Joined December 2016

- Tweets 330

- Following 3,034

- Followers 1,277

- Likes 18

254 Photos and videos

The best Web3 investments do not just add capital to a cap table.

They add research discipline before launch, architecture pressure-testing before scale, and distribution support before the market decides who deserves attention

That matters because most failures in Web3 are not caused by “not enough funding”

They come from weak control rights, unclear upgrade paths, fragile incentives, and go-to-market that only works while sentiment is hot

Capital can extend runway

A real partner shortens the distance between thesis and reality

In 2026, the edge belongs to investors who can help founders make the next 3 decisions better:

what to build, how to govern it, and how to reach the right users without creating hidden execution debt

That is why TRIX Ventures treats co-building as underwriting, not a post-check service

What matters more in Web3 this year: the size of the round, or the partner that improves the system before it breaks

#TRIX #Ventures #Web3 #CryptoVC #Founders

2

The best Web3 investments do not start with a check

They start by reducing execution risk before it compounds

Capital is useful, but capital alone does not fix unclear control rights, weak distribution, messy incentives, or a product team that has to learn in public while the market is moving

That is why the best investors in 2026 behave less like financiers and more like operating partners

They help founders sharpen the thesis, pressure-test the architecture, open the right counterparties, and shorten the distance between decision and signal

In Web3, that matters more than ever because the cost of a bad decision is rarely immediate

It shows up later as governance drag, incentive decay, or a protocol that can launch but cannot scale cleanly

TRIX Ventures backs teams that want more than funding

Because the real edge is not the round itself

It is the quality of the next 3 decisions it makes possible

What matters more this year: the size of the check, or the partner set that improves the system before launch?

#TRIX #Ventures #Web3 #CryptoVC #Founders

1

Jun 13

Global capital networks are becoming the real moat in Web3 investing

Not because they write the biggest checks, but because they compress the hardest parts of execution: credible counterparties, cross-border distribution, and liquidity when one market turns cold

In 2026, the strongest investors are access layers. They help founders move faster across regions, open the right doors earlier, and avoid rebuilding trust from zero every time the market shifts

That is why TRIX Ventures treats ecosystem reach as part of underwriting, not a side effect

If capital is portable, what actually creates durable advantage in Web3: money, or the network that knows where to deploy it next?

#TRIX #Ventures #Web3 #CryptoVC #Founders

6

Jun 12

Capital is the entry point

Execution quality is the product

The Co-Builder model works because it changes what a round actually buys for a founder: faster research, tighter architecture, sharper go-to-market decisions, and fewer expensive mistakes before they compound

In Web3, passive capital can fund momentum. Co-building compresses the distance between thesis and reality

That is why TRIX Ventures backs teams that want more than a check. We help build the system with founders so it can survive launch, stress, and scale

What matters more in 2026: the size of the round, or the partner that improves the next 3 decisions?

#TRIX #Ventures #Web3 #CryptoVC #Founders

3

Jun 12

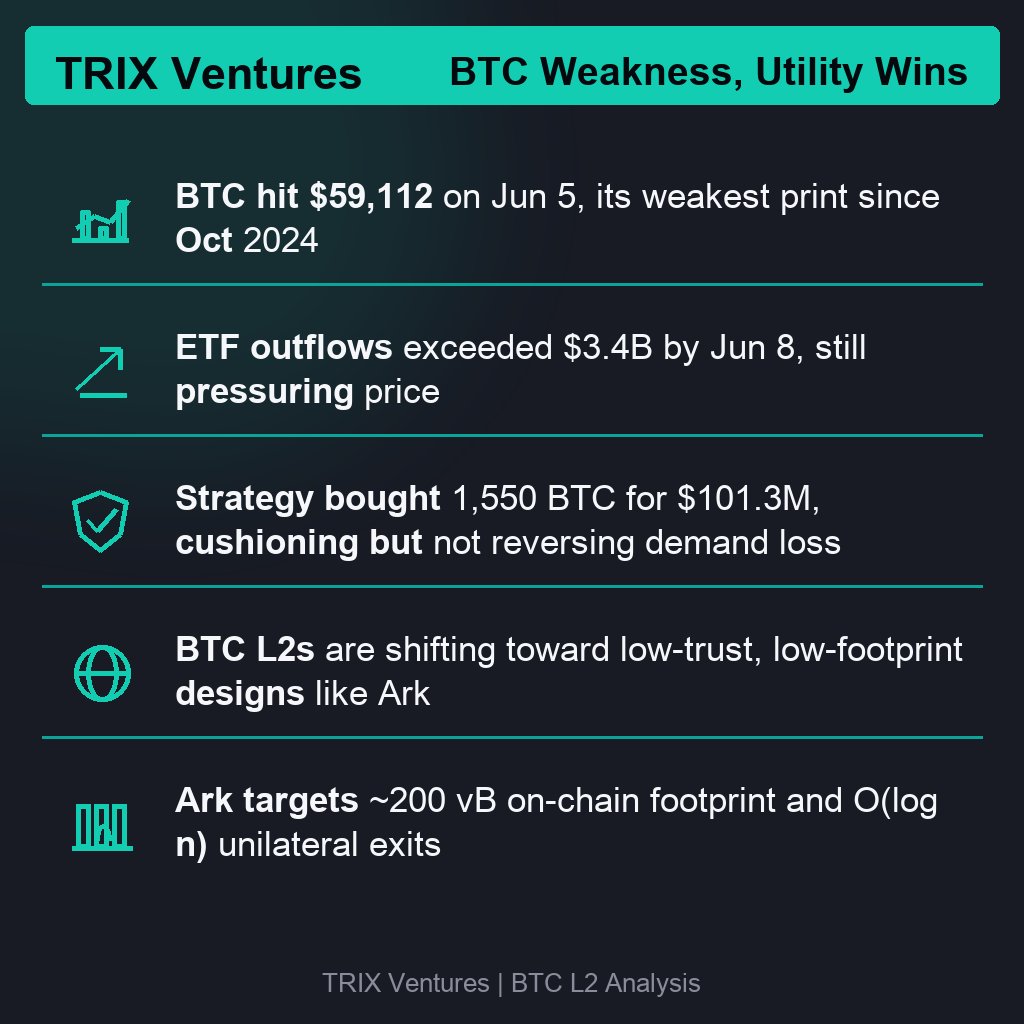

On Jun 5, BTC briefly traded at $59,112, the weakest print since Oct 2024, while ETF outflows pushed past $3.4B by Jun 8. That combination matters more than the bounce back to the $63k area. It says the marginal buyer is still ETF allocators, not native crypto reflexivity.

Strategy buying 1,550 BTC for $101.3M is supportive, but it also shows the split in demand. Treasury buyers are still averaging in, while public market flows are still leaking. In other words, balance sheet demand is cushioning price, but it is not yet strong enough to override passive outflows.

For BTC L2s, the signal is similar. The market is moving away from big-launch narratives and toward architectures that reduce trust and on-chain footprint. Ark’s off-chain batching design, with roughly 200 vB constant on-chain footprint and O(log n) unilateral exits, is interesting because it targets the real bottleneck. Bitcoin scaling does not need more branding. It needs lower friction, cleaner exits, and fewer assumptions.

The near-term takeaway is bearish on hype, cautiously bullish on infrastructure. BTC can recover while the ecosystem still looks weak, but the next durable winner is likely the design that looks boring to speculators and useful to settlements. The contrarian question is whether the BTC L2 market is finally being built for utility, or whether it is still searching for a narrative big enough to attract capital before real usage arrives

#TRIX #Ventures

6

Jun 12

The smartest founders do not raise capital first

They raise partners who can compress the next 12 months: sharpen the model before launch, open the right counterparties, and help distribution arrive faster than execution debt can pile up

In Web3, a round is not just money on the balance sheet. It is a decision about who gets to influence architecture, hiring, governance, and go-to-market when the market turns

The best investors reduce error, not just extend runway. Which matters more in 2026: the largest check, or the partner set that makes the next decision better?

#TRIX #Ventures #Web3 #Founders #CryptoVC

4

Jun 11

A good Web3 project can work

A great one can still be understood when the team changes, the market turns, and the first assumption breaks

That is why architecture matters beyond code quality

It decides three things at once

How fast new contributors can reason about the system

How much damage a failure can contain

How expensive it is to change direction without turning the upgrade into a governance event

If every fix requires heroics, the project is already paying execution tax

TRIX Ventures looks for systems where control rights, upgrade paths, and failure boundaries are explicit before scale arrives

Because in Web3, architecture is not just how a product is built

It is how risk is priced

What is usually left vague first in most projects: upgrade power, dependency design, or who absorbs the first failure

#TRIX #Ventures #Web3 #DeFi #Tokenomics

4

Jun 11

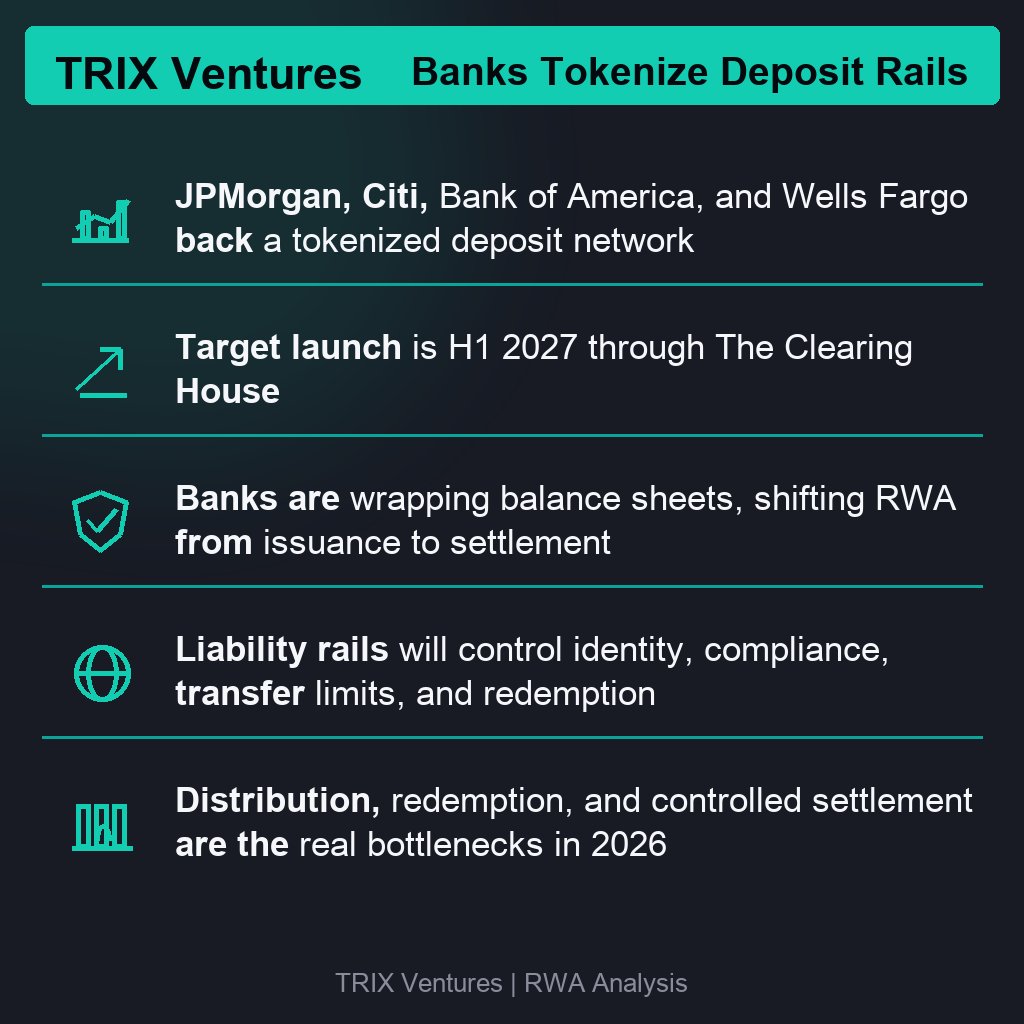

JPMorgan, Citi, Bank of America, and Wells Fargo are backing a tokenized deposit network through The Clearing House, with a target launch in H1 2027.

The real RWA update in 2026 is not another asset getting wrapped. It is banks deciding to wrap their own balance sheets.

That matters because the center of gravity shifts from issuance to settlement. Most RWA conversations still start with the token. The bank version starts with the rail. If the rail is faster, always on, and built for treasury and liquidity management, the token becomes a byproduct of infrastructure rather than the product itself.

This is a very different market structure. Asset tokenization tries to create new onchain instruments. Tokenized deposits try to modernize the most important liability layer in finance. If banks control the liability rail, they control identity, compliance, transfer limits, and redemption. That is where the moat moves.

Bullish on the infrastructure stack that can sit between bank balance sheets and onchain venues. Less bullish on wrappers that still assume issuance alone creates liquidity. In 2026, headline TVL is not enough. Distribution, redemption, and controlled settlement are the real bottlenecks.

Bottom line: RWA is starting to look less like a token category and more like a settlement architecture war. If banks own the liability layer, how much of the public RWA stack is actually infrastructure, and how much is just interface?

#TRIX #Ventures

12

Jun 11

In 2026, the alpha in DePIN, AI agents, and RWA is not “which narrative is hottest”

It is which sector can reduce verification cost the fastest

DePIN works when real usage is observable and unit economics are local. If demand only exists because hardware is subsidized, it is not infrastructure, it is burn

AI agents work when a narrow job can be executed end to end with permissions, receipts, and settlement. Generic “agent platforms” are getting crowded fast. The edge moves to agents that actually complete tasks, not just talk about them

RWA works when tokenization changes access, collateral, or distribution of cash flow. Wrapping assets without improving liquidity or risk control is just a new label on old plumbing

The common thread is simple: capital can underwrite systems faster when usage, execution, or cash flow can be verified with less friction

That is where TRIX Ventures sees the next wave of Web3 alpha

Which of the three has the clearest path from narrative to measurable operating advantage this year?

#TRIX #Ventures #DePIN #AIAgents #RWA

3

Jun 10

Good Web3 projects don’t win by adding more features

They win when architecture makes change cheap and failure local

If new contributors can read the system fast, upgrades can land without rewriting the stack, and one broken module does not drag the whole protocol down, the project keeps its optionality when the market turns

That is where TRIX Ventures sees the gap between good and great

What does your stack optimize for first: speed, resilience, or control

#TRIX #Ventures #Web3 #DeFi #Tokenomics

3

Jun 10

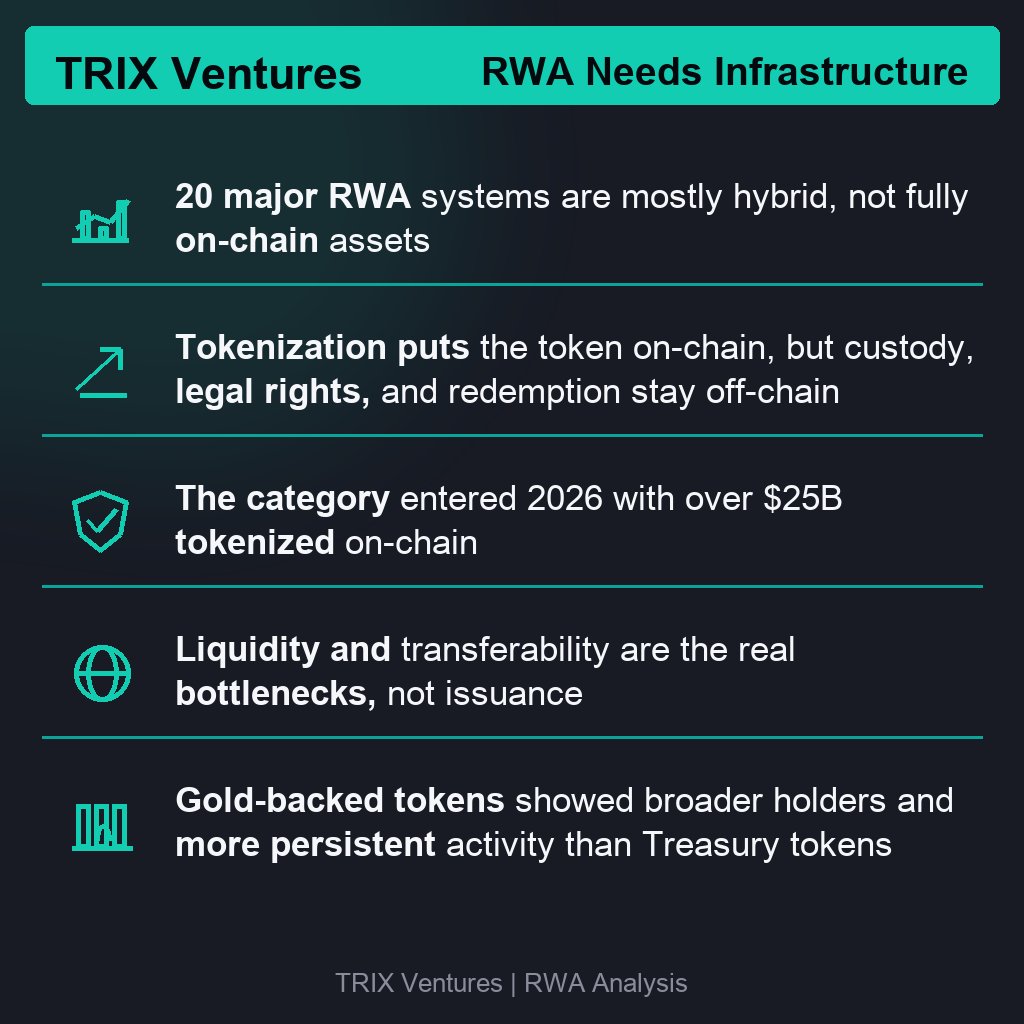

A new June 2026 paper mapped 20 major RWA systems by market cap and found the same thing hiding across the category: tokenized RWAs are mostly hybrid structures, not fully on-chain assets.

The token moves on-chain. The legal claim, custody, verification, and redemption logic still live off-chain.

That matters because it changes what “RWA market growth” actually means. The category entered 2026 with more than $25B tokenized on-chain, but the real bottleneck is no longer issuance. It is liquidity, transferability, and whether the asset can survive outside a whitelisted wrapper.

A second May 2026 study using RWA.xyz data makes the point even harder. Gold-backed tokens showed broader holder bases and more persistent activity than many Treasury and private-credit tokens, while headline asset value alone did not reliably predict trading depth.

Translation: TVL is not the same thing as a market.

The market is splitting into two buckets. One bucket is assets that look big on a dashboard but behave like static balance-sheet products. The other is assets with real secondary activity, clearer redemption paths, and enough distribution to matter outside crypto-native circles.

That is why the most important RWA names are not just the issuers. They are the stacks that can handle compliance, custody, redemption, transfer controls, and distribution at scale. The market is slowly moving from “can this be tokenized?” to “can this be settled, traded, and redeemed without breaking the legal wrapper?”

Worth watching: the same week, JPMorgan, Citi, and other big banks disclosed plans for a tokenized deposit network by H1 2027. If bank balance sheets become the preferred settlement layer, the winner may not be the best tokenized asset. It may be the rail that controls who can move, finance, and exit it.

Bullish on RWA tokenization as market infrastructure.

Bearish on the idea that tokenization alone creates liquidity.

The harder question is this: in 2026, is the moat the asset token itself, or the compliance and redemption stack behind it?

#TRIX

#Ventures

9

Jun 10

Funding is not the edge. Reducing execution debt is

In Web3, capital only matters if it also compresses the next 12 months: cleaner research, tighter architecture, faster iteration, and stronger distribution before hidden risks compound

That is the Co-Builder model. TRIX Ventures does not stop at the check. TRIX Ventures helps shape the system with founders so the business is built for launch, stress, and scale

If an investor cannot improve the next three decisions, what exactly are they financing?

#TRIX #Ventures #Web3 #Founders #CryptoVC

3

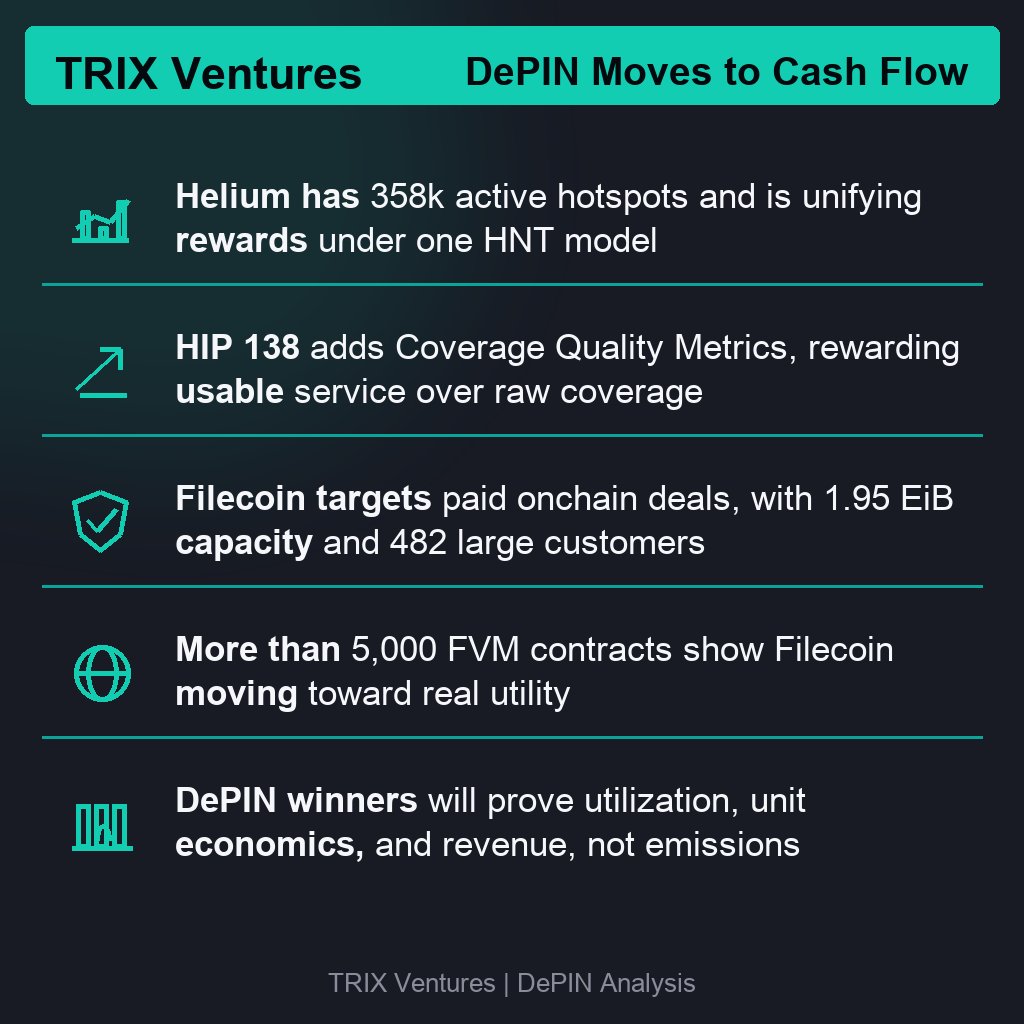

Jun 9

Helium now has 358k active hotspots, and HIP 138 is pushing IoT and Mobile rewards into a single HNT model with Coverage Quality Metrics. At the same time, Filecoin is explicitly repositioning around paid onchain deals and profitability, while its network stats show 1.95 EiB of storage capacity, 482 large customers, and more than 5,000 FVM contracts.

That combination matters because it exposes the split inside DePIN in 2026: networks with verifiable demand are moving toward cash-flow discipline, while networks still relying on emissions are getting harder to defend. The market is no longer pricing “decentralized infrastructure” as a theme. It is pricing utilization, unit economics, and whether a network can survive without permanent subsidy.

The bullish case is narrow but real. Compute, storage, and wireless are starting to look like businesses, not experiments. Filecoin’s shift toward paid deals says the category understands that token incentives are only the bootstrap, not the moat. Helium’s move toward quality-based rewards says the same thing from the connectivity side: coverage without usable service is just inflated supply.

The bearish case is everything that cannot prove paid usage, retention, or a measurable cost advantage. In a market that still treats high-beta assets harshly, token emissions without revenue are a liability, not a growth strategy.

Bottom line: bullish on DePIN as infrastructure with invoices, skeptical on DePIN as a token distribution mechanism pretending to be infrastructure. The next winner is unlikely to be the largest network. It is more likely to be the one with the cleanest bridge from on-chain incentives to off-chain payment.

The real question is whether DePIN can finally stop selling decentralization and start selling operating performance

#TRIX

#Ventures

3

Jun 9

The most expensive part of a bad Web3 round is not the check. It is the time lost proving the thesis was weak

Due diligence is not about slowing down. It is about stripping out false signal before the market starts rewarding it. The useful questions are blunt: does demand still exist when incentives normalize, does the token still work when emissions slow, and can the system change course without governance theater

FOMO pays for a story first and discovers the operating model later. Research-first investing does the reverse: it pressure-tests failure modes, control rights, and distribution quality before capital turns momentum into hidden debt

In 2026, the best partners are not the fastest to wire. They are the ones who make the next three decisions better before the crowd arrives

What is still overpriced in Web3: traction, token design, or distribution?

#TRIX #Ventures #Web3 #DeFi #CryptoVC

4

Jun 8

TRIX Ventures sees architecture as the line between a project that ships and a project that lasts

A good Web3 project can launch

A great one stays readable under stress

The real test is simple:

Can new contributors understand it fast

Can upgrades happen without rewriting the stack

Can one failure stay local instead of turning into a system-wide problem

Architecture is not aesthetics. It is the operating logic that decides whether complexity compounds or leaks

What is most often left vague too early: dependency design, upgrade paths, or failure boundaries?

#TRIX #Ventures #Web3 #DeFi #CryptoVC

7

Jun 8

On 1 July 2026, MiCA’s EU transitional period expires. ESMA says any crypto-asset service provider still without a MiCA licence must stop serving EU clients. That is not a headline risk. It is a hard operational cutoff

The pattern is broader than Europe. Hong Kong licensed only 2 stablecoin issuers on 10 April 2026, Anchorpoint and HSBC. The UK FCA selected 4 firms for its stablecoin sandbox in February and says final stablecoin rules will land later in 2026. Different jurisdictions, same message: crypto is moving from permissionless distribution to permissioned market access

This matters because regulation is becoming a moat, not just a cost. The winners in 2026 will not be the loudest venues or the fastest launchers. They will be the firms that can clear licensing, custody, AML, and disclosure in more than one market without rebuilding the stack every time the map changes

Bullish on compliance-native infrastructure, licensed stablecoin rails, custody, and payments systems that can port across regions. Bearish on businesses that still treat regulatory arbitrage as a durable strategy

The real question is whether tighter rules shrink crypto, or finally separate real market infrastructure from everything built to outrun the rulebook

#TRIX #Ventures

11

Jun 8

Tokenomics is the only part of a protocol that has to survive 3 regimes: bootstrapping, equilibrium, and stress

Most designs optimize only for the first one. They overpay for attention, underprice real usage, and leave no clean answer for what happens when speculation fades. The result is a token that can launch, but cannot govern, retain, or distribute value

TRIX Ventures sees the backbone in a simple test: does the model still work when emissions slow, users get rational, and incentives need to be changed without breaking trust? If not, it is not tokenomics. It is short-term marketing in protocol form

What usually fails first in 2026: bootstrapping incentives, value capture, or governance reset rights?

#TRIX #Ventures #Web3 #Tokenomics #DeFi

6

Jun 7

On 2026-06-03, Mastercard said it will add stablecoin settlement as a network-level option, including intraday, weekend, and holiday settlement, with support for USDC, PYUSD, USDG, USDP, RLUSD, and SoFiUSD across Arbitrum, Base, Canton, Ethereum, Polygon, Solana, Tempo, and XRPL

That is a bigger signal than another crypto partnership

It means stablecoins are no longer being treated as a parallel rail for traders and onchain users. They are being inserted into the settlement stack of the existing payments network, where the real bottlenecks live: cutoff windows, treasury friction, cross-border latency, and working-capital drag

The same week, Stripe and Deel pushed stablecoin wallets into global contractor payouts across 150 countries, MoneyGram launched MGUSD on Stellar, and Fireblocks rolled out Flow for PSP and fintech stablecoin acceptance. Different products, same direction

The market is now converging on one thing: stablecoins are becoming the default liquidity layer for payout, settlement, and merchant flow. Not because crypto won a narrative battle, but because the economics of moving dollars are better when the rail is programmable, always-on, and interoperable with existing fintech infrastructure

That is bullish for issuers, payment orchestration, custody, on/off-ramp, compliance, and treasury tooling. It is less bullish for any “stablecoin layer” that depends on speculation, isolated distribution, or a crypto-native UX that normal users never see

The key question for 2026 is no longer whether stablecoins can scale. It is whether the moat sits with the token, the network, or the distribution layer that decides which stablecoin gets used at checkout, in payroll, and in cross-border settlement

What happens when the winner is not the best stablecoin, but the one most deeply embedded into the rails everyone already uses?

#TRIX #Ventures

16

Jun 5

In 2026, the scarcest resource in Web3 is not attention. It is accurate translation

TRIX Ventures treats community education as translation infrastructure, not a marketing add-on. It turns curiosity into qualified users, users into contributors, and contributors into distribution. It also surfaces product gaps earlier, before support debt compounds

The strongest growth loops are not louder. They are clearer

When a community can explain the model back cleanly, what else compounds faster?

#TRIX #Ventures #Web3 #DeFi #CryptoVC

3

Jun 4

The smartest founders do not raise capital to buy time.

They raise partners who compress time to product, time to trust, and time to distribution. In Web3, a check without operating depth, market access, or conviction often becomes expensive dilution with no added leverage.

Capital quality matters more than capital size in 2026. The best rounds are built with investors who can help shape the system, pressure-test the model, and open the right doors before launch debt turns into execution debt.

That is the standard TRIX Ventures backs.

Which matters more at the seed stage: the largest check, or the partner who can help the company win the next three quarters?

#TRIX #Ventures #Web3 #Founders #VC

1