people can fly

Joined July 2020

- Tweets 17,646

- Following 231

- Followers 2,193

- Likes 48,171

2,389 Photos and videos

$tungf

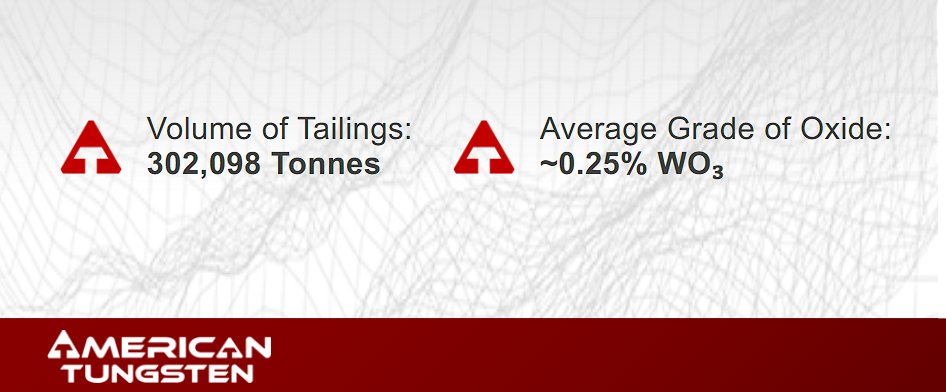

results highlight quality of resource & expansion potential. Successfully delineated multiple stacked tung-bearing polymetallic veins in footwall beyond historically mined areas, while step-out drilling in 5 & 7 veins confirm significant mineralization.

untapped upside Ima

2

195

Stonegate Capital Partners Updates Coverage on $TUNGF

near-term setup increasingly catalyst-rich, underground drilling, tailings, metallurgy, permitting

C$4.91 midpoint valuation(130% above current price)

capital position (C$51M cash) & operating cadence improved materially

1

1

262

$TUNGF

On 1D almost oversold, last time it was close to oversold (November) it almost 3x the following 3 months

The last time it actually was oversold (June), the following 2 months it also 3x

Fundamentally, major catalysts around the corner, resource update &PEA next months

1

273

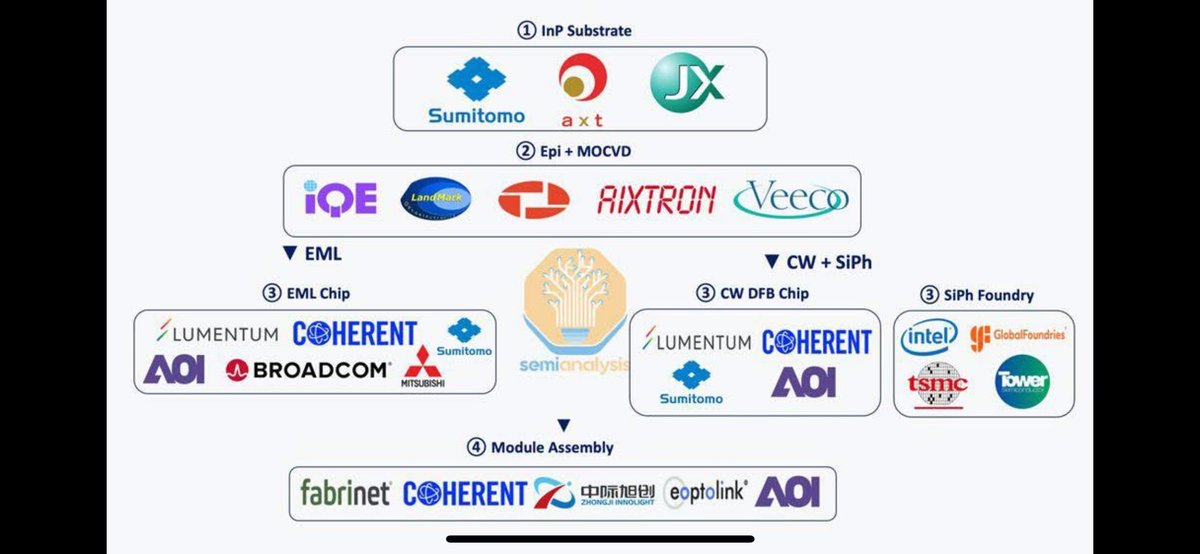

Fabri retweeted

I saw this helpful InP (Indium Phosphide) optical communication supply chain summary from a Taiwan Facebook investment account and found it quite useful, so I’m sharing it with everyone! 📡

InP Optical Communication Supply Chain:

(1) Upstream InP Substrate

$AXTI ・ Sumitomo Electric (5802) ・ JX Metals (5016)

(2) Epitaxy MOCVD Equipment

Epitaxy: IQE ・ LandMark Optoelectronics (3081)

MOCVD: $AIXA ・ $VECO

(3a) EML Chips

$LITE ・ $COHR ・ $AAOI ・ Sumitomo ・ Mitsubishi Electric (6503) ・ $AVGO

(3b) CW DFB Chips

$LITE ・ $COHR ・ $AAOI ・ Sumitomo

(3c) Silicon Photonics Foundry

$TSEM ・ $GFS ・ $TSM ・ $INTC

(4) Assembly

Zhongji Innolight (300308) ・ Eoptolink (300502) ・ $COHR ・ $FN ・ $AAOI

#InP #Photonics

Purely personal sharing • Not investment advice! (More details in the original post)

3

13

73

10,339

I like them! I see lot of upside left!

331K MTU/yr, even at $1500/mtu with 78% payability, they make $388m which is ~ half of current MC.

Without including the 462 tonnes of tin.

One of the largest resources in the world

AISC pretty low too so once in prod. a pretty safe play

Apr 25

Your thoughts on tungsten-west #tun.L?

1

2

560

Full commercial production is planned for Q1 2027 which means they should still profit of higher tungsten prices so the potential cash flow will be even greater.

Bull case

$3000 / mtu

Revenue : 774.5M without tin, for a full year in commercial production

Which is insane.

2

1

328