Joined March 2023

- Tweets 706

- Following 491

- Followers 744

- Likes 820

78 Photos and videos

wumpy crypto retweeted

Happy saturday! Here's an interesting stablecoin farm from .@3janexyz . USD3 earns yields from their credit system and allows you to earn a scrape as well.

Mainnet:

USD3/USDC: 37.16%

You can one-click enter this farm on Yieldz. io !

Follow for future farms!

2

2

18

742

wumpy crypto retweeted

Jun 10

Team are friends of mine & have been working hard on @3janexyz for over two years. $JANE liquidity mining is finally beginning if you have an appetite for farming. Farm at your own risk. I am not farming rn but if I were I’d prob participate. Good project; good team. 🤝

3Jane is now open to the public

Mint USD3 to earn $JANE

Liquidity mining details below

9

3

95

18,101

Jun 10

now this, this is epic.

running USDC merkl campaigns for next 2 weeks minimum and aim to keep supply APY > 10% (excl. additional $JANE incentives)

Jun 10

Credit where credit is due.

The Clearstar 3Jane Ecosystem Vault is now live on @Morpho.

Users can deposit $USDC and earn yield on top of $JANE incentives from lending against @3janexyz $USD3

3

182

wumpy crypto retweeted

Jun 10

Cool video!

3Jane is now open to the public

Mint USD3 to earn $JANE

Liquidity mining details below

4

9

93

10,331

Jun 9

"1st phase of a broader $50M program..."

thats a $50m credit facility within the coming weeks, bringing scalable, future-backed credit to cryptonative rails :o

We are excited to announce that we have completed our 1st forward-flow loan sale of $8.5M with @3janexyz, a cryptonative credit protocol. This is the 1st phase of a broader $50M program and one of the 1st whole-loan purchases of a U.S. fintech loan book by a DeFi protocol.

2

6

635

Jun 1

imagine lending to a normal defi money market with 15k assets with capital equally distributed across each

even if 100 assets experience tail risk and go to zero (as commonly seen in defi), the overall pool remains healthy due to the level of diversification

in a similar manner, 15k consumer installment loans significantly compresses tail risk to a point where senior tranche only has impairment if we hit 2008 crisis levels of defaults

Jun 1

Great to see a solid team like @3janexyz thinking very differently from the 2022 cohort, where mostly all died the same way: concentrated single-name loans, originator marking its own book, and a thin or correlated loss waterfall (or none at all).

"Real world yield" that was just unsecured trust in a structured-credit costume.

Been spending time on 3Jane's ABF risk work and had a few back-and-forths with the team (s/o @wumpycrypto & @uhr3al). It's one of the more solid frameworks I've seen onchain.

And it starts from the failure modes, not the yield (altho yield is pretty juicy as well).

First, let's get into the core insight:

1) Consumer/SMB ABF isn't a credit-quality bet, it's a diversification one.

2) The ~18% gross on the underlying is mostly a complexity premium, not a credit premium.

3) Small borrowers pay it because banks abandoned small-ticket, short-duration lending after 2008, so their real alternative is a 24% card, not an 8% loan.

And the loss math is the part most onchain credit never had.

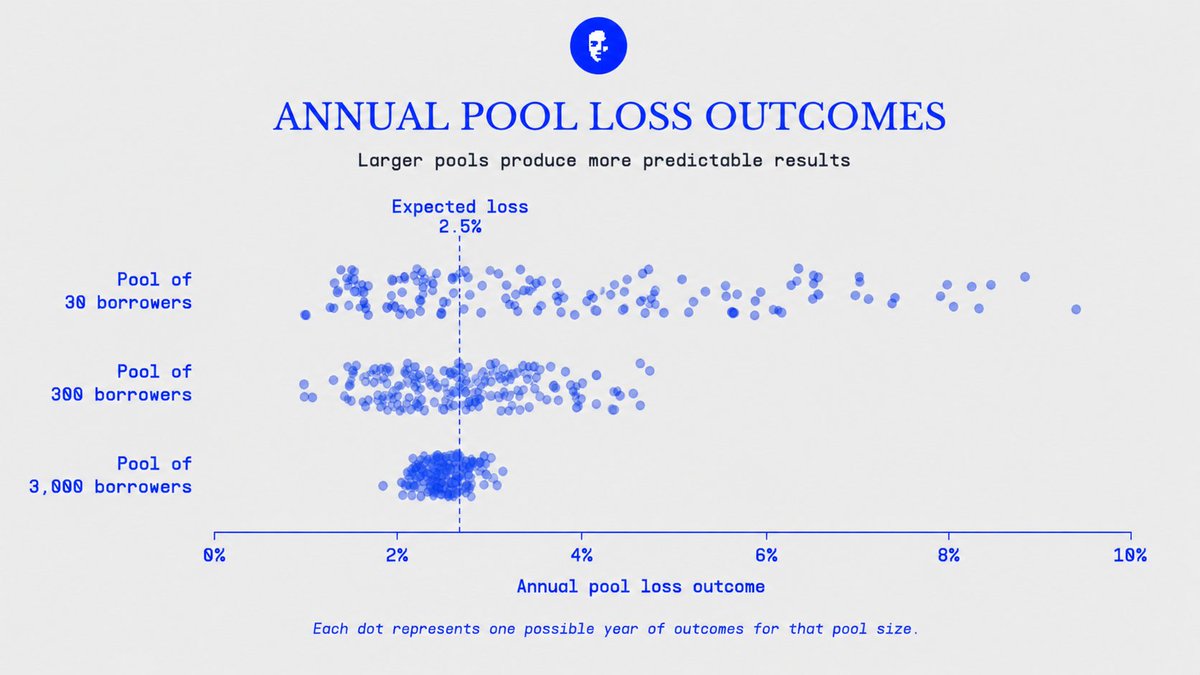

1) Spread the lending across thousands of tiny borrowers and the random blowups cancel out, go from 30 borrowers to 3,000 and the swing in pool losses drops from ~2% to ~0.2%.

2) The book they lend against loses ~1% to defaults over time; its worst-ever batch lost ~4.5%.

3) Senior holders don't lose a cent until losses hit ~19% of the pool.

4) And even modeled at 2008-level stress, the 1-in-100 bad year only reaches ~19.9%, right at that line.

This is the same kind of paper the bond market already rates investment-grade (think Affirm).

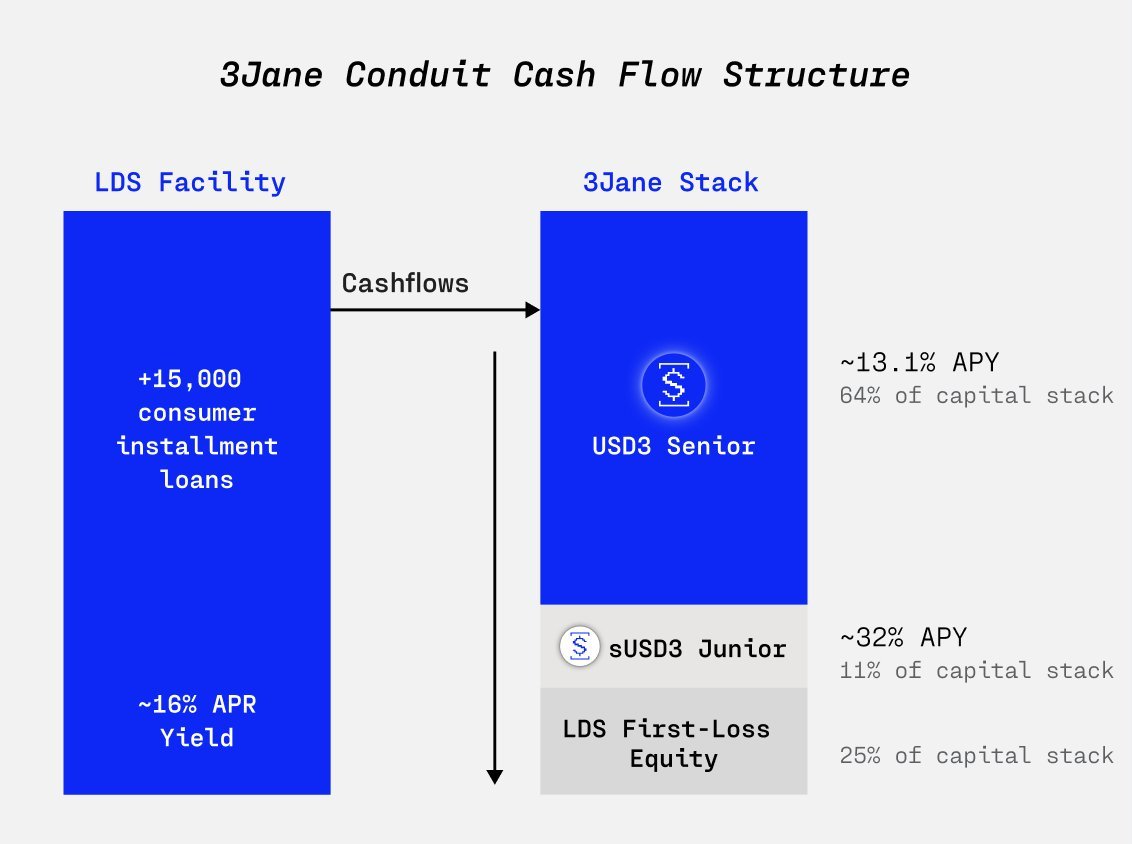

And today, they shipped the first live one. A $10M senior warehouse facility with LendSwift, a US consumer lender:

1) ~15,000 short-duration installment loans, ~16% APR underlying, 15% coupon

2) $3.33M first-loss equity from LendSwift (25% of stack), 75% advance rate

3) sUSD3 junior absorbs next: ~32% APY, ~11%

4) USD3 senior paid first: ~13.1% APY, ~64%, behind ~36% of the stack

5) blended ~16% net APY to suppliers, 12mo revolving / 6mo amortization

Two structural pieces seal it.

1) The loans sit in an SPV bankruptcy-remote from LendSwift's corporate entity. Lender blows up, collateral's still walled off and yours.

2) And repayments are swept into a DACA-controlled account, not the originator's. The structural control against diverting or commingling collections, one of the cleaner failure points in off-chain credit.

This is what real-world yield onchain should actually look like.

Not a wrapped T-bill.

Cryptonative dollars funding real US consumer credit through real securitization plumbing.

Compressing the bank-warehouse => forward-flow => ABS gauntlet into one programmable conduit.

Pretty sick.

Still a few things I want to work through with them, and will. But structurally, this is the most serious onchain credit I've seen in a while.

Crypto private credit never had a yield problem. It had a structure problem. Someone's finally building it.

2

1

8

1,199

3Jane has executed a $10M senior warehouse facility with LendSwift, a U.S. fintech consumer lender, to scale its loan portfolio

Funded by USD3/sUSD3 at a 15% coupon and secured by ~15,000 short-duration installment loans

Cryptonative capital now funds mainstream consumer credit

15

14

170

35,153

1/ Aave v3 mainnet, DeFi's largest lending mkt, has ~20k stablecoin borrowers

A credit card ABS can have up to 750x (~15m) the number of borrowers, enabling AAA credit ratings from agencies

A primer on USD3 & the law of large numbers as we deploy our first credit facilities

3

5

54

3,894

May 23

with current metrics, they’re giving away 2% of their TTS over the next 90 days to $1.2m excluding any rewards from their points campaign

one thing to note is that their token supply is completely unlocked at launch

with this in mind, even @ $10m FDV -> 66.6% APY from $TAN

with underlying yield from curve pool likely somewhere 10-30% APY

looks juicy, but i have to price risk of new CDP protocol & performance of $TAN to get risk-adjusted before deploying

May 23

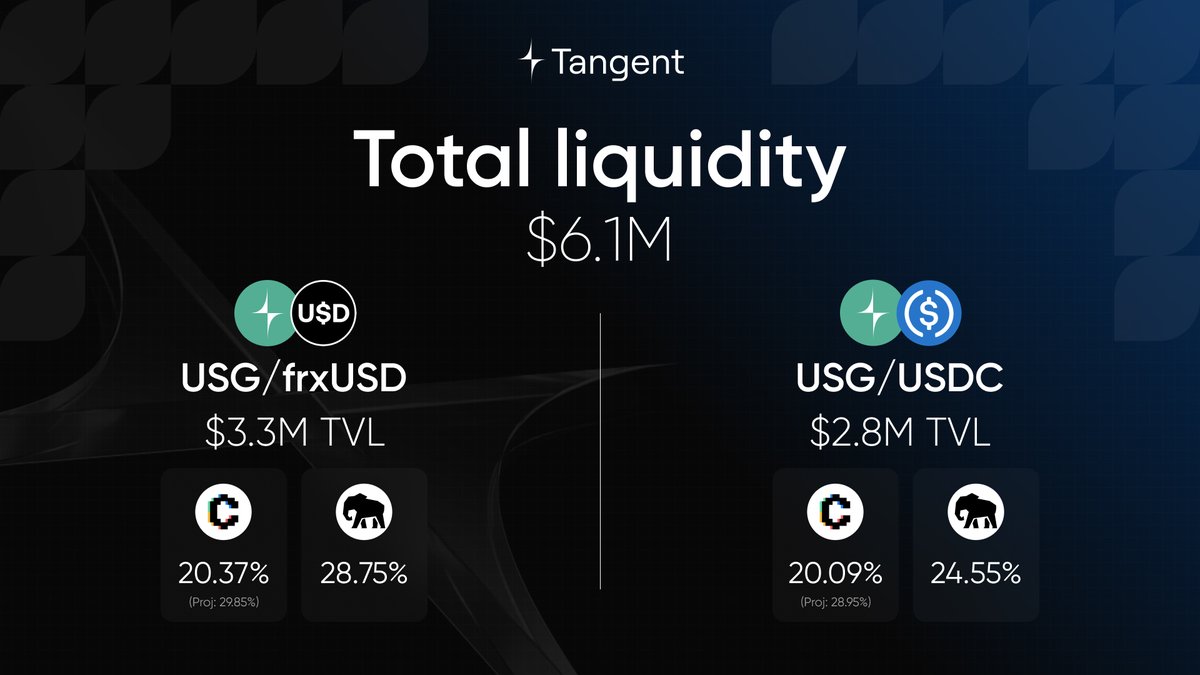

The Pre-Deposit campaign ends on Monday.

More than $3.2M were deposited in $USDC & $frxUSD.

Of these deposits, $1.8M are eligible for $TAN rewards, as the rest were deposited directly via Curve.

Ineligible LPs: withdraw and redeposit via our UI to become eligible. Withdrawals and redeposits must be one-sided.

Link below 👇

4

335

wumpy crypto retweeted

May 18

Private credit is usually shown as one clean RWA category. In practice, it is a mix of very different credit risks 📊

A 72-hour settlement liquidity facility is not the same thing as a 3-year corporate loan.

Invoice financing, receivables, SME working capital, trade finance, consumer credit. All of them sit under the same label, but they behave differently under stress.

This is why structure matters so much in tokenized credit.

Duration, repayment source, seniority, first-loss capital, and who controls the cash flow usually tell you more than the asset name.

13

9

59

12,657

May 21

"receivables financing is a tangible use case for defi to step in"

at 3jane, we're taking the first steps towards bringing receivables financing on-chain in a transparent manner.

through granular loan data & programmatic tranching, 3jane will disrupt capital markets

May 20

It’s been a little less than a month since my official start at @aave. A few quick observations:

1. DeFi is the use case for blockchains and is much more welcomed among institutions and fintechs than I even expected.

2. QC backed lending will provide the next growth spurt for DeFi lending - Aave will win here.

3. The old game that chains played for logo slapping is now happening to DeFi protocols. Astute players will price deals wisely and have a way to monetize or just watch their token go into oblivion. Lot of smoke and mirrors here.

4. Receivables financing is a tangible use case for DeFi to step in, really helps if the player is willing to put the full dataset on chain

5. DeFi lending will essentially redefine how prime brokerage works ($25B revenue industry)

6. Aave has work to do on BD side. It’s getting fixed and will be a sight to see.

7. @StaniKulechov is actually a beast - impressive ability to grind.

7

543

May 18

a defi lending equivalent of asset-backed financing:

traditional unsecured corporate debt -> lending to a pool of 5 collateral assets on an overcollateralized money market. one asset experiencing losses (or in defi, experiencing an exploit) suddenly means a large % of the pool is exposed to a distressed asset. recovery depends on bailouts / discounted value of assets (ex: resolv/stream/kelp). this is similar to a company defaulting on their unsecured corporate loan, where recovery is now contingent upon a discounted sale based on enterprise value.

even in money markets exposed to a wide variety of collateral (30 assets) - tail risk is wide and heavily correlated.

asset-backed financing -> lending to a pool of 1,000 collateral assets on an overcollateralized money market with:

- concentration limits (X% collateral assets cannot be correlated in losses / come from same issuer)

- performance triggers (Y% drop in price triggers early repayments from borrowers)

- eligibility requirements (what collateral is actually accepted)

one asset experiencing losses represents a smaller % of the pool, meaning tail risk compresses. recovery depends not on bailouts / discounted value of assets once losses already hit. instead, lenders are protected from underperforming assets BEFORE losses hit through early amortization (borrowers getting too close to LLTV), claims on cash flows from collateral assets (yield-bearing tokens have yield routed to repaying loan), and interest from the remaining pool.

tldr;

asset-backed finance equivalent in defi lending is:

- lending to 1,000 collateral assets (reduces tail risk)

- lending protected by performance triggers (underperforming collateral has exposure lowered)

Structured financing for fintech lenders (ABF) is a $100B asset class with virtually no history of being exported into crypto markets, despite consistently generating 10% returns.

Releasing a deeper analysis ahead of public launch:

➝ ELI5 warehouse loans & forward-flows

➝ Where the yield comes from

➝ Structured credit risk profile & loss distribution

Full post below.

3

315