人生旅途,荣幸遇你!

Joined January 2022

- Tweets 12,023

- Following 2,268

- Followers 4,677

- Likes 19,175

860 Photos and videos

世界杯期间不管是平台撒钱还是大哥撒钱,机会还是太多了!

恭喜大哥被塞成泡芙😼

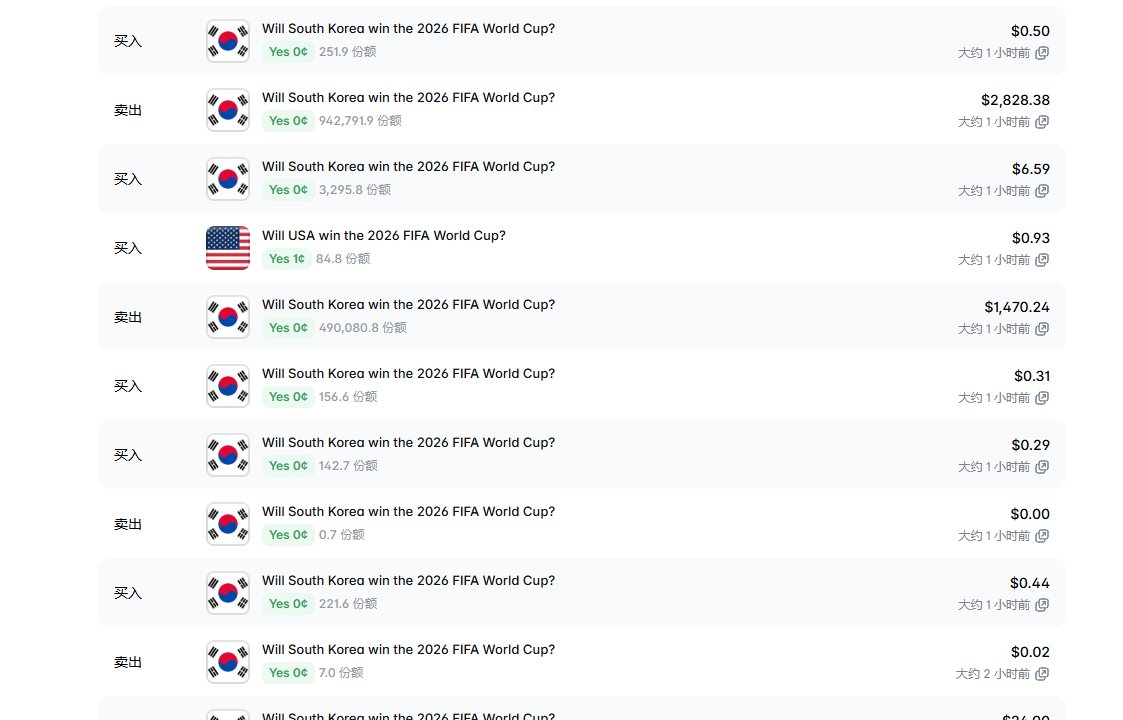

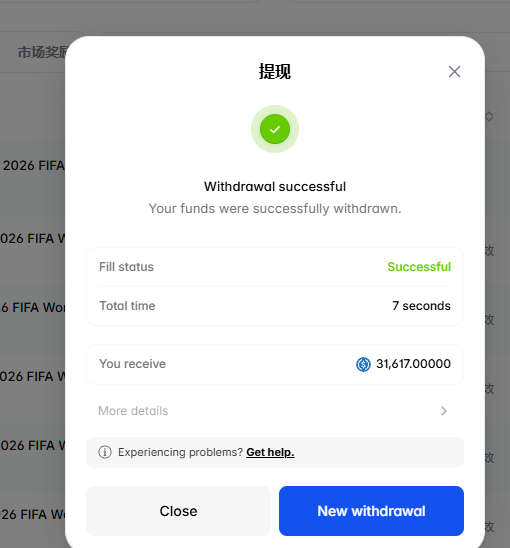

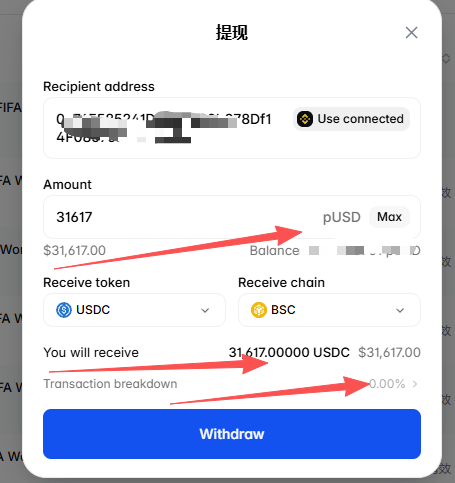

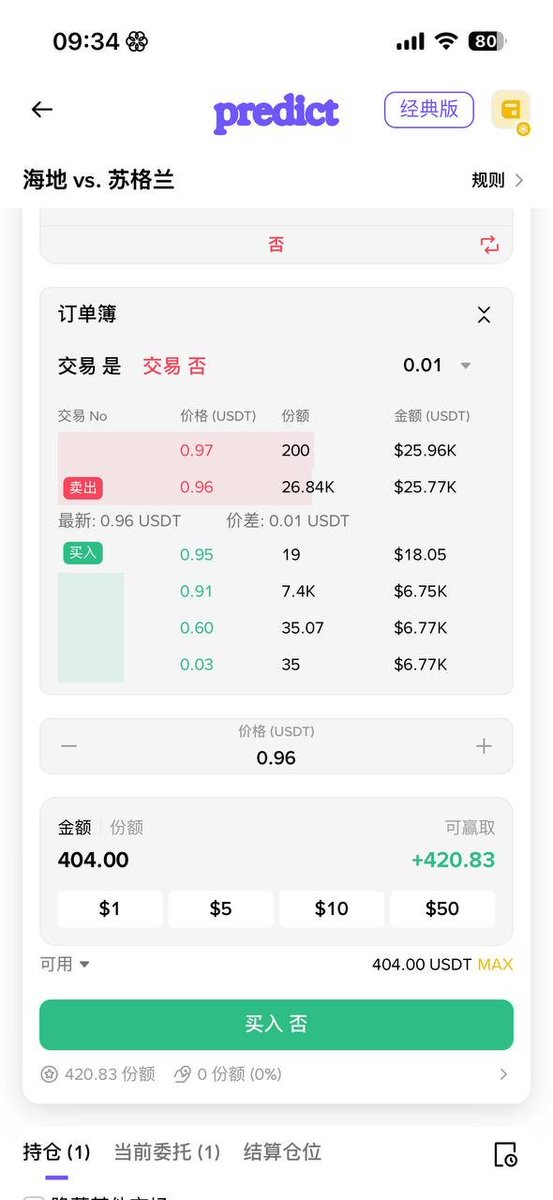

某大哥在 @predictdotfun 上苏格兰对阵海地的比赛上在盘口0-0比分 以 3$的价格挂单了50w份忘记撤单,此时球已经进了!

在群友的呼叫下成功注入 了48.5WU的社区资金,大哥被塞成泡芙,净亏损1.5WU

其实因为最近 @predictdotfun 2m的活动开启, @predictdotfun 与 @Polymarket 的跨平台套利机会非常多,Pf普遍价格比poly高1-2个点,某些比分晚间也会很高,可以双平台对冲套利

倒霉蛋地址围观:

predict.fun/zh-cn/portfolio/…

1

6

1,338

x.com/Caneleo55/status/20658…

现在看来确实是为代币的实用性在做开发!

2

667

poly代币正在加速!

10h

It looks like the CLOB fee module is now being tested on testnet by @mustafap0ly 👀

So once everything is done they simply plug $POLY in as the fee token 🧐

6

1

11

2,120

limitless也搞了一个世界杯百万美金活动!

WE'RE GIVING AWAY $1,000,000 DURING THIS WORLD CUP! ⚽️

Trade WC markets on Limitless, earn XP, climb the leaderboard, and compete for your share of an up to 1,000,000 USDC prize pool

More activity = bigger prize share

Your road starts now → limitless.is/wc2026

2

679

用Ai抽出来了中奖的三位,公平公正!

恭喜这三位!

1. @xmg215215

2. @wuyou818

3. @biquanfangyuan

三位dm我下收获地址谢谢,我统一报给官方一起到时候一起发给你们!

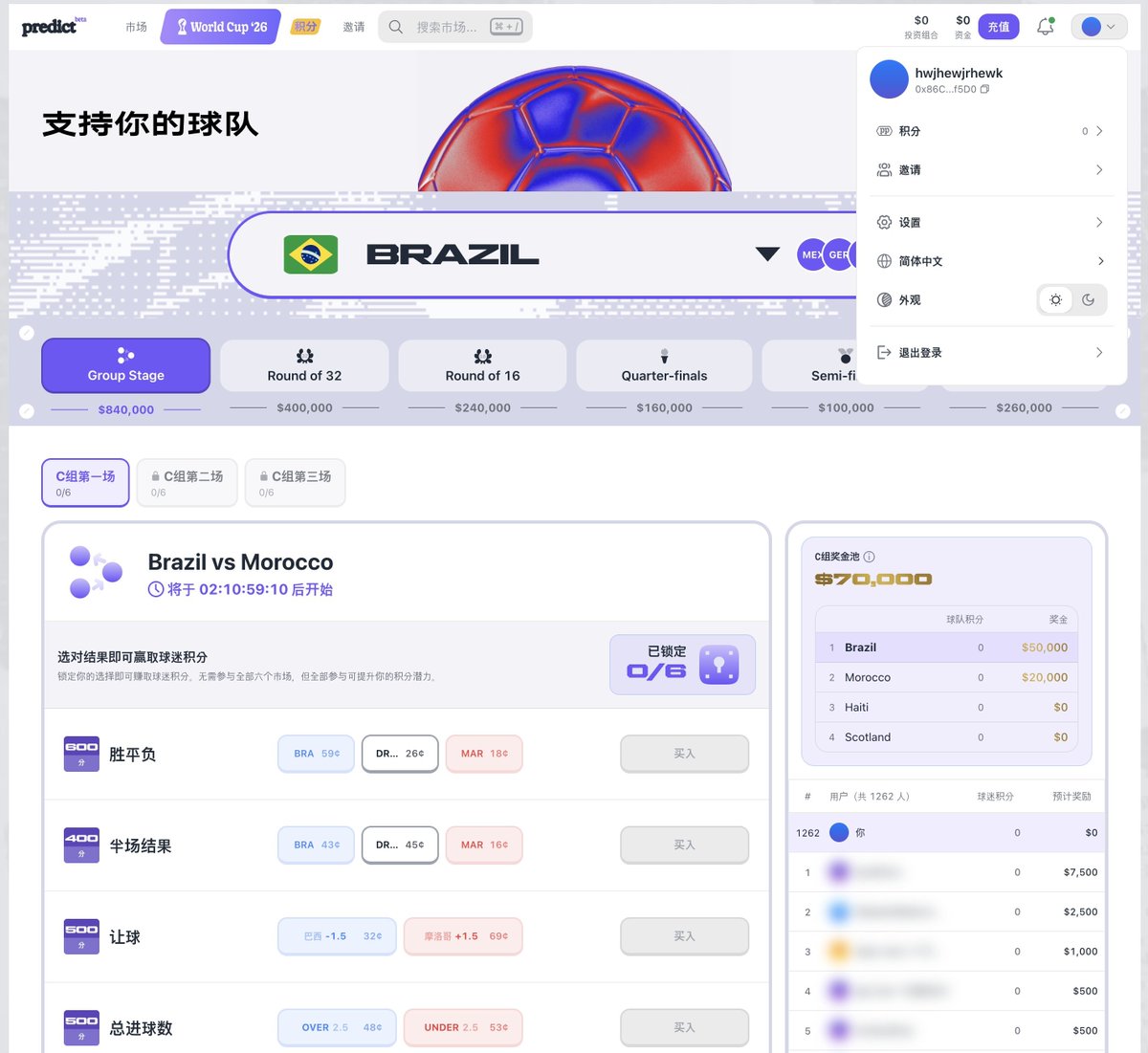

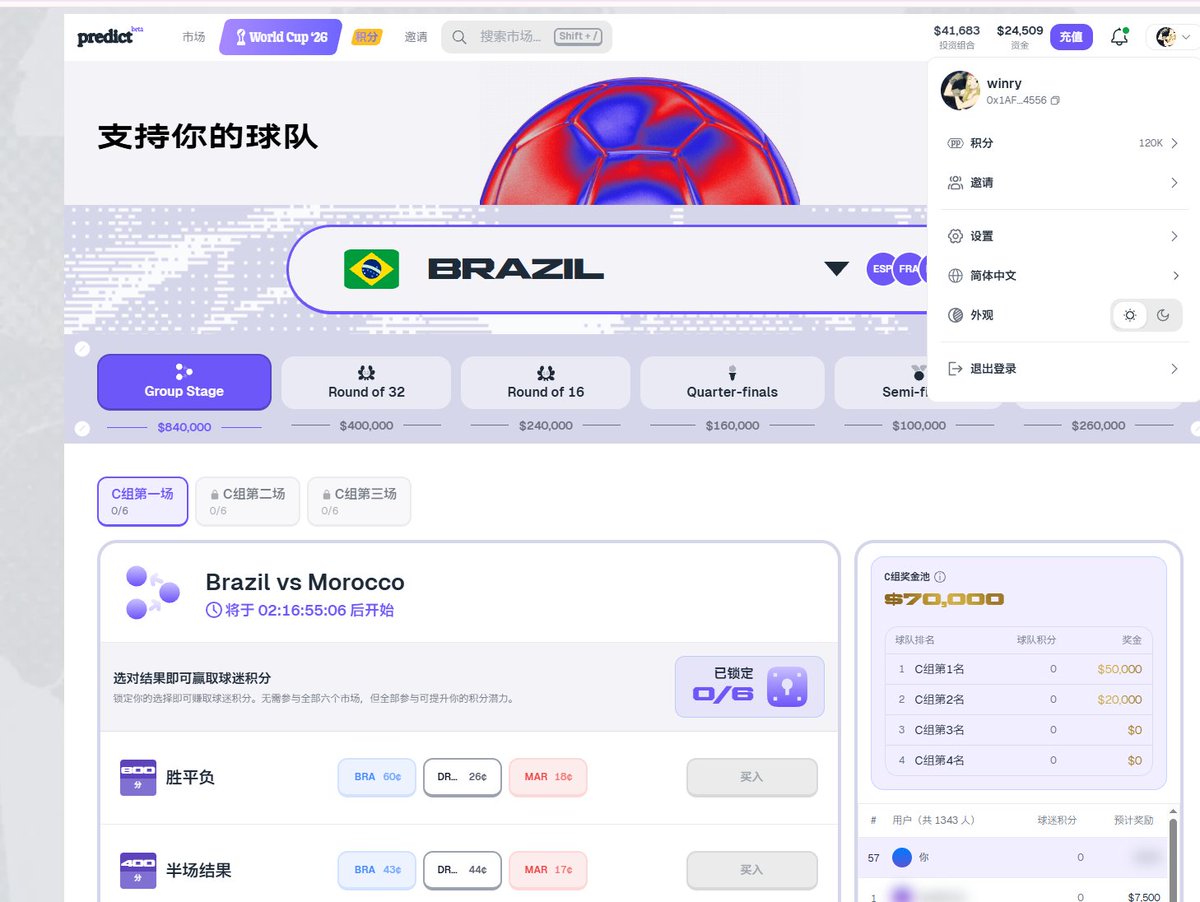

Predictfun200万美金的世界杯预测活动开始啦,你会选哪支球队夺冠呢?

活动入口在 :predict.fun/zh-cn/world-cup

感谢@predictfun和 @yuexiaoyu 老师的特别支持赞助,我这里抽出3套世界杯定制周边给预测市场的家人们!(包含球衣、足球、球袜、幸运硬币)

要求:参与世界杯预测活动,在评论区晒出选队截图(需包含账户名称、积分数、支持的球队,如示例截图!

开奖时间:48小时后@predictdotfun

1

7

1,215

Predictfun200万美金的世界杯预测活动开始啦,你会选哪支球队夺冠呢?

活动入口在 :predict.fun/zh-cn/world-cup

感谢@predictfun和 @yuexiaoyu 老师的特别支持赞助,我这里抽出3套世界杯定制周边给预测市场的家人们!(包含球衣、足球、球袜、幸运硬币)

要求:参与世界杯预测活动,在评论区晒出选队截图(需包含账户名称、积分数、支持的球队,如示例截图!

开奖时间:48小时后@predictdotfun

15

1

16

3,574

Winry retweeted

Jun 13

The CFTC has released its proposed rule on prediction market public-interest determinations. The document is pretty long, so I had AI summarize the key points for me.

The biggest takeaways:

* War, military action, terrorism, assassination, and other crime-related markets would generally not be allowed.

* Election markets are not automatically prohibited and would continue to be evaluated under the existing framework.

* Economic and financial markets (GDP, CPI, rates, etc.) remain largely unaffected.

* Most traditional sports outcome markets appear to be allowed, while highly manipulable “micro markets” could face restrictions.

The biggest impact is likely on geopolitics. If this proposal is finalized in its current form, it will probably become very difficult—or impossible—for regulated platforms to list war-related prediction markets.

federalregister.gov/document…

3

4

17

2,153

Winry retweeted

Jun 13

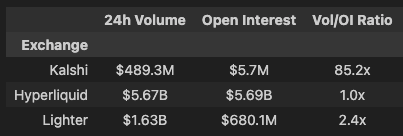

Personally, I think Kalshi’s products are net negative for on chain liquidity. Every product they launch pulls trading liquidity off chain rather than onchain.

As a result, new users entering through Kalshi are more likely to remain within a closed, off chain environment instead of flowing into platforms like Hyperliquid or Polymarket or other chains.

The second order effect is that less liquidity and user activity become composable with the rest of crypto. When state lives onchain, other apps can build on top of it, integrate it, and create new products. When state is offchain, those network effects are harder to capture.

Over time, I suspect many successful onchain products could be replicated offchain via Kalshi or others. I’m sure there is enough liquidity onchain for the ecosystem to absorb some of this, but the question is where the marginal user and marginal dollar end up.

If new demand is captured inside Kalshi first, then the capital, positions, and settlement state tied to that demand are less likely to become composable with the rest of crypto.

Maybe that is fine. Kalshi could grow the overall pie and create more awareness for prediction markets and perps broadly. But the risk I’m watching is that crypto’s strongest consumer finance products get validated in the mainstream while the most valuable network effects accrue offchain

27

4

168

16,190

Winry retweeted

Jun 12

From a release: @Betr today announced it has hedged a 10,000,000 free spins promotion, worth approximately $1.776M, on the US to win the World Cup on @Polymarket . It returns approximately $1.776 million if the U.S. wins, which offsets Betr's exposure to the promotion.

2

4

33

29,003

Winry retweeted

Friday Update - Week of June 8th, 2026:

- Combos beta live: Trade multiple world cup outcomes as a single position, auto-redeem supported from day one. Player props and more sports up next.

- Combos for builders: TS and Python SDK support shipped, plus a new market-maker docs page and Data API endpoints

- Beacon Deposit Wallet: launch moved to 6/22 (from 6/11) to complete full E2E testing and QA post-Combos launch

- Market Resolution upgrade: new system fully live in production, batched on-chain resolutions, markets now settle much faster after close

- Markets deployment: new automated deployment live in production, rolling out from weather markets to all market types

- Perps: taker delay, reduce-only, and TP/SL now live in production; latency improvements on order placement and cancels landing next week; SDK support in progress - Data API: latency cut across endpoints, new market-resolution endpoint added, parimutuel endpoints deprecated; in-house indexer being prepared for production

- Sessions: auth improvements live, fewer unexpected logouts, plus Coinbase smart wallet sign-in support

12

12

58

5,249

Winry retweeted

Jun 12

Protect users when things don't go as planned.

👋

binance.com/en/support/annou…

829

259

2,673

690,272

Winry retweeted

Jun 12

turns out the winners were always going to be the products people actually use

prediction markets and perps

14

4

70

3,899

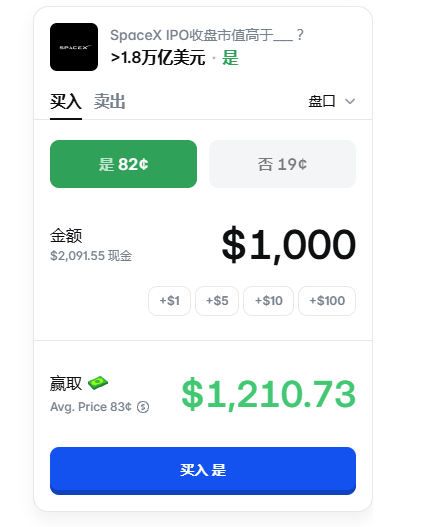

你要是在预测市场参与你现在就是赚的😂

我发现现在各个交易所的SpaceX的Pre-IPO活动是有5%服务费的,相当于你认购的对应SpaceX总市值大约是1.86万亿美金!

但是在 @Polymarket SpaceX上IPO当日总市值收盘在1.8T市值以上概率是82%,投入1000U的收益在1210u,大概收益率在20%左右!

假设你要参加交易所那种额度打新模式,要拿到这20%收益那么卖出的SpaceX的总市值至少在2.2万亿以上。而且现在这么fomo的情况下可能你投入10万u才有这1000u的额度,所以我认为小资金其实完全没必要去交易所打新了,可以用预测市场这种方式参加下历史上最大的IPO,也算参与到人类重要历史进程之一了!人生重在参与对吧,参与了就算亏钱了,老了也有给孙子辈吹嘘的资本!

当然这种风险肯定比传统Pre-IPO的方式高不少,就比如当天SpaceX总市值收盘在1.8万亿以下,那你的本金就没了,DYOR!

4

6

2,711

Winry retweeted

Jun 12

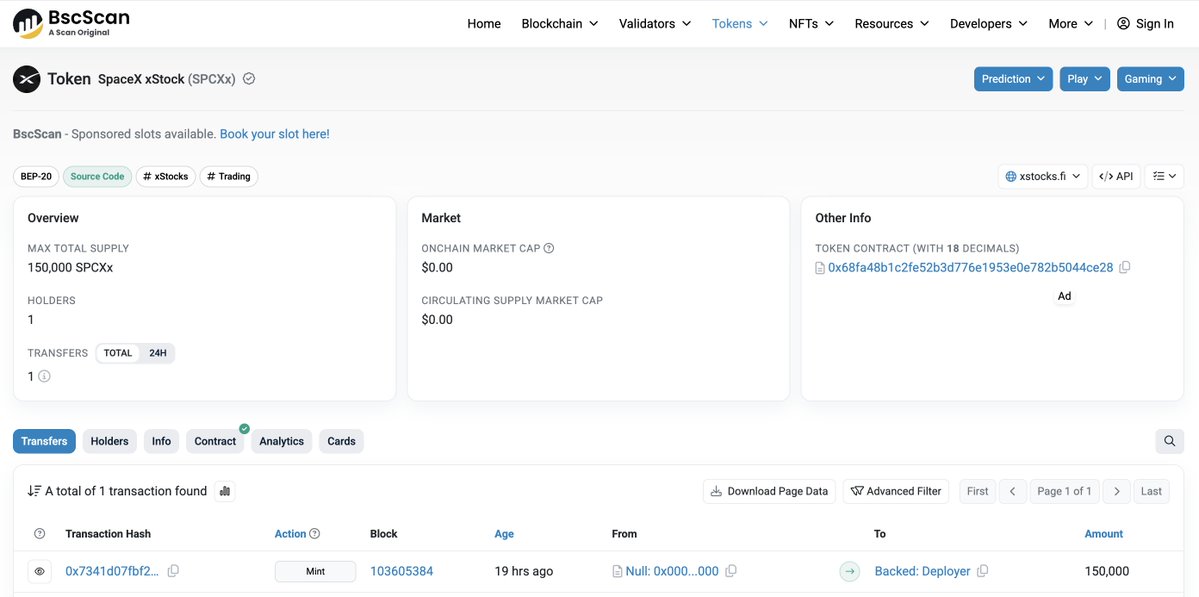

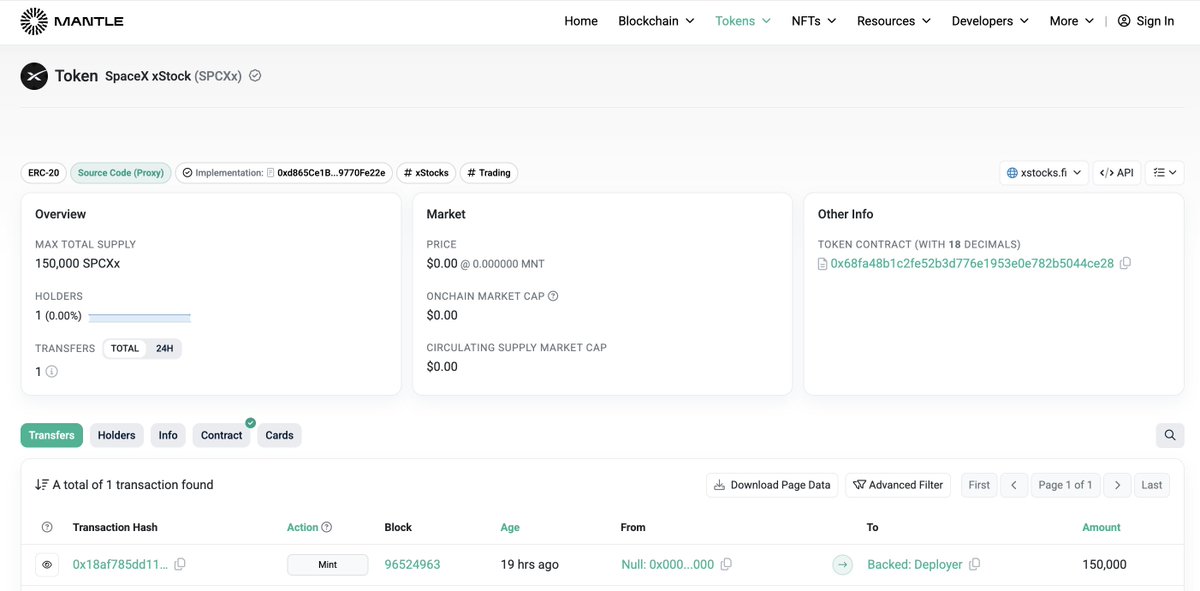

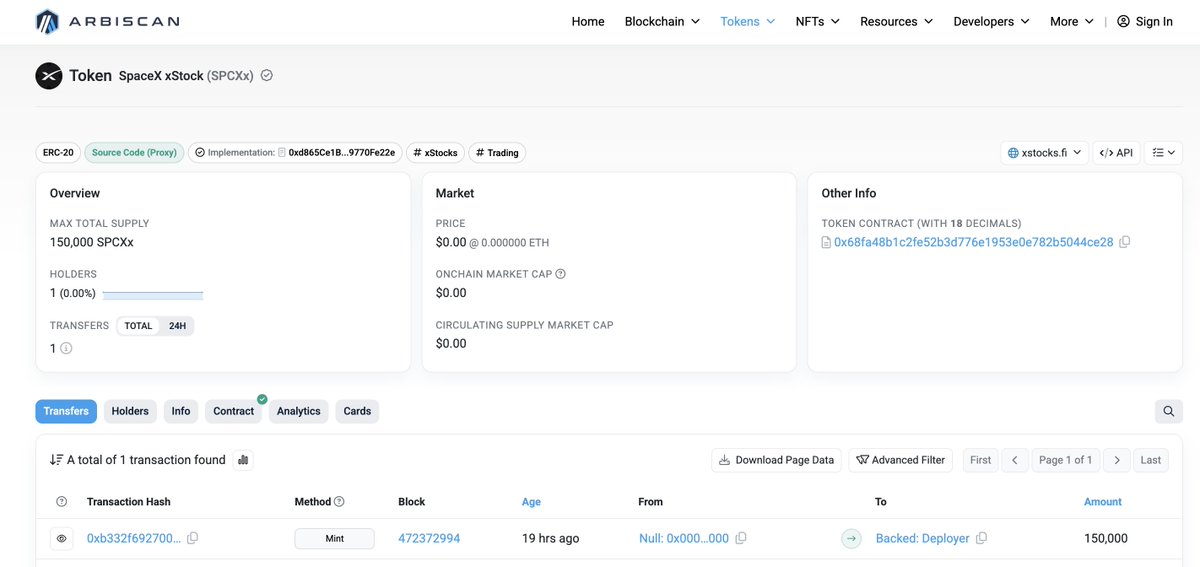

那些担心Binance的SPCXx只有15万股额度的,大可不必

15万股大概率只是各条小链的初始流动性,聪明人只需要看一下其他链的SPCXx的量就知道了,都是15万股

主要额度分配应该在Solana链,当然也不排除会分配到其他链的可能,例如Binance的分配在Bsc、Bybit的分配在Mantle、Gate/BG这些分配在Eth、Kraken的分配在Solana(那各条链就还会再加),都是我猜的

这东西我本来不想发出来的,如果你足够聪明知道我想表达什么👀

22

13

109

59,851