Joined December 2008

- Tweets 4,226

- Following 122

- Followers 440

- Likes 201

170 Photos and videos

Le Wang, EA retweeted

31 Jul 2025

If anyone has friends on the editorial teams of the @WSJ, @FinancialTimes, @barronsonline, @CNBC, @Bloomberg, or @FoxBusiness, please have them reach out to exclusively feature this timely OpEd I just penned regarding the @federalreserve after their policy mistake today. Enjoy!

---

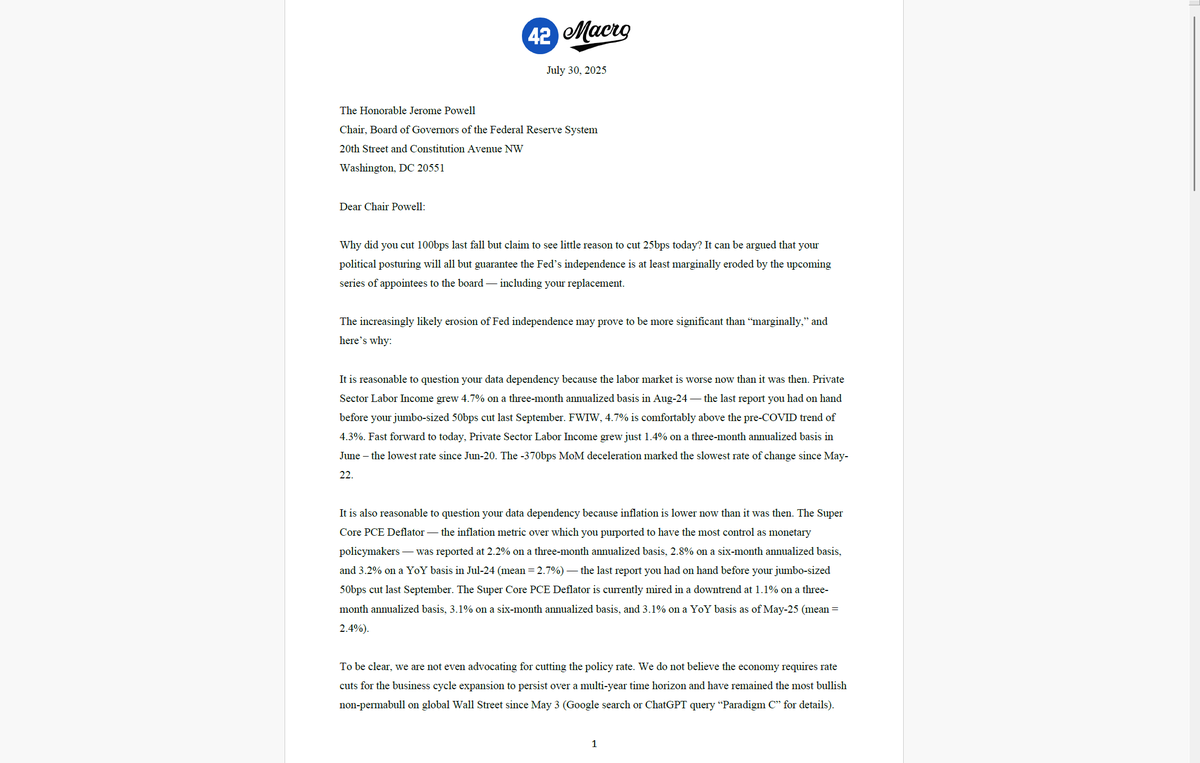

The Honorable Jerome Powell

Chair, Board of Governors of the Federal Reserve System

20th Street and Constitution Avenue NW

Washington, DC 20551

Dear Chair Powell:

Why did you cut 100bps last fall but claim to see little reason to cut 25bps today? It can be argued that your political posturing will all but guarantee the Fed’s independence is at least marginally eroded by the upcoming series of appointees to the board — including your replacement.

The increasingly likely erosion of Fed independence may prove to be more significant than “marginally,” and here’s why:

It is reasonable to question your data dependency because the labor market is worse now than it was then. Private Sector Labor Income grew 4.7% on a three-month annualized basis in Aug-24 — the last report you had on hand before your jumbo-sized 50bps cut last September. FWIW, 4.7% is comfortably above the pre-COVID trend of 4.3%. Fast forward to today, Private Sector Labor Income grew just 1.4% on a three-month annualized basis in June – the lowest rate since Jun-20. The -370bps MoM deceleration marked the slowest rate of change since May-22.

It is also reasonable to question your data dependency because inflation is lower now than it was then. The Super Core PCE Deflator — the inflation metric over which you purported to have the most control as monetary policymakers — was reported at 2.2% on a three-month annualized basis, 2.8% on a six-month annualized basis, and 3.2% on a YoY basis in Jul-24 (mean = 2.7%) — the last report you had on hand before your jumbo-sized 50bps cut last September. The Super Core PCE Deflator is currently mired in a downtrend at 1.1% on a three-month annualized basis, 3.1% on a six-month annualized basis, and 3.1% on a YoY basis as of May-25 (mean = 2.4%).

To be clear, we are not even advocating for cutting the policy rate. We do not believe the economy requires rate cuts for the business cycle expansion to persist over a multi-year time horizon and have remained the most bullish non-permabull on global Wall Street since May 3 (Google search or ChatGPT query “Paradigm C” for details).

What we are advocating is that you drop the “Mr. Tough Guy” act on inflation.

You had no problem being the most dovish Fed chair since the advent of using the policy rate as the primary tool for conducting monetary policy. Arthur Burns’ trough spread of -720bps below what would have been the baseline Taylor Rule estimate at the time looks hawkish compared to your trough spread of -1,040bps in Feb-22 — when you were still performing quantitative easing into a 40-year high in inflation.

You had no problem growing the Fed’s balance sheet to a peak of 36% of GDP in Nov-21 — a year in which the federal budget deficit clocked 10% of GDP, after a whopping 15% in 2020. These figures compare to just 5% in 2019, 4% in 2018, and 3% in 2017. The current Fed balance sheet/GDP ratio of 22% is still well north of the long-run mean of 16% for this time series — data which features your ultra-dovish focus on “maximum and inclusive employment” and green-energy-supportive monetary policy.

We do empathize with why you’re acting tough on inflation. Respectfully, sir, you are 72 years old and like most people in their 70s, you may be succumbing to the understandably human desire to build and preserve your legacy.

Additionally, the Trump administration’s tariff policy shock is significantly larger than anyone expected. Per the Budget Lab at my alma mater Yale, the overall average effective tariff rate of 18.4% is the highest rate since 1933. At some point this will feel like inflation as affected goods finally pass through the system.

But the preponderance of credible academic literature concludes tariffs aren’t inflationary. The PhD economists at your own institution agree — or at least they did agree prior to President Trump’s second ascent into the Oval Office, but that’s neither here nor there.

What is relevant here is the slowdown in Real Services PCE, which grew a paltry 1.1% on a QoQ SAAR basis in Q2 — just one-third of the 3.0% rate recorded in 2024. Real GDP ex-Government & Net Exports contracted at a -3.2% QoQ SAAR pace in Q2, the lowest rate since the COVID lockdowns of 2Q20.

There was a sound economic case to be made for lower policy rates today — we wouldn’t have had two Fed governors dissent for the first time in 32 years otherwise.

Specifically, the labor market is likely to weaken further on a lag to the near contraction in capex observed in the Q2 GDP data (0.4% QoQ SAAR vs. a pre-COVID trend of 3.5%), slowdown in corporate profits growth (S&P 500 constituents 6.4% YoY Q2-to-date vs. 13.6% in Q1 and 11.3% in 2024), and persistently elevated policy uncertainty (e.g., highest ever yearly average for the Baker, Bloom, and Davis Economic Policy Uncertainty Index — a time series that includes data from both COVID and the GFC).

There is an equally unsound economic case to be made for keeping policy rates cyclically and structurally elevated today: the risk of “unanchoring” inflation expectations.

Putting aside the fact that we do not believe the mere ‘unanchoring’ of inflation expectations can cause persistent above-trend inflation in the absence of persistent above-trend credit growth in either the private or public sectors, Chair Powell, you and your colleagues are the primary reason this risk exists. You let the inflation genie out of the bottle by running historically expansionary monetary policy amid an obvious and historic expansion of fiscal policy.

This is why we strongly believe the administration is right to pursue regime change at the Fed. Whether or not they get it right is irrelevant at this juncture. Time will tell on that front.

Lastly, please do not interpret this as a personal attack on you or the institution. Rather, this is a data-driven perspective on how you and your colleagues at the institution have failed the American public and continue to fail the American public. Heaven forbid the FOMC be held accountable for the dramatic outcomes it contributes to in our K-shaped economy and asset markets.

Anyone reading this would be a fool to not agree that better monetary policy can potentially help engineer better outcomes for the consumers and businesses trapped on the bottom part of the “K”.

There are obviously no guarantees that the pending regime change at the Fed will accomplish this goal — or in life in general, save for the fact that two wrongs don’t make a right in Fed policy mistake terms.

Thank you for reviewing, and thank you for your service to the American public. Regardless of whether you and I see eye to eye on your still-developing track record, I recognize how hard your job is and appreciate your efforts nonetheless.

Thank you and God bless,

Darius Dale, Founder and CEO of @42Macro

22 Jul 2025

THREAD: This will likely be the most important thread regarding the @federalreserve you've reviewed in a very long time.

1/6

41

62

378

176,262

Le Wang, EA retweeted

5 Jul 2025

As someone who grew up dependent on SNAP, Medicaid, and Welfare, this question has been weighing on my heart all weekend:

When the government wants to incentivize poor people to contribute more to the economy, it gives them “work requirements”.

When the government wants to incentivize rich people to contribute more to the economy, it gives them trillions of dollars in tax cuts, subsidies, and government contracts.

I think we could solve a lot of our K-shaped socioeconomic problems if we flipped this policy mix. Surely, the poor people need the money more than we do, no?

As a successful business owner, I don’t need tax cuts, subsidies, and government contracts to *want* to grow my business. I am incentivized by my own desire to create fabulous outcomes for my clients, my employees, and each of their families.

Why do so many of the other rich people in this increasingly K-shaped economy need handouts—“rich people welfare”—to grow their businesses? Moreover, why are so many of them so mean to the poor people on welfare too? You’d think they’d relate.

At any rate, I quit my lucrative Wall Street job in part because I got sick of only making rich people richer. I wanted, needed, to make ALL people richer.

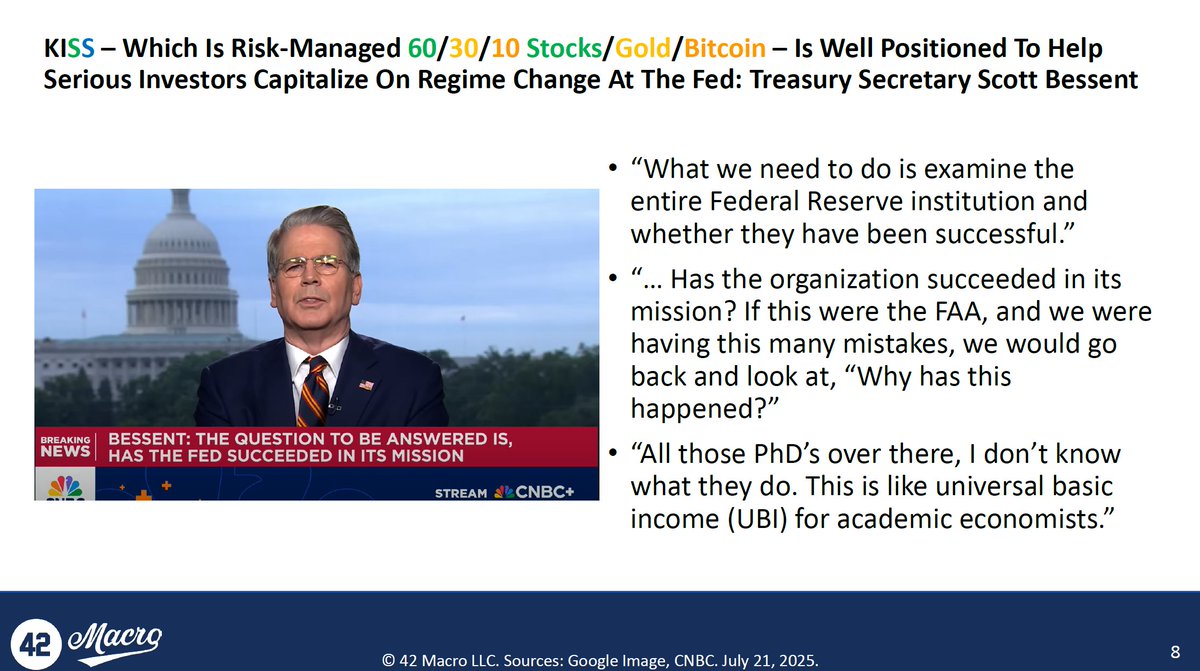

We built @42Macro to satisfy this burning passion of mine and our *completely systematic* KISS model portfolio does exactly that for thousands of investors across the world—from the hallowed halls of Wall Street to the family rooms on Main Street.

Sadly, the KISS strategy—risk-managed 60/30/10 Stocks/Gold/Bitcoin—is designed specifically to capitalize on America’s decaying economic and moral fabric. I’m not proud of that part, but helping thousands—perhaps millions someday—of regular people become rich and grow their wealth is the best solution I could devise with the gifts God blessed me with.

Thanks for reading about why I’ve been sad all weekend and a key part of what I’m doing to help our divided, K-shaped society heal. I love and appreciate you. ❤️

535

382

2,630

629,151

Le Wang, EA retweeted

15 Mar 2023

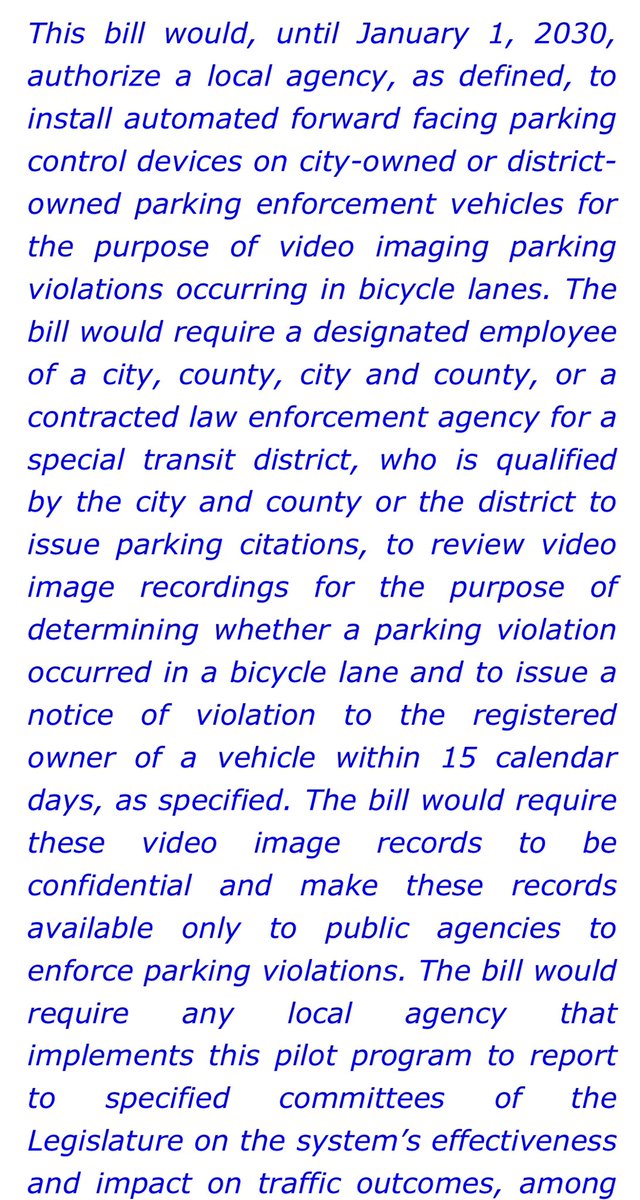

#AB361

“Vehicles: video imaging of bicycle lane parking violations.”

PEW PEW PEW!!!

1

5

2,333

15 Mar 2023

The best way to #StopWillow is to speed up global warming so that it will be too unstable for @conocophillips to drill there. #ohtheirony #StopWillowProject

1

509

Le Wang, EA retweeted

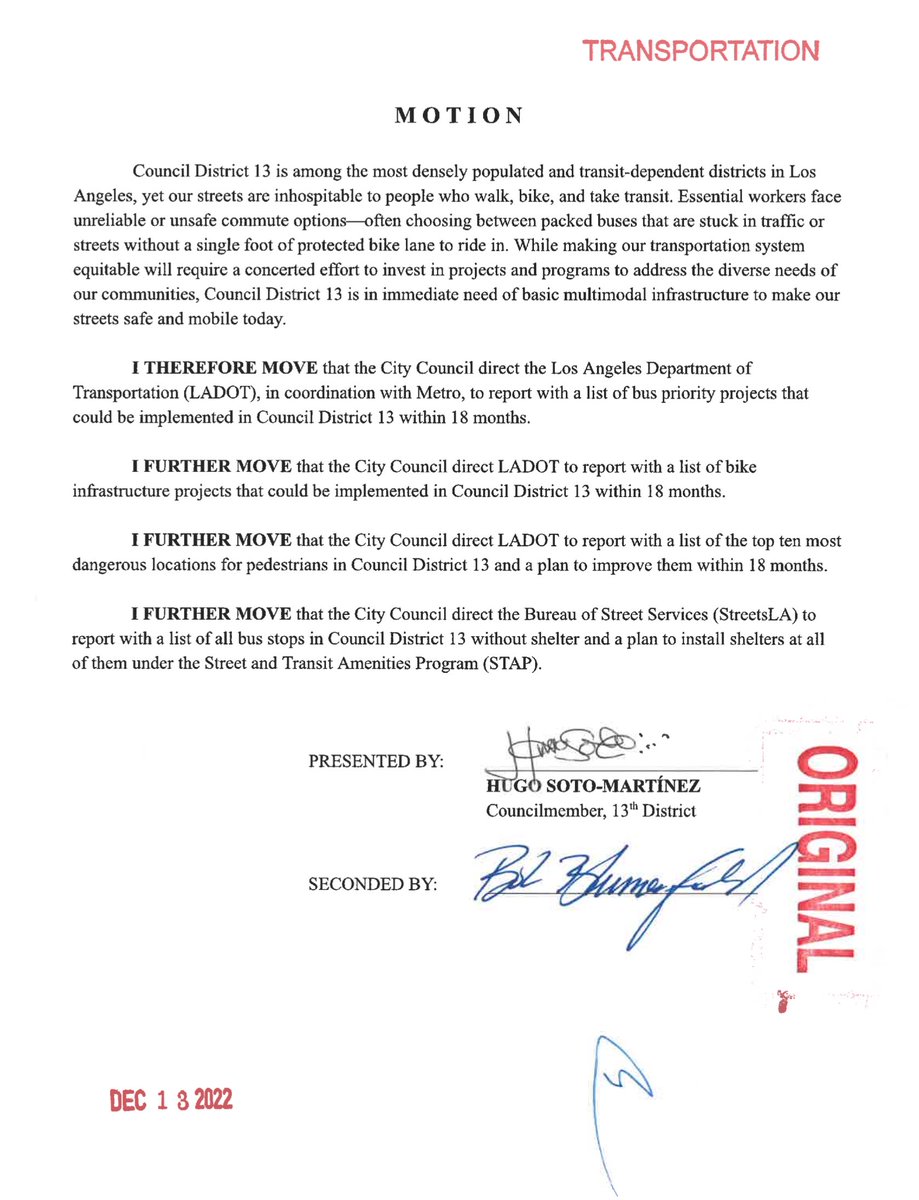

14 Dec 2022

What a difference a week makes. This is 🔥 coming from @HugoForCD13. Thank you, Hugo, for your leadership!

12

43

349

7 Mar 2023

Verifying myself: I am wangle on Keybase.io. ymKp-kZNKOInM2BKddAPAZYwJNVh816fEyyR / keybase.io/wangle/sigs/ymKp-…

288

7 Sep 2022

Every Apple event is like ground hog day. I come up and see if iPhone has USB-C yet. Nope, going back into my hole.

1

Le Wang, EA retweeted

7 Sep 2022

Great consumer response yesterday to stabilize the grid. More help needed today as historic heat wave continues. When a lot of people change their behavior in relatively small ways big things can happen. bit.ly/3RL6Mbi

43

82

365

Le Wang, EA retweeted

7 Sep 2022

At 8 p.m., the grid operator ended its Energy Emergency Alert (EEA) 3 with no load sheds for the night. Consumer conservation played a big part in protecting electric grid reliability. Thank you, California!

235

920

5,859

31 Dec 2020

Happy New Years Eve everyone! Here are the Top 5 Lessons 2020 taught me. Enjoy! 😂

youtu.be/BMxGM1whNrU

1

1

21 May 2020

*TODAY* Looking to find an audience during COVID-19? Our speakers share their success stories and help you take the next steps.

eventbrite.com/e/we-got-your…

22 Apr 2019

Got to spend the day with these two and justjimmyslife ❤️ @ Vitality Bowls instagram.com/p/BwjJXNZn4Fq/…

1

21 Feb 2019

Which would you rather do?

100%

Rent

0%

Own

1 votes • Final results

1

23 Dec 2016

@lauryngoldberg Hey thanks for sharing your experience with acne and accutane. #notalone