I am the founder and CIO of Verdad Advisers and author of The Humble Investor. Views are my own. Join our email list: eepurl.com/dibK3L

Joined January 2018

- Tweets 3,910

- Following 1,096

- Followers 47,415

- Likes 11,781

454 Photos and videos

Pinned Tweet

9 Dec 2024

Very excited to announce that my new book The Humble Investor is available for pre-order! See below for links to bookstores...

28

19

193

82,406

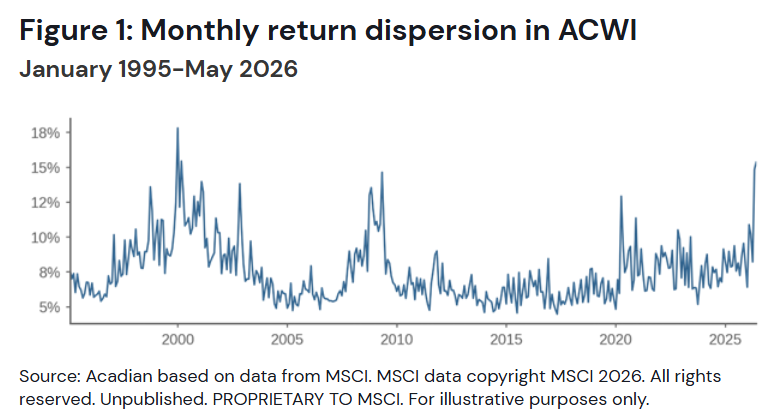

DISPERSION IS HERE

“Now this is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning.”

-- you know who

During the eighth step of the bubble, the flow of new investors starts shrinking while existing investors approach their risk and leverage limits. Volatility and dispersion grow, and gains become less uniform across stocks.

Now, dispersion is here.

Owen Lamont posted this graph today, which illustrates well how cross-sectional dispersion of monthly returns peaks at tops and bottoms.

My interpretation of the graph is not that high dispersion is always a sell signal, or a buy signal for that matter. To me, it's a signal that what has worked very well so far will stop working relatively soon. High beta was great during the late nineties, being short levered small caps was great going into the global financial crisis, and having just cash was great when Covid lockdowns hit. When the dispersion peaked each of those times, what worked on the way in stopped working soon, and what didn't work on the way in started working very well.

The obvious caveat is that we don't know that the dispersion has peaked yet. If this is a bubble, then we are close to the end of the beginning of it, but it's not yet clear whether the correct analogy is April 2000 or December 1999, the two alternative analogies having very different short-term return implications. To build on the analogy of the quote, the battle of El Alamein has started, but it hasn't been won (lost, if you're a Platner supporter) yet.

x.com/ptuomov/status/2054753…

THE LIFE CYCLE OF A BUBBLE

1. A genuine advancement creates real productivity gains. A real technological or economic improvement increases productivity and leads to genuine revenue and earnings growth.

2. Stock prices leak into reported profitability. Rising stock prices improve reported earnings, financing conditions, collateral values, and perceived business performance.

3. Reported profitability drives real investment. Companies increase hiring, capital spending, construction, expansion, and speculative investment because of their own or their customers’ reported profitability.

4. Bubble beliefs and abandonment of present-value discipline. Investors stop focusing on discounted cash flows and begin relying on continuing gains from the greater fool theory, believing they can sell later at a higher price.

5. Inflows from sideline investors. Previously cautious investors enter the market in large numbers. New money from existing and new investors participation drive prices higher.

6. Extreme overvaluation. Prices rise far above historical normal multiples of reported fundamentals, even ignoring the fact that reported fundamentals have been driven by rising stock prices.

7. Issuance. Companies take advantage of high valuations through IPOs, secondary offerings, stock-based acquisitions, SPACs, and insider selling.

8. Exhaustion of inflows. The flow of new investors starts shrinking while existing investors approach their risk and leverage limits. Volatility and dispersion grow and gains become less uniform across stocks.

9. Earnings disappointments from slowing price appreciation. As stock prices stop rising rapidly, the earlier boost from higher valuations into earnings weakens or reverses. Companies begin missing expectations.

10. Stock-price collapse with high volatility. Confidence in both the fundamental growth and in the greater fool theory break down and prices fall sharply. Volatility rises further as leverage unwinds.

11. Bear-market rallies and progressively greater exhaustion. Bargain hunters and frustrated latecomers repeatedly buy the dips, creating violent temporary rallies that fail. Markets make lower highs and lower lows.

12. Capitulation, abandonment, and normalization. Bubble participants eventually give up in disgust or exhaustion. Volatility falls, valuations normalize, and the market returns to more ordinary behavior.

11

22

166

72,783

Dan Rasmussen retweeted

Software buyouts down 43% YoY. PE can't price these names.

Don't worry, private credit still has the debt marked at cost.

2

9

69

9,840

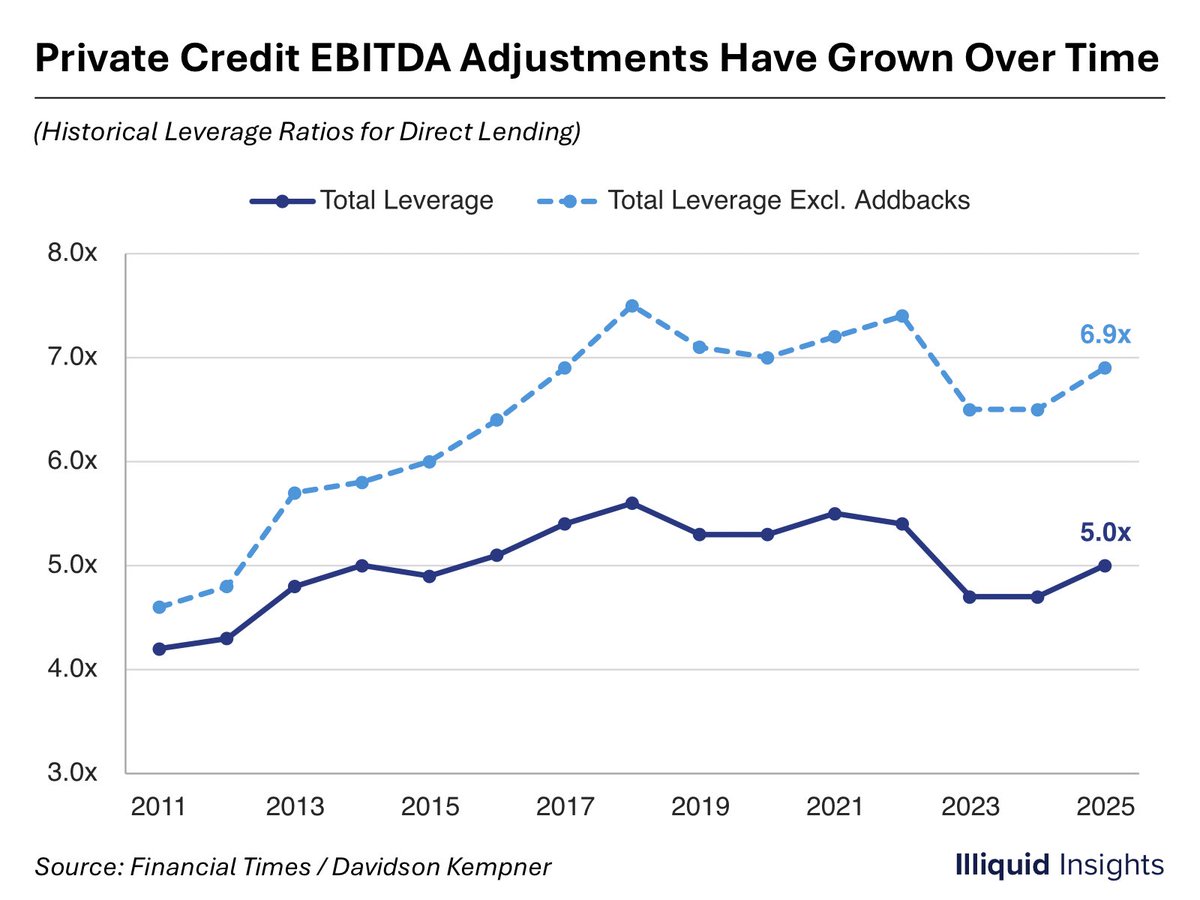

Dan Rasmussen retweeted

EBITDA is inflated. 6.0x leverage today is very different than a decade ago.

3

7

46

5,987

Dan Rasmussen retweeted

Jun 5

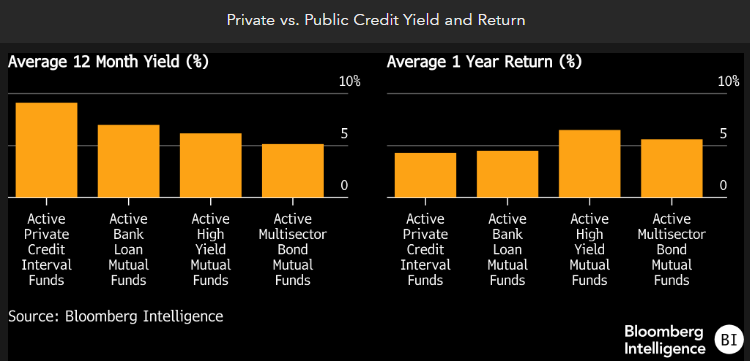

Is private credit worth it? What do you really get that's so great it's worth a 4% expense ratio? Yes, there's a 9% yield but the total return is more like 4%, meh, trails multi-sector bond funds, bank loans, junk bonds (which you can get for near free nowadays). Good note today from @DavidCohne questioning this whole asset class (or at least the interval funds that offer it)

23

16

92

78,955

Jun 4

Congratulations to Verdad's own @GregObenshain for being named a hedge fund rising star by Institutional Investor!

institutionalinvestor.com/ar…

6

2,163

Dan Rasmussen retweeted

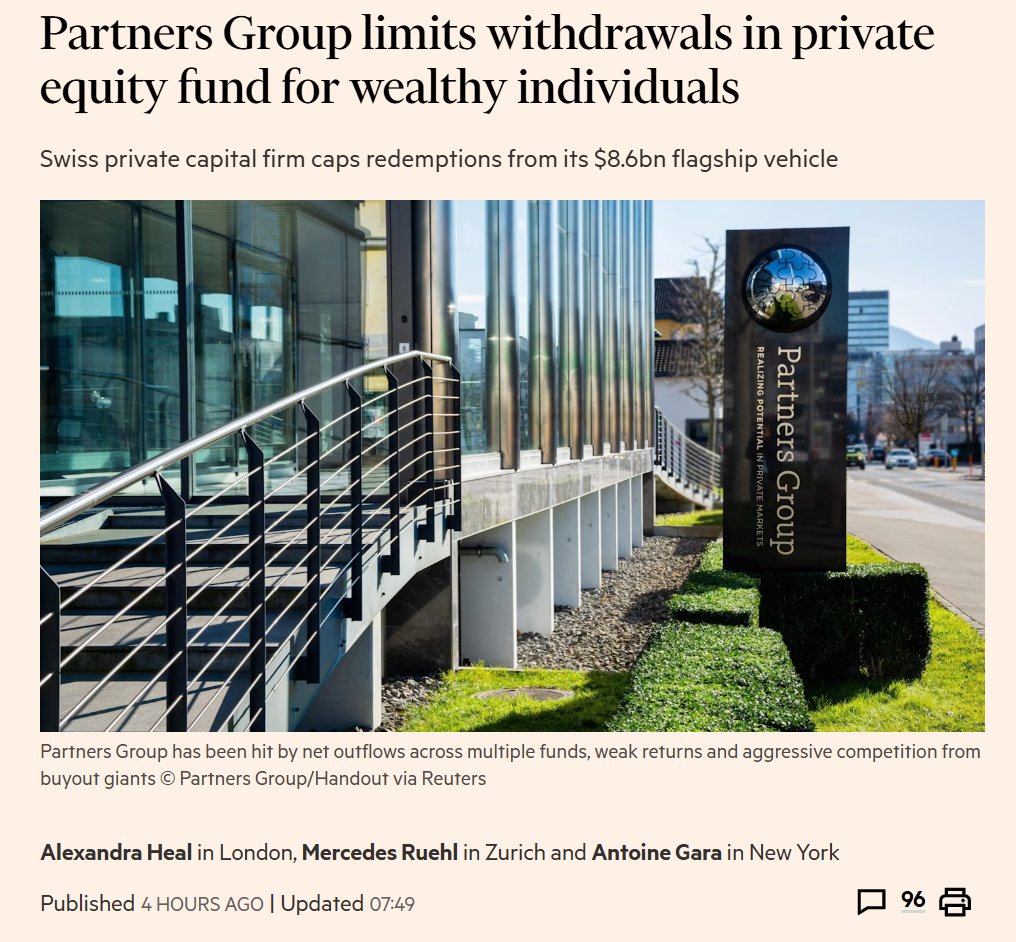

For months the question was why retail would flee private credit but stay in private equity

Partners Group answered it - they're fleeing both now

First PE retail fund to gate

6

29

128

19,282

BUBBLES AND DIVERSIFYING ASSETS

As a large bubble inflates and creates the unbearable FOMO vacuum that sucks almost everyone in, the bubble causes people to sour on otherwise sensible, reasonably high expected-return diversifying investments. One of the signs of the bubble is the expected long-term real returns actually increasing on assets that aren't participating in the bubble.

For example, during the 1999 TMT bubble, U.S. REITs, EM equities, EM debt, U.S. TIPS, Barclays developed gov't debt, and international small-cap equities were all shunned and had their expected returns grow to reasonable levels. You could lend money to Bill and George W. at 4% real because the market loved equities and there was no love left over for anything else! The price of these diversifying investments didn't go up or down much during the 1999 TMT bubble, even though fundamental values did steadily grow, which over time increased the long-term expected returns on these diversifying investments.

Investing in those kinds of bubble non-participants doesn't really protect your mark-to-market relative P’n’L during the bubble. Only being long the bubble can protect your relative P’n’L from the bubble!

However, investing in those diversifying investments does position you well for the bubble burst and deflation, as those investments work well during the deflation stage. Such diversifying investments during the bubble may make sense if you aren't confident about being better at timing the bubble than the next guy.

Of course, those who believe they have the divine touch of market timing will plan to be long the bubble until they can see the eyeballs of the enemy and then rotate to these diversifying investments at the last moment. Godspeed to those of you, whom I know are numerous!

Relating this to my framework about the stages of bubbles:

Steps 5-8:

- Diversifying investments become less correlated with the bubble.

- Diversifying investments start producing disappointing returns.

- Diversifying investments begin to have muted price reactions to legitimately good fundamental news.

Step 9 and after:

- Diversifying investments continue to produce acceptable absolute returns and start producing very good alpha.

- Diversifying investments’ past fundamental news will be reinterpreted more positively as new fundamental news arrives.

THE LIFE CYCLE OF A BUBBLE

1. A genuine advancement creates real productivity gains. A real technological or economic improvement increases productivity and leads to genuine revenue and earnings growth.

2. Stock prices leak into reported profitability. Rising stock prices improve reported earnings, financing conditions, collateral values, and perceived business performance.

3. Reported profitability drives real investment. Companies increase hiring, capital spending, construction, expansion, and speculative investment because of their own or their customers’ reported profitability.

4. Bubble beliefs and abandonment of present-value discipline. Investors stop focusing on discounted cash flows and begin relying on continuing gains from the greater fool theory, believing they can sell later at a higher price.

5. Inflows from sideline investors. Previously cautious investors enter the market in large numbers. New money from existing and new investors participation drive prices higher.

6. Extreme overvaluation. Prices rise far above historical normal multiples of reported fundamentals, even ignoring the fact that reported fundamentals have been driven by rising stock prices.

7. Issuance. Companies take advantage of high valuations through IPOs, secondary offerings, stock-based acquisitions, SPACs, and insider selling.

8. Exhaustion of inflows. The flow of new investors starts shrinking while existing investors approach their risk and leverage limits. Volatility and dispersion grow and gains become less uniform across stocks.

9. Earnings disappointments from slowing price appreciation. As stock prices stop rising rapidly, the earlier boost from higher valuations into earnings weakens or reverses. Companies begin missing expectations.

10. Stock-price collapse with high volatility. Confidence in both the fundamental growth and in the greater fool theory break down and prices fall sharply. Volatility rises further as leverage unwinds.

11. Bear-market rallies and progressively greater exhaustion. Bargain hunters and frustrated latecomers repeatedly buy the dips, creating violent temporary rallies that fail. Markets make lower highs and lower lows.

12. Capitulation, abandonment, and normalization. Bubble participants eventually give up in disgust or exhaustion. Volatility falls, valuations normalize, and the market returns to more ordinary behavior.

10

13

156

59,846

"For investors, the implication is clear: Be an aggressive user of AI but a selective investor in it." Great stuff from @verdadcap

1

2

44

7,014

Dan Rasmussen retweeted

May 29

Harvard endowment:

2017: 16% allocation to private markets

2025: 41% allocation to private markets, $1.7B in cash against $7.9B in unfunded commitments, and no distributions in sight

And the real pickle: to raise cash, they can either

- sell LP stakes in the secondary market (at a discount, which will drag returns down)

- sell some liquid positions (which will increase private markets exposure due to the denominator effect) ..

.. neither of which is a great option

22

36

332

129,320

Dan Rasmussen retweeted

92% of LBO targets miss EBITDA projections in year one, per S&P.

EBITDA addbacks have become massively inflated.

4

5

82

17,199

Dan Rasmussen retweeted

May 27

"If Credit is problematic, that means the Equity is really problematic" needs to be said louder for the people in the back.

May 27

Apollo’s Marc Rowan Believes Software PE Returns Will Be "Disastrous"

"The price they paid reflected a future that did not have AI in it and now there's AI in it."

19

57

1,012

149,028

Dan Rasmussen retweeted

May 27

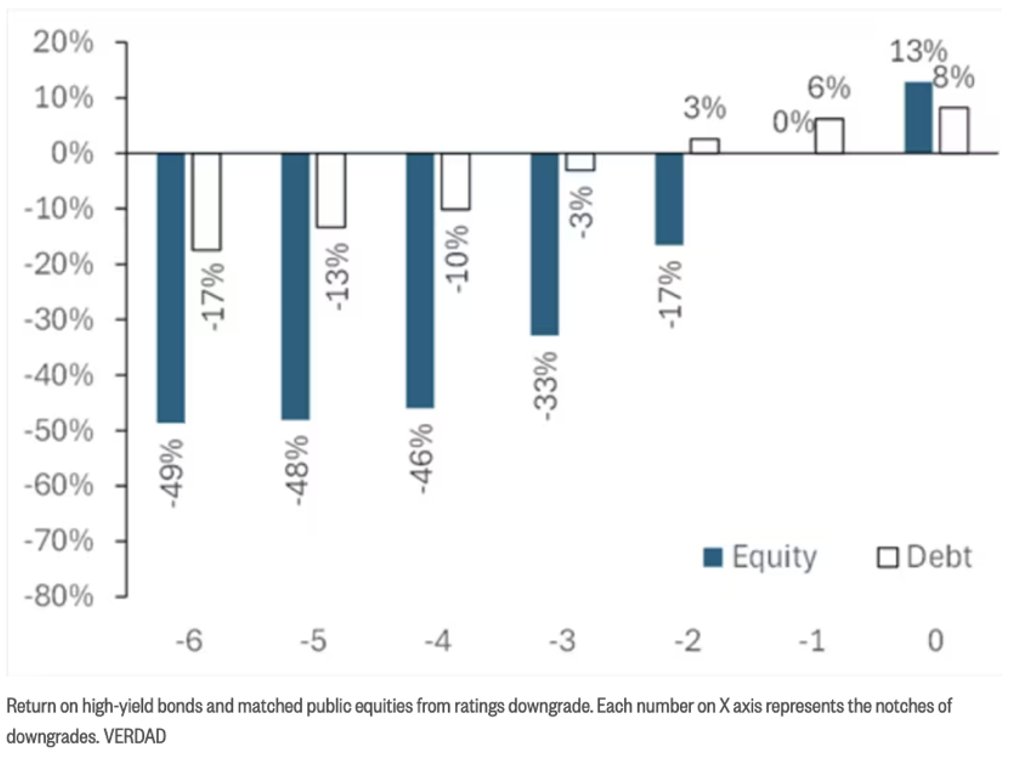

Too often in today’s fixation on private credit’s weaknesses, the bigger-picture risk is neglected. To our mind, private credit is more a canary in the coal mine than a systemic threat in and upon itself. The below chart reflects one key reason why. @verdadcap looked at the return of high-yield bonds to the matched public equities for every notch deterioration in credit over the last 20 years. The equity returns were always worse than the debt returns at each downgrade level.

Unsurprisingly given their symbiosis, private equity possesses much the same vulnerabilities as private credit—pandemic-era malinvestment, overly concentrated exposure, and widespread “kick-the-can” tactics that have delayed a full reckoning with this downcycle, likely storing up pain. US private equity AUM is more than double US private credit AUM. Today, private-equity-backed companies account for roughly 8% of US employment. Market participants are neglecting that private credit’s challenges are likely evidence of more significant challenges brewing in private equity.

What we fear is that turbulence in private credit YTD is a warning shot for tighter financial conditions to come. This is particularly concerning at a time when the US debt burden is ballooning and the war in Iran threatens stagflation amidst persistently higher energy prices. As of writing this, Goldman Sach expected Brent crude at an average of $90 per barrel in the fourth quarter of the year while JP Morgan expected that number to remain above $100 through the end of the year. It is also concerning given increasing signs of US consumer fragility, from record-high credit card debt and rising auto and student loan delinquencies to a savings rate hovering near a record low. And it is concerning given elevated valuations across asset classes. In this era of unprecedented financialization, main street and Wall Street have never been more intertwined.

Learn more about Sage Road's new report on "The Private Credit Reckoning": sageroadresearch.com/product…. Interested in subscribing? Message me.

4

4

10

3,391

Dan Rasmussen retweeted

May 26

In GMO’s latest Quarterly Letter, Ben Inker and John Pease reassess the risks and assumptions underpinning private equity portfolios.

Read Part 1: gmo.com/americas/research-li…

Read Part 2: gmo.com/americas/research-li…

#PrivateEquity #PE

1

4

14

15,487

Dan Rasmussen retweeted

May 23

One does not need to be a bear on technology to identify that this moment in market history is likely to be characterized by over-investment, over-spending, excessive valuations.

Disappointment is inevitable as an uncertain future surprises a consensus narrative that is too specific and too confident relative to the pace of change.

~ @verdadcap

mailchi.mp/verdadcap/priced-…

1

11

3,904

May 21

1

4

2,916

Dan Rasmussen retweeted

May 21

Japan has the most >200 year old companies in the world (56% of 5,586 globally) but still gets assigned negative terminal value multiples

3

3

53

6,647

May 19

The best counter argument to my piece yesterday

May 19

Absolutely true — I was meeting with those same telco equipment guys regularly in 2000.

Also irrelevant to the point I was trying to make. Back then, supply could largely keep up with demand because there was massive underutilized wafer capacity coming out of the 1998 Asian crisis that could ramp quickly. The relatively quick supply response led to an overbuild, which caused the crash as the overbuild was largely debt funded which required an immediate ROI for the CLECs to service their debt.

There is no comparable slack in the system today. Leading edge wafers and power are both structurally constrained, and neither can be turned on in a matter of months. That’s the core difference imo. And obviously the largest buyers of compute will have no trouble servicing their debt anytime in their near future.

I might be wrong, we might be in a bubble, you might be right, time will tell. Good luck!

5

37

39,602

Dan Rasmussen retweeted

May 18

I like when two investors I admire disagree

on his latest article, @verdadcap calculates that ~75% of the current value of the global semis industry (13% of global market cap and ~17% of US market cap) is derived from CF projections that are > 10 years in the future

while @GavinSBaker on his recent appearance at Sohn Investment Conference 2026 said, “I am optimistic that we may avoid a bubble this time. Smoother for longer is what we all want... b/c we have fundamental shortages of watts and wafers”

both quote @mjmauboussin, so may he be the one cutting the Gordian knot?

5

6

77

12,983

Dan Rasmussen retweeted

May 18

there’re many old value pe/hf dogs who are one-dimensionally cheap and love the compelling math of bad companies, so they end up in value traps, grindy 2 baggers over 6 yrs etc (i.e. little to no chance of compounded/non-linear outcomes from things like high returns on capital etc)

but there are also many out of touch vc/growthy folks who seem to have basically no regard for things like math, fundamentals, price etc.

so i have a theory that best investor guys in 2026 should be like 50% Buffett/Thorndike/Rasmussen/etc and 50% Paul Graham/Theil/Helmer/etc said differently, some combination of each side of the below dichotomies:

>empirical/data-driven vs anecdotal/feel (although I think Helmer’s a pretty rigid empiricist)

>avoids egg-on-face vs believes “pessimists-get-to-be-right-but-optimists-get-to-be-rich”

>base-rates/past vs open-to-paradigm-shifts/new-world-economics (e.g. buffet in late 90’s annual was asked why he didn’t invest in internet/tech and he said something like “show me one internet company w more than $100m revs”…so correct via base rates, but also just so wrong)

>rigid vs flexible

>multiples etc. vs network effects/winner-takes-all, returns on capital, 0 marginal costs, TAM etc

>math vs idea

>value vs growth

>east vs west

>quantitative vs qualitative

>past vs future

>pe guy vs vc guy etc

(for sure overly rigid dichotomies but each side is probably some composite those words)

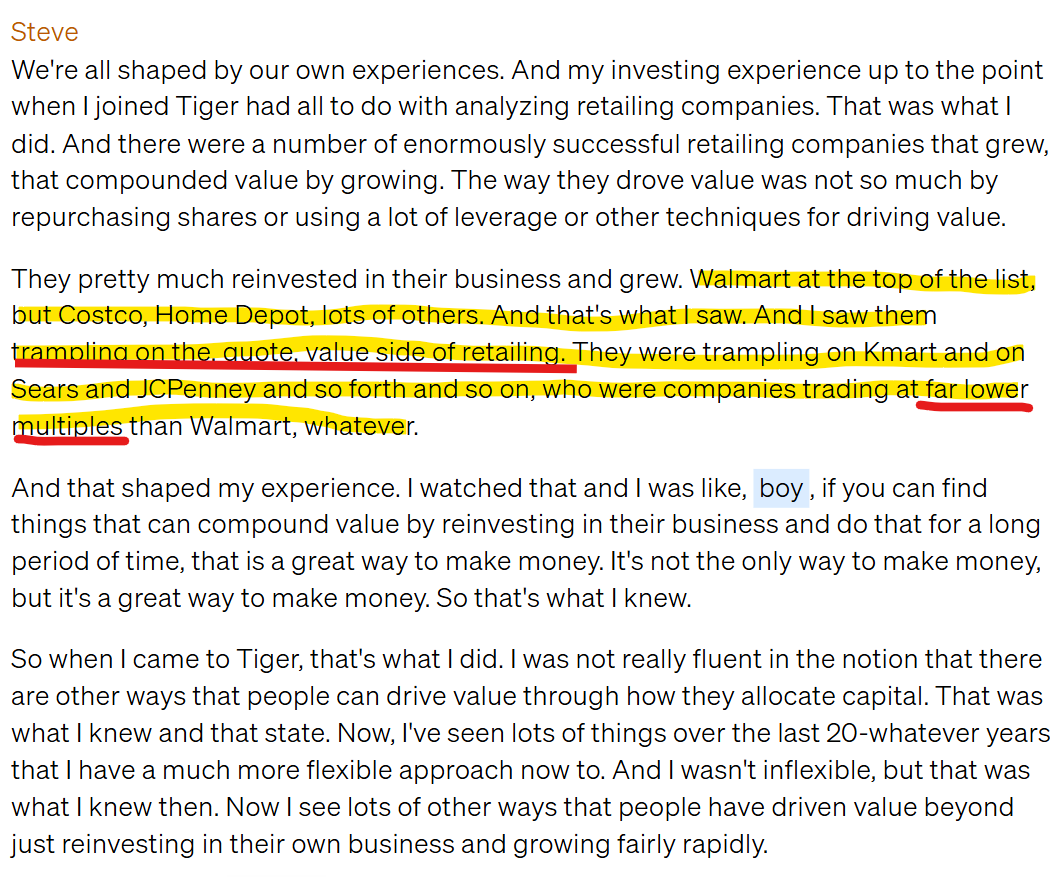

I think Steve Mandel has some great commentary that gets to this balance, here's one example (and Mandel generally seems like a good representation of this balance)

(via awesome @joyscompounding interview) (@hamiltonhelmer, @verdadcap, @paulg tags)

(pls send farm any $2m EBIT deals!)

5

5

51

7,951

Dan Rasmussen retweeted

May 18

Today’s piece from @verdadcap is spot on: mailchi.mp/verdadcap/priced-…

I am very much AI pilled, use it all day for everything, and think it is going to change the world meaningfully. It’s the most transformative technology we’ve seen in decades, and is incredibly dynamic in its use-cases.

I also think we are in some kind of mania / frenzy that eventually will have to pop. I’ve read enough history to not really buy into the ‘this time it’s different’ view

Particularly loved the ending:

“The future is too uncertain and unpredictable to make high-certainty bets. Yet today’s market—and today’s largest tech companies—are taking one of the largest bets in the history of economics on the future of a new technology. One does not need to be a bear on the technology itself—we are power users and love AI—to identify that this moment in market history is likely to be characterized by over-investment, over-spending, excessive valuations, and inevitable disappointment as an uncertain future surprises a consensus narrative that is too specific and too confident relative to the pace of change.”

1

1

13

3,333