18 Photos and videos

Rene retweeted

Feb 24

💰 Fundraising at the earliest stage — what do investors actually look for?

Join @xrendolf, CEO of @moonhillcap, as he shares how founders can prepare for idea & pre-seed fundraising — from team signals to investor expectations.

🗓 Feb 25, 11:00 AM (UTC 8)

🎙️ Set reminder: x.com/i/spaces/1qKDzPzWnQOJV…

For founders raising now — this is a must-join session. 🚀

1

1

10

1,501

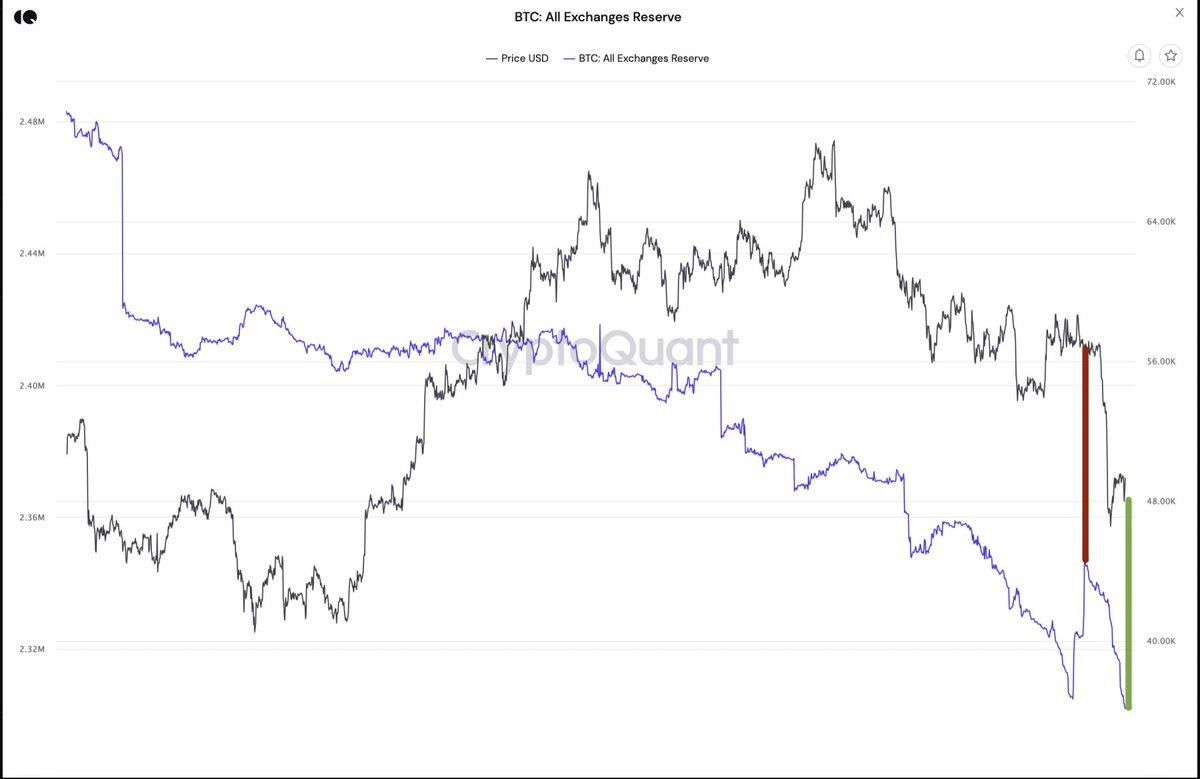

Japan just triggered a shift that could reshape global markets for the next decade and most people still don't care or think this is “just another stimulus.”

It’s not.

For 30 years, Japan quietly played the role nobody else could - the world’s supplier of nearly free capital.

When Japanese rates sat at zero, their insurers, pension funds, and banks had to send money abroad.

That single dynamic kept global borrowing costs artificially low, especially in the U.S.

Now that Japan finally offers a real return at home, the flow reverses.

And this change hits at the exact moment the world has the least buffer.

This isn’t an inflation story.

It’s the end of a regime.

Here’s what’s actually happening:

1. Japan stops exporting cheap capital

For decades, global markets relied on a constant stream of Japanese money:

Into U.S. Treasuries

Into European bonds

Into emerging markets

Into the yen carry trade

Even into crypto liquidity

That flow kept risk premiums artificially low.

Now Japanese yields are rising, and that same capital finds a reason to stay home.

The carry trade loses its anchor.

Liquidity quietly evaporates.

This alone would be disruptive.

But it’s only the first domino.

2. The U.S. suddenly has to absorb more of its own debt

If Japan steps back as a buyer, America loses a stabilizer it never acknowledged out loud.

Result:

Long-term rates become sticky

Financial conditions tighten

The margin for policy error shrinks

You can already see the Fed adjusting in real time:

ending QT early, loosening bank rules, and checking the plumbing to make sure nothing snaps when liquidity thins.

This is how regimes change. Gradually, then suddenly.

3. AI-driven deflation breaks the old fiscal playbook

The irony: Japan’s yields are rising without the inflation that normally justifies it.

Because AI is swallowing service-sector inflation.

Productivity is exploding exactly where prices used to be “sticky.”

Fiscal stimulus raises yields but barely moves nominal growth.

That’s the trap - borrowing costs rise, but the economy doesn’t.

This deflationary undertow is what makes the shift so dangerous for everyone else, especially the U.S.

4. Add tariffs and the picture gets volatile fast

Tariffs alone don’t cause a depression.

But they do raise costs, slow trade, and stress supply chains.

In the 1930s, this made a bad downturn worse.

Countries tightened simultaneously and pulled demand out of the system.

Today, global growth is already soft.

China is weak.

Europe is struggling.

U.S. consumers are slowing.

And Japan just stepped away as the global shock absorber.

Layer tariffs onto that?

You increase fragility at the worst moment.

5. The real risk isn’t collapse. It’s a world with no safety net

Japan moving out of its old role doesn’t guarantee a crisis.

But it does guarantee:

Less global liquidity

Higher real rates

Fewer automatic buyers

More pressure on deficits

More volatility in currencies and equities

Less room for error in policy

This is what a regime shift looks like.

Not panic, but fragility. Panic follows.

The world gets tighter, not louder.

6. Could Japan go back to zero rates? Yes, but only if things get much worse

Japan would return to the cheap money factory only in a global deflationary bust:

falling demand, collapsing trade, rising unemployment, shrinking prices.

Yields would crash for the wrong reasons.

A world where everything is contracting, not stabilizing.

The real message

Japan just signaled the end of a 30-year assumption:

that someone, somewhere, would always provide the liquidity the world needed.

That assumption is gone.

We’re entering a more fragile, less forgiving phase where:

capital is scarce

policy mistakes matter

liquidity buffers are thin

and AI changes the economics of inflation itself

Most investors are still positioned for the world we had.

Not the world we’re entering.

The shift has already started.

5

8

463

Rene retweeted

13 Oct 2025

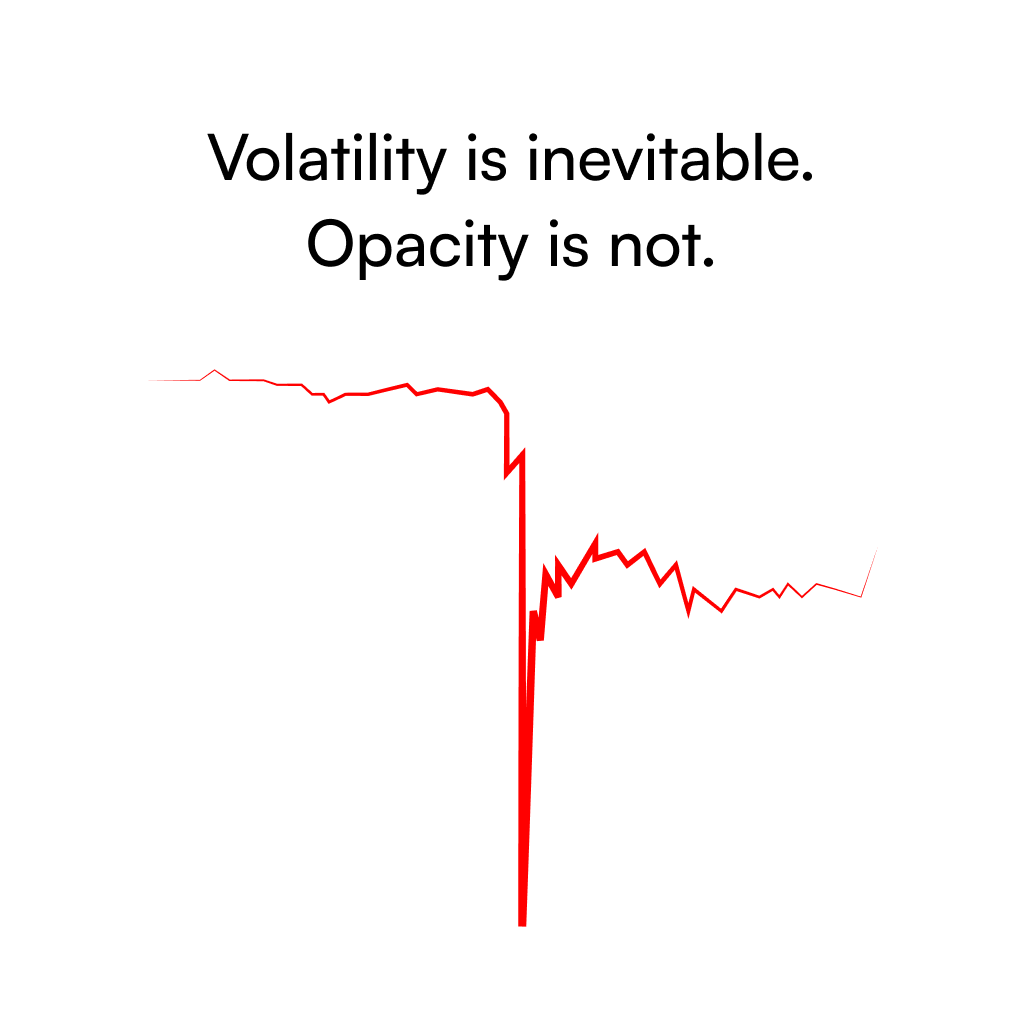

Friday’s market shock highlighted a structural weakness across digital finance: no one has real-time visibility into solvency. Here's a quick POV from the trenches, building infrastructure to solve this in a comprehensive way and hopefully soon set a new industry standard:

Protocols, oracles and risk systems all operate on delayed or assumed data about who holds what and who owes what. When prices dislocate, that lack of visibility turns volatility into systemic risk.

The problem isn’t the technology that moves assets btw - it’s the data that describes them. Current oracles quote market prices but cannot verify what those prices are backed by. For asset-backed tokens like stablecoins, RWAs, and liquid-staking assets, value depends on reserves, counterparties and redemption mechanics - details that price feeds don’t capture. So as a result, markets can react to noise while staying blind to real exposures.

What’s needed is continuous verification of financial truth = assets and liabilities proven cryptographically as they change.

Proof-of-Reserves was the first step in that direction, showing that assets exist and can be verified on-chain. But solvency depends on more than assets; it depends on obligations.

So what PoR should evolve into is Proof of Solvency, a model that extends to the full balance sheet, confirming that what’s held exceeds what’s owed and doing so in real time.

This shift matters A LOT because it turns solvency from an assumption into a verifiable data stream. Oracles can reference proven balance-sheet facts, risk engines can adjust exposure dynamically and auditors or regulators can see integrity without pausing the system.

That’s the direction @AccountableData is building toward: continuous verification as infrastructure. When markets can rely on live, verifiable solvency data instead of static disclosures, stability stops being a matter of luck or timing and becomes a property of the system itself.

Volatility will always be part of markets. But not being able to see what’s real doesn’t have to be 🤝

2

17

45

4,523

Rene retweeted

22 May 2025

#Token2049 Dubai 2025 Recap 🇦🇪

Token 2049 in Dubai managed to gather the most important people in Web3, sold out, and confirmed its significance. With over 700 side events, it was impossible to cover everything - we mainly focused on in-person meetings, so our feedback is definitely biased.

> Proper mixture of retail people with institutions creates a feeling of solid interest for the industry

> AI overtake - @0G_labs is present everywhere

> RWA follows - Plume gets recognition

> While interviewed, constantly getting questions about what will be hyped in the next 6 months

> Institutional capital flooding into bitcoin, stablecoins, and trading

> Market matures and has become a trader’s market

> Some VCs still allocating despite no real visible innovations or solid problem solutions

> A lot of VCs under water

> Majority of funds have been doing a lot of OTC deal

Full breakdown here: moonhill.capital/news/dubai-…

7

16

61

1,360

Rene retweeted

27 Apr 2025

Moonhill Capital is headed to #TOKEN2049 Dubai !

We’re looking forward to connecting with the sharpest minds in crypto - founders, builders, and investors. Catch us at these key side events throughout the week.

> Bybit demo day: lu.ma/08ju9340?tk=50yErk

> Sky Lounge by ATP, Kraken & ABEX: lu.ma/4fh555eb?tk=0PfLf3

> STXN Investor VIP Dinner w. Tane Labs & HackVC lu.ma/2tum18ga?tk=xikiOH

Attending @token2049? Let’s connect — shoot us a DM or come say hi at the events! Big week ahead.

2

11

54

995

Rene retweeted

23 Apr 2025

Meet our GP, @xrendolf in Dubai. He will be speaking at the Tokenized Capital Summit during #TOKEN2049 on April 29.

Expect sharp insights and fresh alpha — catch him there! @GammaPrime_Fi

2

12

50

832

Rene retweeted

21 Apr 2025

9

4

14

1,439

Rene retweeted

18 Apr 2025

How Do First-Time Founders Raise $10M In Just 30 Days? Join us AMA on 📅 April 21st at 11:00 UTC to find out!

🎤Speakers:

・Laura K. CGEO @Gate_io & Principal @gate_ventures @laura_gateio

・Benjamin Rameau, Angel Investor @Permaoptimist

・Rene Darmos, Managing Partner at Moonhill Capital @Xrendolf

・Andres Menese, Founder of Crypto OGs @Andreswiftv

・Elliot Hagemeijer, CEO at Decubate @ElliotMeijer

・Gaurav Dubey, Chairman at TradeDog Group @GauravDubeyLive

🎧 Set a reminder & tune in! twitter.com/i/spaces/1rmxPyD…

6

16

34

16,703

Rene retweeted

4 Apr 2025

Moonhill Capital is heading to #Web3Festival Hong Kong (April 5-13)!

We look forward to connecting with visionary founders, investors, and industry leaders. You can meet us at these key side events:

> 8/4 Liquidity by @LTP_primebroker: lu.ma/oqmyj67h?tk=WN4GT0

> 9/4 Crypto Forum by @ambergroup_io: lu.ma/MetaEra?tk=OaWlhF

> 10/4 ETH Asia: lu.ma/ETHAsia?tk=1qegaz

If you're attending @festival_web3, let’s connect! Send us a DM or meet us at these events

9

10

49

692

Rene retweeted

30 Mar 2025

#ethdenver 2025 was smaller, quieter, and heavily focused on builders. Some founders showed up, but many just stayed home. Now that the dust has settled, here’s what actually mattered:

> Smaller crowd, lighter energy—many builders didn’t show up.

> ETH underperformance is obvious—most builders are bearish and don't hide it

> Restaking fatigue— Babylon & BTC restaking gets attention but feel forced.

> Berachain dominates—the hype machine is working

> Crypto x AI is the new norm—most projects are still early.

> Mantle stood out quietly – @sozuhaus had strong vibes, and their treasury is being run like a real business

> Too many side events – Many were half-full, and others were overcrowded. Scheduling was chaotic.

> Cosmos losing teams to Ethereum/Solana .

> Marketing agencies everywhere, but only a few deliver.

> Teams want users, not just capital—frustration with adoption grows.

> Clear communication is rare—many projects still can’t explain what they do

> Hyperlane gaining traction over Layer Zero —interoperability preferences shift.

The bigger picture:

There’s too much noise, and not enough traction. People are tired of recycled narratives, and restaking isn’t moving the needle anymore. Attention still matters (Berachain proves that), but hype alone isn’t enough. AI is here to stay, but only real usage will separate winners from buzzwords.

For the full breakdown, read our full report here: moonhill.capital/news/eth-de…

ALPHA tip: innovations are coming from @OnePieceLabs on the pic, where @xrendolf had a chat with @sosovalue & @itplaysout, worth watching OPL !

8

15

60

1,697

Rene retweeted

21 Mar 2025

Moonhill Capital hit Consensus HK 2025 — plenty of capital, but conviction is missing.

Key Takeaways:

> AI – Serious interest in human-like AI and digital ID projects

> DePIN, RWA, stablecoins – Strong plays, attracting real capital

> BTC L2s – Back on the rise, institutional money flowing in

> Sentiment – Surprisingly bullish despite ETH and alts underperforming

> Aptos – Moving away from retail, building ties with governments

Challenges & Gaps:

> Retail is missing – Old retail got smarter, new retail isn’t showing up

> Restaking and shared security – Awareness is low across the board

> AVS confusion – Teams still don’t know if they should decentralize

Full breakdown of what’s happening behind the scenes: moonhill.capital/news/consen…

12

18

58

828

Rene retweeted

17 Feb 2025

🔥Moonhill Capital x OnePiece Labs: Empowering Web3 Founders!🔥

We're thrilled to announce our strategic partnership with @OnePieceLabs, aiming to empower Web3 founders and drive innovation in the decentralized technology space.

This partnership brings mutual benefits, giving incubated projects direct access to our network of:

✅VCs

✅Market Makers

✅Strategic Partners

✅Decentralized Infrastructure through MHC Labs

Moonhill Capital will enhance our deal flow with early-stage projects incubated by professionals, setting them on the right path to Web3 success.

Excited to hear more? Our CEO @xrendolf will be speaking at OnePieceCon during ETHDenver 2025, diving into transformative trends in AI & ConsumerFi.

Visit us at @EthereumDenver and talk to us about the future of Web3 along with top founders from @0G_labs!

More details:

🔗 Partnership Announcement onepiecelabs.xyz/blog/onepie…

🔗 Denver Luma Event: lu.ma/OPC2025FEB

🔗 Notion Summary: onepiecelabs.notion.site/Str…

14 Feb 2025

🔥OnePiece Labs x MoonHill Capital: Empowering Web3 Founders!🔥

We’re officially teaming up with MoonHill Capital to take our accelerator to the next level. 🚀

@moonhillcap isn’t just another investment firm—they’re deep in the trenches of DeFi, tokenomics, market-making, and validator infra. With a network spanning Polychain, Spartan, TRGC, and top global accelerators, they bring the kind of hands-on expertise that Web3 founders actually need.🧩

What this means for OPL startups:

✅ Better token models & liquidity strategies – No more guesswork on market-making & tokenomics.

✅ Access to top-tier investor networks – Fundraising? You’ll be talking to the right people.

✅ Decentralized validator infra & security – Supporting sustainable blockchain growth.

✅ Advisory from industry veterans – From talent sourcing to exchange listings, we got you.

If you’re building in Web3, AI, or DeFi, this is your chance to level up with the best in the game. 🌍🚀

We’re seeding the future of Web3—are you in?

🔗 More details: onepiecelabs.xyz/blog/onepie…

5

33

59

1,510

Rene retweeted

13 Feb 2025

🔥 VC Alpha Incoming: OnePieceCon Speaker Reveal!

We’re hyped to welcome René Darmoš, Managing Partner at Moonhill Capital, to OnePieceCon FEB2025 @ ETHDenver! 🚀

@moonhillcap is seeding the future of Web3, managing digital assets with a long-term vision and deep market insights. @xrendolf will share hard-hitting investment trends and what it takes to back the next wave of billion-dollar protocols. 👀

📅 Feb 28, 2025 | Denver, CO

🎟️ Lock in your spot: lu.ma/OPC2025FEB

Builders, founders, and investors—this is your chance to tap into next-level Web3 alpha. Don’t miss it! ⚡

6

9

3,169

Rene retweeted

12 Feb 2025

SuperGG - Fundraising Risks & Milestones for Web3 startups! x.com/i/broadcasts/1lDxLzdQR…

7

19

1,832

Rene retweeted

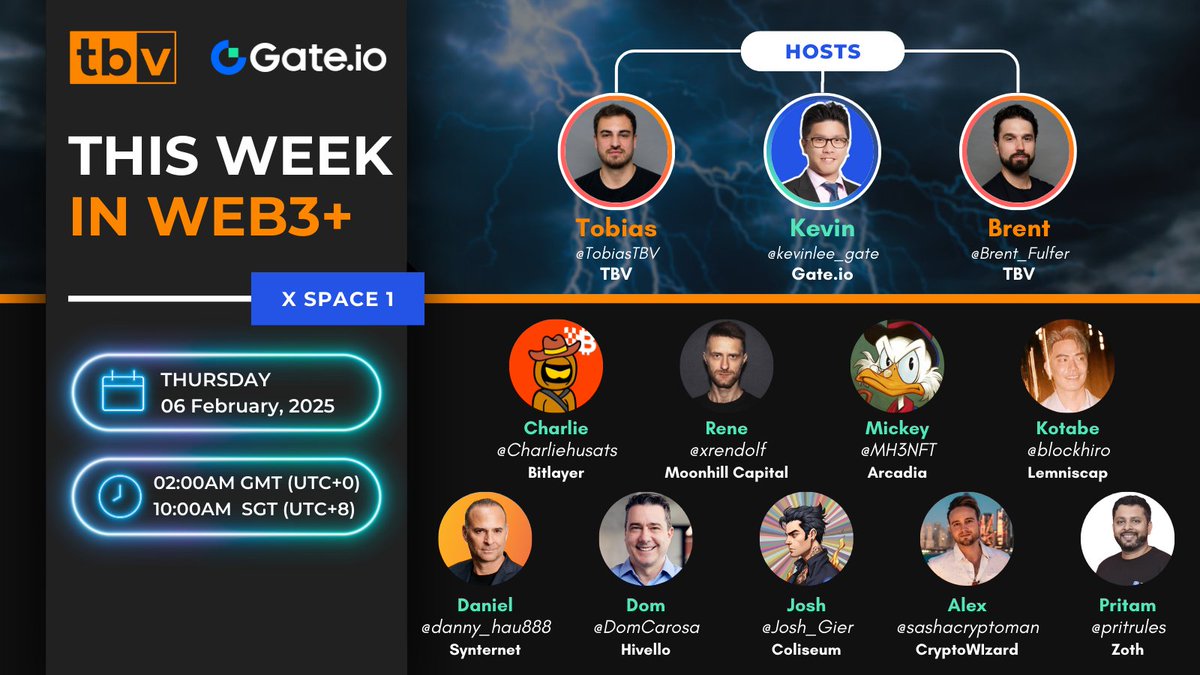

5 Feb 2025

Join @tbvxyz & @gate_io's 1st #XSpace on ‘This Week in Web3 ’ as we unpack the week’s news with hosts @TobiasTBV @Brent_Fulfer @kevinlee_gate alongside a great mix of speakers 🔥

Happening Soon ⏱ Feb 6th | 10 AM GMT 8 | 2 AM CET

See you here: x.com/i/spaces/1ZkJzYMBqNyGv

8

6

54

17,062

Rene retweeted

31 Jan 2025

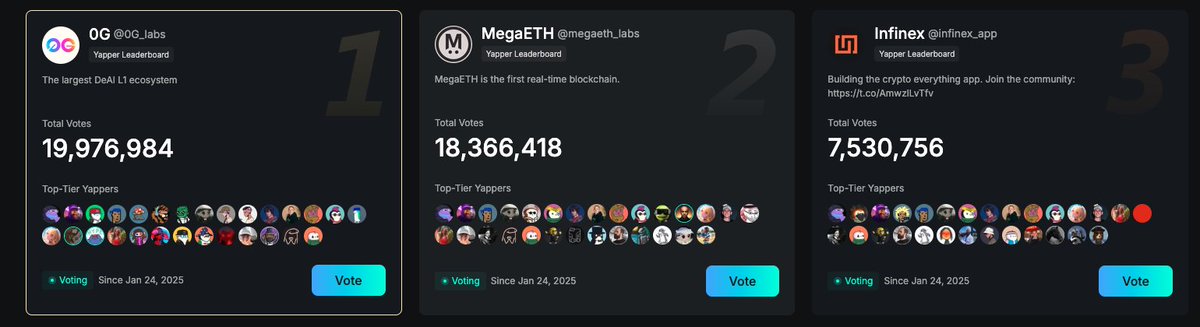

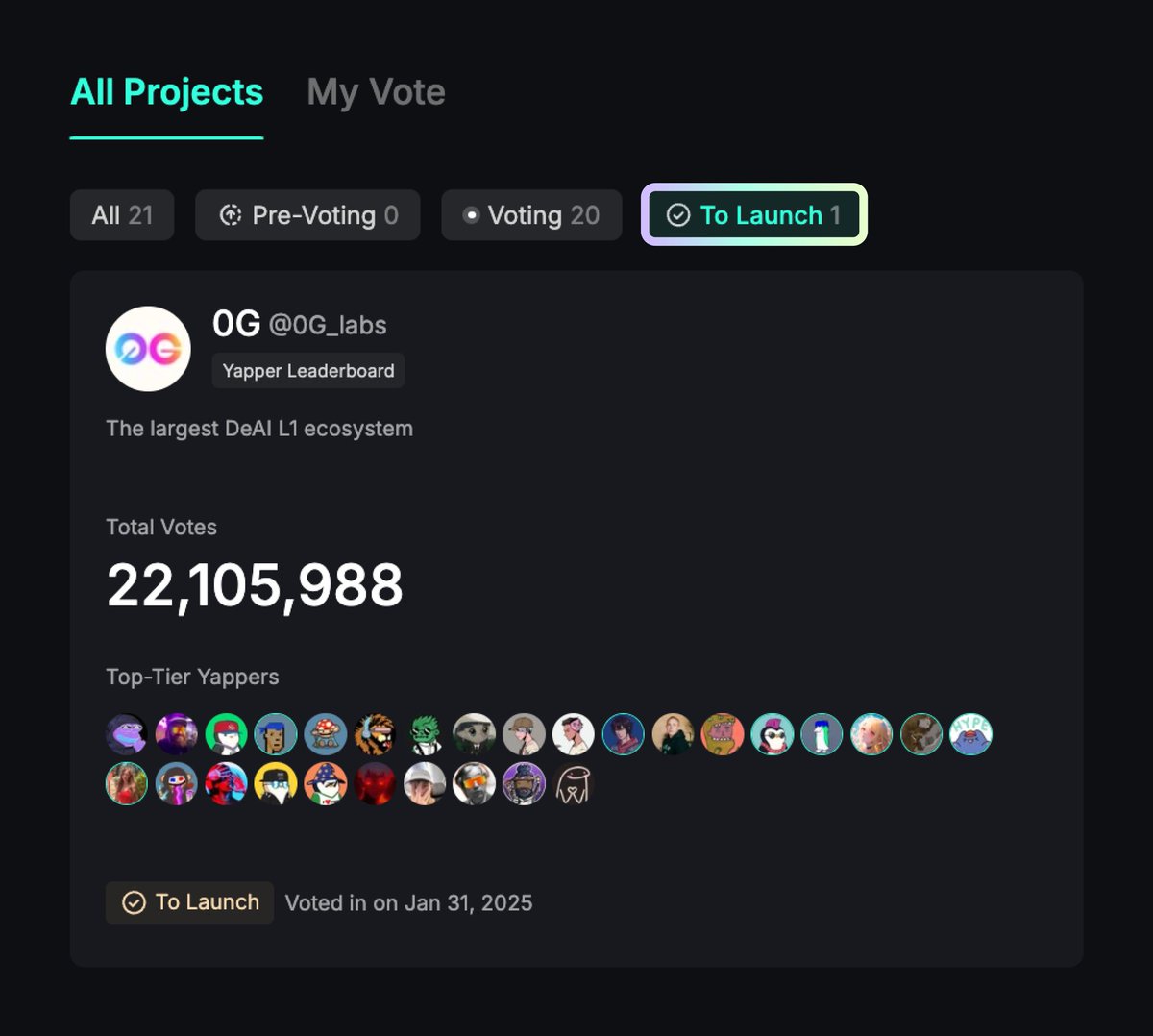

The first Yapper Launchpad project has been decided!

@0G_labs got the most votes from all of you, and will now have a Yapper Leaderboard in 7 days time.

So what happens next? Well all the projects remain for the next selection.

As planned, going forward, every Mon, Wed & Fri the next projects will be selected!

As communicated before, every vote is locked up for 7 days, after which you can reassign at any time (or remain).

If you voted for 0G, your vote will automatically be returned 7 days after it was cast.

If you voted for another project, 7 days after it was cast, you can reassign at any time.

Overall - if your favorite project didn't get selected today, it's far from over 🫡

593

136

1,055

198,205

Yap early, yap only, yap often.

@_kaitoai is connecting AI, attention and capital with Yaps.

Just claimed my social card and I'm accumulating Yap points in real-time.

Claim yours 👉 yaps.kaito.ai/referral/93072…

& vote for @0G_labs , which is oc leading :)

yaps.kaito.ai/connect/172224…

6

132

Rene retweeted

20 Jan 2025

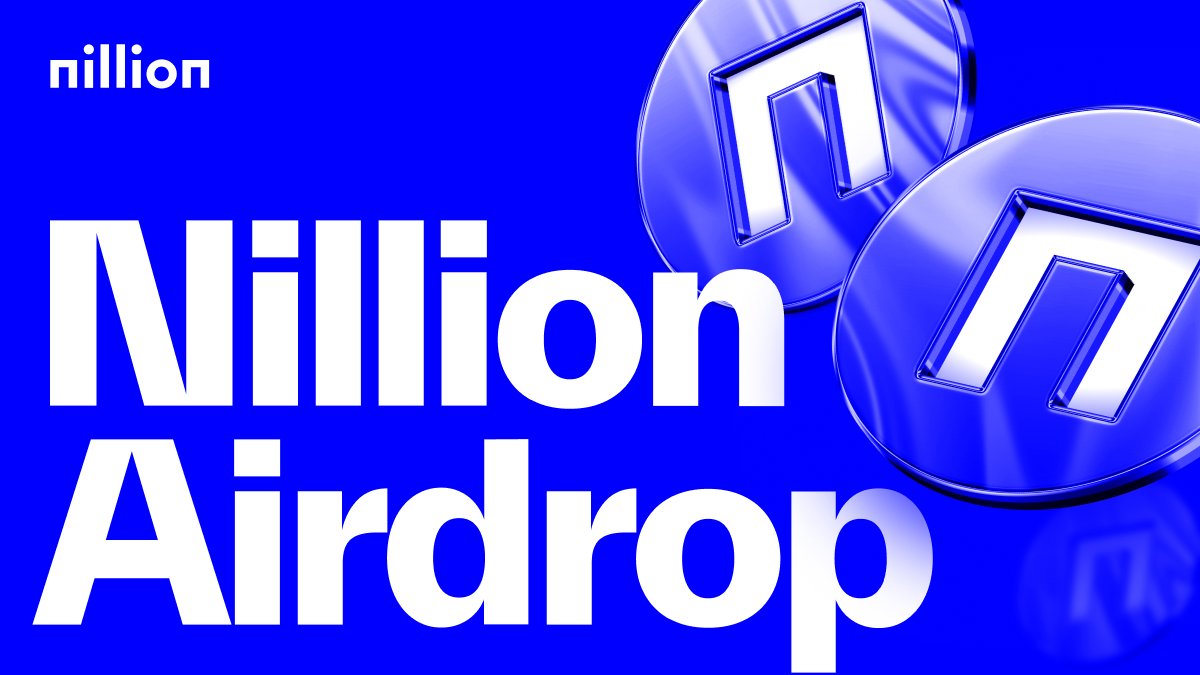

We are thrilled to support Nillion as they take a major step toward decentralization with the NIL Airdrop program!

With 75M tokens allocated to the community, this initiative empowers supporters, builders, and contributors ahead of the Alpha Mainnet launch. Exciting times for the future of privacy and Web3! 🚀

#Nillion #Web3

As Nillion approaches its third phase with the Alpha Mainnet launch, we’re thrilled to announce the NIL airdrop.

NIL airdrop is our way of rewarding the Nillion community members and early adopters, complementing our Community Round in 2024.

Here’s the details 🧵

8

45

92

2,225

Rene retweeted

31 Dec 2024

Accountable Secures $2.3M Funding to Enhance Transparency in Crypto Lending and DeFi Platforms.

With the power of zero-knowledge proofs, we’re solving the balance between privacy and transparency in the lending markets.🌐

🔒 Restore trust with real-time, verifiable financial reports.

💡 Enabling secure, undercollateralized lending to drive a more inclusive #DeFi ecosystem.

Our mission: A more transparent, efficient, and privacy-preserving financial future for all.

117

252

727

87,401

Rene retweeted

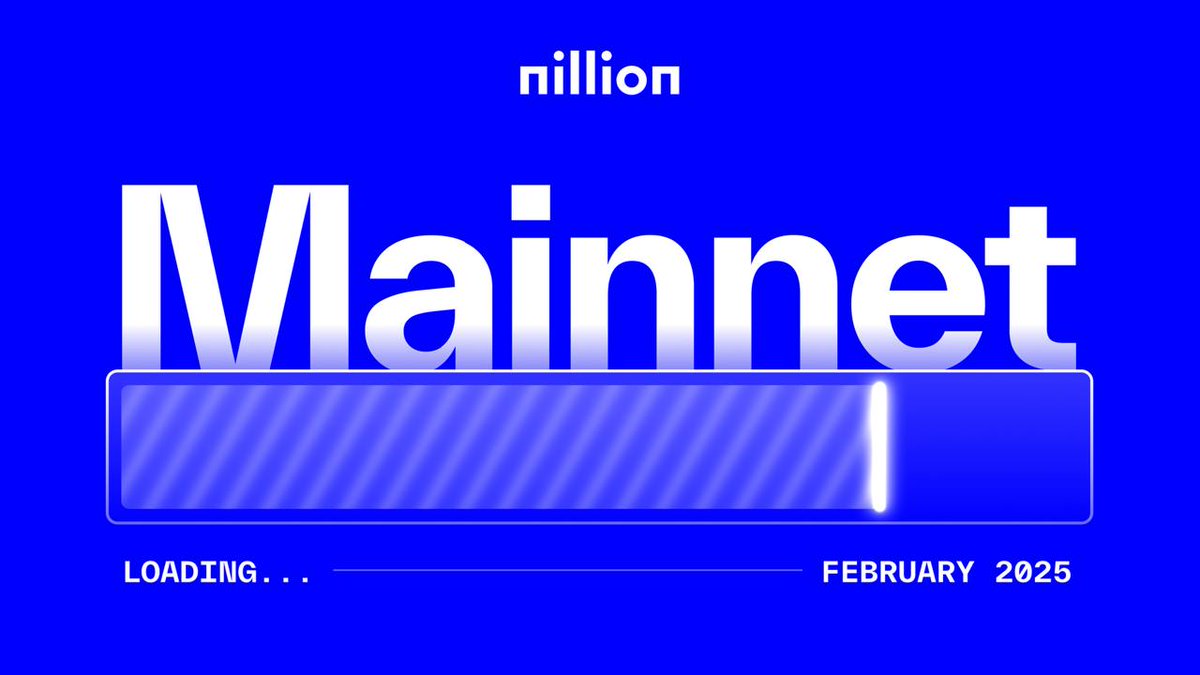

20 Dec 2024

Different privacy tech solve different problems.

Nillion is building the only system that will power them all.

MAINNET LAUNCH 2/25

Been supporters since 2021.

Proud on the great team.

Make privacy great again!

&

Don’t trust, verify

Nillion mainnet.

Every revolution has its genesis moment.

February 2025.

11

61

86

1,829