Joined July 2023

- Tweets 18,387

- Following 61

- Followers 1,219

- Likes 101,311

3,251 Photos and videos

Pinned Tweet

Most investors skip the first question.

Not "is this stock cheap?"

Is this actually a good business?

Those aren't the same thing. And confusing them is where most mistakes start.

New article: the 5 economic traits that separate a genuinely good business from one that just looks that way.

1

1

1

114

Buffett spent years hunting bargains.

Graham taught him to buy cheap and move on.Then he met Munger

One conversation rewired his entire approach: stop looking for discounts.

Start looking for durability

That's not a strategy upgrade. That's a philosophy transplant.

1

19

Everyone celebrates the company growing 40% a year.

Nobody asks where the cash went.

Buffett did. In 1988, he bought Coca-Cola, not for the growth rate. For the cash that showed up every single quarter, without fail, for decades.

That's not boring. That's the blueprint.

38

Most investors skip the first question.

Not "is this stock cheap?"

Is this actually a good business?

Those aren't the same thing. And confusing them is where most mistakes start.

New article: the 5 economic traits that separate a genuinely good business from one that just looks that way.

1

1

1

114

Sir John Templeton called them the four most dangerous words in investing.

"This time it's different."

He'd seen railroads. Radio. The Nifty Fifty. The dot-com bubble. Every generation discovers new reasons the rules don't apply.

The rules always apply.

1

2

5

304

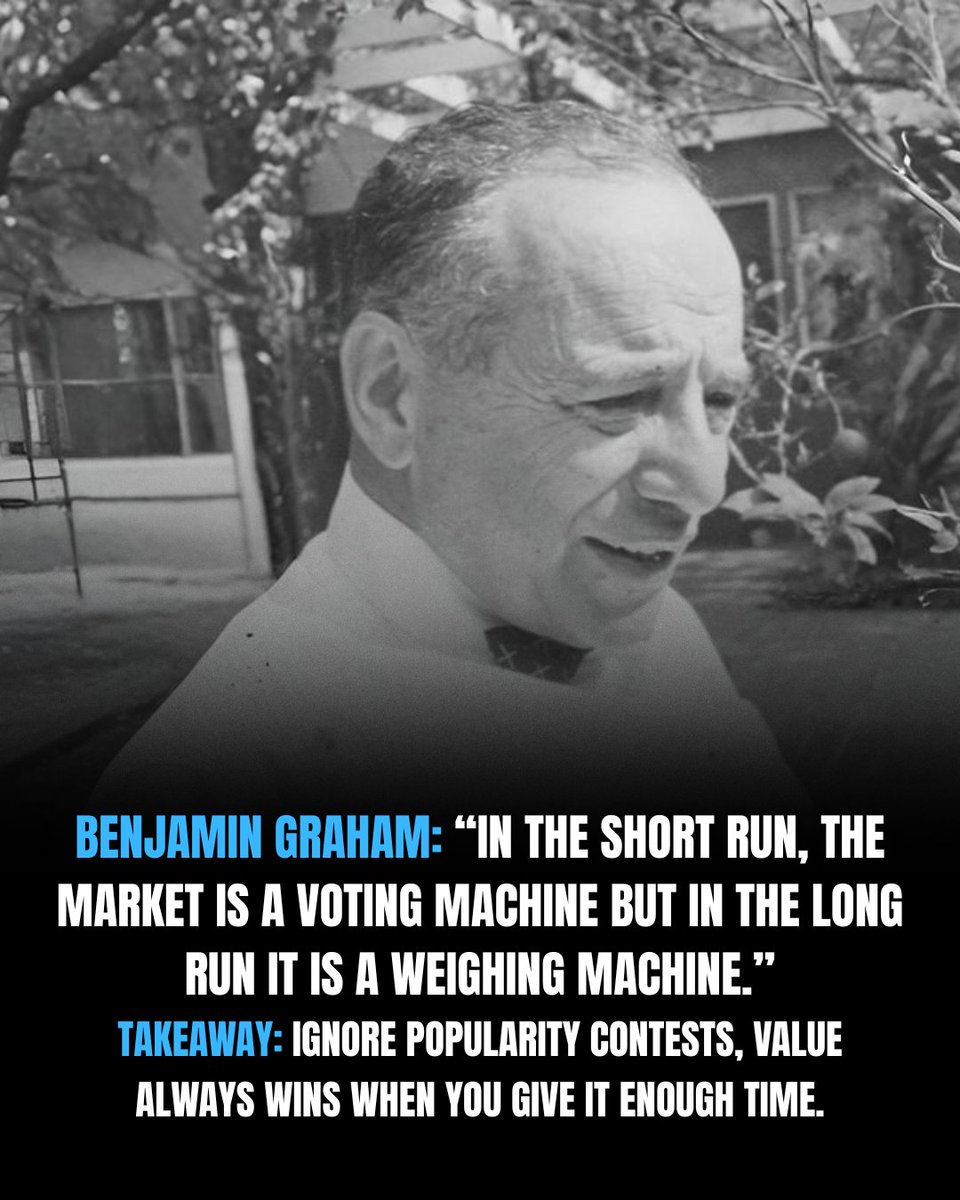

Graham watched investors panic-sell great businesses for decades.

His diagnosis: they forgot what they owned.

A ticker is a price. A business is earnings, customers, moats, and managers.

One fluctuates. The other compounds.

That's not a distinction. That's the whole game.

2

74

They raised $2B. Hired aggressively. Hit every growth target.

Shareholders lost money.

Munger saw this pattern in the 90s and called it what it was: legal wealth transfer, from investors to insiders.

Not fraud. Just incentives working exactly as designed.

2

81

The average investor in Lynch's Magellan fund lost money.

Lynch himself returned 29% annually.

Same fund. Opposite result.

They kept buying the highs and selling the lows, scared out every time it dropped.

Fear isn't a feeling. It's a tax.

2

119

Munger didn't have a sophisticated investment system.

He had three buckets: yes, no, and too hard to understand.

Wall Street sells complexity. He got rich selling himself simplicity.

3

116

In 2000, every analyst had a model showing internet stocks were worth it.

The models were technically correct.

The assumptions were fantasy.

A valuation is only as honest as the person building it.

66

"You make most of your money in a bear market. You just don't realize it at the time."

Shelby Davis said it. Buffett lived it. Munger never forgot it.

The panic isn't the risk. Staying on the sidelines is.

1

74

Lynch beat the market for 13 years straight.

He passed on dozens of hot tech names the whole time.

Not because he was cautious.

Because he couldn't draw what they did.

Complexity isn't a moat. It's a warning label.

1

61

Mr. Market shows up every morning with a new price.

Same business. New price. Every single day.

Graham figured out the trick early: the price is just a number someone's willing to transact at. The value is what the business earns, year after year, while you ignore the number.

One changes your net worth. One changes your mind.

78

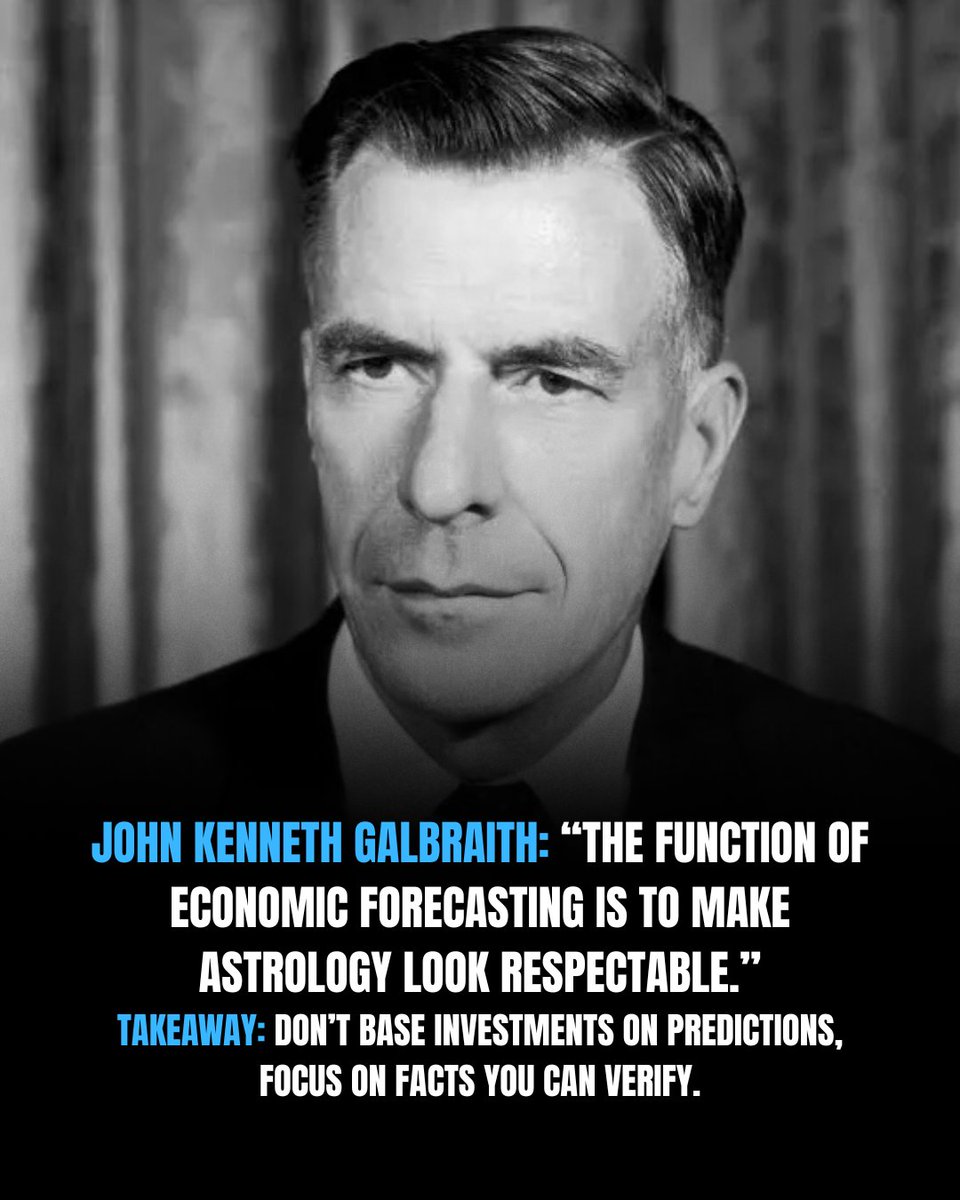

Galbraith said it plainly: economic forecasting exists to make astrology look respectable.

Buffett heard that and built an empire ignoring every macro prediction ever made.

The forecast was never the edge. The facts were.

69

Klarman doesn't care what the business is worth.

He cares what the business is worth relative to what he's paying.

That gap, between price and value, is where all the money lives.

2

77

In 1973, Washington Post shares fell 50% in a year.

Buffett called it one of the greatest investments he'd ever make.

The market was pricing fear. He was pricing the business.

Same asset. Two completely different questions.

77

Everyone remembers Buffett being greedy when others were fearful.

Nobody remembers when he waited 10 years to do it.

The quote is famous. The patience behind it isn't.

That's not contrarianism. That's discipline mistaken for boldness.

1

2

73

Buffett said it in five seconds flat: "It takes 20 years to build a reputation and five minutes to ruin it."

He's watched it happen. Salomon Brothers. Enron. Lehman.

The market prices speed. History prices character.

2

81

See's Candies needed almost no capital to grow. Every dollar Berkshire put in came back as two.

That's the standard Buffett actually uses, not "is it profitable?" but "does it earn above what capital costs?"

Most businesses fail that test. Most investors never think to ask.

2

58

Benjamin Graham watched the same stock soar and then collapse without a single thing changing about the business.

That's when he stopped asking "what does the market think?"

And started asking "what is this worth?"

Popularity fades. Math doesn't.

76