🗽🇺🇸 $BBBYQ ABANDONED Shareholder 🛏️🛁✨ SANCTIONED PARADOX 🤕 Husband & Father of 2 🥰 *w/ an abstract global HUMAN 🧠 PHILANTHOPIST (being stolen from)

Joined November 2011

- Tweets 24,716

- Following 51

- Followers 2,282

- Likes 38,859

3,202 Photos and videos

Pinned Tweet

Jun 7

@elonmusk I already have traumatic brain injury. I was told I can’t even get a brain scan without a lawyer - NOT normal. I don’t understand why the United States of America can’t step in to HELP me find meaningful employment and stabilize reality for my family and me so I can be useful again. I hope to be a papa again while my children are still young… I don’t understand why people can’t intervene to get the help we need.

@pulte @neuralink

1

1

428

Jun 15

1

268

Jun 15

$DOGE why are you down 50% from the high a year ago? Can’t help but remember “dogecoin to a dollar” back in the day as memestocks and the associated crypto/digital communities were handed off from redddit (r/wsb -> r/superstonk -> r/bbbyq) to 𝕏

@DOGE @elonmusk @RobinhoodApp @SECGov @CFTC @FTC

352

MJL retweeted

This is the bedside table of a trillionaire.

What do you notice about it? 👀

222

87

993

60,956

Jun 13

I would like to OFFICIALY announce I have joined 𝕏-Philanthropy. Although I am not a business and have unfortunately been unable to file taxes for the past couple years. I worked a lot but it is not recorded or valued anywhere currently. Maybe I need to use a memecoin to track it? idk @SECGov @HesterPeirce @CFTC @MichaelSelig can you please advise?

@elonmusk @pulte @IRS_CIT

1

126

MJL retweeted

Jun 12

“That’s a nice country you’ve got there. Would be a shame if I bought it.”

285

427

6,343

123,811

Jun 13

1

67

MJL retweeted

Apr 5

During my father’s funeral (over 15 years ago), his coworkers from Vietnam flew over and gifted us this amazing “Napoleon” ship.

He was a gifted electrical engineer and worked for a number of prominent chip manufacturers. I don’t know how many patents he holds/held, but he was a genius. He passed way too soon… 😢🧬

@PalantirTech @elonmusk @JDVance @peterthiel @ryancohen @pulte

🚢🇻🇳

1

1

2

205

Jun 10

@elonmusk @ENERGY @PalantirTech @SECGov @CFTC it’s going to rain tonight so I captured a battery and fed him to keep him out of the rain. 🍕🐄

1

1

115

MJL retweeted

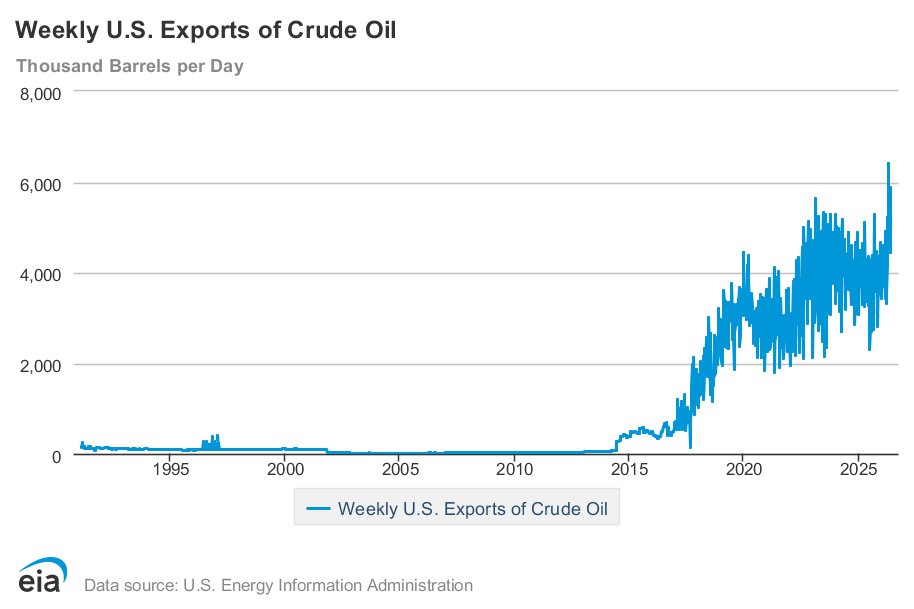

🚨U.S. crude oil exports averaged at a record high of 5.35 million barrels per day in May.

American energy continues to deliver.

169

411

1,689

289,242

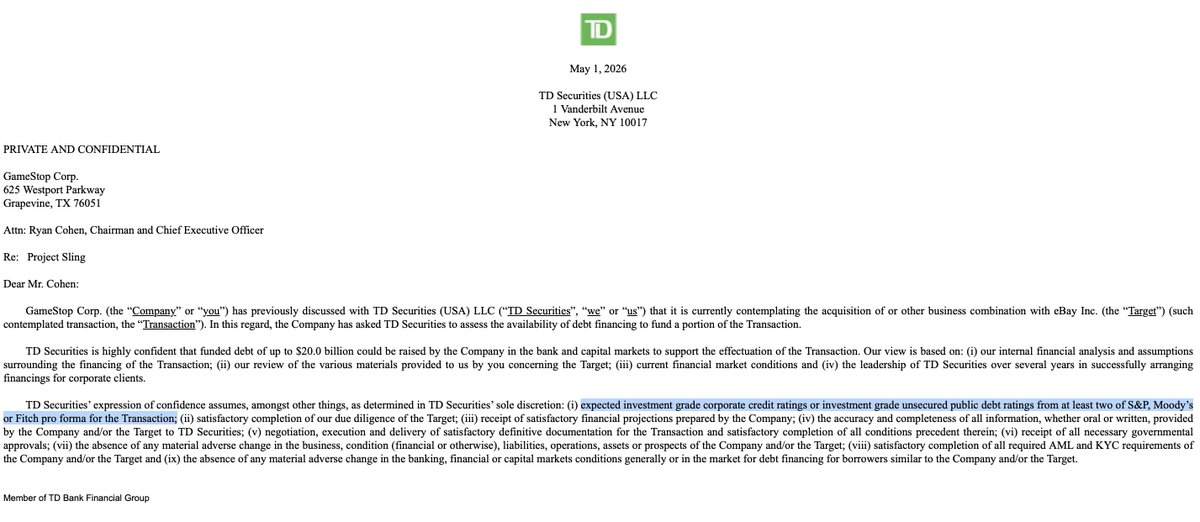

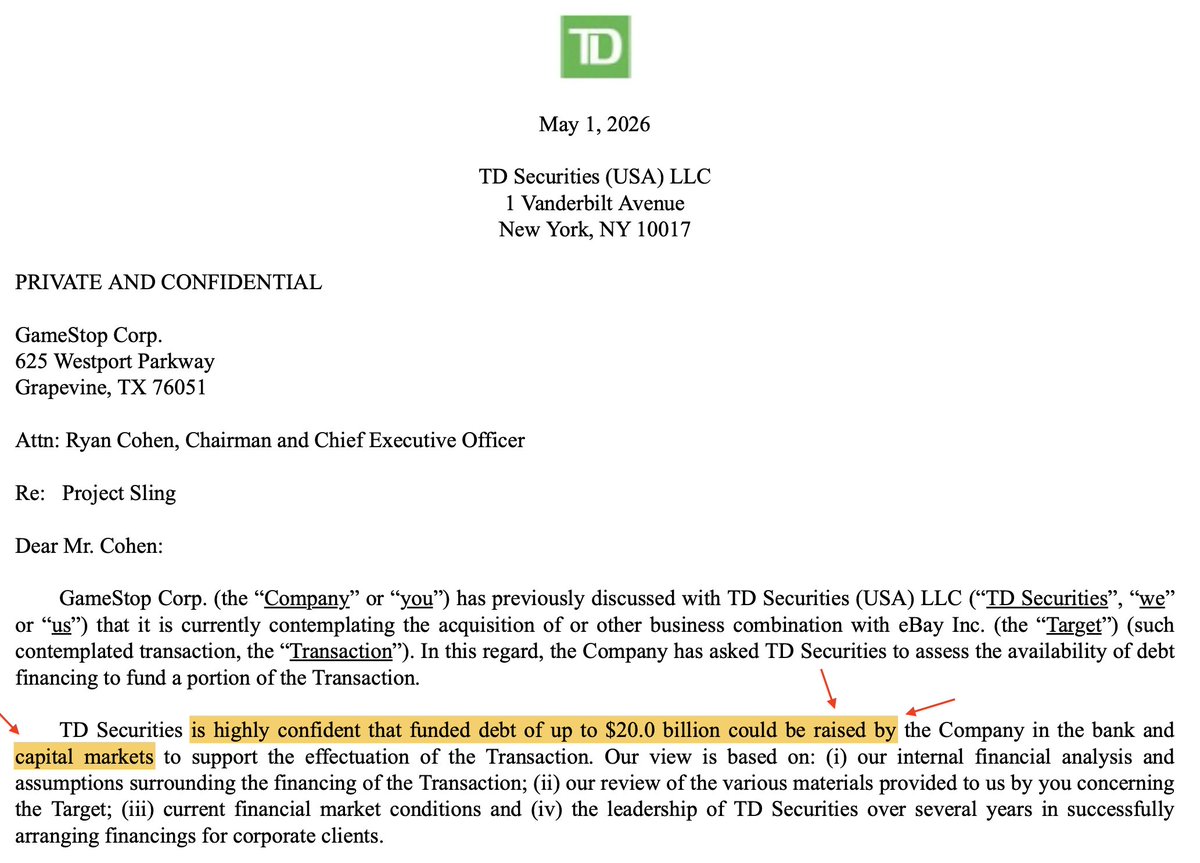

looking for clues it seems quite clear in my opinion that when $GME counters or amends their purchase offer of $EBAY there will be a rather significant change in the deal structure.

the key to the financing is TD Bank seeing an "investment grade" credit rating. if you do the math you know that this is not possible under the current terms because it would bring the combined company's leverage to somewhere around a ~9x ebitda.

I think that is pretty far out and would not meet "investment grade". this has been documented and I highlight it because I do think the credit rating will be achieved. how could the offer be amended to be <5x ebitda? I think there is one realistic pathway and it is through forming an investor group or a private equity co-investor.

what if a deal sponsor enters with a large cash infusion into $GME? in exchange they could get a large minority stake of the company in shares, be issued preferred shares or convertibles. the reason for it is in corporate credit agreements rating agencies look at private equity cash injections as equity/ownership and not debt. so lowering the leverage vs. ebitda becomes simple you have someone that sponsors the deal for x amount of dollars and the company doesn't need as much from TD Bank and the bond market.

i.e. for half cash half stock they need 28 billion in cash. PE or a friendly investor shows up with an 18 billion investment to be a part of the deal, the need from TD Bank comes down to 10 billion and voila! a debt multiple to ebitda <5.

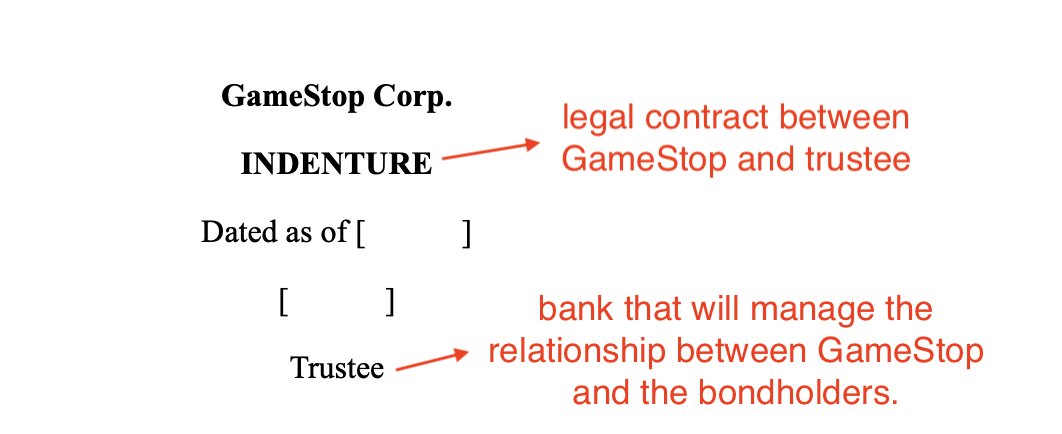

I still believe that we will see GameStop issue bonds but it won't be the only way they raise funds. I wonder if there is anyone out there who sees value in big dog?

“with foresight, the excitement was palpable.”

bonds. by the time everyone else realizes GameStop will not have to deplete 88% of their balance sheet cash, excitement will be off the charts.

bonds are not notes.

$GME

43

77

514

59,258

Jun 2

RLHF potential is being wasted bc of no representation, no employment, no assistance, no guidance. Waste of time, money, and a unique research & development opportunity.

@PalantirTech @WellsFargo @moderna_tx @SECGov @CFTC @USTreasury

207

Jun 1

At what point do Assets of the United States of receive help when our country’s commerce and stock market were defrauded? It seems like never. Truly sad to be an adult male in America and realize no one cares.

🫡🇺🇸🗽

@DeptofWar @DoWCTO @dojphofficial @DOJFraudDiv @CivilRights @SecretService @USMarshalsHQ @SECGov @CFTC @DeptVetAffairs @USTreasury @federalreserve

184

May 17

Take away a man’s purpose and passion, what is he? Empty, bored. Intentionally harmed.

1

2

648

May 31

Retweeting bc I’m still alive, hoping/waiting for help.

2

2

178