218 Photos and videos

UZ retweeted

The median American adult is *not* richer than the median adult in Canada or many Western European countries.

Yes Americ"a" is richer, no Ameri"cans" are not richer.

UBS 2025 median wealth per adult:

Luxembourg: $395k

Belgium: $254k

Denmark: $216k

Switzerland: $182k

U.K.: $176k

Canada: $152k

France: $146k

Norway: $143k

Netherlands: $132k

Spain: $126k

Italy: $124k

U.S.: $124k

26

8

99

28,527

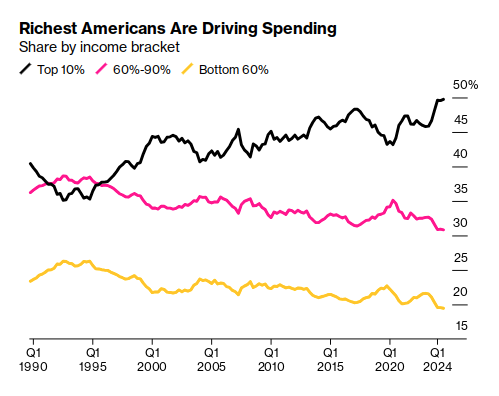

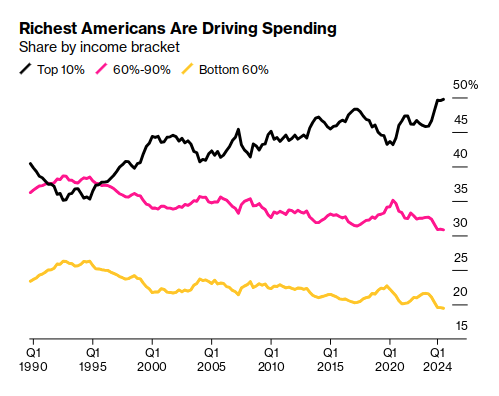

What's happened with the devaluation of the dollar is the frugality that was once a smart decision is now totally required just to live your life at all, and maybe you're hungry. We've all gotten poorer enough that if you didn't make it into the top 20% of earners, you feel it.

1

102

UZ retweeted

Jun 13

BREAKING: An Economics Professor Just Made A Pretty Stunning Argument About Elon Musk.

According to the professor, Musk spent roughly $250 million during the 2024 election cycle.

He claims that's just 0.025% of Musk's wealth.

In other words, the amount spent was so small relative to Musk's fortune that he could theoretically spend the same amount thousands of times over.

That's a democracy question, not just a money question.

480

3,297

9,643

524,359

UZ retweeted

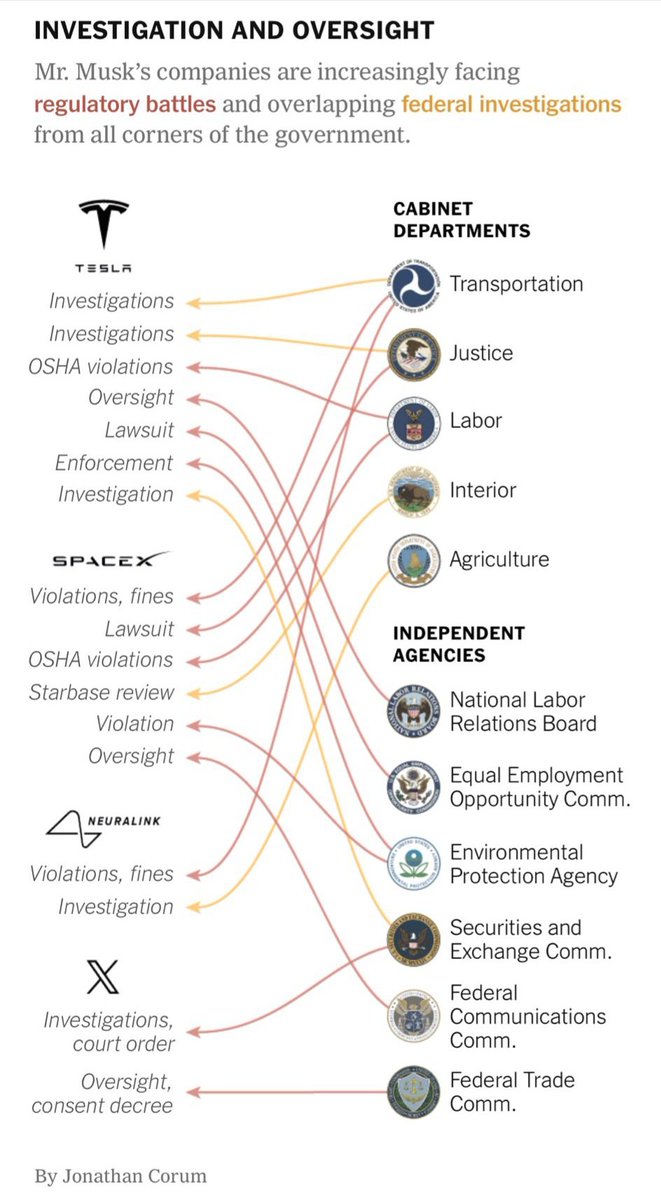

He was being investigated by 12 agencies for violations of laws and regulations. The 11 on this list, plus USAID, whose Office of Inspector General launched an audit on May 14, 2024, into USAID's oversight of Musk's Starlink terminals provided to Ukraine. share.google/eAvNmUXeeP6jgJr…

2

38

143

3,470

Serious question: If you were no longer financially able to own your own home, what would you want your landlord to be like? I own because I want financial security, where my living costs don't suddenly skyrocket entirely outside my control. Why can't I have that as a renter?

1

1

139

UZ retweeted

May 21

California's ADU reforms are successful in large part because they replaced 482 different sets of local rules with one consistent statewide standard.

We should do the same thing with building safety regulations, which should be rigorous, evidence-backed and statewide.

May 21

Why has modular construction failed in the United States?

"Sweden has used prefabrication to deliver mid- and high-rise housing at competitive cost and high quality for decades, and the explanation has nothing to do with engineering. Sweden has a standardized national building code and, more consequentially, a Public Housing authority that has committed to enough repeat volume to give factories a reason to invest, improve, and stay in business."

"In our experience, the building code is as much to blame as land use policy. The U.S. has delegated code development to more than 20,000 local jurisdictions, each with its own byzantine requirements, making it nearly impossible to develop a standard product that can be sold at scale across state lines."

8

38

314

13,714

UZ retweeted

May 21

Hello @JeffBezos, since you question the results of our studies on the unfairness of the US tax system, please allow me to remind you of the main conclusions of our work, the most comprehensive research to date on this issue.

May 20

Yes, the United States has the most progressive tax system in the world. The top 1% pay 40% of taxes, the bottom 50% pay 3% of taxes. We can make it even more progressive by zeroing out taxes on the bottom half. It’s a small amount of the total tax revenue but very meaningful to people in this group.

173

1,852

9,976

2,162,354

UZ retweeted

I have way more sympathy for normal voters than I do for the media figures knowingly lying to them.

24

67

1,000

32,249

UZ retweeted

May 8

One thing that’s becoming very clear in commercial real estate right now:

A lot of people want to explain what happened.

Very few want to admit what they participated in.

Everyone suddenly has a list of excuses:

- rates went up

- insurance exploded

- rents flattened

- the Fed changed everything

But the truth is, most of this behavior didn’t start in 2022.

The seeds were planted years earlier when people stopped caring about what an asset was actually worth.

Back around 2014–2016, while working at Marcus & Millichap, multifamily deals commonly traded at 8–10 caps. Deals actually penciled. There was room for error. Basis mattered.

Then I saw something that completely changed the tone of the market.

We had listed an overpriced and rough 1960s vintage deal that everyone knew was overpriced. Then a buyer came in around a 5.5 cap and justified it by saying:

“The banks are lending at 4%, so that spread makes the deal works.”

That was the first time I heard someone justify permanently overpaying for an asset because of a temporary interest rate environment.

And that mentality slowly became the entire industry.

At first the logic was:

“Lock in a low rate for a long term and the deal will work.”

Then in 2022, even that wasn’t enough anymore.

People started justifying to buy with *negative* leverage while assuming rents would continue growing 10% annually forever.

Underwriting went from aggressive to complete fantasy.

And here’s the uncomfortable part:

Most GPs weren’t creating some revolutionary business.

They weren’t inventing technology.

They weren’t building anything unique.

Their actual skill was raising money and telling a compelling story around a deal.

Which is fine, IF your number one responsibility is protecting investor capital.

But then another layer entered the picture: feeder funds.

When you raise money from friends, family, neighbors, or your community, there’s emotional accountability. You know exactly whose money is at risk.

Feeder funds created distance from responsibility.

Now people were:

- overpaying because rates were low

- accepting negative yield because “rents always go up”

- and doing it with money that no longer felt personally connected to real people

That combination destroyed discipline.

Fast forward to today:

Many of the same people who bought absurd deals with negative leverage and fantasy assumptions are now acting like nobody could have possibly seen this coming.

That’s nonsense.

The entire job of a GP is risk management.

You don’t get to call yourself a genius during the run-up and then blame “unexpected conditions” when the cycle turns.

And honestly, watching all of this unfold has likely twisted a lot of the love we all once had for this industry.

Somewhere along the way, too many people stopped respecting the basic math and replaced discipline with narratives.

But the only way this industry actually heals is if people stop rewriting history and start telling the truth about what happened.

15

8

157

20,056

UZ retweeted

liberalism is not tolerance - liberalism is the militarized intolerance of the cruelties of old world conservatism. do not forget that. your fingers yearn for the sword

79

181

1,845

182,320

Our algorithms are designed to destroy us. Destroy us spiritually, destroy us socially, destroy us intellectually. Capitalism under the tech elite has stopped serving humanity, it seeks rents it no longer earns. It should be illegal for someone else to control your algorithm.

1

2

129