Simple portfolios. Data-driven • Windmill Capital Private Limited • SEBI-regd RA: INH200007645 • SEBI-regd PMS: INP000009852 • Dsclsr: l.smlc.se/wnd-dsc

Joined May 2021

- Tweets 2,814

- Following 14

- Followers 15,298

- Likes 178

615 Photos and videos

Pinned Tweet

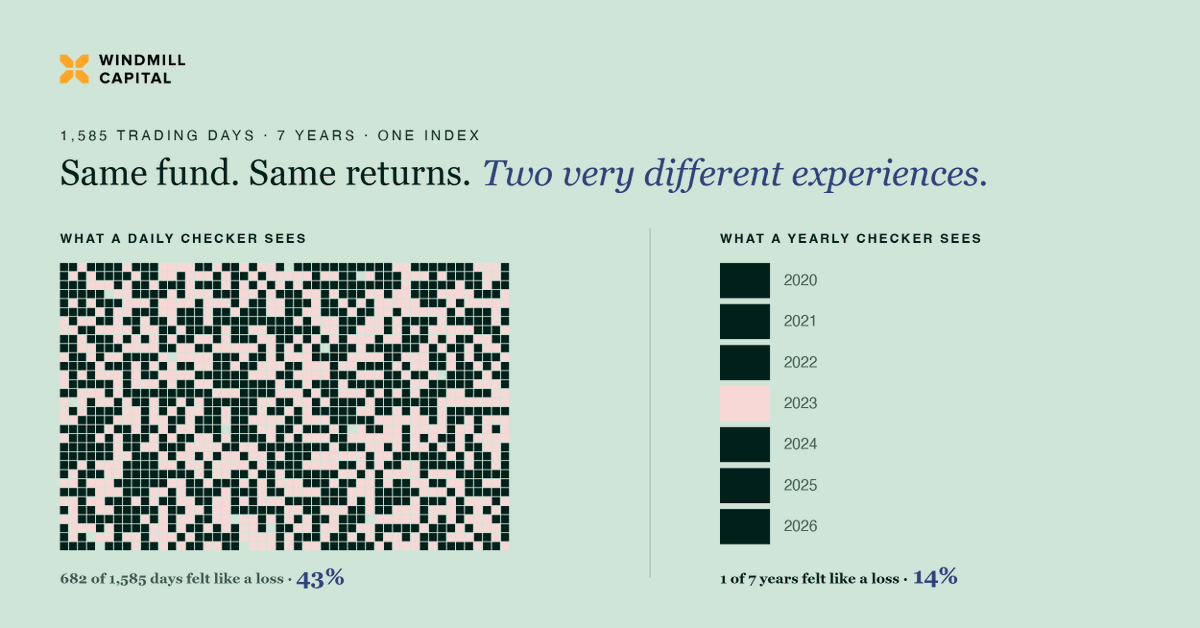

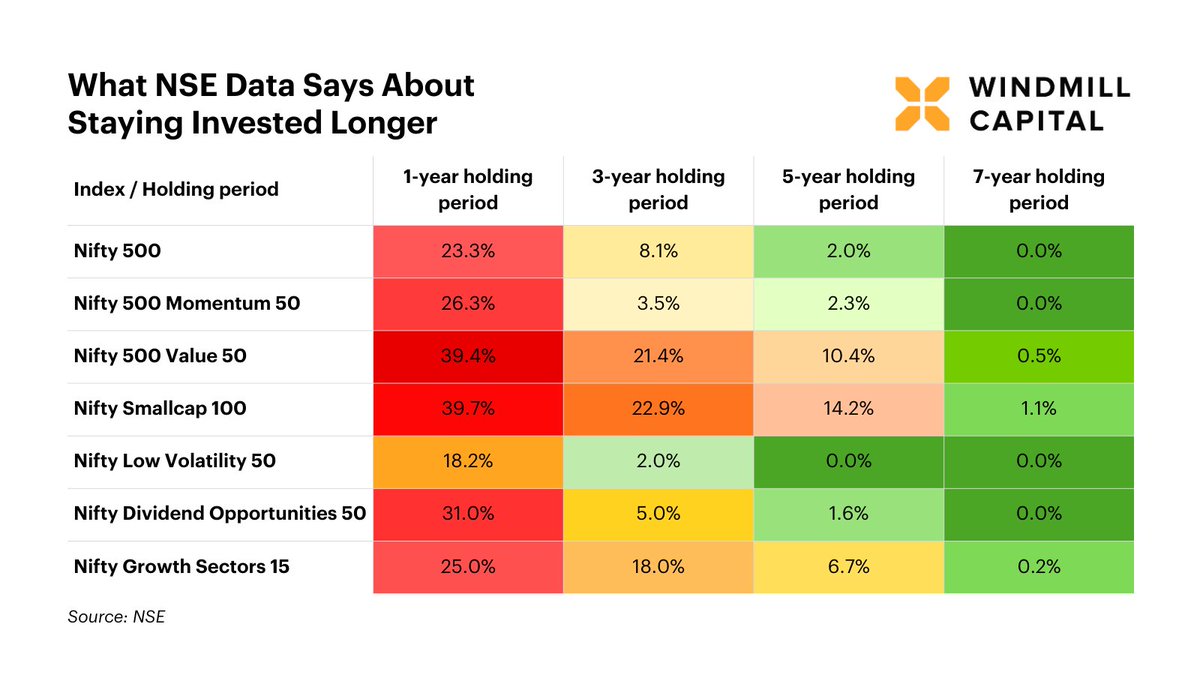

Same fund. Same six years. Identical returns.

One investor enjoyed the ride. The other found it unbearable.

The thing that separated them? A habit so small it sounds trivial.

1,585 days of Nifty 500 data tell the story 🧵

1

1

2

334

South Korea's top 5 stocks gained 152% YTD. Samsung and SK Hynix are riding the AI chip supercycle.

Taiwan & Korea's broader markets rose too: their entire supply chains plug into AI, not just one or two names.

The US, Germany, France? Only the names at the top. The rest shrank.

1

1

85

Nvidia alone: $5.21 trillion.

FTSE 100 (all of UK): $3.60 trillion.

CAC 40 (all of France): $2.90 trillion.

DAX (all of Germany): $2.32 trillion.

Europe's largest stock markets fit inside a single balance sheet.

1

1

63

This isn't a bull market. It's 100 stocks and 9,900 bystanders.

Durable as long as earnings hold. If AI capex stalls, the narrow leadership unwinds with nothing to cushion it.

Concentration is a feature right now. It could become a risk.

56

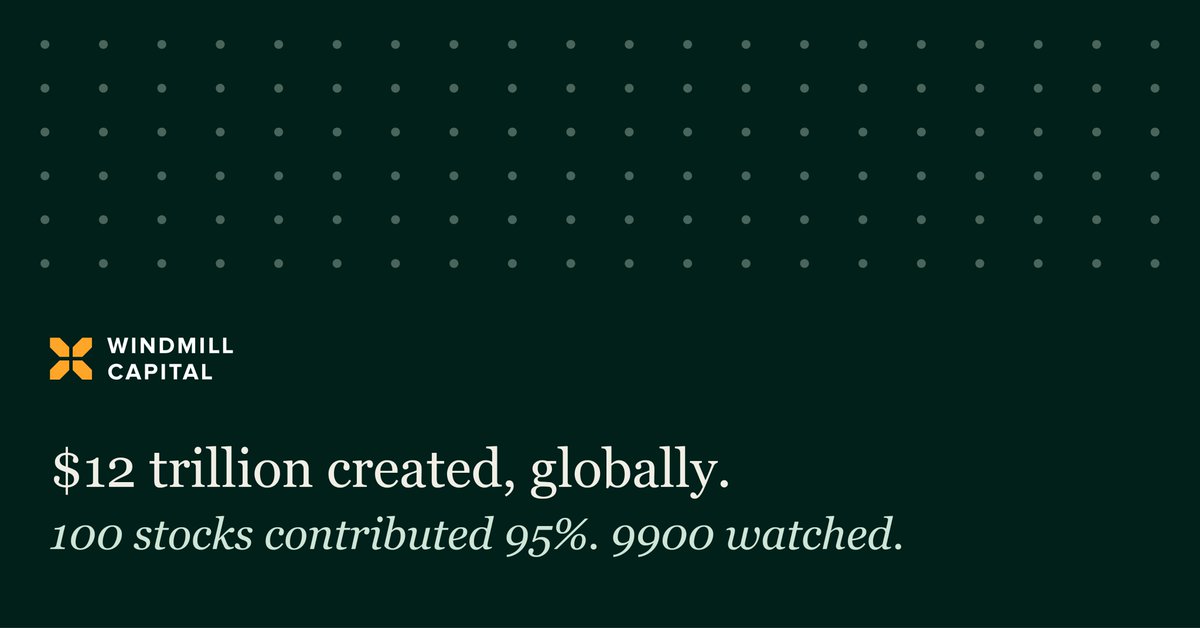

$12 trillion in global market cap was created this year.

100 companies accounted for $11.4 trillion of it.

The other 9,900? $600 billion. Combined.

1

1

396

The US market rallied. The average US stock lost value.

53 names added $7.4 trillion. The broader US market declined 3.2%.

The S&P gains you read about fit inside roughly 50 company names.

1

212

This isn't broad optimism. It's one theme: AI.

Information Technology alone drove 66% of all gains globally. Energy, industrials, and communications are in the top 100 because they power the AI buildout. Not because the economy is booming.

1

360

Same fund. Same six years. Identical returns.

One investor enjoyed the ride. The other found it unbearable.

The thing that separated them? A habit so small it sounds trivial.

1,585 days of Nifty 500 data tell the story 🧵

1

1

2

334

Psychologists call this myopic loss aversion.

Losses hurt about twice as much as equivalent gains feel good.

Even in a rising market, daily noise creates stress that frequent checkers absorb. Unnecessarily.

1

86

The lesson isn't to ignore your investments.

It's that discipline around how often you check can improve your investing experience.

Without changing your returns by a single rupee.

81

Every mutual fund investment is actually two decisions.

The first: which fund to buy. You research, compare, and choose.

The second: whether to still own it, three years later.

The first feels like a decision. The second feels like nothing, which is exactly the problem.

1

1

256

The shift that helps:

Stop asking which fund has done well.

Start asking which fund is positioned to do well from here.

It's a question you have to keep asking. Not once. Continuously.

1

1

126

Windmill Capital's Mutual Fund smallcases do exactly that.

A focused basket of 3–4 funds within a category. Monitored against ten factors with consistent predictive power. Rotated when the evidence shifts.

The second decision, handled: windmillcapital.smallcase.co…

84

India “fell” from #4 to #6 in global GDP rankings.

Sounds like bad news.

It isn’t.

Here’s what actually happened 👇

1

1

537

Even within GDP, the mix changed.

Some sectors look bigger.

Others look smaller.

That’s not decline. That’s recalibration.

1

123