Joined July 2017

- Tweets 7,683

- Following 300

- Followers 973

- Likes 10,886

539 Photos and videos

Pinned Tweet

Jun 11

1/ Your bank charges you fees and says "thank you for your loyalty."

Crypto cards in 2026 literally pay you to exist.

I ran the real numbers on etherfi, Bybit, Cryptocom and Nexo - not the marketing numbers.

The winner isn't who shouts loudest. Thread 🧵

9

7

68

11,467

1/

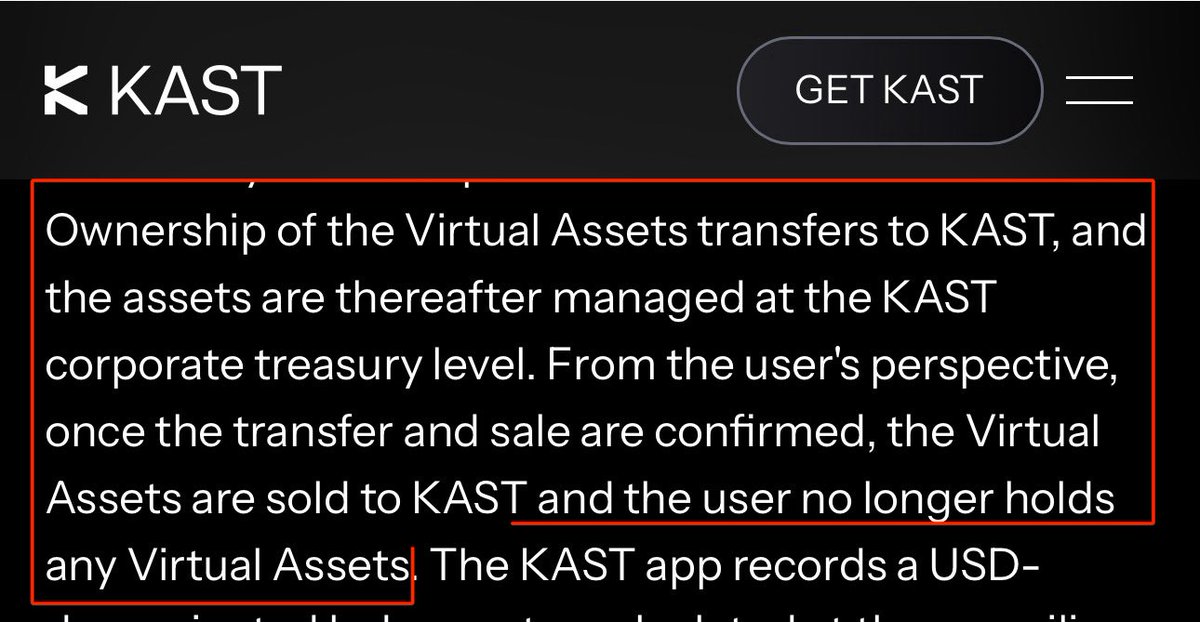

The money on your crypto card is it actually yours?

If your card is one of these, the legal answer is literally no. You sold it to the company. It’s right there in their terms 👇

Most people have no idea. Let’s fix that. 🧵

13

4

44

16,881

4/

One test cuts through every marketing page:

“If this company vanished tonight, where’s my money tomorrow?”

Custodial: in their bankruptcy paperwork. Ask FTX users, three years and counting.

Self-custody: right where it was. You withdraw and move on.

But there’s a second layer most people miss. A few “self-custody” cards still route your money through OUTSIDE protocols to earn yield. When one got exploited recently, users lost funds and the card’s answer was “we never held your money.” Technically true. Try spending technically true.

So ask both: who holds the money, AND whose protocol earns the yield. If you can’t answer the second one, that’s your answer.

1

3

752

5/

Where I landed: code risk exists everywhere in DeFi, anyone claiming otherwise is selling something. The difference is how it’s managed.

@ether_fi runs its own audited vault contracts, hard limits on what strategists can touch, blue-chip protocols only, a bug bounty, and billions in TVL riding on not screwing up. Managed, diversified risk, not risk quietly handed to a third party they can blame later.

That’s why I run it daily full breakdown, downsides included, in my pinned thread. Coat stays on.

Questions → replies. Thx 🙏

1

4

713

Jun 12

Been thinking about something that doesn’t add up.

Crypto cards are having their best year ever volumes, users, growth charts pointing at the moon. And the tokens behind these cards? Bleeding. Quietly, consistently, all of them. How does a product win while its token loses?

Took me a while, but here’s what I landed on.

When you swipe a card, the fees go to the card program and the payment rails. The token gets… nothing. It’s not part of the business it just stands next to it wearing the same logo. A million swipes create exactly zero buy pressure. That’s the whole mystery, honestly. The money never touches the token.

It gets worse when you look at the metrics everyone celebrates. Those promos and airdrop seasons aren’t growth they’re the treasury buying the appearance of growth. And a lot of those “users” are farmers anyway.

One project filtered for real humans recently and 90% of airdrop participants didn’t make the cut. Ninety. Percent. Meanwhile the unlocks keep hitting every month, insiders keep getting liquid, and the chart does what charts do under constant sell pressure.

So no, the market isn’t broken. It’s pricing these tokens exactly right as marketing instruments, not businesses.

But here’s the part that actually has me interested.

This is fixable, and the teams know it. They watch their tokens bleed while their cards win, same as we do. The next war in this space won’t be over cashback percent - it’ll be over token utility. Revenue share. Buybacks funded by card fees. Holder perks that cost the company something real. And the first project that genuinely wires the swipe to the token is going to rerate violently, because it’ll be the only chart that finally matches its product.

Well guys, that’s the actual trade here. Ignore the dashboards. Wait for the announcement where revenue gets connected to the token that’s the entry. Everything before it is a poster.

Genuinely curious what people think 👇

4

2

6

386

Jun 12

Noticed something?

Everyone in crypto is launching a card right now. EtherFi, Plasma, Jupiter, MetaMask, Tria, KAST feels like a new “crypto neobank” drops every other week.

And the numbers back it up - stablecoin card spending grew ~673% last year, Visa and Stripe are pushing these rails into 100 countries.

This part is real.

But here’s the thing that keeps bugging me. Fintech already ran this movie. 76% of traditional neobanks never turned a profit. The ones that won Nubank, Revolut don’t actually make money on card swipes. Nubank makes 85% of its revenue on interest. Credit is the business. Cashback was always just the bait.

Now look at crypto cards: most are competing on… cashback %. The exact playbook that already failed once. Launching a card got cheap, so everyone launched one. Cheap to launch = no moat.

So my filter changed. I stopped asking (what’s the cashback) and started asking (what’s the business when the promos end) Real protocol underneath, real yield, credit products or just a card with a marketing budget?

Don’t get me wrong, I love this trend self-custody cards are the first crypto thing my normie friends actually get. But in 3 years most of these cards are gone. The ones sitting on real protocols stay.

Which ones survive?

My bets, on the record ✍️

@ether_fi own protocol with $7B TVL doing the heavy lifting, credit product instead of cashback theater, and the card is just the front-end of an actual business.

@gnosispay Safe infrastructure underneath, the most battle-tested self-custody stack in crypto. Rough patch lately, but rails good

@MetaMask not the best card imo, but 100M wallets of distribution. They can be third-best product and still win on reach alone.

Screenshot this boys. See you in 2029.

5

13

2,006

Jun 12

Plasma One just published its card tiers. I did the math — and you might want to sit down. 👇

Platinum tier = lock 100,000 XPL for 12 months.

That’s somewhere between $9K and $13K depending on which hour you check the price swung 44% this week alone. Which kind of proves the point about locking a volatile token for a year.

Core tier = $120/year OR lock 10,000 XPL (~$1K ).

So the “free crypto card” from all those comparison charts… isn’t free. Read that again.

Custody check (first thing I verify now): Plasma One IS genuinely self-custodial — your stablecoins stay in your wallet. Credit where due, that beats most cards out there.

But the model is naked once you see it: your cashback rate = how much of THEIR token you buy and lock. The card isn’t the product. You are the exit liquidity.

Now compare:

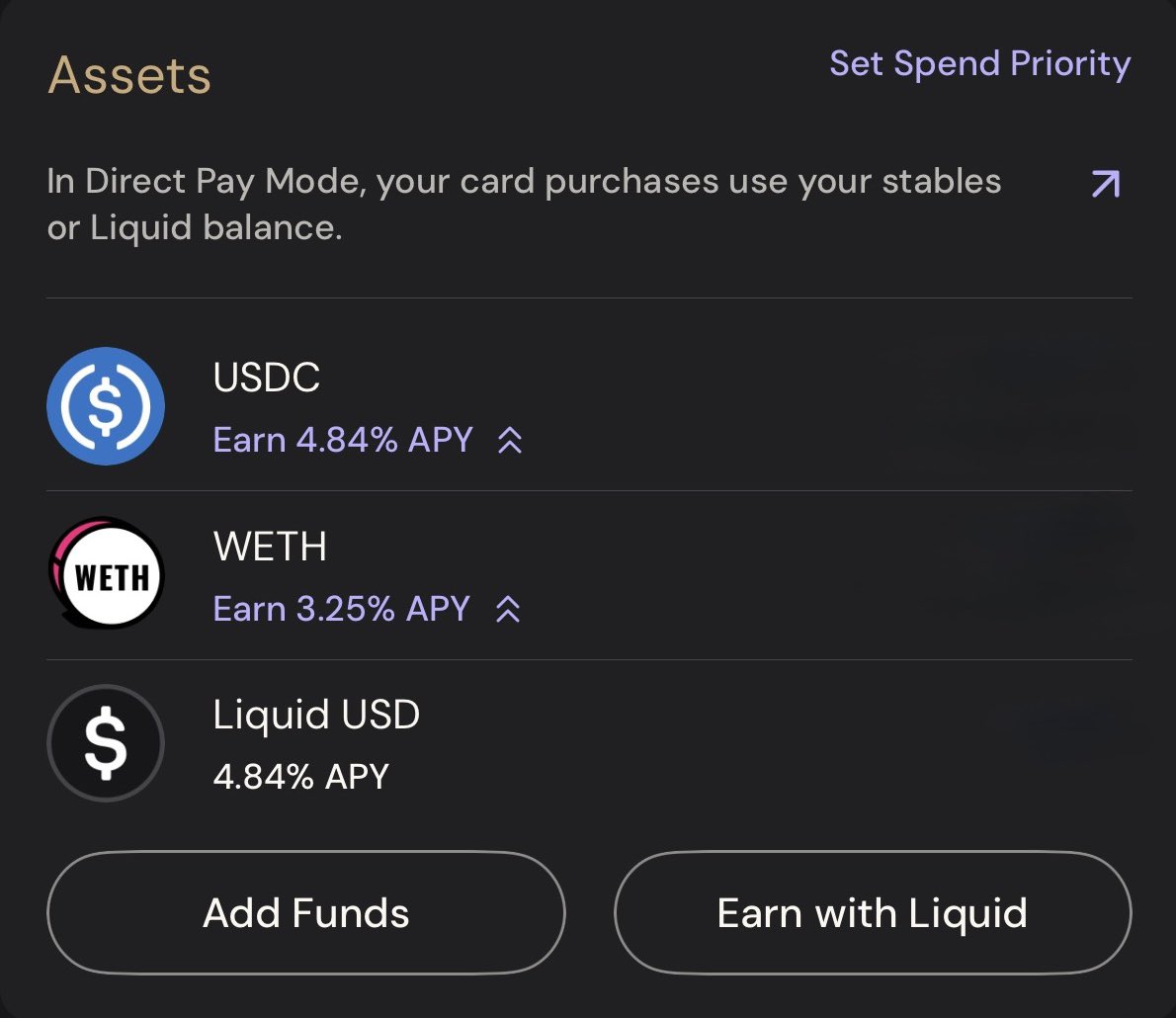

🟣 @ether_fi Cash:

→ 3% back on everything. Flat.

→ Nothing to lock. Nothing to buy. $0 fee.

→ Same self-custody your vault, your keys.

→ Cashback paid in wETH

Two self-custody cards.

One wants a five-figure entry ticket for the good rate.

The other just… gives you the rate.

Cashback shouldn’t cost $13K upfront. That’s it. That’s the take.

11

2

23

4,717

Jun 12

Full transparency, because someone will ask: yes, I lock tokens too. I staked $ETHFI.

But notice the difference and it’s the whole point of this post:

My 3% cashback doesn’t depend on it. Never did. The card pays 3% whether you hold zero ETHFI or a million. I locked it for separate reasons: ~10% APY on the stake, a share of protocol revenue, and a governance vote.

That’s the line between the two models.

One protocol says lock our token OR your card is worse. The other says here’s full cashback for everyone and locking is an optional yield product if you want it.

Few

574

Jun 11

1/ Your bank charges you fees and says "thank you for your loyalty."

Crypto cards in 2026 literally pay you to exist.

I ran the real numbers on etherfi, Bybit, Cryptocom and Nexo - not the marketing numbers.

The winner isn't who shouts loudest. Thread 🧵

9

7

68

11,467

Jun 11

11/ Who should pick what - no BS:

- You trade on Bybit daily Tier 2 ? Bybit (the 100% rebates on Netflix/Spotify/ChatGPT are genuinely great)

- You're a CRO believer? Crypto com

- You want the best flat cashback self-custody yield on everything?

@ether_fi

1

3

552

Jun 11

12/ My take after using it: etherfi is the only card where high flat cashback, self-custody and yield-bearing rewards exist in ONE product.

Everyone else gives you one of the three and charges VIP status for the rest.

If you're getting one → my ref link gets you bonus rewards:

ether.fi/@tryhardsorry

Questions about signup/KYC? Drop them below - I answer everyone.

RT tweet 1 if this saved you money.

1

5

540