You have money questions. We have money answers. Get started for just $1. Featured in @Forbes, @FastCompany, and @Axios.

Joined April 2020

- Tweets 1,609

- Following 409

- Followers 2,640

- Likes 1,530

390 Photos and videos

Pinned Tweet

9 Sep 2025

Bad financial advice has existed for ages. Origin’s AI Advisor changes that.

72

71

584

2,125,283

Jun 11

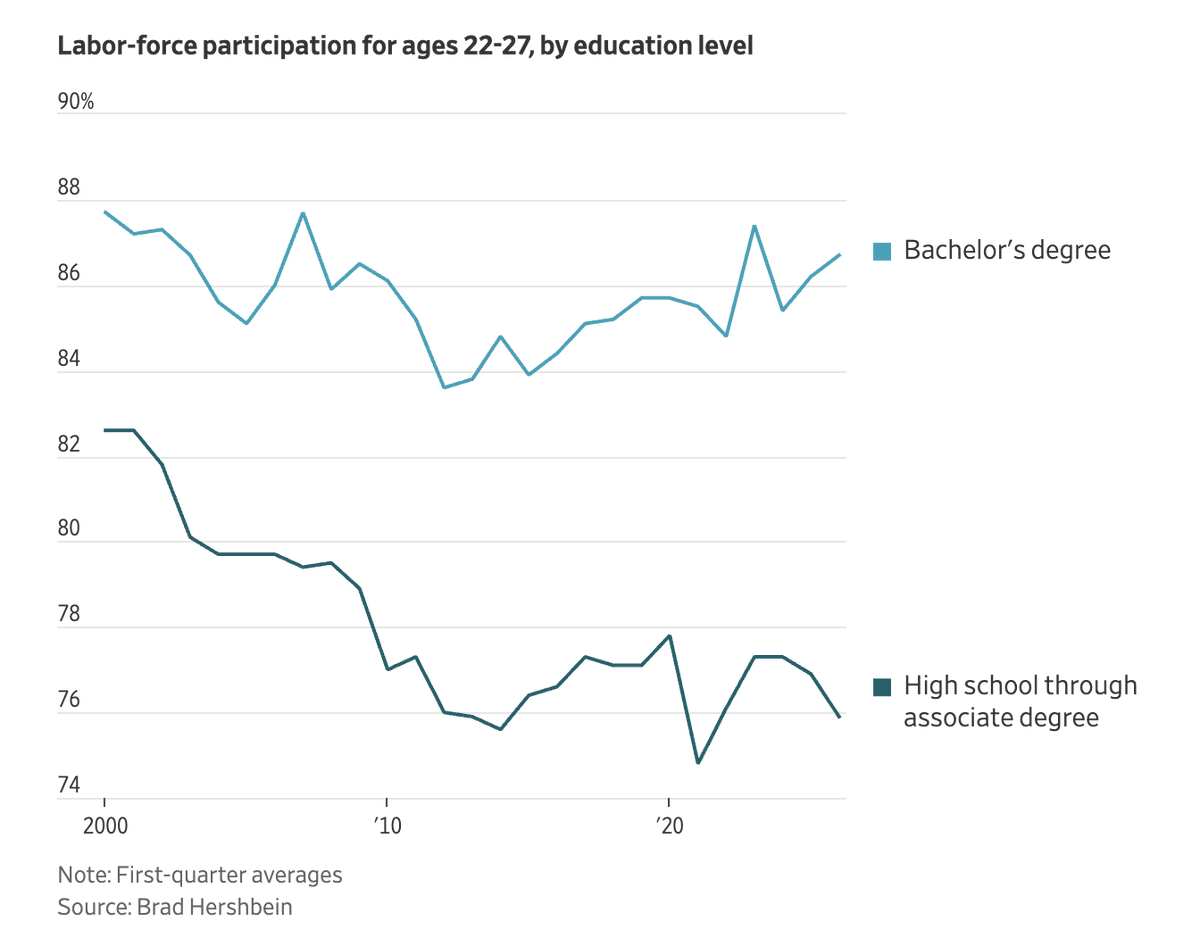

In true Gen Z fashion, the college class of 2026 is pessimistic about their job prospects — and that’s kind of fair, because they’re entering a genuinely rough job market.

Unemployment among 22-27-year-olds with bachelor's degrees hit 5.6% in March—up from 3.6% pre-pandemic.

But the unemployment rate is a pretty narrow lens, so let’s zoom in (and out).

Less-educated young people are faring worse. The overall unemployment rate for that age group is 7.2%, which sounds only slightly higher on the surface, but dig deeper, and you’ll see it’s because less-educated workers are dropping out of the labor force entirely.

For college grads ages 22-27, the employment-to-population ratio is sitting at 82.4% — basically flat with pre-pandemic levels. For high school through associate degree holders? 70.5%, down from 71.8%.

So new grads do have a structural edge. A bachelor's degree still buys you something. The problem is that "something" keeps getting smaller.

The wage premium for a college degree (what you earn versus someone without one) has compressed from about 63% in 2015 to 55% last year. Why? Because everyone has one now. As of March, 42% of U.S. employees hold a bachelor's degree or higher, up from 36% a decade ago.

This is the historical pattern economists have been watching for years. In the early 1900s, a high school diploma was rare and lucrative, but by the 1980s, it was table stakes. The college degree is sliding down that same curve.

1

4

119

Jun 5

"AMAZON.COM $147.32"

Sorry for the jump scare — that’s usually how Amazon transactions used to feel — not anymore.

Want to know what you actually bought on Amazon, not just how much you spent?

Now you can. Connect your Amazon account in the Origin app →

app.useorigin.com/?origin_di…

1

5

176

Jun 4

Americans aged 15–34 are now significantly less optimistic about the labor market than older adults, marking the largest generational confidence gap in the world.

Just 43% of younger Americans said it was a good time to find a job locally last year, compared to 64% of Americans aged 55 .

And the drop happened fast. Since 2023, younger Americans’ confidence in the labor market has fallen 27 percentage points — a decline comparable to what we saw during the financial crisis.

Check out the deeper dive below ⬇️

useorigin.com/resources/blog…

1

3

138

Jun 3

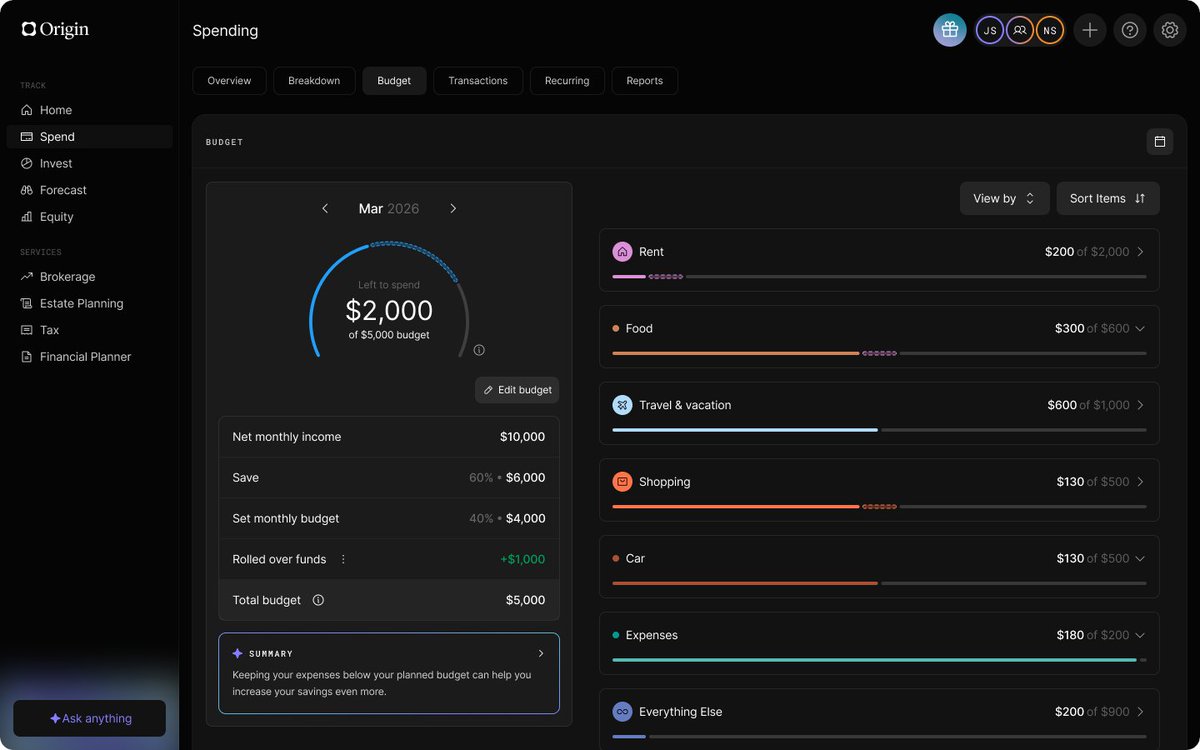

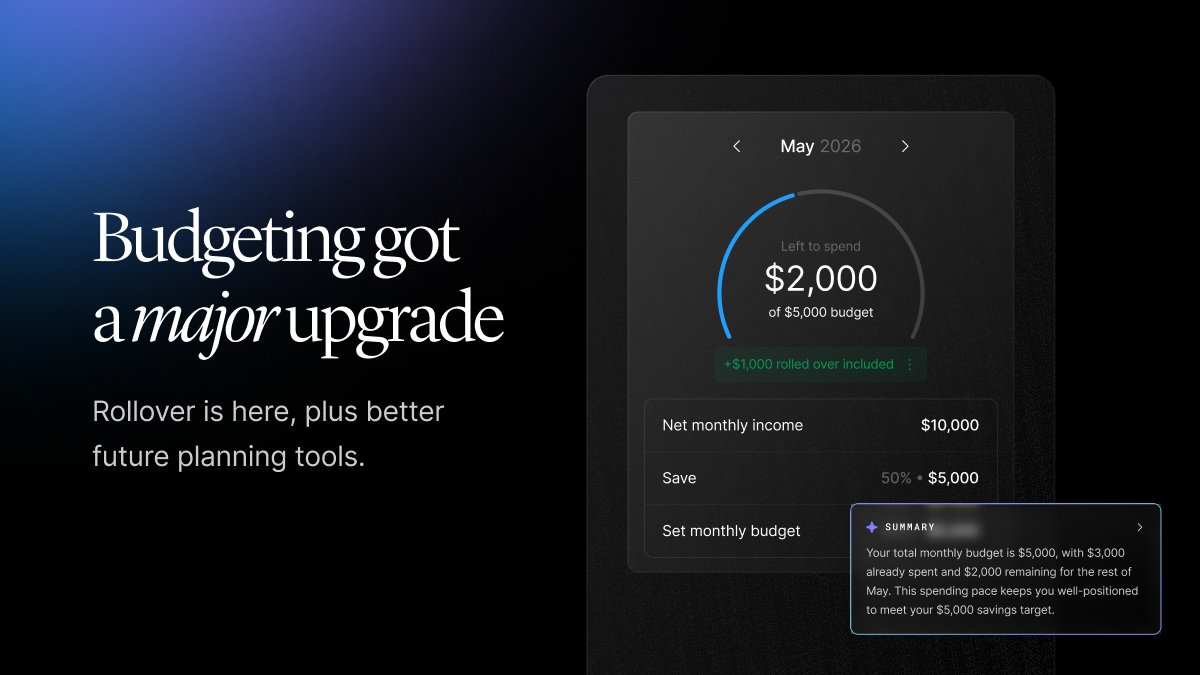

Origin's budget experience just got a major upgrade.

Unused budget now carries forward. Plan for expenses months in advance. Always know what you have left to spend.

Live now in Origin →

app.useorigin.com/spending/b…

1

2

267

Jun 2

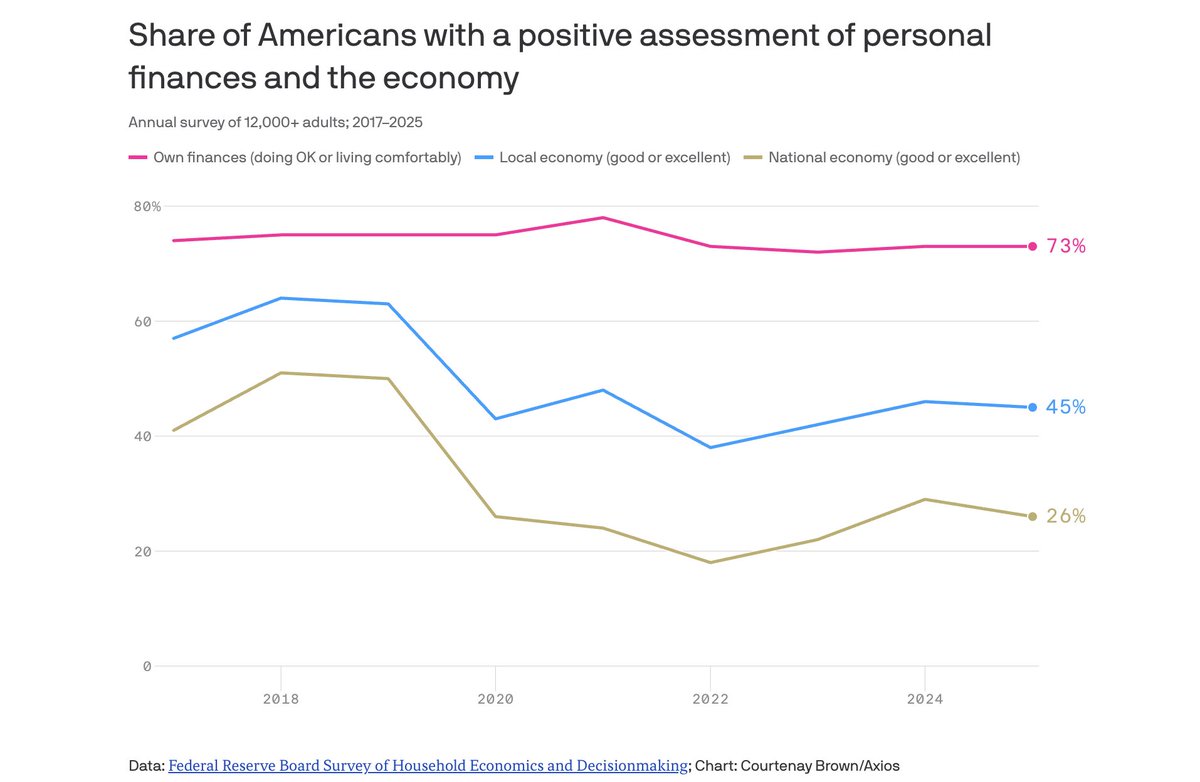

73% of Americans say their personal finances are doing okay, but also…75% think the economy is a disaster. Make it make sense.

The Federal Reserve recently released its most comprehensive annual look at how American households are actually doing — and the headline number is, genuinely, fine. 73% of adults say they're either doing okay or living comfortably financially — unchanged from 2024.

And yet: Only 1 in 4 Americans rates the national economy as "good" or "excellent." That's actually down 24 points from pre-pandemic levels. So people feel okay about their own money, but are convinced the broader economy is broken. That gap is wider than it's ever been, and it's been sitting there, largely unexplained, for a few years now.

1

2

125

May 28

Origin's budget experience just got a major upgrade.

Unused budget now carries forward. Plan for expenses months in advance. Always know what you have left to spend.

Live now in Origin →

app.useorigin.com/spending/b…

1

5

309

May 26

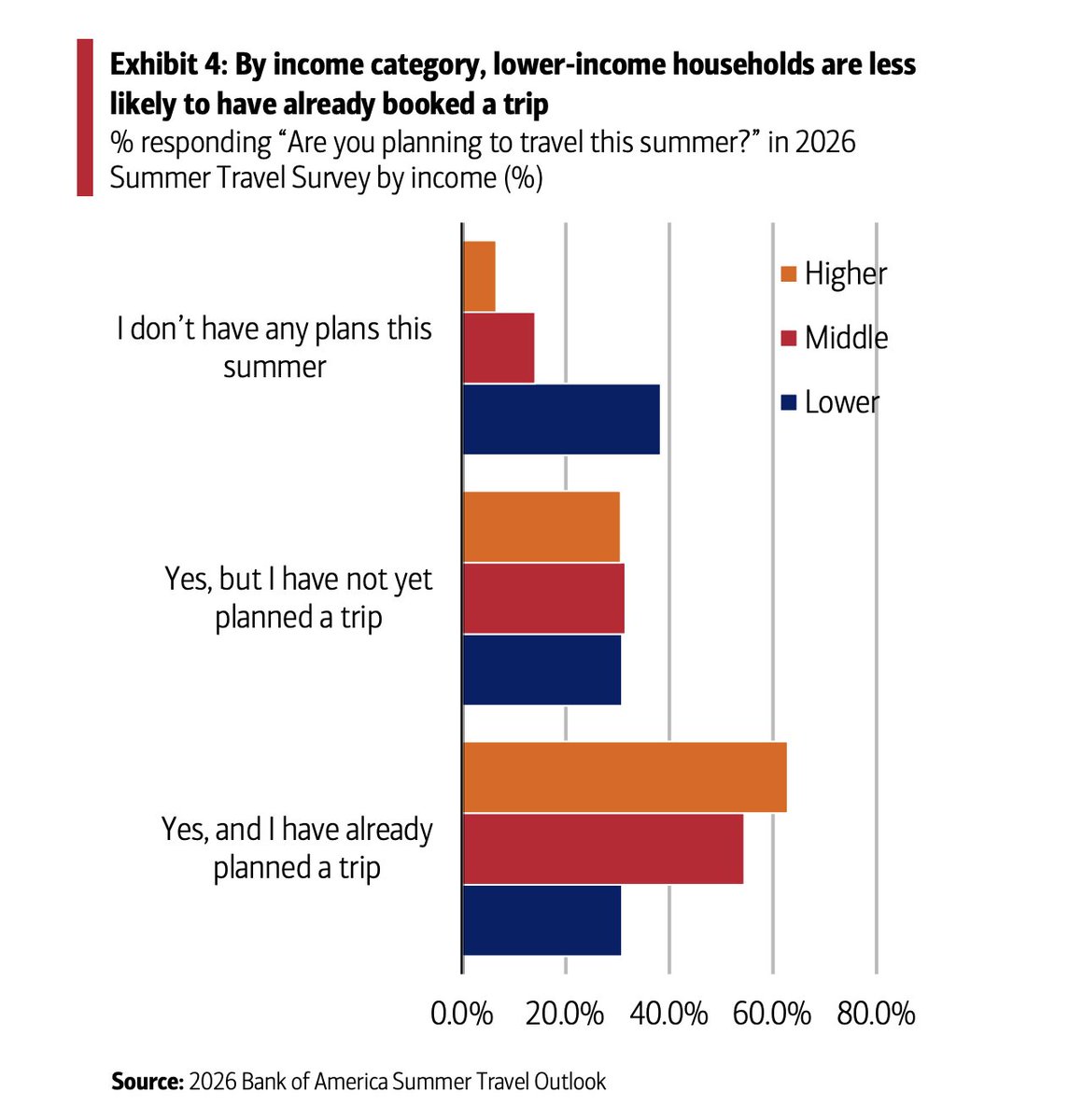

Americans are heading into peak travel season with record-high budgets and strong intent to actually use them.

The average leisure travel budget has climbed to about $6,556 this year, the highest on record, and nearly 80% of travelers already have at least one summer trip planned.

The K-shaped economy is visible here, too.

Higher earners are, unsurprisingly, taking more trips (5 per year), and lower-income households are much more likely not to have any trips planned (about 40% don’t), and data from Bank of America shows lower leisure spending amongst this tax bracket compared to higher spending on travel amongst higher earners.

2

160

May 21

It's a buyer's market for homes right now — but the window may already be closing.

The first thing you’d think when you see a headline like this is likely something along the lines of: “Buyer’s market? Prices haven’t even gone down,” and…you’d be right — that’s kind of the point.

Statistically speaking, though, home sellers do outnumber buyers this year. In fact, they outnumbered them by the widest margin ever back in Q1: 600,000 more sellers than buyers.

But yes: It’s done little to nothing for the actual median average sale price of homes in America — it’s still roughly ~403,000. That’s because this isn’t a traditional buyer’s market driven by collapsing demand and forced selling.

It’s more of a frozen market. Millions of existing homeowners are still locked into ultra-low mortgage rates from the pandemic era and simply aren’t willing — or financially able — to sell at materially lower prices unless they absolutely have to.

At the same time, elevated mortgage rates near ~6.5% continue to crush affordability for new buyers, even as inventory improves.

1

2

160

May 19

Just a few months ago, the AI trade was somewhat polarizing amongst retail investors.

Markets spent much of March and early April getting punched in the face by tariff fears, recession chatter, and growing skepticism around whether the AI boom had simply gotten too euphoric, too expensive, and too detached from reality.

Then…April 1st hit, and the market basically hit a giant red “lol never mind” button. Since the late-March lows, the S&P 500 has surged roughly 16%, while the Nasdaq has exploded about 26%, dragging markets back toward record highs.

And the money flowing into this thing is getting genuinely absurd. Semiconductor companies alone have added roughly $3.8 trillion in market capitalization over the past six weeks.

“Hyperscalers,” as some call them, are expected to spend something like $755 billion on AI capex this year alone.

So yes, it’s well worth asking as an investor: Is this… a bubble, or a real thing? Then again, FOMO is real.

As one retired investor interviewed by the Journal described the current environment: “the party is best about a half-hour before the police shut it down.”

1

4

173

May 18

Unfortunately, you're already late competency mogged here...

useorigin.com/resources/blog…

May 15

A preview for Pro users: a new personal finance experience in ChatGPT.

Pro users in the U.S. can securely connect financial accounts, see where their money is going, and ask questions based on the information they choose to connect.

Your full financial picture, now in ChatGPT.

1

3

8

756

Origin Financial retweeted

May 15

We launched this product six months ago at @useorigin and have learned a lot in answering over 1,000,000 personal finance questions from our users.

1. For specific, repetitive use cases customers want purpose built features. Chat is an amazing accompaniment that enhances our experience, but when a user has a defined task (eg tracking or managing money), richer, deep features are much more useful.

2. Finance Chat is poweful to the extent you know what and how to ask. Simple queries (how much did I spend where) are more easily discovered and engaged with in product UI. The value of chat is in the complex and idiosyncratic. Equipping users with the tools to become power users in this way is critical.

3. The user doesn’t know what they don’t know. The killer feature is taking all known financial questions a user should be asking, turning that schema into proactive monitoring and telling the user exactly what financial opportunities exist in real time and allowing agentic execution of that opportunity. This requires the right combination of determinism, grounding and LLM to execute well and is my personal product focus at the moment.

May 15

A preview for Pro users: a new personal finance experience in ChatGPT.

Pro users in the U.S. can securely connect financial accounts, see where their money is going, and ask questions based on the information they choose to connect.

Your full financial picture, now in ChatGPT.

7

2

35

8,506

May 14

The "K-Shaped economy" is alive and well.

For all the talk about a “resilient consumer,” it’s worth asking: Which consumer are we talking about here?

Because right now, the economy is splintering in different directions, and framing it like one cohesive narrative is misleading.

Higher-income households (roughly $125K ) are still spending at a solid clip, while everyone else is noticeably more constrained.

Since 2023, real spending from higher earners has climbed about 7.6%, compared to roughly 3% for middle-income households (~$40K–$125K) and just over 1% for lower-income groups (under ~$40K).

That’s how you end up with headlines that say “consumer spending is holding up,” even though that strength is coming from a relatively narrow slice of the population.

1

3

166

May 12

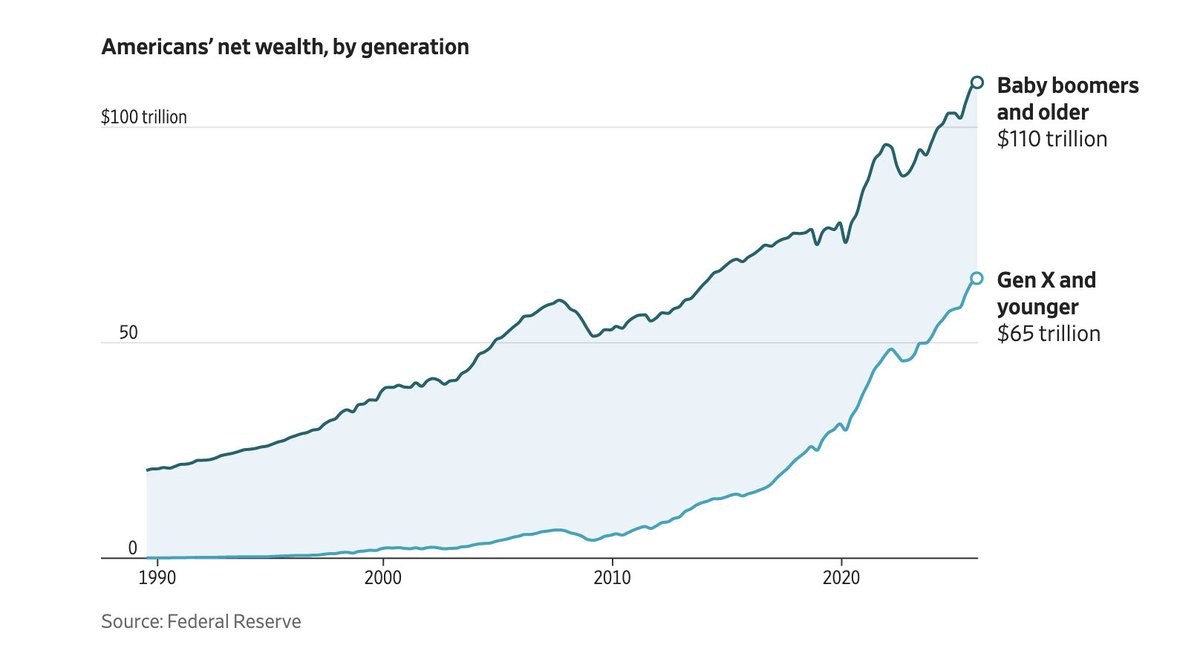

For years now, there’s been this idea floating around that we’re on the verge of a massive “great wealth transfer” — trillions of dollars flowing from baby boomers down to younger generations.

That part is true, but the timing isn’t precise at all. Older Americans (roughly 55 ) are currently sitting on about $110 trillion in wealth, more than any other group by a wide margin.

And yes, eventually, that money will get passed down. Death is not exactly optional yet (sorry, @bryan_johnson ).

But it’s not just going to get deployed all at once. People are living longer — especially wealthier people — and many of them are still actively accumulating assets.

Some are spending more on themselves (travel, retirement communities, longevity bets), others are passing money down gradually, helping with things like homes or tuition instead of waiting for a single lump-sum inheritance.

And when that transfer does happen, a lot of it doesn’t go straight to millennials or Gen Z — it goes sideways first. Spouses inherit from spouses, and then eventually it flows down a generation later, which is why the data looks a bit different than the narrative.

Right now, Gen X is actually positioned to receive the bulk of inheritances over the next decade, not younger generations.

And even that is happening later in life — the peak age for receiving an inheritance has shifted from the late 50s to the mid-60s. So instead of a sudden windfall, what you’re really looking at is more of a slow release.

2

185

May 8

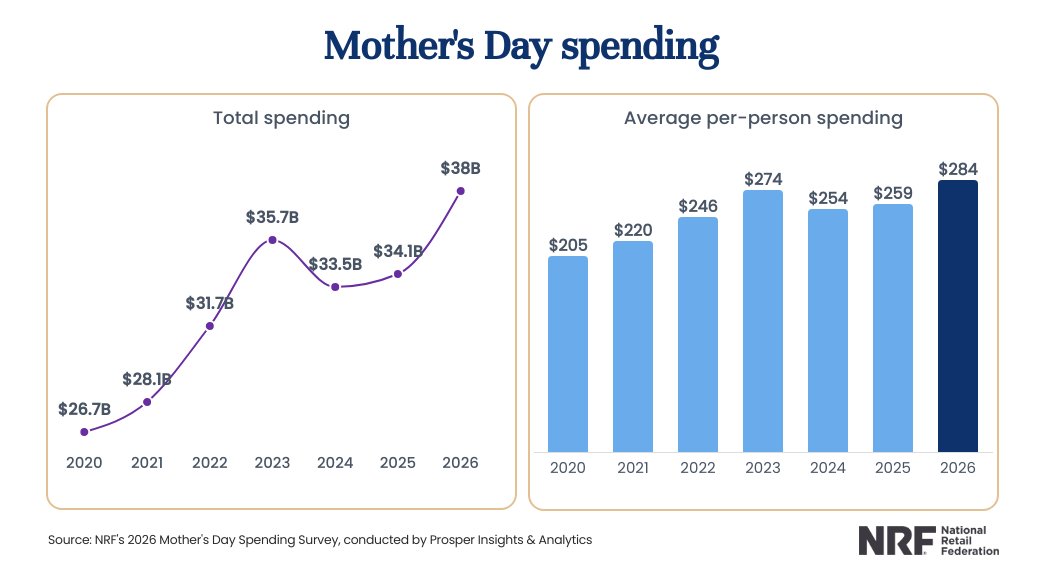

Mother’s Day spending is expected to hit a record $38 billion this year, blowing past last year’s $34.1 billion and setting a new high for the holiday.

On a per-person basis, that’s about $284, which is…also a record (shocker) as 84% of U.S. adults plan to celebrate.

1

2

166

May 4

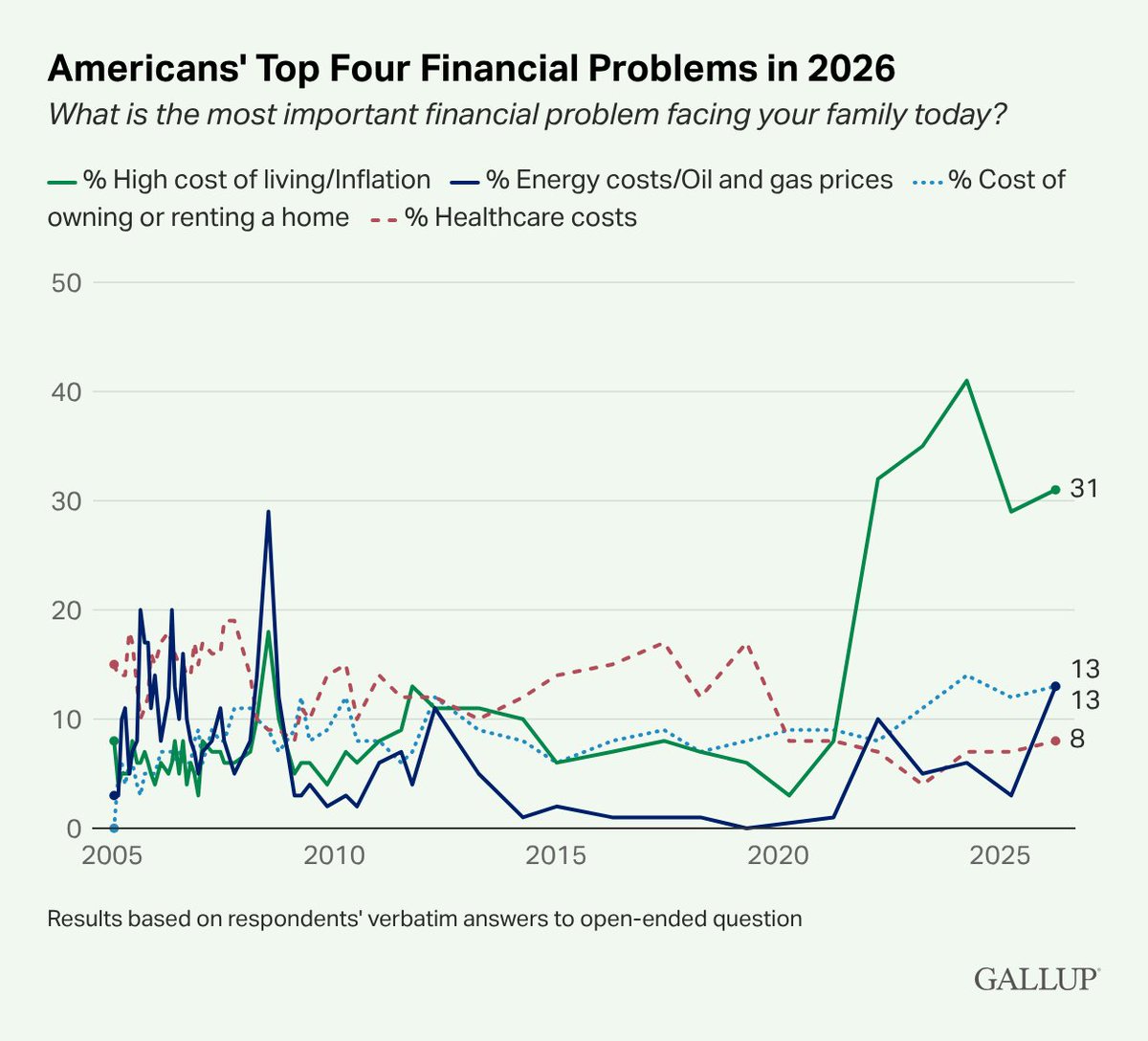

A new Gallup survey found that a record 55% of Americans say their financial situation is getting worse — one of the most negative readings we’ve ever seen, outside of the Great Recession.

This is now the…fifth straight year more people have said their finances are deteriorating rather than improving.

The reason isn’t especially complicated: it’s still affordability.

About 31% of Americans say inflation or high prices are the biggest financial problem facing their household, with energy and housing costs right behind it.

Healthcare, transportation, and basically anything that shows up on a monthly statement are all part of the same story.

2

192

Apr 30

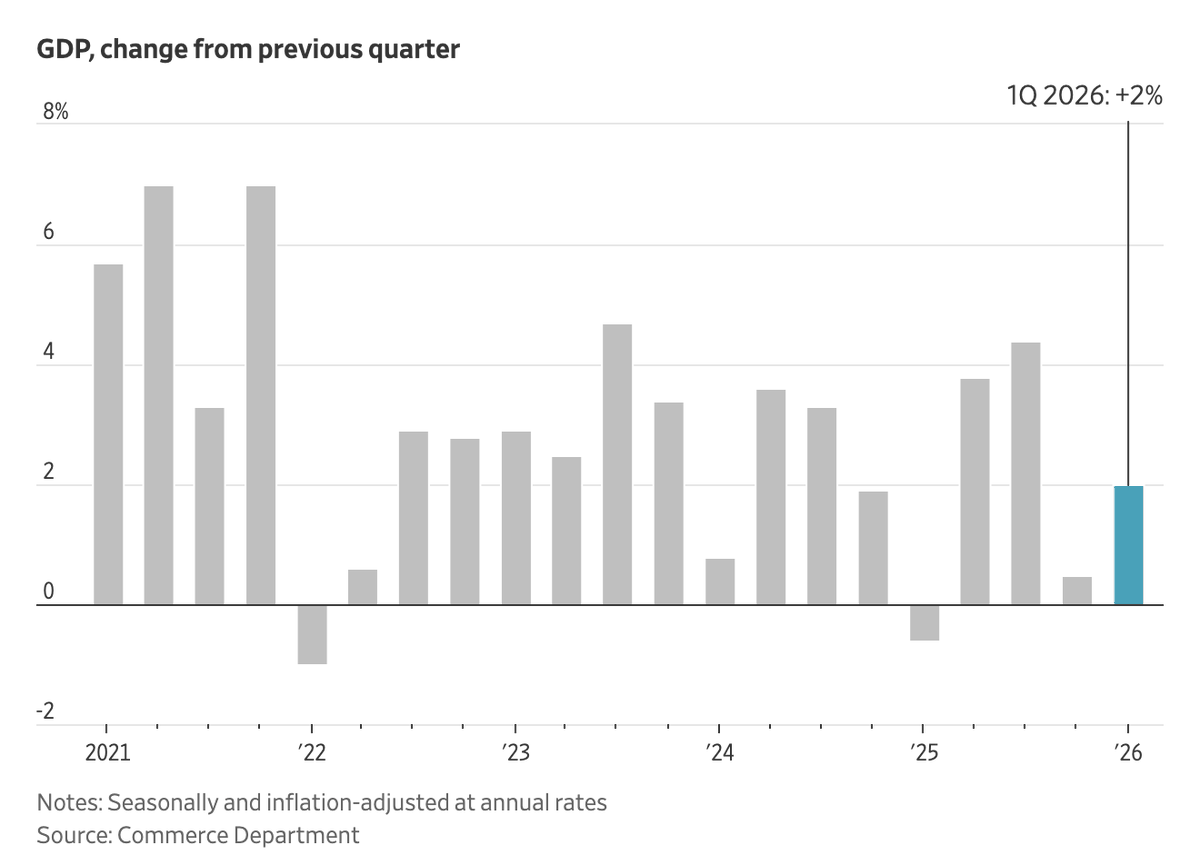

Economists' first projection for Q1 GDP growth just came in at 2% annualized — roughly in line with expectations.

This was a big rebound from Q4, and in contrast to a downward trend in projections leading up to the release.

But — on the flip side of that growth is another kind —because today, the U.S. national debt officially crossed over the 100% of GDP threshold.

We have roughly ~$31.265 trillion in publicly held debt, while last year’s GDP was about $31.216 trillion. This wasn’t unexpected by any means, and there’s no switch-flip from 99% to 100%, but crossing this line is both psychologically and economically disturbing.

We surpassed 100% briefly back in 2020, but the U.S. hasn’t officially ended a fiscal year above this milestone since 1946 — and there’s no sign of a reversal coming this time.

1

2

181

Apr 28

For several decades now, the job of bonds has simply been: When the market goes down, these should offset my losses a bit.

But over the past 5-6 years, bonds have grown more interlinked with the markets — what used to be an alternative has now become just another asset to sell.

So, what changed? In the old setup, bad news for the economy usually meant lower growth, lower rates, and a boost for bonds. Since 2020, though, the dominant risk hasn’t just been growth — it’s inflation.

When inflation is the problem, that relationship breaks. A shock that hurts stocks can also push yields higher, forcing bond prices down.

So instead of acting as a hedge, bonds start moving in the same direction as equities — especially during periods of stress. At the same time, bonds themselves have become a bit less “safe” than they used to be.

Governments are issuing more debt, central banks are stepping back from being consistent buyers, and investors are demanding higher yields to compensate.

3

162

Apr 23

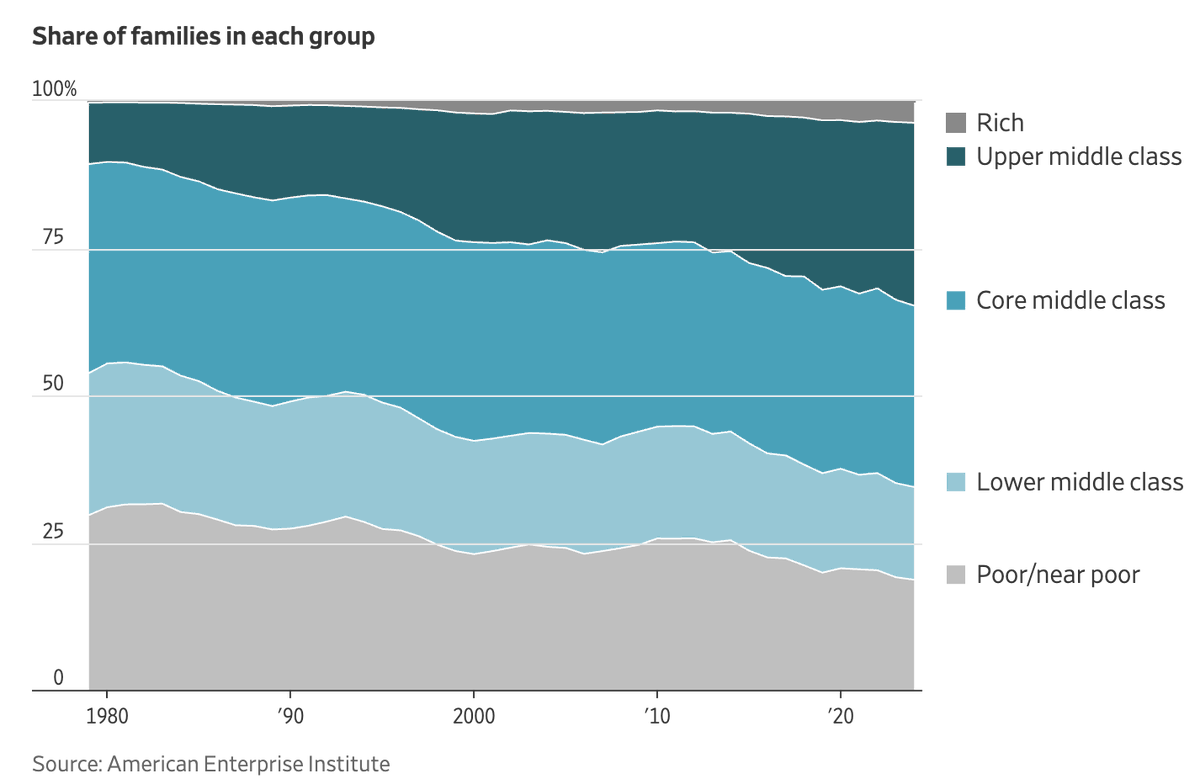

The middle class is shrinking — but is that bad, or good?

New research from AEI found that the share of Americans in the upper middle class has surged over time — from about 10% in 1979 to roughly 31% today. At the same time, the share of people considered poor or near-poor has actually declined, falling from around 30% to 19%.

But it’s not a singular narrative all the way through, because the gains haven’t been evenly distributed. Income has grown across the board, but it’s grown faster at the top — meaning the distance between groups is still widening.

So is this good, or bad? It really depends on how you define progress.

1

2

178

Apr 21

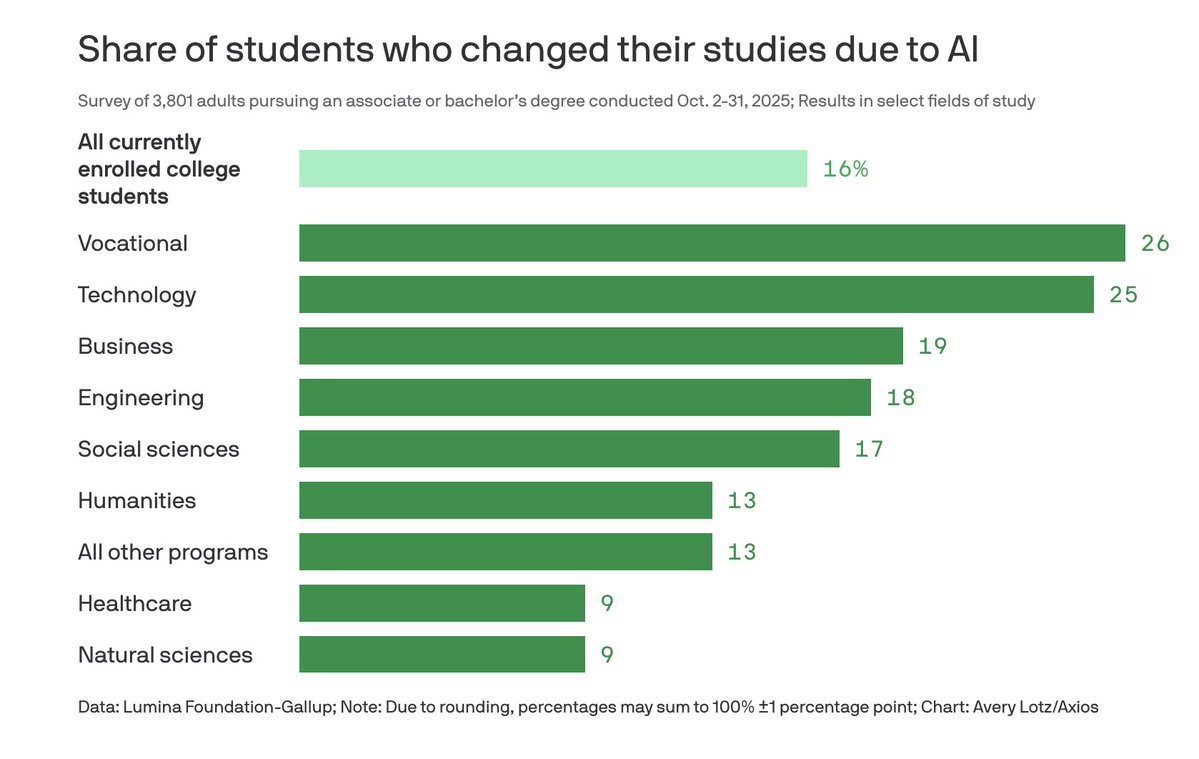

Nearly half of college students say they’ve spent a meaningful amount of time thinking about changing their major because of AI, and about 1 in 6 have already done it.

That’s a pretty aggressive response to something that, at least so far, hasn’t actually played out in the way people keep describing it.

If you look at what AI can do right now, it’s not replacing jobs in clean, obvious chunks. It’s just getting better at pieces of them. MIT’s latest work has models handling around 65% of text-based tasks at a “good enough” level, with that number likely to climb over time — but “good enough” still comes with a lot of caveats, and most of it still requires a person involved somewhere along the line.

So the reality is slower and more uneven than the narrative. Jobs aren’t disappearing overnight — they’re getting chipped at, reorganized, and in some cases, made more valuable depending on how the work changes.

Students don’t really have the luxury of waiting to see how that shakes out, though. If you’re in school right now, you’re making decisions based on what you think the market will look like in a few years, not what it looks like today.

And right now, the signal you’re getting is a mix of “learn this immediately” and “this entire category of work might not exist,” often in the same conversation.

2

4

319