68 Photos and videos

Scip retweeted

Jun 14

More limited & expeditionary wars are somewhat poor predictors of existential military confrontations. A state fighting a war of choice and a state fighting for survival commit on entirely different scales, and it is the scale of commitment, not solely the underlying capabilities & resources, that usually determines the outcome of such conflicts.

1

7

44

7,741

Scip retweeted

Jun 13

They are both downstream of the fact we have failed to integrate capital markets to where they offer sufficient depth for companies to scale

Jun 13

it's not lack of compute that's the issze. it's that in Europe, it's unthinkable to pay a guy in his mid 20s $600k salary and give him resources and freedom to train models without having oversight by a committee of gerontocratic professorswho don't keep up with the research

5

9

70

7,064

Scip retweeted

Jun 12

Its called Eurovision

Jun 12

Here's an idea: World Cup but without the football. Just ethno-nationalist rivalries.

27

1,639

43,125

605,541

If you have any investments in index funds you have major exposure to AI because the vast majority of stock market gains in the past years have been AI related, from semis to energy and even various industrials. Will be ugly if it goes bust.

Jun 2

Documenting the headwinds I now see for AI.

It won't seem like it, but I love AI and am long-term positive. But when "math doesn't math" I take note.

1. The core thesis for foundation model lab investment has been high upfront investment made worthwhile by significant long-term profits.

2. These are capital intensive businesses and the compute commitments are very high relative to revenue and require strong growth over long time periods. The "leverage" (commitments versus revenue) is extremely high.

3. The fundamentals are not as positive as they previously were:

• Input costs are higher (commodities, chips, power)

• Interest rates are higher

• Competition is more intense

• Scaling Laws are now problematic: exponential costs/power cannot continue

4. Forecasting compute spend is challenging and high risk due to (a) revenue uncertainty and (b) algorithm uncertainty

5. Revenue growth appears to be slowing. The technology is valuable, but ROI is proving to be more expensive and take longer than anticipated.

6. The future is likely "different models for different use cases" with the lower end of the market being highly competitive.

7. Core use cases such as agentic software engineering are likely to need approaches beyond next-token prediction. They are Σ₂ᴾ complexity problems requiring multi-objective optimization and likely a combination of Transformers and other methods.

8. Current forecasts in memory makers are built largely on quadratic attention. That will not persist: we are already seeing work from DeepSeek, Minimax and Nvidia that can cut RAM needs by 80% or more.

9. This means semiconductor valuations are substantially overinflated and will go through the traditional glut versus shortage cycle.

10. For foundation model providers: lower costs with competitive differentiation is good. However, lower costs with a lack of differentiation would mean lower revenues. This makes it harder to (a) service commitments and (b) pay back investors.

11. Leverage is substantially higher than in previous cycles, evidenced by leveraged ETFs, call option activity and margin loans. Korea is particularly susceptible.

12. 0DTE options create a profile that has stronger parallels to portfolio insurance and 1987 than any other point I can remember.

13. The combination of exponential increases in call activity coupled with the ties of semiconductors to structured products means there is a non-trivial systemic risk to the financial system.

14. Implied earnings growth rates are inconsistent with other periods in history.

15. Macroeconomically we cannot and should not fund exponential cost increases. History has shown us repeatedly that there are better ways (see Quick Sort and Simplex).

16. Significant supply is hitting the market via IPOs.

––

Taken together: costs and competition are increasing while revenue growth is likely slowing. Valuations are fragile and prone to technology disruptions that are already here. Systemic financial market risk is extremely high.

1

1

204

Scip retweeted

Jun 2

Documenting the headwinds I now see for AI.

It won't seem like it, but I love AI and am long-term positive. But when "math doesn't math" I take note.

1. The core thesis for foundation model lab investment has been high upfront investment made worthwhile by significant long-term profits.

2. These are capital intensive businesses and the compute commitments are very high relative to revenue and require strong growth over long time periods. The "leverage" (commitments versus revenue) is extremely high.

3. The fundamentals are not as positive as they previously were:

• Input costs are higher (commodities, chips, power)

• Interest rates are higher

• Competition is more intense

• Scaling Laws are now problematic: exponential costs/power cannot continue

4. Forecasting compute spend is challenging and high risk due to (a) revenue uncertainty and (b) algorithm uncertainty

5. Revenue growth appears to be slowing. The technology is valuable, but ROI is proving to be more expensive and take longer than anticipated.

6. The future is likely "different models for different use cases" with the lower end of the market being highly competitive.

7. Core use cases such as agentic software engineering are likely to need approaches beyond next-token prediction. They are Σ₂ᴾ complexity problems requiring multi-objective optimization and likely a combination of Transformers and other methods.

8. Current forecasts in memory makers are built largely on quadratic attention. That will not persist: we are already seeing work from DeepSeek, Minimax and Nvidia that can cut RAM needs by 80% or more.

9. This means semiconductor valuations are substantially overinflated and will go through the traditional glut versus shortage cycle.

10. For foundation model providers: lower costs with competitive differentiation is good. However, lower costs with a lack of differentiation would mean lower revenues. This makes it harder to (a) service commitments and (b) pay back investors.

11. Leverage is substantially higher than in previous cycles, evidenced by leveraged ETFs, call option activity and margin loans. Korea is particularly susceptible.

12. 0DTE options create a profile that has stronger parallels to portfolio insurance and 1987 than any other point I can remember.

13. The combination of exponential increases in call activity coupled with the ties of semiconductors to structured products means there is a non-trivial systemic risk to the financial system.

14. Implied earnings growth rates are inconsistent with other periods in history.

15. Macroeconomically we cannot and should not fund exponential cost increases. History has shown us repeatedly that there are better ways (see Quick Sort and Simplex).

16. Significant supply is hitting the market via IPOs.

––

Taken together: costs and competition are increasing while revenue growth is likely slowing. Valuations are fragile and prone to technology disruptions that are already here. Systemic financial market risk is extremely high.

61

234

1,721

551,498

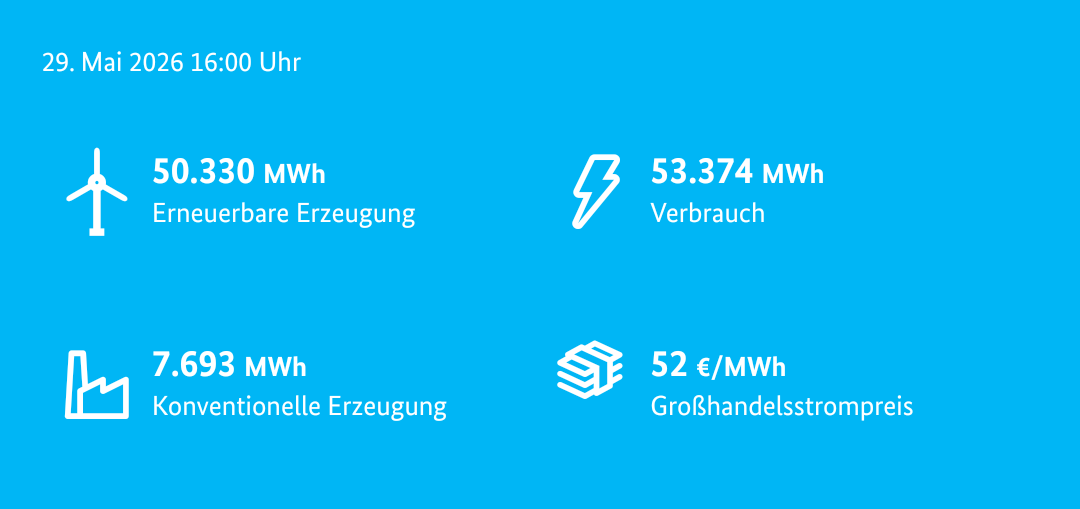

Except there will be no one to export to because every country with solar and wind will be in a similar position. The biggest challenge isn’t having enough renewable energy, it’s balancing the grid and providing enough power when there is no wind and the sun isn’t shining.

May 30

Yesterday, almost the entirety of Germany's electricity needs were filled by renewables.

Germany produced 50k MWh in renewable electricity and used up 53k MWh. Fossil sources made up only 7k MWh.

Meaning Germany is not only self sufficient but can now EXPORT electricity.

1

52

Scip retweeted

May 30

After years of searching and hope, the Commission for Missing Persons announces that the children of the Abbassi family didn't survive.

They were forcibly disappeared by Assad's Intelligence in 2013.

Surviving relatives were informed and out of respect for the family's privacy, no visual documentation will be released to the public.

tensofthousands.amnesty.org/…

الهيئة الوطنية للمفقودين:

📌توصلنا إلى نتائج موثوقة ومتقاطعة تؤكد وفـ ـاة أطفال الدكتورة رانيا العباسي

📌لا تزال جهود البحث للعثور على الـ ـرفات مستمرة

📌لن ننشر أي مواد بصرية أو معلومات من شأنها المساس بكرامة الأطفال أو انتهاك خصوصية العائلة نظرًا للحساسية الإنسانية البالغة لهذه القضية

17

101

348

89,966

Scip retweeted

May 24

JNIM is not HTS and Mali is not Syria. The group histories and local contexts are different. Most notably, JNIM is still al-Qaeda and HTS stuck to Syria. JNIM operates its insurgency across multiple states. Once you get to specifics it falls apart.

May 24

Syria showed them what is possible. This does not mean that JNIM will do it to the letter, but it proves that there is a pathway to power. Though, one way or another, they will have to make concessions and enter into deals with others @Jacob_Judah @FT ft.com/content/c19f91a1-3e19…

7

49

265

45,735

Scip retweeted

May 23

Industries that are wiped out by state supported Chinese competition (now aided by an undervalued currency) do not innovate -- Europe and the US missed out on 20 years of "process" innovation in rare earth refining when that industry disappeared

6/

1

5

53

15,650

Scip retweeted

May 23

The unique feature of China's economy today is how unbalanced it -- there has been massive expansion of exports, with no offsetting rise in imports. This is something that Dr. Draghi, based on his writing and speeches, understands well

2/

2

6

28

2,749

WSJ reported that Anthropic is expected to turn profitable in Q2 of this year.

AI’s growth trajectory is insane. And this is not just growth that burns cash — it is growth that generates an enormous amount of money.

Look at this. Anthropic’s previous forecast was that it would not become profitable until 2028.

Even they themselves failed to predict the magnitude of their own growth.

OpenAI needs to move faster.

42

78

636

125,173

I was in southern Egypt 5 years ago and there you have Nubian villages where women wear the niqab and the men listen to Bob Marley and smoke hashish.

May 16

His wife literally wears a niqab you fucking dolt, there is no interpretation of Islam that isn’t on the extreme end that does that.

1

231

Scip retweeted

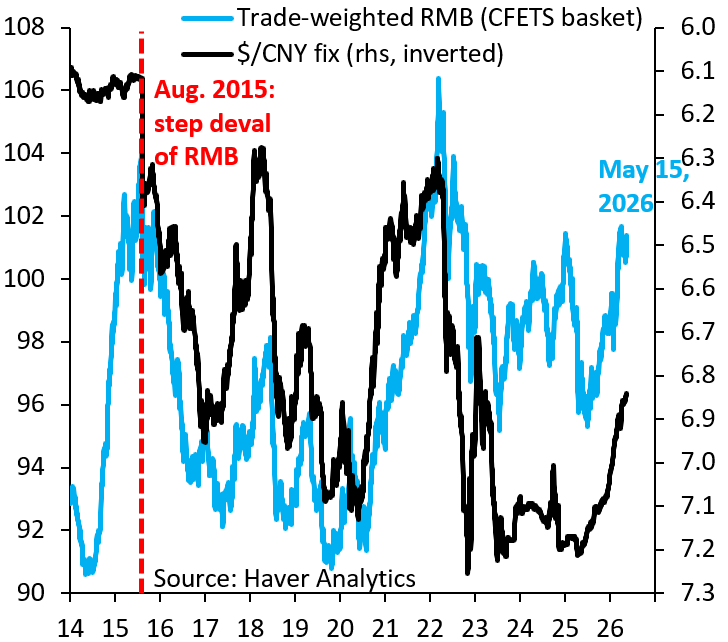

The RMB Trap: How China Makes the World Pay for Its Mercantilism

China is not trying to win a fair productivity race. It is trying to lock the world into structural dependency on Chinese industrial capacity, while pushing the adjustment burden onto everyone else. The result is simple: China exports deflation, absorbs global demand, and forces others to carry the cost.

May 15

The single best thing China can do for the world is to allow the massively undervalued RMB to rise, but it'll never do that. RMB is just a function of China's mercantilist growth model that takes growth for itself from everyone else. That'll never change.

robinjbrooks.substack.com/p/…

6

11

40

16,246

Pretty bad that tokens are too expensive for many and yet AI companies are selling tokens at a steep loss. AI is going to be revolutionary but it also seems like it's moving too fast to make a profit. AI companies want the best models but it's hurting the economics.

May 9

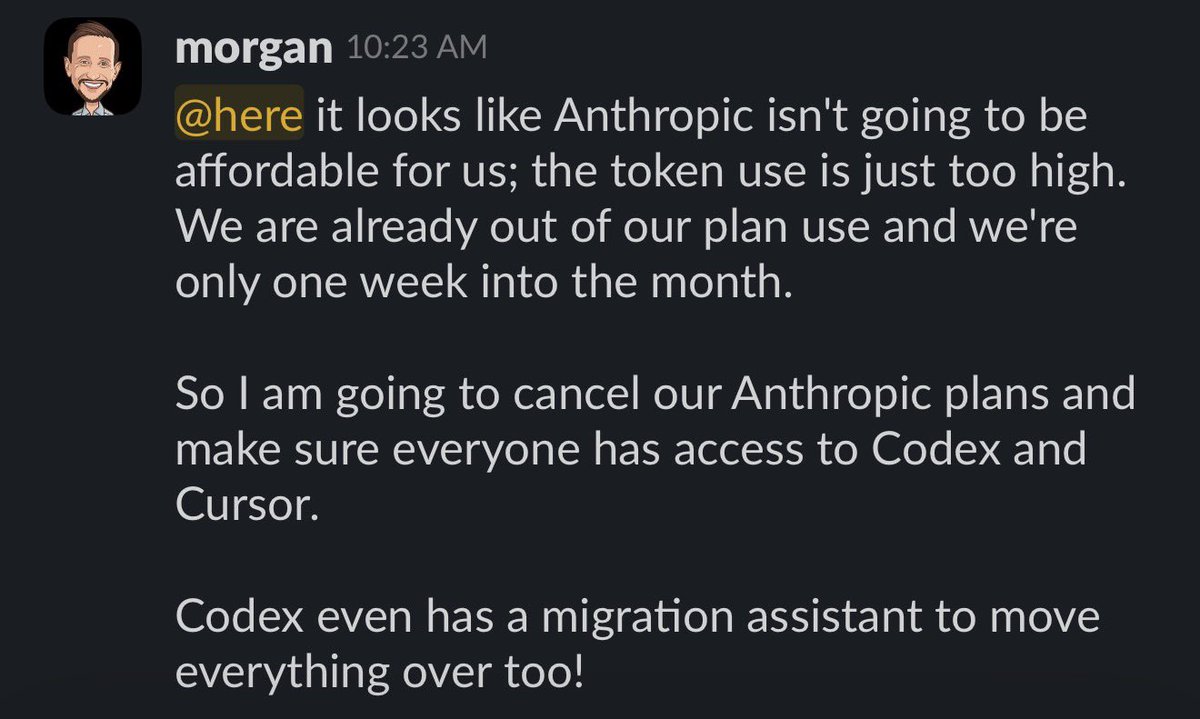

Officially canceling our Anthropic plan, it’s Codex Cursor for my little 16 person eng team.

Anthropic is great for companies that can spend $2,000/mo and up per engineer, but not affordable for us.

Codex really upped their game recently, and with GPT 5.5, it’s just so good, and so token efficient.

Still using Cursor plenty, my team still looks and reviews a lot of code.

But with Cursor, we’ve never hit a limit, and Composer 2 is pretty awesome for most stuff.

Testing out Droid as well and see some good early results with Droid GLM 5.1, but still more testing to do before rolling it out to the whole team.

My guess is many more engineering leaders will be sending messages like this. Anthropic makes great stuff but phew, it’s so darn token hungry.

My team loves Codex and Cursor, onward!

2

215