Mining analyst with @AdamasIntel

Joined December 2016

- Tweets 1,532

- Following 651

- Followers 1,321

- Likes 5,031

283 Photos and videos

Primero, an Australian EPC mostly known for building reliable spodumene concentrators, also has a conceptual potassium-chloride atmospheric leach technology which has $PMET interested. Shaaki is undefeated in optionality. Plug an electric calciner on this and it could work well👀

Jun 14

PMET has completed a concept study looking at a potential longer-term refining pathway at Shaakichiuwaanaan — converting spodumene concentrate into battery-grade lithium carbonate directly at site.

Key points:

• 7 processing options reviewed

• Primero’s ALi® atmospheric leach process selected as the preferred pathway for further study

• Bench-scale testwork produced 99.8% Li₂CO₃ battery-grade lithium carbonate

• Overall process recovery of 92.5%, including calcination

• Potential to reduce logistics intensity by shipping a higher-value lithium product instead of moving large volumes of concentrate

• Could leverage Québec’s low-cost renewable hydro power, including potential electric calcination

Full NR here: pmet.ca/news/concept-study-i…

$PMET $PMT.AX

2

20

1,422

High conviction advisory comes from countless hours of grindy research, analysis, and experience. It always produces winners and losers, but therein lies the value. Thanks @RKEquityRocks for the opportunity to highlight some of our methodoligies used in the lithium sector

China inventories are moving. So is the lithium debate

@zempheth argues the market may still be tighter than the restart headlines suggest

• China inventory noise

• DLE execution risk

• Quebec hard rock

• Vulcan, Q2 and project quality

• Restarts, delays, cycle timing

📺: youtu.be/9P1NTz2oUXw

3

1

17

1,861

imo, this is what excited $PLS to go after Latin Resources in 2024. Pilgan now achieves consistent ~75% Li2O recovery even when processing high contact ores, thanks to xrt ore sorting

youtube.com/watch?v=fWHqsBil…

20

1,714

Christopher Williams retweeted

Jun 3

Each taking their own path. It's not a story of 'one or the other' #Lithium

$QTWO.v : "Big, open pit, good location, easy sell (story/asset)"

$PMET.TO : "Multiple flowsheets (revenue/interest diversification), further advanced, A-Team"

May 7

It's been a good month . One of discovering new heights and another of rediscovering previous ones ..:)

Congrats to the longs on these two. Been a ride.

$QTWO $PMET $PMT

1

4

44

4,391

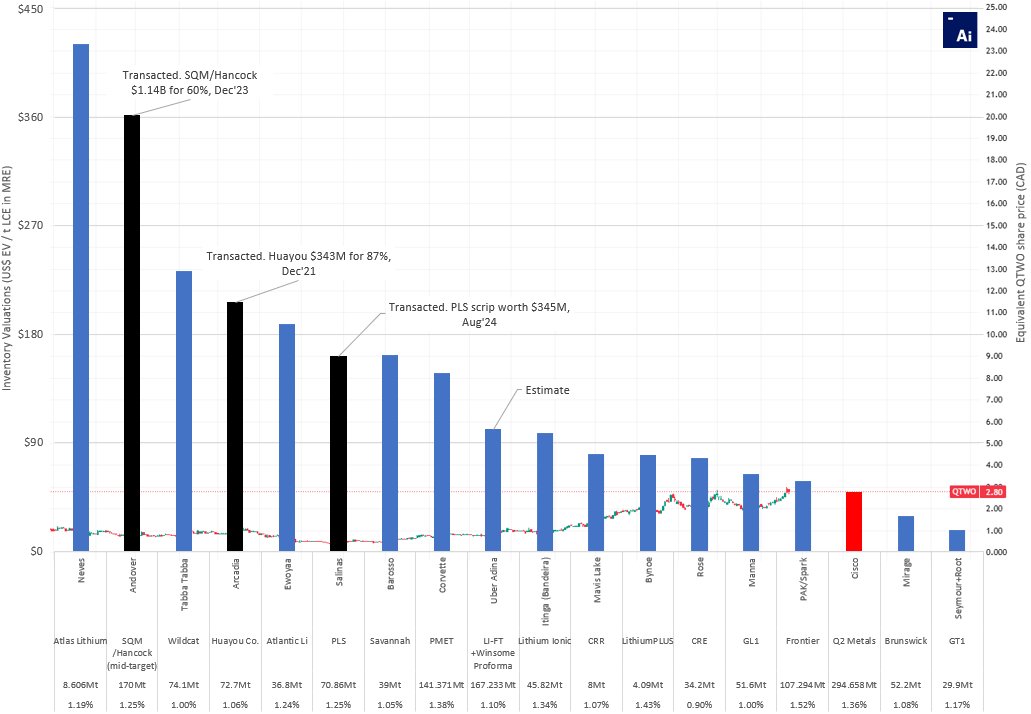

$QTWO pick your comp, pick your target

#inefficientmarkethypothesis

$QTWO price equivalents of spod peers, aligned with their inventory valuation (EV/t LCE in MRE)

Yes, mixing advanced projects with early, but nonetheless a powerful perspective for what possible for the #4

ie. $20 QTWO = SQM/Hancock - Andover transaction at the pre-MRE stage🤯

2

2

17

4,396

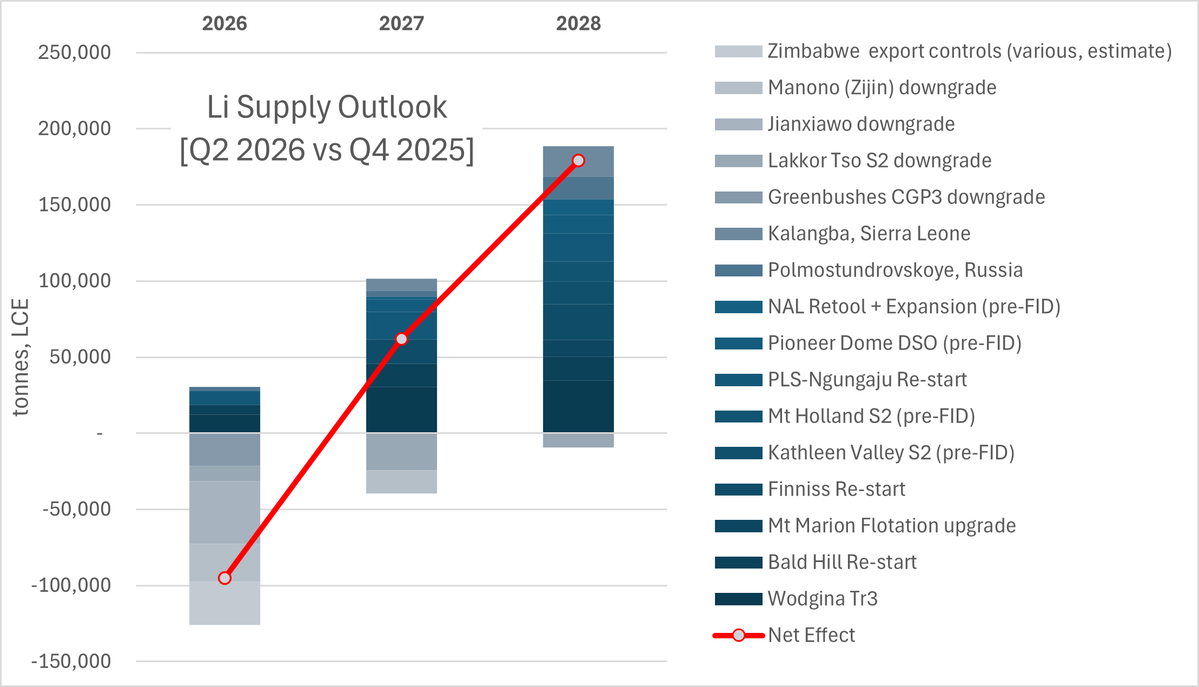

Lithium production delays nullifies Aus Can spod re-starts and expansions until 2028.

Meanwhile ESS upside suprise more than negates EV dissapointments, imo

In summary, without even consulting my primary model, I remain bullish here.

Full writeup here:

linkedin.com/posts/cdw4870_i…

6

10

62

7,615

I recall not too long ago Australian spodumene was considered dead. Now, Zimbabwe is shifting goal posts and Nigeria wants to be a fast follower but it’s too disorganized to be taken seriously. Meanwhile China continues offtakes with Australia, and appetite for more is insatiable

May 31

Zimbabwe's billion dollar initiative to lure Chinese capital into processing #lithium at home.

Firstly, Zimbabwe banned the export of raw lithium and "unbeneficiated" minerals, resulting in nearly $1 billion in investments for local processing plants.

As a result, Chinese companies particularly the likes of Huayou and Sinomine have led investments and construction of several lithium sulfate processing facilities.

The first lithium sulfate shipment from Zimbabwe was exported in April. See photo below.

--->“This inaugural shipment represents the first lithium salt ever produced in Zimbabwe and across Africa, marking a major step forward in regional mineral beneficiation and industrialization.”- Huayou’s Zimbabwe unit

Zimbabwe is now flexing their weight when it comes to the global lithium supply chain.

According to Business Insider Africa lithium sales have surged in 2026, with volumes rising 2% and value increasing 106% year-over-year, highlighting strong global demand and government policy impact.

9

1,354

$WR1.ax @ 52c trading -16% discount to $LIFT last close $5.7 even after the positive vote, pending courts final approval.

3

1

6

2,987

Exciting news for the Northern Territory and to all who stand to benefit from ex-China NdPr oxides $ARU #CUintheNT

1

7

794

DS💯on the money, once again.

At spot sulfur, Thacker, or any clay project for that matter, is now looking at an additional $6k/t LC above and beyond the assumed $6k/t LC OPEX in studies, so $12k/t LC OPEX.

Consider too, clays require ~$20k/t profit to achieve a 20% return $LAC

May 18

With sulfur prices this high, the costs of processing lithium clays, oxide ores (copper, nickel, REEs) is going to BLOW OUT.

The smelting of sulphide ores produces sulphuric acid as a byproduct. The processing of oxide ores consumes sulphuric acid.

#LAC's Lithium America's Thacker Pass for example is going to do 40,000 tonnes per year of carbonate in phase 1. They've stated a 2250t/day sulphuric acid plant, which is 821,250 tonnes of acid per year.

So each tonne of carbonate could require 20.5 tonne of sulphuric acid per tonne of Li₂CO₃. That's about 6.8 tonnes of sulphur.

Using the Chinese futures price of US$1050t, that's US$7140t worth of sulphur per tonne of Li₂CO₃.

#LAC will most likely source their sulphur internally. American fertiliser companies during Q1 paid US$488/t for molten sulfur, which is $3318 per tonne of Li₂CO₃. I'd imagine its higher now looking at the Chinese price.

Spodumene uses 50-60% less acid. Food for thought. I love spod.

1

18

3,191

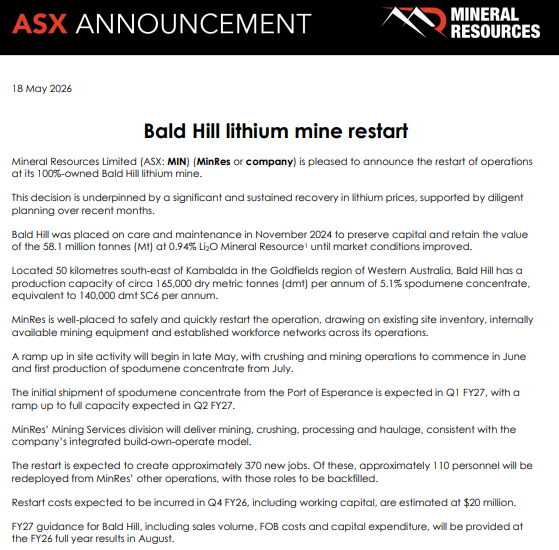

$MIN.ax Bald Hill incentivized back into market. Quick restart - aiming for July, 165ktpa at 5.1% Li2O capacity by Q4 2026

clients3.weblink.com.au/pdf/…

1

21

4,338

RE: Andover “it is against that backdrop of improved commodity prices that the lithium mine is now going ahead.”

Not true. There’s a team in Perth that have been driving this project forward since the day 1. This isn’t some marginal project we’re talking about here.

Andover begins its journey.

Gina Rinehart plots new Australian lithium mine as prices soar afr.com/companies/mining/gin…

1

1

10

1,915

Christopher Williams retweeted

May 15

Recently, our CEO @KenBPMET sat down with the @TMXGroup for a quick project update interview, discussing permitting steps, the importance of caesium and funding. You can watch it here: youtube.com/watch?v=Dm4oPyGR…

$PMET $PMT

11

32

4,167

From what I understand this is a re-tooling of BlueOval EV cells to ESS. Have not seen an official announcement on this yet but I hear rumours PowerCo’s St Thomas cell plant in Ontario is also pivoting. Peak pessimism in North America on local EVs?

May 11

Ford has officially introduced Ford Energy, following in the footsteps of @Tesla.

"Ford Energy will provide U.S.-assembled LFP prismatic battery energy storage systems for a variety of uses. Units are planned for availability beginning in late 2027."

Specs:

• 2-hour & 4-hour configurations

• Rated Energy: 5.45 MWh

• Cell Capacity: 512 Ah

• Cell Dimensions: 73 × 275 x 210 mm

• Voltage Range: 1040 - 1500 VDC

• Dimensions: 20 ft standard container

• Product Weight: ~43.5 tons

• Aux. Power Load: Max 37.5 kW

• Noise: <75 dBA

• Cooling Method: Liquid Cooling

• Corrosion Protection Level: C5

• Ingress Protection (IP) Rating: IP55

• Operating Temperature: -35°C to 55°C

• Operating Altitude: ≤ 4000m (No Derating)

2

789

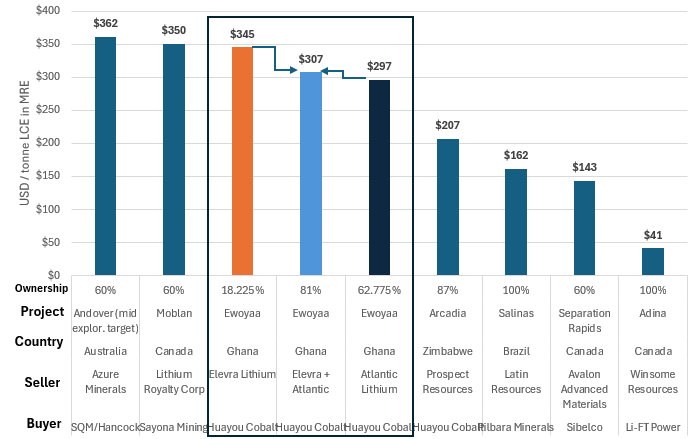

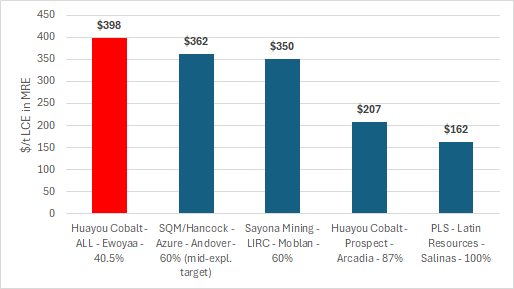

Update on hard rock Li valuation chart as $ELV to sell its Ewoyaa interest to Huayou Cobalt for US$71M. $A11.ax $ALL.l

(ps. added a couple Canadian transactions in, just look at $WR1.ax ....)

possibly the end of the road for the long and suffering #A11 $ALL.l holders - Huayou Cobalt to buy 40.5% of Ewoyaa for US$210M. If backing out 40.5% of $ELV US$70m earn-in, the price paid per t LCE in-situ is actually one of the highest recorded, and twice that paid for Arcadia

4

12

2,651

@EvanCranston is exactly right. QC logistics is often overstated as a showstopper.

ie, PMET sits at $150/t logistics disadvantage to a PLS on a CIF China basis (delta $125 trucking/rail, $25 ocean). It can easily claw this back with project specific merits!

May 9

Can someone explain to me like im an idiot how logistics are an issue in some jurisdictions and not others?

Ganfeng trucks ore from Goulamina over 1000km to port (across 2 countries)

Liontown trucks 700km to port

Mt Holland 500km truck

Manono literally in the middle of no where.

Logistics is a function of costs. pure and simple. yes PMET has the most expensive logistics costs but its mine gate costs are some of the lowest in the hard rock world (without by product credits)

What analysts fail to mention is that Quebec has 1 major advantage is that the majority of the mines can connect to the cheapest most reliable power source on the planet benig hydro at 5c/kwh

when the market wakes up and realise that this is an advantage whilst solving the down stream problem at the same time logistics will never be mentioned again.

1

1

14

1,976

However, i'd say the electricity advantage is overstated at the spod con level. PMET DMS plant only draws 13MW - they'll claw back $20-40/t compared to a WA float plant using 20c/kwh elec. It helps keep UG mining and paste cost down but unfrotunately those are comparitively high.

2

5

542

$WR1.ax @ 52c trading -16% discount to $LIFT last close $5.7 even after the positive vote, pending courts final approval.

1

1

14

2,707

possibly the end of the road for the long and suffering #A11 $ALL.l holders - Huayou Cobalt to buy 40.5% of Ewoyaa for US$210M. If backing out 40.5% of $ELV US$70m earn-in, the price paid per t LCE in-situ is actually one of the highest recorded, and twice that paid for Arcadia

Atlantic Lithium is pleased to announce it has entered into a binding Scheme Implementation Deed with Zhejiang Huayou Cobalt Co., Limited ("Huayou"), under which it is proposed that Huayou will acquire all of the issued shares in Atlantic Lithium by way of an Australian scheme of arrangement.

Read in full: shorturl.at/pfC7J.

#ALL #A11 $A11 #ALLGH #Lithium #Ghana #Mining

7

3

21

8,868