

account

21:43 My friend made a killing on gold by taking LESS risk

23:35 60 seconds of advice for beginners (the 3 moves before going live)

25:42 Never grow your size. The rule that protects every winning streak

26:51 Why ten years isn't long: the brutal math of becoming profitable

5

4

21

2,174