Tweets are informational only, never investment advice.

Joined January 2018

- Tweets 8,713

- Following 650

- Followers 34,415

- Likes 70,836

1,217 Photos and videos

Pinned Tweet

14 Oct 2025

8 Oct 2025

In investing, the best way to get to yes is by running out of reasons to say no

3

2

11

19,538

May 26

Imagine going to a cocktail party and being the only person there who doesn't own a single share of $MU

You can't

9

1

30

20,071

Apr 17

My fav part of recovery rallies is that they are 2x as ferocious as the selloffs that preceded them. Market structure has changed. Props to anyone successfully managing an idio short book.

7

4

94

15,842

Mar 30

What I don’t get about the Ackman GSE plan: under current PSPA terms, once GSE hit capital targets, treasury effectively sweeps ~100% of net income forever via the senior pref.

So why would the govt voluntarily deem the pref repaid and thus ending up w 80% of the GSEs (instead of 100%), while letting hedge funds capture a massive windfall?

Seems way more likely to happen via court pressure than voluntarily…and especially unlikely before midterms.

Mar 30

The math on Fannie and Freddie is so dislocated it looks like a pricing error.

Fannie printed $14.4 billion in net income last year. Freddie printed $10.7 billion. Combined market cap on the pink sheets right now: ~$12 billion. The market is pricing $25 billion in annual earnings at a 0.48x multiple. Find me another 0.48x earnings multiple anywhere in American finance. It doesn't exist.

The dilution fear is the reason the stock is cheap and the reason the stock is wrong. Treasury put in $187 billion. The GSEs have swept back over $300 billion since 2012. That's an 11.6% IRR. If Treasury exercises its 79.9% warrants at today's price, the government's stake is worth ~$9.6 billion. If it exercises post-relist at 10x earnings, that stake is worth $200 billion. The difference is $190 billion. Washington doesn't leave $190 billion on the table to spite penny stock holders.

Capital requirements look scary until you do the arithmetic. The ERCF says $334 billion. They have $179 billion. The FHFA can lower Tier 1 to 2.5% without Congress. New target: ~$190 billion. Gap: $11 billion. One IPO closes it. One year of retained earnings closes it twice.

G-fees are already at 65 bps. Pre-crisis they were 20. The GSEs have been charging privatized pricing inside a conservatorship for 14 years. Credit losses outside of 2008 average under 5 bps. The margin is so fat that mortgage rates don't move at all on release.

So what are you actually buying at $5? A royalty on the American mortgage system. 65 bps on $7.5 trillion in outstanding MBS. $48 billion in gross annual revenue. Under 5 bps in historical losses. The most predictable spread in finance, backstopped by a guarantee both parties have publicly committed to preserving.

JPMorgan trades at 13x and takes real credit risk. Utilities trade at 15x with half the visibility. These two trade at 0.48x collecting tolls on other people's risk.

The second those warrants convert and the NYSE listing goes live, every index fund and pension fund with a financial sector mandate has to buy. Two of the ten most profitable companies in America, sitting on the pink sheets, waiting for one signature.

16

2

31

19,978

Mar 30

Open to feedback for why this is a bad take btw. Would love to understand the asymmetry…

1

2

2,671

Mar 4

Insider buys usually feel like PR fluff. But $45M into $KKR at these levels is clearly an investment, not signaling. Especially meaningful coming from guys whose entire schtick is figuring out what things are worth...

18

26

383

95,237

Mar 3

“A lot of being successful as an investor is finding an investment's philosophy that fits your own emotional makeup, such that you can be rational when you are wrong.”

So spot on @GavinSBaker

Mar 2

Investing is entering a new regime defined by AI acceleration, crossover convergence, and a widening gap between insight and execution. A conversation with @GavinSBaker of Atreides Management on rigorous debate, conviction, and how culture & risk management drive performance across public and private markets.

capitalallocators.com/podcas…

With thanks to @AlphaSenseInc, @MorningstarInc, and Ridgeline.

2

2

42

9,136

Feb 12

Not to worry… if AI is replacing us as fast as Elon promised FSD, we’ve all got about 20 years of job security left

62

88

2,030

110,779

29 Jul 2022

There’s no such thing as a perfect investment. It’s all about deciding which risks you can live with and at what price.

15

28

293

14 Oct 2025

10 Dec 2023

When good investors say ignore macro they mean ignore how it impacts stock prices, but not how it impacts the underlying businesses.

Buying stuff at attractive prices means understanding how macro will impact earnings and not overpaying for cos that are massively over earning.

3

2

2

8,460

Feb 10

Feb 10

Unleveraged upside has a greater margin of safety than leveraged upside...when you are wrong on the business.

Lower multiple stocks have greater risk/reward...when you are right on the business.

2

1

2,990

Feb 10

Unleveraged upside has a greater margin of safety than leveraged upside...when you are wrong on the business.

Lower multiple stocks have greater risk/reward...when you are right on the business.

1

2

24

6,493

Jan 22

The January 2026 BofA Global Fund Manager Survey says global investor sentiment is the most bullish since Jul’21...the broadest measure of FMS sentiment, based on cash levels, equity allocation, and global growth expectations, rose to 8.1 from 7.3.

1

4

9

3,581

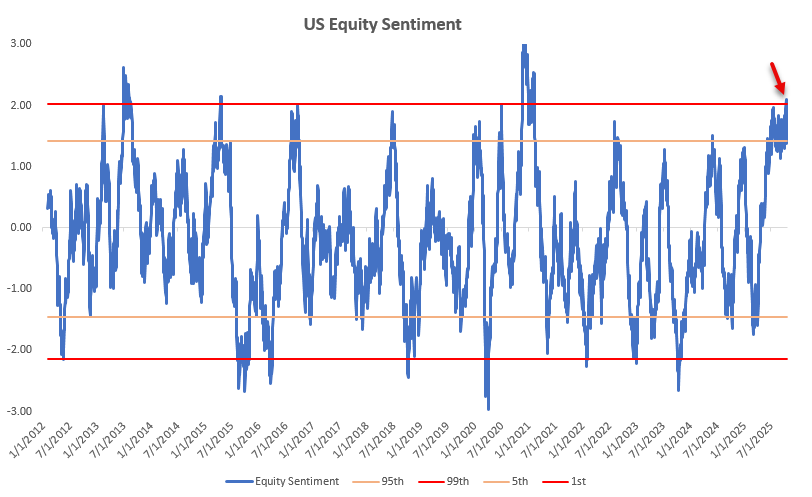

22 Oct 2025

Is it time to btfd yet?

20 Oct 2025

"Buy the Dip" trading strategy having its best return in more than 30 years

~Bespoke h/t jefferies

6

3

16

12,675

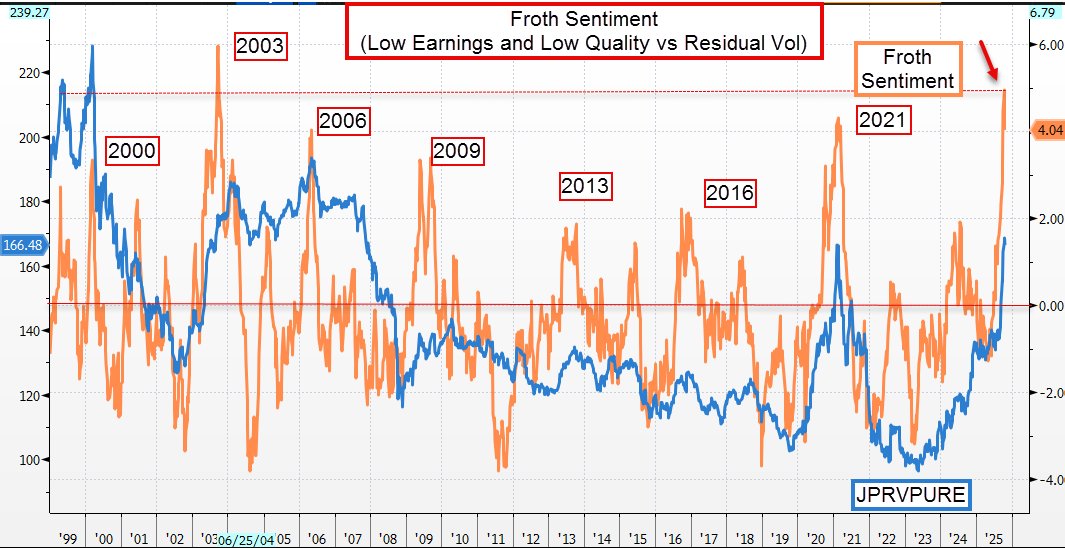

22 Oct 2025

JPM Froth Sentiment is near its highest levels since '98

3

28

124

40,900

22 Oct 2025

Which is closely linked to low profitable crowding (i.e. the greatest hits from the album titled: "2021 ipo's despacs")

1

4

9

4,502