Joined June 2024

- Tweets 952

- Following 91

- Followers 83

- Likes 91,218

75 Photos and videos

Jun 12

$gme has Ryan Cohen made a deal with shorts to bail them out

67%

Yes

33%

Yes

33 votes • Final results

2

3

16

1,912

Jun 3

$gme hype bots can start spamming for the next 2 weeks played by Ryan Cohen and the shorts like cello. Buybacks won't happen only did this shit so you vote yes.

5

1

17

1,045

Weeee retweeted

Jun 2

So that’s why $GME was suppressed a few days longer than expected…

Someone knew and used the q1 results (which came a week early!!) as the pressure release justification.

16

24

427

20,609

May 22

$gme watch the eBay stuff fall apart after apes vote to approve more shares and Ryan Cohen's pay package.

3

1

14

1,182

Weeee retweeted

May 14

The Hollow Chairman

American retail investing is rotting from the top down.

We replaced the “Owner-Operator” with something far more dangerous:

The Cultivated Insider.

By “Insider,” I am not referring to a title. I am referring to the modern celebrity CEO who understands that in today’s market, perception matters more than performance, and loyalty matters more than results.

These are the hollow men of modern finance.

They speak in memes instead of guidance.

They communicate through riddles instead of accountability.

They cultivate mythology instead of execution.

They position themselves as anti-Wall Street revolutionaries while operating the oldest game in corporate America:

Using shareholder devotion as leverage for personal empire building.

In a functioning market, shareholders invest in a business because management allocates capital responsibly and creates value.

Today, we have severed that relationship.

Now shareholders are expected to invest in a personality.

The modern Insider no longer needs transparency. He needs engagement.

He does not need fundamentals. He needs believers.

If the stock rises, he is hailed as a genius visionary building the next Berkshire Hathaway. If the stock collapses, the retail investor is told to “zoom out,” “trust the process,” or laugh along with another cryptic joke online.

Heads, the Insider wins.

Tails, retail is told to wait longer.

This is the new shareholder contract:

Retail absorbs dilution.

Retail absorbs volatility.

Retail absorbs emotional exhaustion.

Meanwhile the Insider absorbs power, cash reserves, optionality, and compensation structures tied to ambitions far larger than the original business itself.

And the manipulation is psychological more than financial.

The memes.

The mysterious posts.

The calculated silence.

The strategically timed appearances.

The ironic detachment whenever shareholders demand clarity.

Every vague clue becomes a loyalty test.

When technical momentum builds, when sentiment turns euphoric, when the possibility of a breakout starts feeding on itself, somehow another distraction appears at exactly the right moment to cool speculation, reset expectations, or fracture momentum.

Then comes the gaslighting.

“You just don’t understand long-term strategy.”

“Real investors aren’t emotional.”

“This is chess, not checkers.”

But real owner-operators do not endlessly dilute the very people funding the mission while pretending dilution is some enlightened act of strategy.

Real owner-operators communicate clearly.

Real owner-operators respect the people who carried the company through crisis.

Instead, the modern Insider wraps arrogance in irony.

He brags about not taking a salary while shareholders absorb repeated dilution events that accomplish the same extraction through different mechanics.

He mocks the financial media while carefully cultivating his own mythology inside online communities.

He avoids direct accountability because ambiguity is safer than transparency.

And the most dangerous part?

Retail mistakes detachment for genius.

They interpret silence as depth.

They interpret riddles as leadership.

They interpret volatility as proof of hidden strategy.

Meanwhile, the company becomes secondary to the persona.

The stock transforms into a vehicle for ambition far beyond the original shareholder mission: building a legacy, building a holding company, building a personal image as the next Warren Buffett — all funded by investors emotionally conditioned to defend every decision no matter the cost.

This is not alignment.

This is modern financial theater.

And just like every other era of market excess, it survives only as long as people continue confusing symbolism with execution.

The era of the Cultivated Insider must end.

$gme

Feb 18

The Hollow Men

American capitalism is rotting from the head down. We have replaced the "Owner-Operator"—the risk-taker-with a new, parasitic class of corporate bureaucrat: The Risk-Free Insider.

By "Insider," I am not referring to a specific title. I am referring to the entire administrative state that has captured the modern corporation. This includes the Directors who exist solely to collect fees, the Executives who exist solely to collect bonuses, and the Managers who exist solely to hire consultants.

These are the hollow men of the boardroom. They are masters of PowerPoint. They wear the right suits. They say the right buzzwords about "governance" and "ESG." But they are mercenaries fighting a war with someone else’s ammunition.

In a functioning economy, authority is tied to liability. If you make a bad decision, you lose your own money. That fear of loss is the only thing that keeps a business honest. It forces you to cut waste, obsess over the customer, and stay late to fix what is broken.

Today, we have severed that link.

We have rigged the game so that heads, the Insider wins; tails, the shareholder loses.

If the stock goes up, the Insider collects a massive performance bonus. If the stock crashes due to their own incompetence, they are fired with a "Golden Parachute" worth tens of millions. They are gambling with the house’s money, and they never leave the table poorer than they arrived.

This looting starts in the boardroom.

We have normalized a "Country Club" culture where directors are selected based on social profiling rather than their ability to build a business. The modern board member is often a professional tourist—paid an average of $350,000 a year.

Let’s be brutally honest about what that number represents. The average director is paid nearly five times the GDP per capita of the United States. They earn more for attending four quarterly lunches than the vast majority of Americans earn in five years of hard labor.

And for what?

Most of these directors are "over-boarded," sitting on three or four boards simultaneously. They treat directorships as a gig economy for the elite. They fly in, rubber-stamp a compensation package they didn't read, and fly out. They collect checks from companies they do not understand, do not use, and certainly do not love.

They are not there to ask hard questions. They are there to be collegial. They are there to protect the other Insiders.

And what happens when these boards hire executives who also have no personal capital at risk?

We get the Delegation Economy.

When a Risk-Free Insider faces a crisis—bloated expenses, a broken supply chain, or a stale product—they do not roll up their sleeves. They hire a consultant. They pay a strategy firm millions of shareholder dollars to produce a 100-page deck telling them what they already know.

This is not management. It is intellectual money laundering.

They use shareholder capital to buy an insurance policy for their own careers. If the plan fails, they can blame the consultants. They delegate the work because they are terrified of the responsibility. They would rather preside over a slow, comfortable decline than risk a bold mistake.

While American Insiders are busy optimizing their severance packages, our global competitors are optimizing their products. They are not slowed down by bureaucracy. They are not waiting for a slide deck. They are outworking us.

If we continue to fill our C-suites with administrators instead of operators, we will lose our edge. We will see iconic American franchises hollowed out by fees, managed for the benefit of the Insiders, while the true owners—the shareholders—are left holding the bag.

The time for polite governance is over.

If we want to save the American economy from mediocrity, we must demand a return to the "Owner’s Mentality." We need leaders who treat shareholder capital with the same reverence they treat their own savings. The era of the Risk-Free Insider must end.

8

9

33

4,962

May 18

$GME why did Ryan Cohen play along the moass thing to keep stringing shareholders along and keep them trapped?

55

5

105

16,472

May 15

$gme so why does Ryan Cohen always do some bearish right before breakout or after to kill runs?

15

2

57

3,272

May 13

$gme Funny superstonk getting astroturfed by short bots again: "vote yes for dilution. It's infinitely shorted anyway".

1

14

467

May 11

$gme dilute us harder Ryan Cohen we hate making money. Might as well bailout those shorts too while you are at it.

5

209

May 10

$gme Ryan Cohen's bots justifying his pay package by saying he has to buy those shares which is a lie.

27

1

26

5,378

Weeee retweeted

My theory is that Cohen was installed to prevent $GME from squeezing again like it did in 2021. It was setting up to squeeze last week based purely on technicals and FTDs and he killed it with this shitty eBay gimmick. Just like two years ago when he killed it with an offering

9

2

15

2,925

Weeee retweeted

May 4

The $GME proposed acquisition of $EBAY is even dumber than it sounds, which is why he refused to answer @andrewrsorkin's basic questions this am.

To start, the ACTUAL proposal is not GME acquiring EBAY:

GME is the seller, not the buyer.

Ryan Cohen is asking eBay to acquire GME, fire eBay's CEO, and let Ryan run the business.

Onto the dumbness of the proposal details:

The idea is 50% cash / 50% stock for roughly $56 billion of consideration to eBay.

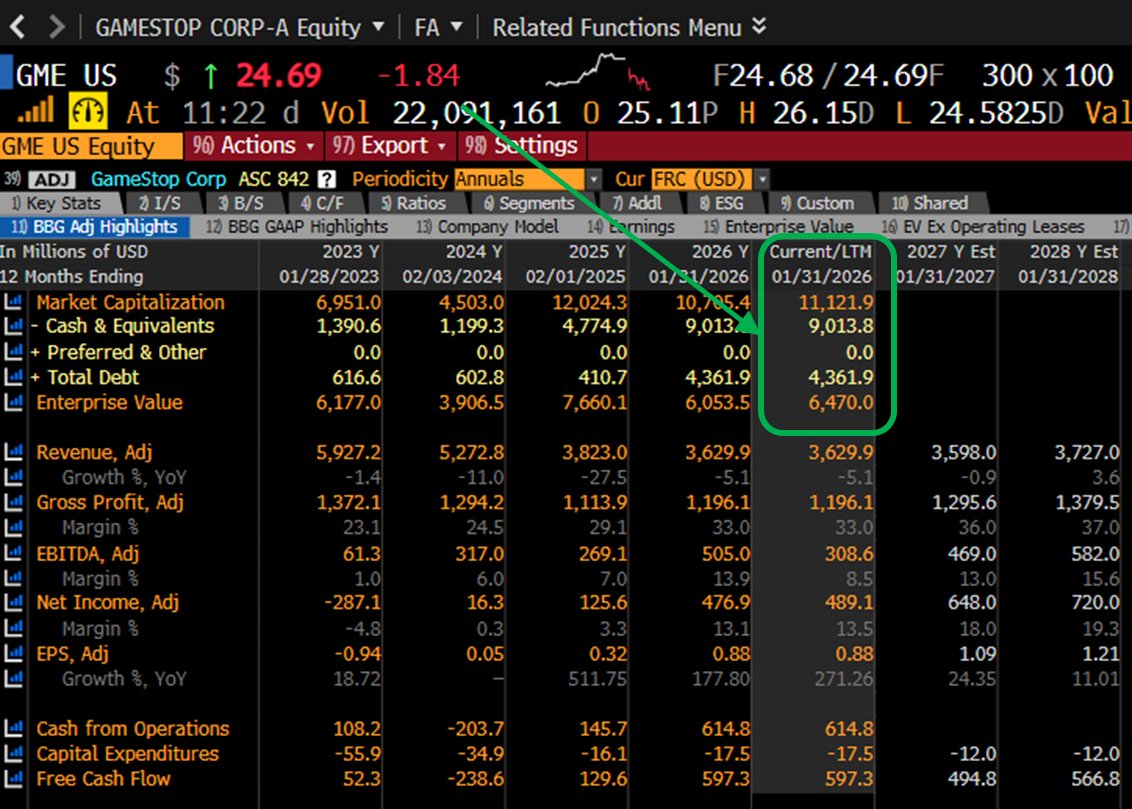

Pundits note GME's ~$11.1B market cap and ~$9B of existing cash.

BUT THAT DOUBLE-COUNTS.

Of GME's ~$11.1B market cap, ~$9B IS THE CASH.

Or 81% of the market cap.

If I have a company worth $110 with $90 of net cash, it's not worth $180: the cash is worth $90, and the company ex-cash is worth $20 = $110.

As shown below, if GME pays eBay the ~$9B in existing cash, the remaining market cap (from eBay's perspective) is ~$2.1B.

GME shares are worth ~$5/share ex cash.

To issue $28 billion of GME shares, it has to issue ~5.6B of new shares to eBay (vs 590B FD GME shares today), giving eBay 90% of the post-deal shares ( $28 billion of cash to eBay owners).

To be clear, GME is proposing that eBay acquire GME, with GME owning 10% of the CombinedCo.

In 2026, eBay is expected to generate $2.8B of free cash flow vs $500 mm by GameStop (15% of combinedco).

eBay revenue is expected to GROW 9% in 2026 while GME's is expected to shrink 1% (and has shrunk >40% in 5 years).

So eBay brings 85% of the cash flow and is growing, and gets 90% of a newco that is dragged down by GameStop's declining revenue.

To compensate for owning a lower quality CombinedCo, it levers up and pays legacy eBay $62/share in cash.

However, that cash is financed by the quality of eBay's business, not GameStop.

eBay doesn't need GameStop to recap its existing business - it could do so and continue to own 100% of the better business.

Ultimately, this is GME attempting to swap into a better business by selling itself to eBay, not vice versa.

Everyone knows this deal won't happen, Ryan Cohen included.

110

129

1,256

506,532

Weeee retweeted

May 4

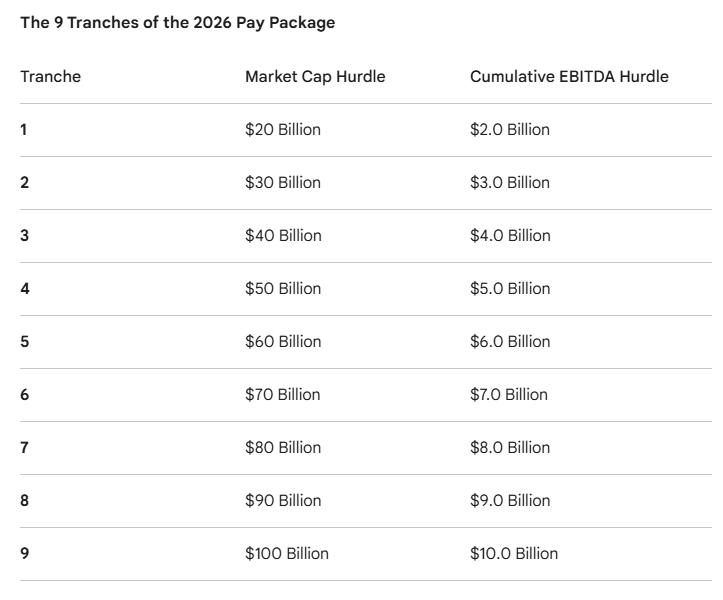

The $GME situation is wild.

The CEO Ryan Cohen has an options package for 171m shares that he can earn if he hits certain market cap and EBITDA hurdles.

The crazy thing is that this is not adjusted for dilution. He needs the market cap to be $20b to get the first tranche but he can just issue a crapload of shares!

This is why he wants to buy $EBAY.

102

88

1,633

315,254