Joined July 2022

- Tweets 1,459

- Following 280

- Followers 10,898

- Likes 42,887

38 Photos and videos

Tim retweeted

Jun 12

Sadly, not part of SpaceX. But winning in my own way today :-)

63

13

1,367

133,750

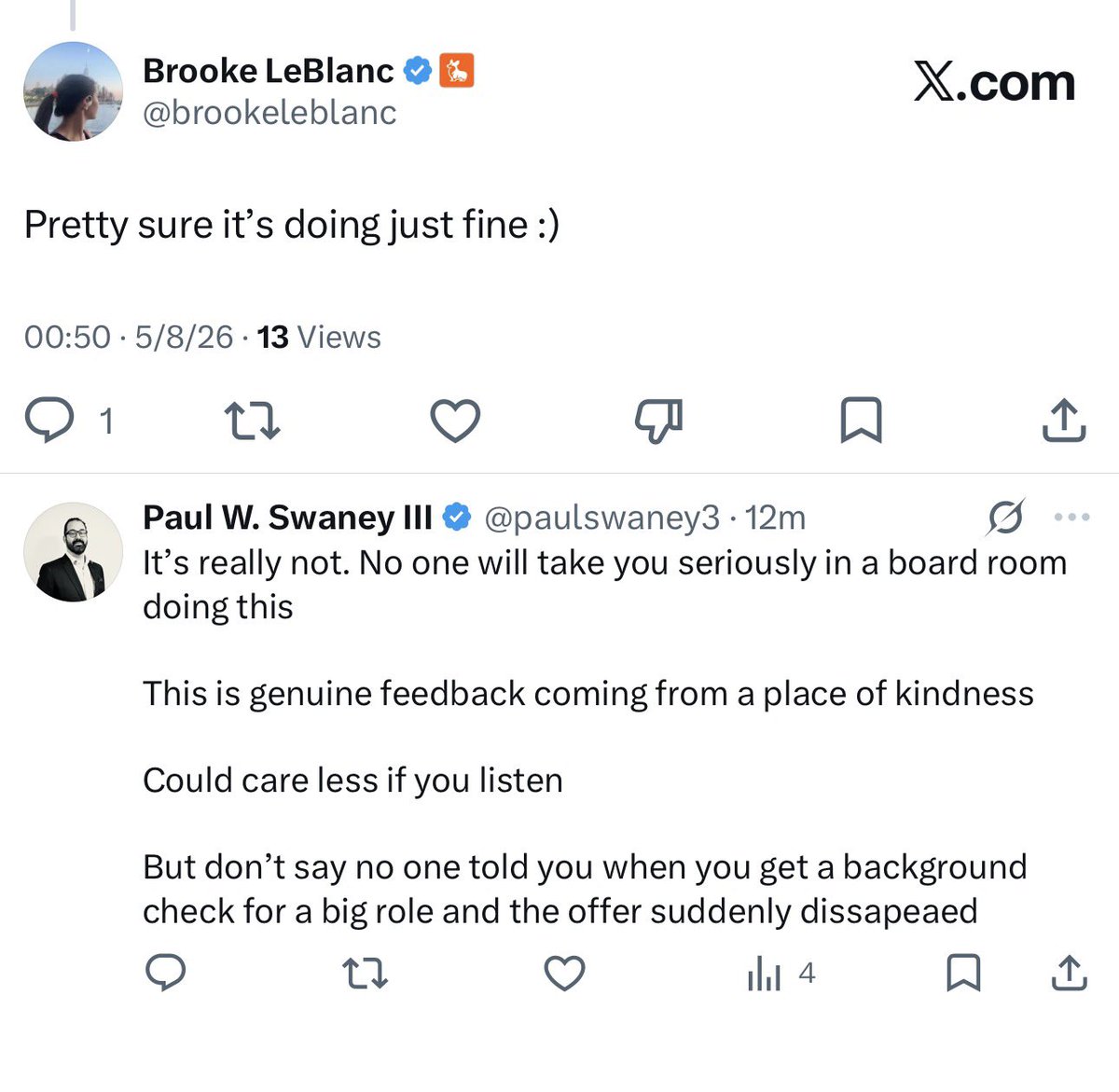

May 8

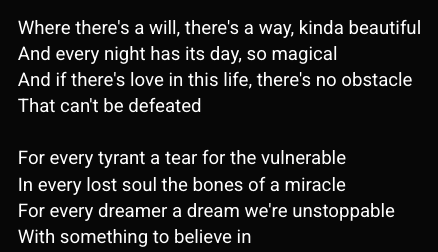

Many seem to profoundly underestimate the downstream impact their social media posts will have. Contrary to popular opinion, we have not made it to the point where nobody cares.

If you ever want to make it to relevant board rooms or even just get mid/high six-figure TC offers, people will run very extensive background checks on you.

I cannot even put into words how much authority a morning routine Insta Reel will cost you.

6

1

32

3,650

May 8

x.com/paulswaney3/status/205…

I wanna add a comment to this because it’s related. I looked through the profile he is referencing.

Posting photos from your run or other selfies the way it’s done in that case - from my experience - won’t be a problem.

I know a White House advisor and ME fund manager who posts shirtless workout pics on with 2010 Snapchat filter on Instagram, that’s ca where the line is I would say.

Just be mindful of what you put online.

Young people massively underestimate how their public social media can kill high-paying job offers

I have personally seen 5 offer letters pulled in NY over social media content. All were 300k plus total comp roles. Real cases

If you are aiming for 85k forever, you are probably fine

If you want bigger things, read this

1

3

1,341

Jan 5

The Danger of Unidentified Luck

We are addicted to causality. When something succeeds, we need a reason. The victorious founder tells a story of vision, grit, and strategic brilliance. The failed founder tells a story of bad timing, unfair markets, or betrayal. Both narratives are constructed after the fact, and both are largely fiction.

The company that survived 2008 and bought distressed assets may have had cash reserves, yes, but it may also have been lucky in its timing, its geography, its particular product cycle. A thousand equally prudent companies failed because their landlord raised rent at the wrong moment, because a key employee got sick, because a pandemic arrived from nowhere.

The human brain cannot tolerate randomness, so it manufactures stories. It sees patterns in static and calls them strategy.

Consider the famous "skill" of market timing. In retrospect, every successful tech founder saw the wave coming and positioned themselves perfectly. But at any given moment, thousands of equally intelligent people are positioning themselves for thousands of different waves - most of which never arrive. The ones who bet correctly get to write the history books - the others disappear without a trace.

Most business advice treats the market like a chess board - a closed system where the right sequence of moves guarantees victory. But business is poker played with a deck that keeps changing size. New cards are added mid-hand, old ones are removed, and occasionally the dealer lights the table on fire. Skill determines how you play your cards, but it does not determine which cards you are dealt.

The practical implication is not that effort is pointless - it is that humility is severely undervalued. The founder who believes their success is 90% skill will make very different decisions than the founder who suspects the ratio is closer to 50-50. The first will double down on their genius. The second will diversify, hedge, and remain paranoid

3

1

38

4,326

29 Dec 2025

The most dangerous lie in business is the level playing field. We are taught from a young age that fairness is a virtue. In the schoolyard, it is. In the market, it is a death sentence.

A fair game is one where the outcome is uncertain. It is a coin toss. If you find yourself in a situation where the odds are fifty-fifty, you have already failed. You are gambling with your time and your capital.

High-level operators do not play fair games. They seek out markets that are inefficient, opaque, or tilted in their favour. They look for the unfair advantage.

If you are competing on price, you are in a fair game. If you are bidding against ten other firms with the same credentials, you are in a fair game. These environments will strip away your margin until there is nothing left but the cost of your own labour.

The goal is to rig the outcome before the first move is made. You do this through proprietary data, deep political ties, or a brand that makes the competition irrelevant. You want a game where you are the only one who knows the rules.

Most people find this idea repulsive. They want to believe that hard work alone is enough. But the market does not reward effort. It rewards the capture of value. And value is easiest to capture where the competition is locked out.

When you hear someone complain that a situation is "unfair", listen closely. They are usually describing a moat they do not possess.

The "unfairness" they see is the result of someone else's superior strategy.

18

31

279

14,137

29 Dec 2025

The Alpha of Staying Alive

In professional tennis, points are won. In amateur tennis, points are lost.

The amateur defeats himself. He swings too hard, chases the impossible angle, and hits the ball into the net. The professional does something far less glamorous - he simply returns the ball, again and again, until the other player makes an error.

This observation comes from Dr Simon Ramo, one of the architects of the American intercontinental ballistic missile programme. He studied thousands of tennis matches and found that at the amateur level, roughly 80% of points are decided by unforced errors. The winner is not the player who hit the most brilliant shots. It is the player who made the fewest mistakes.

Business follows the same physics.

The default state of a company is death. Cash depletes, markets shift, founders burn out. Most businesses do not fail because they made the wrong move - they fail because they ran out of time to make the right one. The graveyard is full of companies that were six months away from success.

We romanticise the breakthrough. We study the pivot, the product launch, the genius insight. But these are the highlights. The underlying game is far more brutal: you must stay solvent long enough to get lucky. Survival is not a passive state. It is the most aggressive strategy available to you.

Every month you remain in the game, a competitor folds. Every quarter you stay solvent, the market consolidates in your favour. The longer you exist, the fewer players share the field. This is compounding, but in reverse. You are not trying to win every point. You are trying to be the last one standing when everyone else has exhausted themselves.

The most valuable opportunities are invisible to those who are fighting for their lives. When you are scrambling to make payroll, you cannot see the acquisition target that is about to become distressed. When you are one month from bankruptcy, you cannot negotiate from a position of strength. Cash is not idle capital but the ability to act when others cannot.

The 2008 financial crisis created more fortunes than it destroyed. The ones who emerged on top were not those who made the most aggressive bets. They were those who had the capital to buy when everyone else was forced to sell.

Consider the careers we celebrate as "overnight successes". James Dyson went through 5,127 prototypes over 15 years before producing a vacuum cleaner that worked. He was sustained by his wife's salary as an art teacher. He nearly went bankrupt multiple times in the process. He was not a gambler. He was an engineer of longevity.

The survivorship bias in business media creates a false map. We see the winners who took enormous risks and succeeded. We do not see the graveyard of thousands who took identical risks and vanished without a trace. The winner's narrative always sounds like courage. The losers' narratives are simply never written.

The irony: "staying alive" is perceived as a conservative, even cowardly, strategy. It is anything but. Most of your competitors are optimising for short-term wins. They are trying to hit the perfect shot, close the deal this quarter, show growth at any cost. They will burn through their runway, their relationships, their credibility - all in the pursuit of acceleration.

To win, you simply need to outlast them.

24

54

478

26,870

28 Dec 2025

The Psyop of Taking Risk

We are living through a cultural fetishisation of "the leap." Risk-taking has been elevated from a necessary evil to a moral virtue. We’ve turned the "all-in" moment into a status symbol. Most people view risk through the lens of bravery. They believe that the magnitude of the outcome is mathematically tied to the magnitude of the danger they face. This is a fundamental misunderstanding of reality. Risk and reward are decoupled. When the "hustle culture" echo chamber becomes loud enough, people start to believe that if they aren't terrified, they aren't dreaming big enough. They begin to seek out risk for its own sake, confusing the adrenaline of a gamble with the discipline of a strategy. In this environment, "taking a risk" is often just a mask for poor planning. The alpha has never been the willingness to jump off cliffs but the patience to build the most efficient bridge.

The market does not care how high your heart rate was when you signed the contract. It does not pay a premium for the nights you spent staring at the ceiling, wondering if you’d lose everything. If you achieve a billion-dollar exit through a sequence of low-risk, high-probability moves, the value of that capital is identical to the capital earned by someone who bet their house on a coin flip. The outcome is a product of your ambition and your execution, not the level of personal peril you endured.

What seems like an immense risk to the outsiders, is likely to be a very low-risk one to the high-performer - he has thought about it deeply.

Consider the logic of the "brave" path. If someone gave you the choice between a 100% chance of receiving $1 million and a 10% chance of receiving that same million with a 90% chance of total ruin, choosing the latter isn’t "living on the edge." It is simply stupid. Yet, we see this exact behaviour mirrored in the professional world every day. People choose high-volatility paths because they’ve been sold the lie that "big risk equals big reward." In reality, the high-risk path is often just the inefficient path. The goal is to reach the destination, and there are infinite routes to any single summit. Some are sheer vertical faces that require a leap of faith; others are paved, gradual inclines. There is no extra credit for choosing the path that might kill you.

True high-level operators are not risk-seekers; they are risk-mitigators. They spend their time ruthlessly identifying and eliminating points of failure until the "risk" is nothing more than a controlled variable. They understand that the "all-in" moment is often a sign of a failed strategy - a point where you’ve left your fate to chance because you lacked the foresight to secure the outcome earlier. The most impressive feats of entrepreneurship aren’t the ones that were a coin toss away from disaster, but the ones that were so well-planned they felt boring.

Not to say that it's impossible that an "all-in" type of path might become the only path you could possibly take, but it shouldn't be the goal to end up at such a point.

The more you can decouple your ego from the narrative of the "brave struggle," the more clearly you will see the low-friction routes that others are too "courageous" to take.

22

54

454

48,822

6 Dec 2025

> You start having an immense unsolvable pain in your life

> Depending on previous experiences you either dull it with drugs or work

> You dull it with work, but the work will results in bigger and more painful pain

> The pain can only be dulled with more work

> You get to the point where more work is not an option

> The pain is still there, it grows bigger everyday

> It can now only be dulled with more risk

> It must be so high-stakes, so dangerous, that you have to be in the moment

> This keeps you away from the pain

> You cannot stop, the pain grows

> The keep increasing the risk to get away from it

> You become a billionaire...

> You realise billionaires and crack addicts are essentially the same

4

5

91

6,880

2 Dec 2025

All in, all out.

Most entrepreneurs operate under the illusion that hedging their bets reduces risk. They keep a failing product line alive "just in case". They maintain a mediocre marketing channel because it brings in a trickle of leads. They keep a B-player employee because "hiring is hard".

They view this as diversification. In reality, they simply dilute resources.

In a winner-take-all economy, the middle ground is the kill zone. The returns on effort follow a power law, not a linear curve. Being 10% better than the competition doesn't yield 10% more revenue; it often yields 100% of the market.

To capture that alpha, you must adopt a binary mental model: All in, or all out.

There is no room for "dabbling". If a project is not worth an obsessive, overwhelming allocation of resources, it is worth exactly zero.

[1] Minimum Viable Intensity

Physics dictates that water at 99 degrees is merely hot. At 100 degrees, it boils and creates steam. That steam can power a locomotive. The single degree difference represents a phase shift.

Business works the same way. There is a threshold of intensity required to break through the noise.

If you allocate 10% of your budget to ten different channels, you will fail in all of them. You are competing against players who have allocated 100% of their budget to just one. They will out-bid, out-create, and out-last you.

You must aggregate your capital - both financial and cognitive - into a spear tip. You only enter a market if you intend to dominate it completely.

[2] The Zombie Tax

The most dangerous initiatives in your company are not the failures. Failures are easy to spot and easy to kill.

The dangerous ones are the "zombies". The projects that are doing "okay". The product features that are used by 15% of the user base. The regional office that breaks even.

These zombies consume massive amounts of mental capacity.

The "All Out" part of the model requires a ruthless stomach. You must be willing to kill moderately successful initiatives to free up oxygen for the potential unicorns. You have to sacrifice the good to buy the space for the great.

14

5

126

7,705

29 Nov 2025

The death of the average.

We are currently witnessing the total collapse of the marginal cost of creation. Copywriting, design, video editing - skills that previously commanded a premium due to the barrier of technical execution are being democratised to the point of irrelevance.

Most marketers view this through the lens of efficiency. They see a tool that allows them to produce 10x the output for 1/10th of the cost.

When the supply of "good enough" content becomes infinite, the economic value of that content plummets to zero. We are entering an era of infinite noise. If you think it is hard to capture attention now, wait until the internet is flooded with billions of synthetically generated articles, tweets, and videos every single day.

(Which is already happening, just not at the quality and volume that it will in 6, 12 months from now)

In this environment, pure volume is no longer a valid strategy. You cannot out-publish a server farm.

The alpha in modern marketing is shifting entirely from production to provenance.

[1] The Trust Premium

As the internet becomes increasingly synthetic, we will see a massive flight to safety. "Is this real?" will become the single most important buying criterion.

We are moving away from algorithm-optimisation and back towards human-optimisation. Personal brands, founders-led sales, and verified human voices will command an exorbitant premium.

The faceless corporate brand is dead. If a consumer cannot verify the human source behind the message, they will subconsciously label it as "spam".

[2] High-Friction Marketing

For the last decade, the goal was "low friction". SEO, programmatic ads, automated email sequences.

As AI cannibalises these low-friction channels, - bots clicking on ads served by bots on sites written by bots - the smart money will move to high-friction channels.

Live events. Physical mail. Handshakes. Closed-door dinners.

The harder it is to scale, the more valuable it becomes. You prove your value by doing things that cannot be automated.

[3] Taste as a Moat

Large Language Models function by predicting the next most likely token. By definition, they regress to the mean. They give you the average of the entire internet.

If you use AI to guide your strategy, you are opting for mediocrity at scale.

"Taste" - the human ability to curate, to select the outlier, to understand nuance and subtext - becomes the only defensible moat.

The future of marketing is about who has the taste to know what *not* to create.

Paradoxically, the more artificial the world becomes, the higher the premium on being undeniably human.

267

667

4,585

503,427

29 Nov 2025

When you exit your company, please hire somebody beforehand to optimise it.

So many unexperienced founders sell at a much lower multiple than they should be and leave millions on the table.

2

2

130

46,618

26 Nov 2025

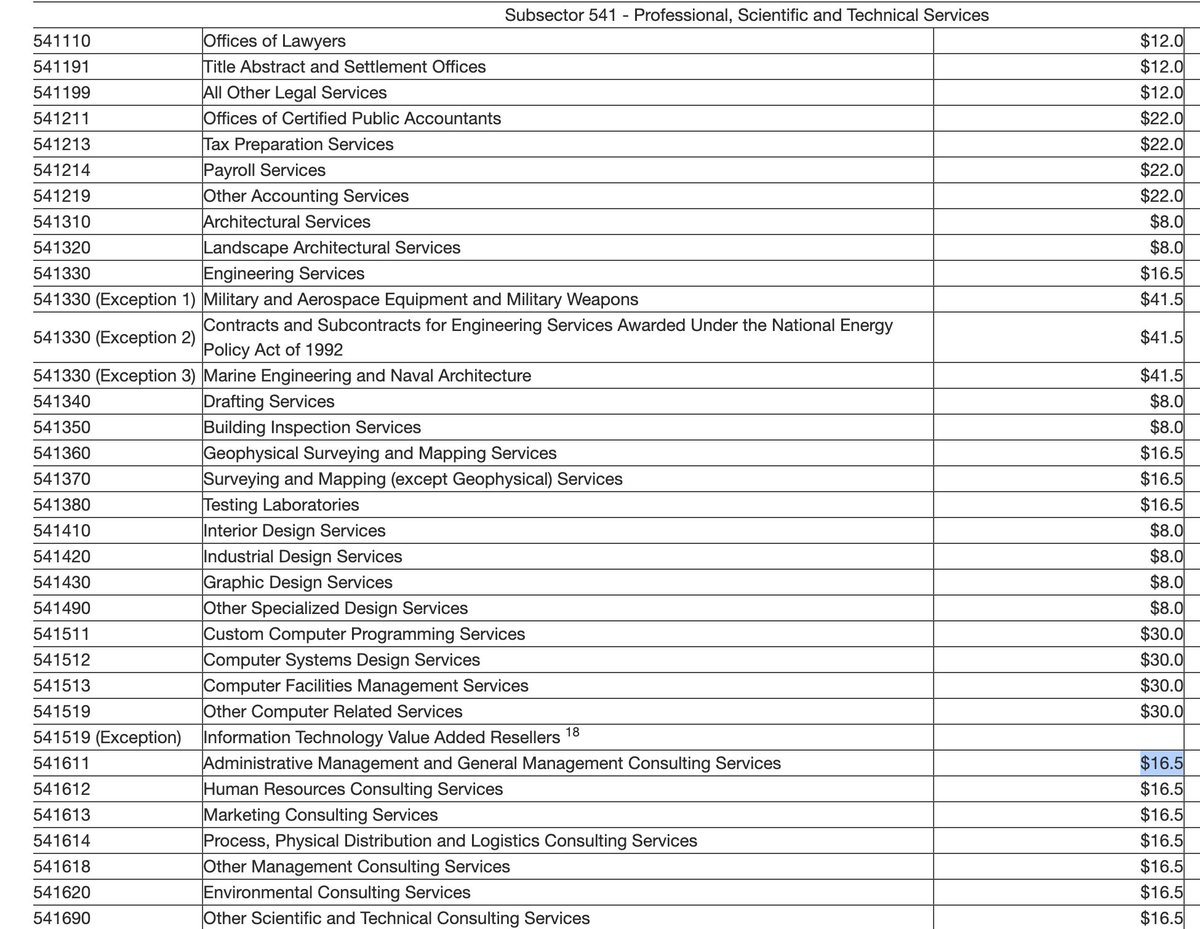

How Multi-Million Dollar Deals Are Done:

On X & social in general, "high-ticket sales" has become quite popular lately due to the info/education industry (where low-ticket is the entry level offer used to get people in the door, and high-ticket is the upsell). Because of that reason, the term itself is somewhat screwed. It doesn't actually refer to sales, but to the offers - which explains why sums of $5K are called high-ticket.

In reality, it's sort of an advanced entry level of sales. It's somehow both far away from the actual entry level (retail), and more advanced niches like B2B software.

But in this post I want to cover something much more interesting, how multi-million B2B or B2G deals are done. Essentially $5M - $50M.

When the contract value reaches this level, the process really shifts from persuasion to risk mitigation. You must navigate a political process and align with the internal governance of the buying organisation.

[1] Wiring the RFP

In government (B2G) or large enterprise, deals are officially awarded through a Request for Proposal (RFP) to ensure fair competition. However, seeing the RFP for the first time when it hits the public often means it is already too late.

Successful firms spend the months prior working with internal stakeholders to help define the problem statement. They effectively "wire" the RFP by inserting specific technical requirements - such as niche security certifications or proprietary integrations - that favour their own solution.

By the time the tender goes public, the scoring criteria are often weighted in a way that makes the outcome highly predictable. The public bidding process essentially becomes a compliance formality.

[2] The Buying Committee

Deals of this size are rarely approved by a single person. They require consensus from a committee where different members have competing incentives. A veto from any one stakeholder can stop the deal.

The political terrain usually consists of:

The Economic Buyer (CFO): Focused on Risk and Internal Rate of Return (IRR).

The Technical Buyer (CTO/CISO): Focused on governance, security, and integration.

The Champion: The internal executive whose objectives align with the project's success.

The strategy involves arming the Champion with the necessary materials to justify the purchase internally, rather than trying to pitch the entire committee directly.

[3] Financial Structuring

The price is often secondary to how the cost impacts the company's Profit & Loss statement. The CFO is usually more concerned with the accounting treatment than the total cost.

Deals are structured to fit the client's capital strategy:

CapEx (Capital Expenditure): If the company wants to protect its EBITDA, it may prefer to purchase software as a perpetual asset. This allows them to pay upfront but depreciate the cost over several years.

OpEx (Operating Expense): If the company is profitable but wants to manage cash flow, it may prefer a subscription model to write off the expense immediately.

[4] Playing the People

Relying on a single champion creates a massive single point of failure. If that person leaves the company, loses political capital, or gets fired, the deal dies instantly.

You need to build a consensus across the organisation. This is known as multi-threading. You are essentially running an internal political campaign where you need to secure votes from different constituencies.

However, the real art lies in understanding the difference between the Corporate Win and the Personal Win.

The Corporate Win: This is the ROI, the efficiency, the "business case". What goes in the slide deck.

The Personal Win: This is what actually drives the decision.

Every stakeholder has a selfish motivation that nearly always contradicts the company's stated goals. You need to map these out, a few examples:

The Climber: Wants a promotion. They need a "flagship project" to put on their resume to justify their move to VP.

The Survivor: Fears being made redundant. They are risk-averse. You sell them safety and compliance.

The Empire Builder: Wants to expand their department. They want more budget and more headcount.

You have to effectively "bribe" them with success. You show them that if this deal goes through, they get what they want personally.

Once you align your deal with their personal ambition, they stop acting like a buyer and start acting more like an embedded sales person. They will feed you internal information, coach you on how to handle their colleagues, and fight for you in closed-door meetings.

16

5

104

10,172

21 Nov 2025

High margins are useless if you are cash poor. The only way to hyperscale without debt is through negative working capital. You essentially force the market to finance your expansion at 0% interest. Collect the revenue weeks before the cost of delivery hits your account, use float to scale customer acquisition.

2

48

13,499

20 Nov 2025

Most of business is just labor arbitrage. You are exploiting the pricing inefficiency between what talent costs and what the market pays for the outcome. If you view the service as "work" rather than a tradable asset, you have already lost. Identify demand -> acquire the supply at wholesale -> capture spread.

2

8

96

4,738

19 Nov 2025

Something I didn't know back when I posted this is how many non-profits are just a scam and have nothing to do with the cause they advocate for.

I talked to someone who runs a government-funded non-profit today, and they have been involved in venture capital and have now started doing rollups.

Barely any of the money goes to the actual cause and nobody ever checks.

5 Jun 2025

The best fundraisers in the world are the ones who did real fundraising for real non-profits. If they convinced people to give them money for literally nothing in return, they can definitely convince people to give them money to (maybe) get more money back.

3

24

3,920

18 Nov 2025

Nobody really is in London anymore. Startup people have left long ago, fintech, PE, and some others stayed, but during the past year even they left.

Everyone goes occasionally, but barely anyone is still based there.

Not a good sign for the UK but also generally annoying bc now everyone is living in random cities. It became so much harder to meet people, everyone is async but IRL.

7

35

7,567

16 Nov 2025

I wonder what's the % of long-form text that's still fully handwritten. Must be in the single digits or even below 1%. It makes no sense to write entirely by hand anymore when you can just tell an AI how you want it, feed it with information, edit the output, and save hours.

1

18

1,713

16 Nov 2025

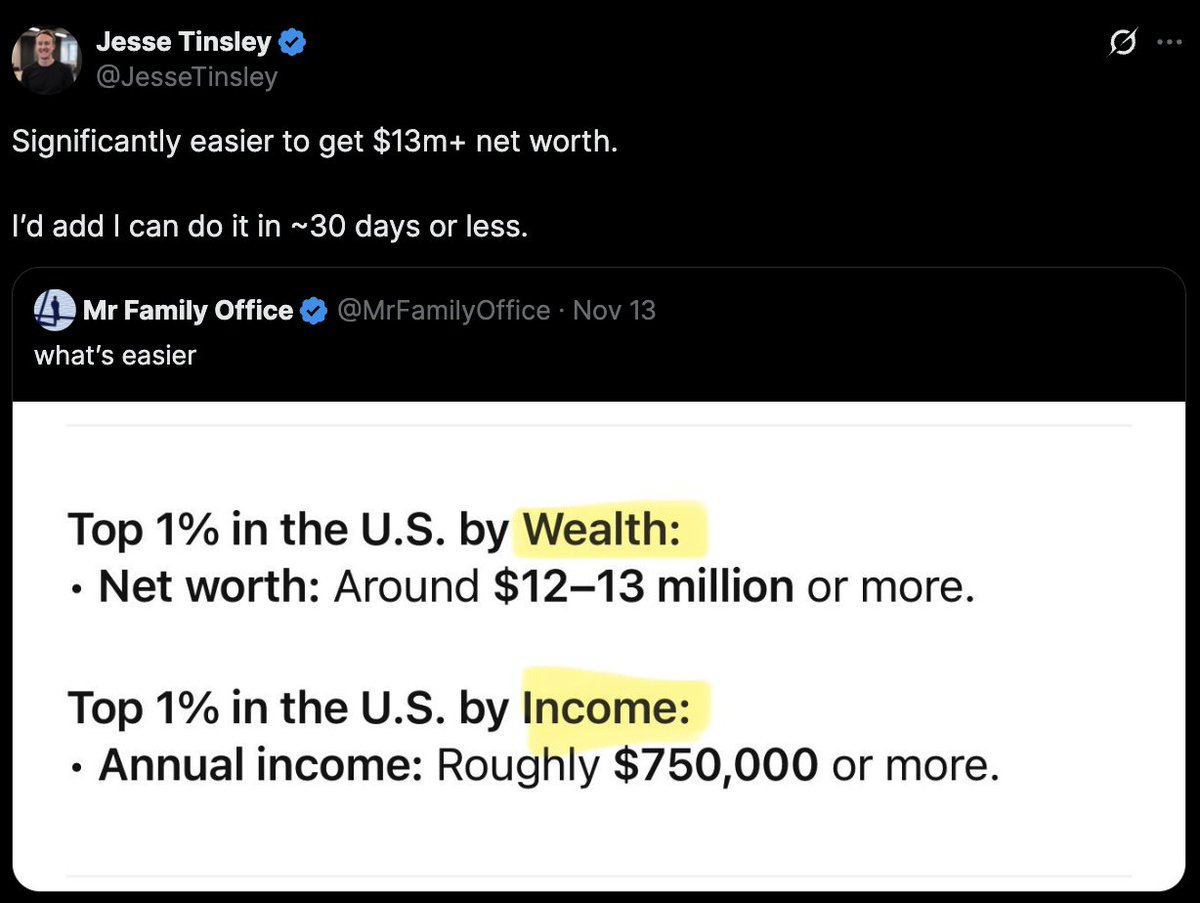

I'd argue that if you start with a budget of ~$20K, $750K annual income is easier to achieve. Without one (so fully from 0), it's the $13M NW for sure. But in both cases, achieving it within ~30 days is definitely doable.

15 Nov 2025

Significantly easier to get $13m net worth.

I’d add I can do it in ~30 days or less.

2

1

86

23,708

15 Nov 2025

Competing on price is a race to the bottom. Simply be the best only option, and win. Compete on quality or go be a loser.

6

1

34

2,135

14 Nov 2025

Many people have the believe that raising money - compared to bootstrapping - is taking the easy path, which in some cases it definitely is.

But that doesn't matter, all that matters is winning. In order to win, you must (1) be fast, (2) stack unfair advantages.

Raising a few million can put you years ahead, for many ppl it's the best thing they could do.

Though it does have it's disadvantages, and more than with bootstrapping, it's very important that you understand the game.

13 Nov 2025

With the right story you can raise pre-seed at $50M, what’s stopping you?

1

2

17

3,455