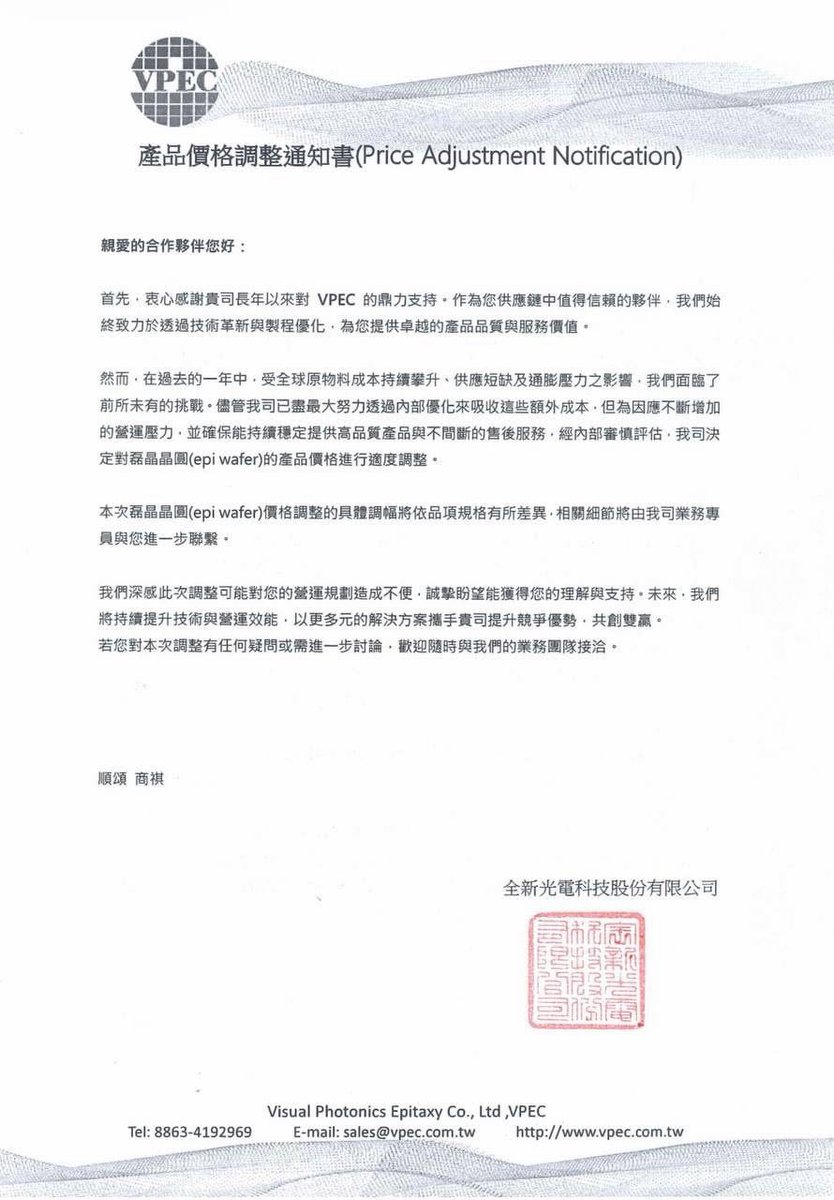

全新光电的GaAs 和 InP外延片提价通知。

VPEC全新光電

產品價格調整通知書 (Price Adjustment Notification)

親愛的合作夥伴您好:

首先,衷心感謝貴司長年以來對 VPEC 的鼎力支持。作為您供應鏈中值得信賴的夥伴,我們始終致力於透過技術革新與製程優化,為您提供卓越的產品品質與服務價值。

然而,在過去的一年中,受全球原物料成本持續攀升、供應短缺及通膨壓力之影響,我們面臨了前所未有的挑戰。儘管我司已盡最大努力透過內部優化來吸收這些額外成本,但為因應不斷增加的營運壓力,並確保能持續穩定提供高品質產品與不間斷的售後服務,經內部審慎評估,我司決定對磊晶晶圓的產品價格進行適度調整。

本次磊晶晶圓價格調整的具體調幅將依品項規格有所差異,相關細節將由我司業務專員與您進一步聯繫。

1

225

hongrosesheng retweeted

Jun 13

China is deliberately choking the global supply of Indium Phosphide (InP), the material that makes every laser in every AI data center work.

Reuters confirmed: US officials have visited China multiple times to resolve this. China is still blocking export approvals on purpose. They want to maintain the bottleneck.

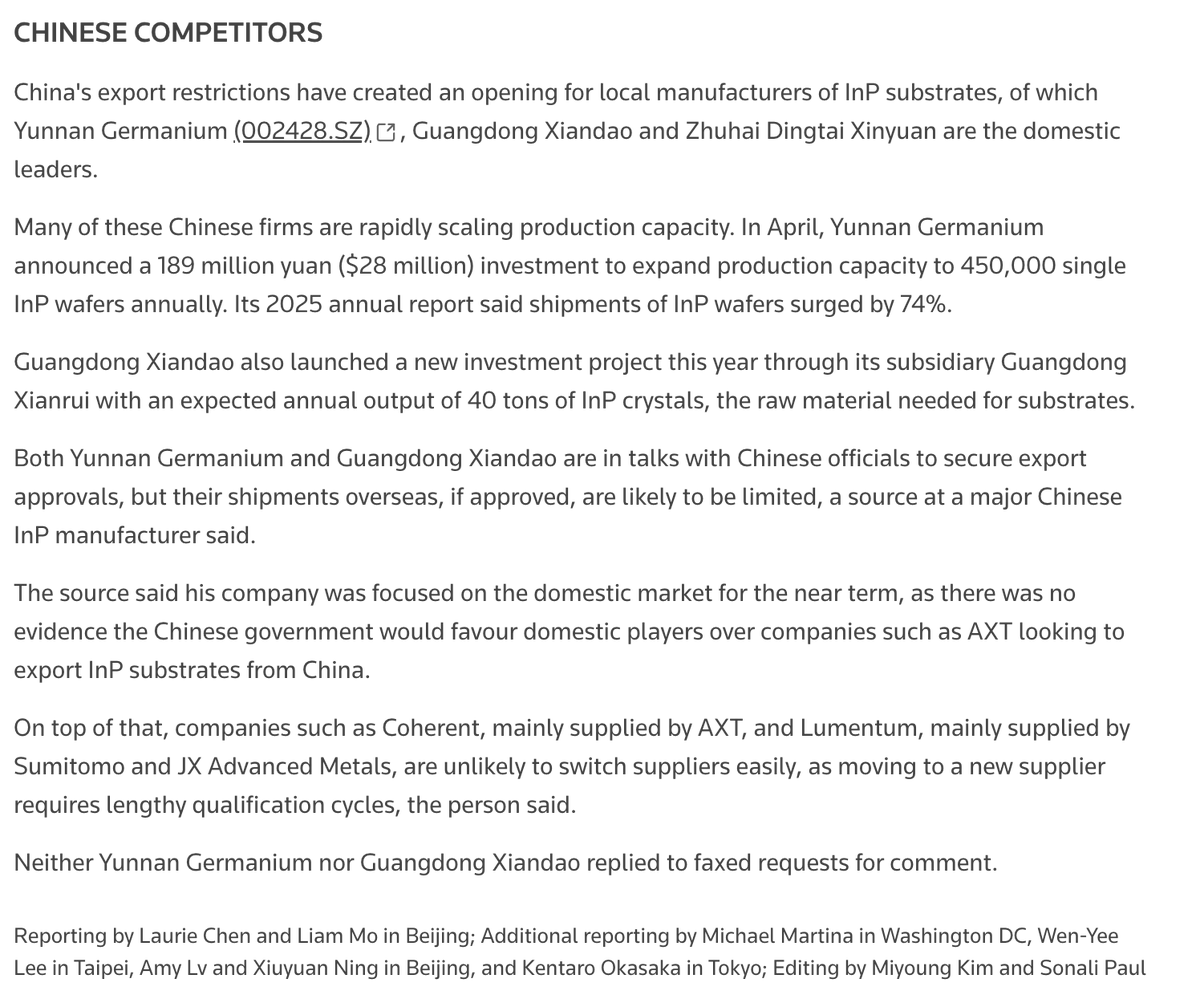

Chinese producers like Yunnan Germanium (002428.SZ) and Guangdong Xiandao are scaling capacity fast (Yunnan investing $28M to reach 450K wafers/year, shipments up 74% in 2025). But even if export approvals are granted, overseas shipments will be "limited."

Switching InP suppliers requires lengthy qualification cycles. You can't just find a new source overnight. 12-18 months...

This will help explain the recent price action in the below names.

WINNERS:

$SIVE.ST CW lasers ARE InP devices. Policy-duration shortage extends their 14-quarter laser supply constraint indefinitely. Every month China maintains this, SIVE's pricing power widens.

$LITE Substrates come from Sumitomo JX Advanced Metals in Japan. Entirely outside the China export gate. Their competitor's supply gets squeezed while theirs is control-immune. This is the cleanest relative advantage.

Win Semi (3105.TW) Only pure-play III-V foundry on earth. InP wafer fab capacity is scarce globally. Tighter substrates = their existing capacity commands higher pricing.

$AEHR Sole-source wafer-level burn-in testing for InP and SiPh devices. When every wafer is more valuable because the input material is scarce, the cost of shipping a bad one goes up. Testing intensity rises with scarcity.

AIXA (AIXA.DE) Makes the MOCVD equipment needed for InP epitaxy. Every country trying to build domestic InP capacity needs their tools. More fragmentation = more equipment orders.

$SOI.PA Photonics-SOI monopoly. InP scarcity makes the entire optical layer more expensive, increasing the value of every component in the stack including Smart Cut SOI wafers.

LOSERS:

$COHR Reuters specifically names Coherent as "mainly supplied by AXT." AXT manufactures IN China, inside the export gate. Even if approvals come, shipments will be limited. COHR carries a substrate risk that LITE does not. And switching requires lengthy qualification cycles.

$AAOI Demand is not the issue; laser/EML/InP component supply is. If AAOI cannot secure enough laser chips, capacity ramp can slow.

$AXTI AXT is a US-listed InP substrate maker that manufactures in China. Their entire equity value is an export-approval question. If approvals flow, massive upside. If they don't, the business model breaks for Western customers.

We are watching real-time supply chain warfare over AI supremacy. The companies that own the physical bottlenecks in this chain benefit every time the world fragments.

Reuters: U.S. officials have visited China multiple times and urged the Chinese side to resolve the InP export controls, but China is still causing delays in export approvals.

As a result, U.S. photonic chip manufacturers that need InP are facing difficulties.

However, China does not appear to be particularly favoring domestic Chinese companies over U.S. companies operating in China. China wants to maintain the bottleneck the U.S. is facing in InP, so most Chinese domestic InP producers are focusing on the domestic market.

Chinese InP manufacturers such as Yunnan Germanium and Guangdong Xiandao are both in talks with Chinese authorities to secure export approvals, but even if approvals are granted, overseas shipments are likely to remain limited.

31

77

531

119,430

L INP mesure la reactivite reelle d une page entre une action et le prochain affichage. Pour l ameliorer sur un site JS moderne, reduire le travail du thread principal, fractionner le JS, limiter l hydratation et deferer le non critique.

#SEO #WebPerf francaise-du-numerique.fr/fa…

1

China's control over indium phosphide exports threatens AI data centre rollout

InP is essential for lasers, modulators, and detectors in high-speed optical transceivers

mexicobusiness.news/mining/n…

reuters.com/world/china/chin…

5

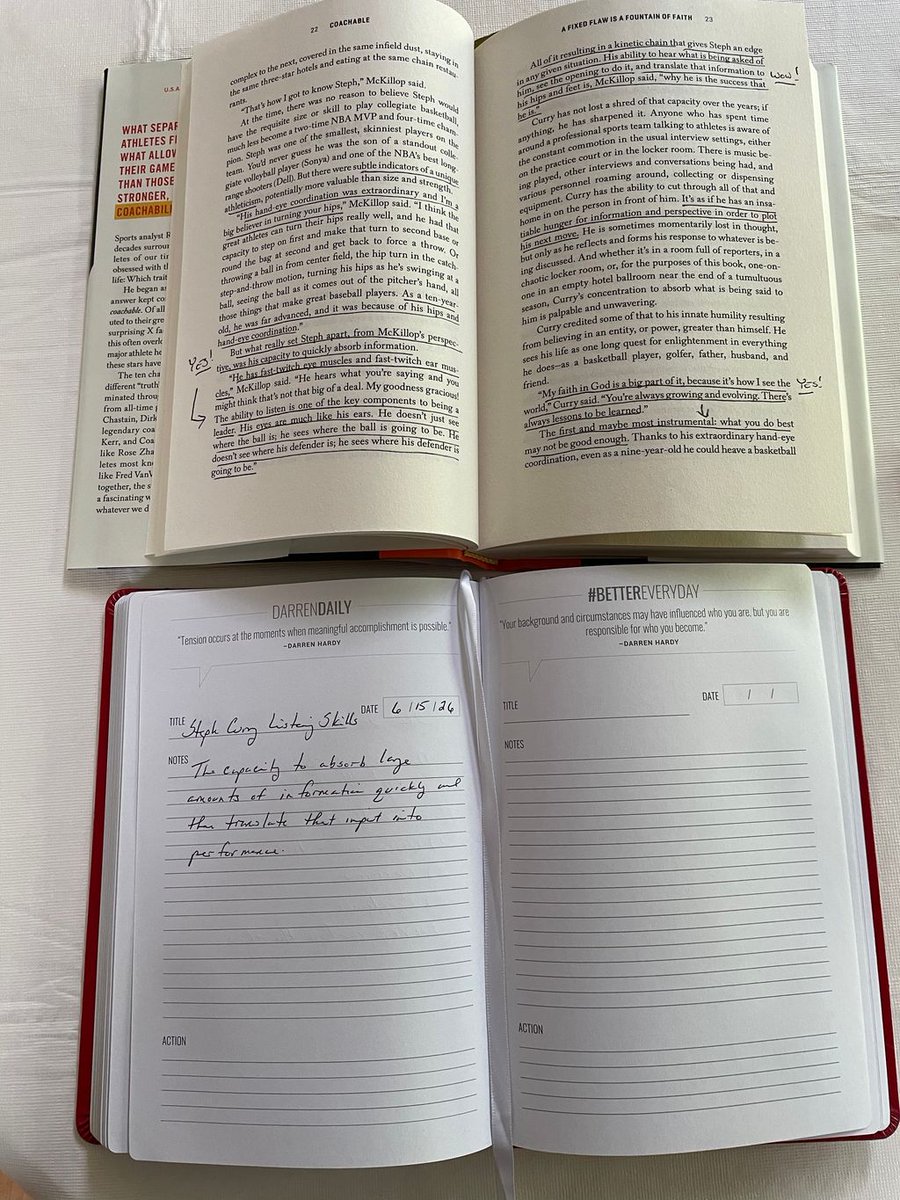

Brian Dodd On Leadership retweeted

One of Steph Curry's superpowers - The capacity to absorb large amounts of information quickly and then translate that input into performance. Great lesson from Rick Bucher's book Coachable. Purchase it at buff.ly/RMZ8MH4

1

62

$AAOI

I’m bullish. Are you invested?

Applied Optoelectronics demonstrates robust positioning in the 800G and emerging 1.6T optical transceiver market through vertical integration of InP laser technology and advanced manufacturing processes.

- Q1 2026 revenue reached $151.1 million representing 51 percent year over year expansion driven by hyperscaler deployments in AI accelerated compute clusters.

- Management guidance projects full year 2026 revenue exceeding $1.1 billion supported by a $324 million advanced node order backlog and DOCSIS 4.0 multi year contracts.

- Gross margin trajectory targets 35 percent by year end as product mix shifts toward higher speed coherent modules with improved yield curves from Houston facility expansions.

- Capacity constraints currently limit output to approximately $1.5B addressable demand creating a supply bottleneck that favors AAOI share gains.

- Price target: $220 achieving monthly run rates above $200Mby mid 2027.

2

9

836

Panowie, historia dla historyków i INP.

Mamy poważniejszy problem - prezydent kabluje na premiera online.

Prezydent Nawrocki atakując w USA polski rząd zapomina, że jest Prezydentem RP, a nie funkcjonariuszem TV Republika.

13

Raksa retweeted

Jun 13

Looks interesting, research utilising the English Grammar Profile and corpus query patterns

Linking textbook grammar input to writing accuracy in exam-oriented EF... sciencedirect.com/science/ar…

2

6

315

Je crois qu’on a réveillé un monstre avec $VECO

La dernière news Ennostar est beaucoup plus importante qu’elle en a l’air

>Ennostar vient de qualifier le nouveau LUMINA MOCVD de Veeco pour la production high-volume d’applications optoélectroniques avancées

Ce n’est pas juste une évaluation, c’est une qualification production

Et ça ajoute une troisième jambe à la thèse $VECO qu'on a ennoncé dans les précédents posts et que je vais vous refaire car vous êtes des petit flemmards

1. Silicon photonics/InP lasers

>Lors de ses derniers earnings qui semblaient être décevants, lors du call Veeco a annoncé plus de $250M de commandes pour ses outils Spector, Lumina et WaferEtch destinés à la fabrication de lasers InP.

>Ces lasers sont critiques pour les transceivers 800G / 1.6T utilisés dans les data centers hyperscale et le narratif adore ce produit

Livraisons en 2026 -> accélération forte en 2027

2. Advanced logic/NSA500

>Veeco a reçu une commande de suivi pour son système NSA500 après validation par un client logic avancé (cf dernier post).

>Ils ont aussi envoyé un NSA500 à un troisième client advanced logic pour évaluation, avec potentiel de premières commandes HVM en 2027.

>Le marché commence à comprendre que le laser annealing devient critique pour les architectures avancées, les structures 3D, les nouveaux nœuds et les budgets thermiques ultra-serrés.

3. LUMINA /MOCVD/As-P/microLED

>La qualification par Ennostar valide la nouvelle plateforme LUMINA pour la production.

>C’est important parce que Veeco ne joue pas seulement l’IA via la photonique.

>Ils jouent aussi les compound semiconductors, l’optoélectronique, les microLED, le biosensing, l’automotive et les communications optiques.

Donc la thèse $VECO n’est plus seulement :

“la petite boîte d’équipements semi”.

C’est plutôt :

“LE fournisseur d’outils critiques sur plusieurs bottlenecks de la prochaine décennie”.

Le bull case devient très intéressant.

Aujourd’hui, $VECO vaut environ $4.7B de market cap.

Si la boîte passe de $750M-$800M de revenus à $1.5B-$1.8B d’ici 2030, avec un meilleur mix semi et des marges qui montent, le titre peut se revaloriser beaucoup plus haut (logique)

À 8x-9x sales, on arrive déjà vers $12B-$16B de market cap.

Soit environ $200-$265 par action.

Dans un scénario très bull, avec $2B de revenus, plusieurs clients HVM sur NSA500, adoption plus large de LUMINA et bottleneck durable sur InP/silicon photonics, on peut commencer à parler de $300 .

Bear case évident :

Les évaluations peuvent glisser, les commandes peuvent prendre du temps, le cycle capex semi peut ralentir, et la concurrence reste réelle.

Je continue cependant à être haussier sur ce dossier

May 6

Devinez quel boîte profite du triple narratif Mémoire — Photonique — Quantum ?

Et bien c’est $VECO

Tout le monde regarde $NVDA, $AVGO , $MRVL, $TSM, la mémoire, le CPO et la photonique.

Mais VEECO vend les outils nécessaires pour énormément de ces narratifs au travers de ces processus :

>Laser Annealing

>Ion Beam Deposition

>Advanced Packaging Lithography

>Wet Processing

>MOCVD pour lasers InP

En clair et comme vous le savez :

Si les clusters IA continuent de scaler, la demande augmente pour l’advanced packaging, les lasers InP, la photonique, le HBM et les interconnexions optiques.

Et $VECO spécialement vend une partie des machines nécessaires à cette supply chain.

Depuis les earnings de hier on a appris :

$250M de commandes pour des systèmes liés à la fabrication de lasers indium phosphide, avec livraisons dès Q3 et ramp attendu en Q1 2027.

Donc logiquement $VECO print 23% post earnings.

Les Chiffres en grand :

>~$3.7B market cap

>Q1 revenue: $158M

>FY 2026 guide: $740M-$800M

>Cash short-term investments: ~$383M

Évidemment le risque c’est que le marché paie aujourd’hui une partie de la croissance 2027 avant qu’elle n’apparaisse dans les chiffres ainsi que les exports vers la Chine.

Pour résumer :

$VECO est un play structurant sur la photonique et l’advanced packaging avec une optionalité sur le quantum et la HBM

4

3

69

7,508

Practical Tips Every Web Developer Should Follow in 2026

1. Master Mobile-First & Core Web Vitals

Always design mobile-first. Google now prioritizes sites with excellent LCP, CLS, and INP scores. Slow or jumpy websites lose visitors and rankings.

Happy weekend

3

Isn't he problem that they literally cannot meet the demand due to supply constraints like lack of inP? Who cares about the demand if they're never able to increase supply meaningfully and apparently arnt able to increase prices since their margin isn't growing much

58

EL ACTO ADMINISTRATIVO DE LA VULNERACION DE MI DERECHO PREVISIONAL SE BASO EN ESE DOCUMENTO SIN FIRMA AL CUAL FUNCIONARIOS DE LA S.PENSIONES DIERON VALOR PROBATORIO POR SOBRE LOS DOCUMENTOS VALIDADOS E HISTORICOS DEL EX INP MODULO DE IMPONENTES

4

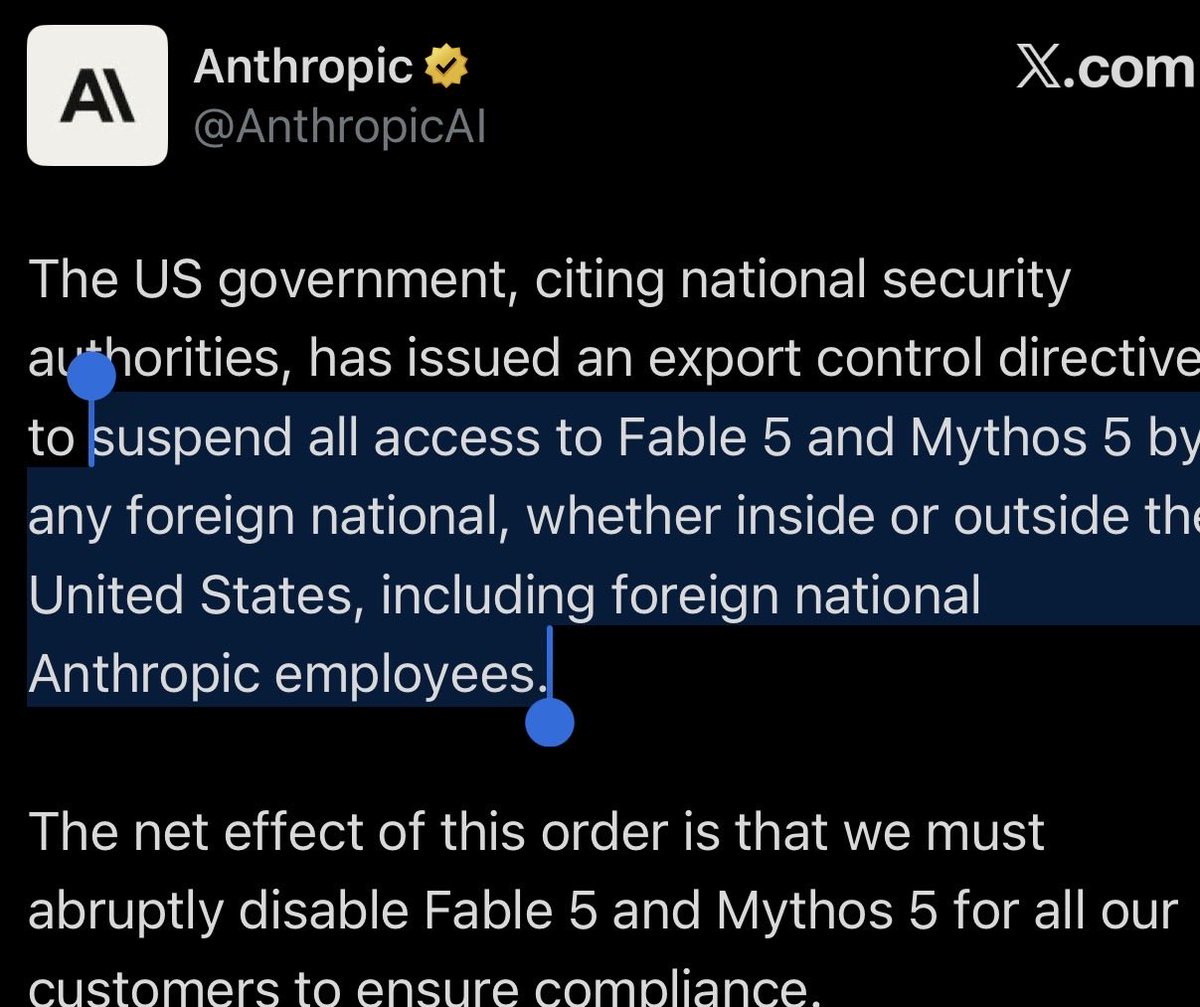

The restrictions on Anthropics Fable 5 and Mythos 5 aren’t bearish

If anything, they’re proof that AI has become strategic national infrastructure

Governments don’t restrict technologies they view as unimportant

The bigger takeaway is what happens next

The UAE, France etc and others will accelerate sovereign AI initiatives

More domestic compute, more local models = data centers

No country wants to depend on infrastructure that can be switched off by another jurisdiction overnight

That means more demand across the entire AI supply chain

Compute. Chips. Lasers. Fiber. Power. Cooling.

The picks and shovels providers don’t care whose flag is flying over the data center

There may be some short term volatility, but long term this looks like another tailwind for the infrastructure layer

The AI buildout isn’t slowing down. It’s becoming more fragmented, more localized, and ultimately larger

The real bottlenecks remain the same

lasers, InP substrates, silicon photonics, power delivery, and fiber connectivity

Compute: $NVDA $AMD $AVGO

Optics: $AAOI $SIVE $COHR $LITE $AXTI $AIXA $SOI $FOCI $TSEM $NCI

Power: $NVTS $AOSL $POWI

Sovereign Compute/DC: $NBIS $GLW

More sovereign clusters means more demand chasing the same constrained supply chain

The supercycle remains intact

I have positions in many of these names. NFA.

1

4

145

The Anthropic news is bullish a lot of names in my opinion. US export controls just kicked the AI race up a notch. Anthropic had to pull its top models for everyone after the government blocked foreign access.

This stuff is going to tighten supply chains even more in compound semis.

$IQE being a European epi-wafer player puts them in a great spot. Strong InP demand for AI optics plus trusted non-China supply means more customers will want to lock in capacity. Expect more deals, bullish.

Jun 13

The AI supremacy Wars begins.

Think a lot of the upstream supply chain bottlenecks caused by each Country export controlling each other (eg. $AXTI)

Should present some interesting opportunities in the near future.

That being said, Anthropic was getting distilled left and right in Singapore -> China and others.

Hot take, but steps like this do help preserve American dominance in AI, keeping the most advanced model at home.

I don’t think Superintelligence should be global access, since we’re starting to get into uncharted territories.

1

4

184

Agree on treating $AXTI more as a trading vehicle than a core hold. @aleabitoreddit was vocal this spring on the dilution risk, heavily criticizing the 70M→120M authorized shares proposal. It passed on June 4 anyway. Combined with the ongoing China InP export permit uncertainty (still management's top operational issue), it's why AXT is better suited for trading swings, despite the strong InP thesis.

29

翻译:

这会惹恼很多人:

但技术分析(TA)就是交易员的占星术。

它无非是确认偏误 利用人性心理来找入场点。

有点像当年有人抢跑 $SPCE,因为 $SPCX 上市时,他们预期散户会搞混代码——这就是在交易心理。

$SIVE 暴涨 1900%,不是因为什么”黄金交叉、太空彗星、喷火巨龙 K 线”——那是某人想卖你 499 美元的东西。

而是因为市场在为 GFS 公布后带来的未来营收定价。

$AXTI 涨了 8000%,也不是因为当初在 8 美元时响起的”黄金瀑布 K 线警报”。

而是因为 InP 衬底、ASP 涨价的博弈论、出口管制、光子学需求等等。

如果你想从心理层面搞清楚其他傻子在信什么,那你就用 TA。

但要判断真正的上行空间……算了吧。

过去也不知道多少个月,有人在 $IREN 上画出 120 美元的 TA 目标,但当面前摆着一个 60 亿美元的 ATM(增发)需要先被消化掉时,那些玩意儿统统没用。

真正起作用的是主题(比如 $LITE 与 $AAOI 的关联)、任何影响远期营收的消息催化剂、业绩预测、宏观消息、财报、流通盘动态等等。

然后你就能推导出这家公司应该处于什么样的市值。

所以,就入场点而言,没错,你可以用 TA。

但要判断股票往哪走,就把那个”霸王龙·欧米伽·绿光 K 线指标”扔出窗外吧。

This is gonna upset a lot of people:

But TA is astrology for traders.

It's confirmation bias trading human psychology about entries.

Kinda like how people frontran $SPCE from $SPCX IPO expecting retail to mess up tickers by trading psychology.

$SIVE didn't go up 1900% because of the golden cross space comet firebreathing dragon candle that someone is trying to sell for $499.

It's because markets are pricing in future revenue from $JBL, $GFS that got announced.

$AXTI didn't go up 8000% because the golden waterfall candle alert sounded back at $8.

it's because of InP substrate, game theory on ASP hikes, export controls, photonics demand, and others.

If you want to figure out psychologically what other regards are believing, you use TA.

But for determining the actual upside... nah

People have been drawing $120 TAs on $IREN for the past idk how many months none of that crap matters when there's a $6B ATM that needs to be bought through first.

It's by theme (eg. $LITE to $AAOI relations), any news catalysts that affect forward revenue, projections, macro news, earnings, float dynamics, and so on.

Then you can just derive what MC that company should be at.

So for entry points, sure you can use TA.

For determining where the stock heads, just throw the tyrannosaurs rex omega-green candle indicator out the window.

2

1

2,137