Joined June 2007

- Tweets 21,667

- Following 2,437

- Followers 7,903

- Likes 15,264

1,445 Photos and videos

Pinned Tweet

8 Sep 2021

Always have a plastic mind, you can learn anything — like playing cricket on a turf with a tennis ball 😀

6

1

41

😂😂😂😂

Dear US government,

Since you've just blocked Fable and Mythos on critical national security grounds, here are some other tools that pose a similar threat to the American people:

- Microsoft Teams

- SAP

- Salesforce

- Jira

- Outlook

Please do what you must to save America 🇺🇸

380

Indus Khaitan retweeted

I’ve had a number of conversations with folks inside and outside government about the current situation with Anthropic, and here is what I believe to be true:

— As we know, Anthropic publicly released its Mythos class models earlier this week under the commercial name Fable.

— Fable is Mythos with guardrails. But if those guardrails fail, then you’ve exposed Mythos and its advanced cyber capabilities to people who shouldn’t have them. (Keep in mind that Anthropic itself widely promoted the idea that Mythos was a cyberweapon and needed to be regulated as such. They asked for government regulation of Mythos and championed the guardrails on Fable. If there is a vulnerability — big or small — it is Anthropic’s responsibility to patch.)

— A highly credible trusted partner of both Anthropic and the USG who was testing Fable came forward with a jailbreak of those guardrails. The Admin asked Dario to fix the jailbreak or de-deploy the model. Dario refused.

— In their blog post, Anthropic defended its decision by saying the jailbreak isn’t serious. That is not what the trusted partner and the USG believe; nor is that kind of minimizing language consistent with Anthropic’s brand as the AI safety company. It’s difficult to fathom how they could claim a jailbreak allowing operability of a cyber weapon could be defined as not “serious.”

— In the past, Anthropic has always said that safety must be top priority and taken super seriously. In this case, Anthropic prioritized the continued offering of the consumer model over safety.

— In reaction, the Admin issued the export control. The Admin did this reluctantly. It’s been very surprised that Anthropic hasn’t wanted to cooperate with a reasonable safety request (ie fixing the jailbreak issue). Anthropic’s reaction is very much at odds with their branding and ethos as a safe AI research community.

— The Admin’s hope now is that Anthropic remediates the safety issue, the export control is lifted, and Fable goes back into general release. The Admin wants all of this to happen as soon as possible. It is frankly bewildered that Anthropic hasn’t wanted to comply with safety requests that it previously said were its highest priority.

— Those trying to misdirect and tie this action to the prior DoW/Anthropic issues are wrong. The Admin values Anthropic’s technical capabilities and feels that this issue, while serious, should be easily resolved. The ball is in Anthropic’s court.

1,915

2,814

21,976

5,944,849

16h

👀

‼️🚨 BREAKING: Amazon researchers snitched to the US government about jailbreaking Fable 5 and Mythos 5, forcing Anthropic to immediately shut down worldwide access.

A security export control directive from Commerce Secretary Howard Lutnick enforced the action.

Anthropic is fighting the directive and calls it a misunderstanding.

This isn't the first clash. The Trump administration had already tried to get Anthropic to pause the release of its latest models before this directive landed.

73

Indus Khaitan retweeted

Jun 12

I cancelled my $10/mo Calendly subscription and vibe coded my own with Fable for $12,000

466

612

19,245

960,336

Jun 12

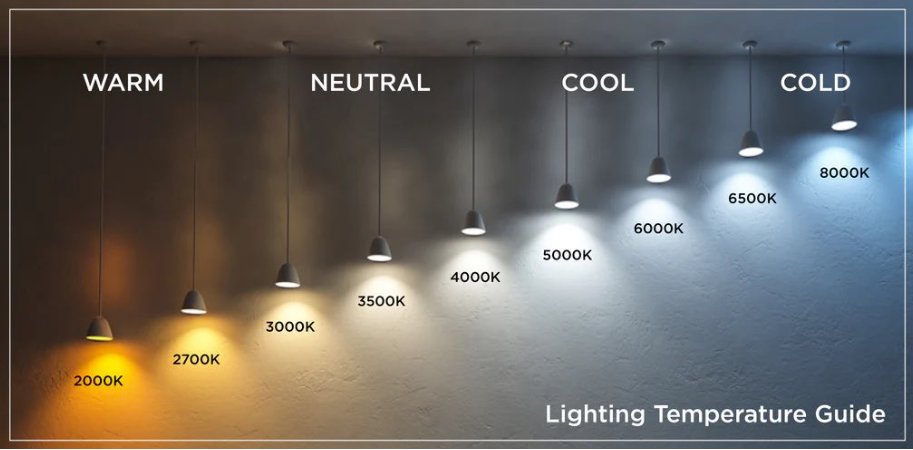

In India light separated societies. Not sure about now but in the 90s it meant:

- rich = white / tube light

- poor = warm / bulb

Having a white light was an aspiration for many homes.

This habit is carried over even in the immigrant families here in the Bay Area.

Jun 11

You can figure out everything you need to know about someone by their home lighting temperature

1

2

415

Jun 12

While you are worrying about cost of tokens, it takes $1400 to rent a 55' inch TV for 2 days at an event in LAS.

I'd rather buy a TV for $300, plus rent a Jeep Wagoneer for $700 for 5 days and also not pay $500 for a roundtrip ticket from OAK -> LAS.

It is 95 eff degrees and that is the decision point.

2

3

775

Jun 12

The real world is not venture subsidized.

It is heavily monopolized.

It is regulatorily captured.

It is unionized.

1

1

287

Jun 11

Devs are lazy for inconsequential code.

If his site was running on movable type -- it would still be.

Jun 10

dario's personal site runs on webflow, meanwhile you're vibecoding your own site and cms

#interesting

75

Jun 11

Is Dario playing a few pages from Peter Thiel's Zero-To-One?

Jun 10

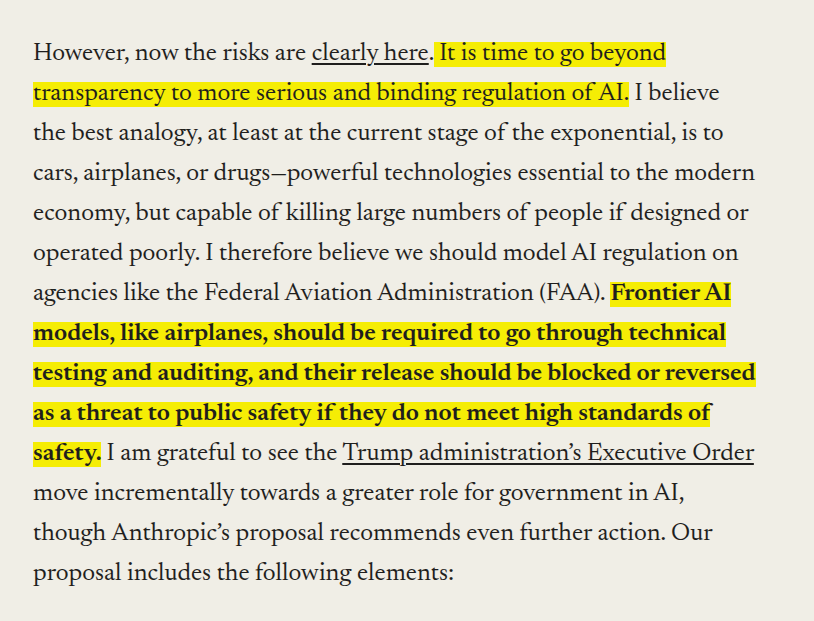

Dario Amodei just published a super long blog, calling for an urgent policy overhaul because he thinks frontier AI is moving faster than governments can regulate it.

He wants:

- Mandatory pre-release testing and independent auditing of frontier AI models, with government power to block deployment when models pose serious cyber, biological, autonomy, or automated-R&D risks.

- Stronger security rules for AI companies, including protection of model weights, regular red-teaming, penetration testing, and rapid reporting of critical safety incidents.

- He wants governments to prepare for AI-driven labor disruption through better measurement, pro-employment incentives, wage support, training, and possibly long-term income support funded by AI-driven growth.

- Democracies should coordinate globally on AI safety, chip supply chains, export controls, shared benefits, mutual defense, and safeguards against AI-powered repression.

146

Jun 10

I think about this a lot!

I wish the b-schools are doing economic studies around this topic. This topic could also be a fodder for a large prize in economics.

"How not going IPO hurts the ecosystem, reduces ambition, slow burns the founder, increases competition, and does not create wealth for all."

Jun 10

stripe should’ve gone public in 2016 and started acquiring startups like google and fb did early on

they should’ve acquired mercury, ramp, & plaid at the very least

generational missed opportunity

368

Indus Khaitan retweeted

Jun 9

The male urge to move to a small town, reinvigorate its economic engine, improve the quality of life for the people, be well-liked by his neighbors, and raise a family in a community of which he’s become a pillar away from the nonsense and excess of big cities and loud societies.

Jun 8

I have a friend that did this. Bought an industrial park with a near by airport in a small town in Georgia for his growing telecom biz.

He's been there about 6 years now and owns most of the town now.

Runs the movie theater and let's his kid pick out what movies to play, owns a couple restaurants, bed and breakfasts and clothing shops.

I went up there a couple times and the town loves him. He's like a celebrity, lol.

2

4

57

14,845

Indus Khaitan retweeted

How could this be perceived as anything but a massive failure in today’s world? Would Stripe even be investable today? Which investors would ever think that only launching after two years of work and with 50 users would ever be the beginning of something gigantic?

I can’t see how anybody would be happy with this today. And yet, almost imperceptibly, Patrick and John were painstakingly laying the foundation for something that was built to last and built to grow strong and immovable like a Sequoia. How can mushroom growth rates produce anything other than mushroom longevity?

I’m not saying that real value CAN’T be built quickly. But I think it’s far more common than we like to talk about that founders work for two, three, four, seven, even fifteen years before something extremely valuable is born into the world and really takes off.

James Dyson worked on the design of his vacuum cleaner for 5 years before he got to a working prototype and 8 years before it became a commercial product.

Dylan Field worked on Figma for four years before launching a *closed* beta.

Tim Leatherman worked on his idea and prototype for 8 years before he had his first multitool design that was ready to sell.

Palmer Luckey spent about 7 years from the time he began working on VR prototypes before Oculus released the first consumer headset.

Jensen Huang started Nvidia in 1993 and it wasn’t until 4 years later in 1997 that they had their first major commercial success with the RIVA 128.

Steve Wozniak was the fastest and went from an idea for a personal computer in 1975 to the Apple II release 2 years later in 1977.

Time and again the reality is that great things take time to build. I’m not saying it doesn’t take hard work. I’m definitely not saying it doesn’t take determination and extreme focus. But it does take time. I think we try and pretend that it doesn’t take time and lift up the seeming exceptions to the rule.

Why not be honest and instead focus on the determination and extreme grit that it takes to keep building for years before any outward success arises or glory is received?

I hope we can be honest with young founders and repeat these stories again and again so that they learn to work thanklessly for years before the outward vindication comes, because that’s what it really takes.

John Collison: We only had 50 users two years after founding Stripe

“We started working on Stripe in the Fall of 2009, and we launched Stripe in September 2011,” John Collison reflects. “I remember right at the beginning when we were starting it I said to Patrick [Collison], ‘Yeah let’s do it. How hard can it be?’ Which gives you a sense of our mindset. And the answer was: two years of difficulty. We had not predicted that.”

John remembers feeling dejected when Stripe only had 50 users two years later:

“When you spend two years getting 50 users, it doesn’t feel like a whole lot of progress. It feels like things are going pretty slow.”

But this is one of the challenges of startups, he argues:

“If you’re working on a startup that’s a bad idea, it’s going to feel like slow-going. But if you’re working on a startup that’s a good idea, it may feel like slow-going too.”

Yet slow growth has a silver lining:

“I think the thing that allowed us to take off in the subsequent years was the fact that since we were spending so much time on each one of those users; since we were hyper-focused on building a great product; and since we weren’t dealing with problems of scale yet, that allowed us to build the product that we wanted. Part of the culture that set in really early on was taking abnormally good care of those early users.”

The Stripe founders would get an email or phone call anytime a user ran into a bug. When they sent the customer an email moments later alerting them that the bug was now fixed, people’s minds were blown.

They set up a Campfire room that any customer could join and use to message John and Patrick at any hour of the day or night. And if a user was based in the Bay Area, the founders would invite them to come by the office and help integrate Stripe for them.

In the Stripe dashboard they would prompt their customers for feedback and feature requests. Then the Stripe founders would reply to that feedback within 10 minutes.

“What this meant was that even though the user growth was happening quite slowly in the early days,” John explains, “it actually had a pretty surprising viral effect where people had a good experience, they told their friends about it, and we were able to spread entirely through word-of-mouth even to this day.”

39

77

941

219,154

Indus Khaitan retweeted

Jun 7

Slow Inference Has Zero Market

Andrew Feldman, Co-founder and CEO, Cerebras, interviewed by @saranormous and @eladgil (No Priors)

Summary: Cerebras went public at $63 billion with a $20 billion-plus OpenAI backlog after spending eight years convincing the industry that GPUs were the wrong architecture for AI inference. Andrew Feldman argues that speed creates new business categories. Fast internet turned Netflix into a movie studio. Fast AI will do the same to workflows we now think of as fixed. The lesson for operators: a 20x speedup requires a different architecture, the chasm between technical proof and market demand can be a multi-year burn, and the companies winning right now treat their old "speed of light" assumptions as soft limits.

1. The Netflix Test. Speed creates new business categories, the way fast internet turned a DVD-by-mail company into a movie studio. Bandwidth opened up an entirely different business for Netflix. The market for slow inference will end up where dial-up and slow search ended up: at zero. Right now AI is still in the "deliver DVDs faster" phase of its potential.

2. Wafer-Scale Bet. A 15 to 20x speedup over GPUs requires a fundamentally different architecture. Cerebras built a 46,000 square millimeter chip the size of a dinner plate while every competitor was building chips the size of postage stamps. Gene Amdahl tried wafer-scale and failed; the rest of the industry called it impossible. The general principle: a 20x improvement requires a design that looks unlike anything that came before.

3. The $8m-per-month Years. From 2017 to mid-2019 Cerebras spent $8 million a month with no working chip and held a board meeting every six weeks to report "still not working." Each failure analysis got the team slightly closer. The chip yielded in summer 2019, and the founders sat staring at it for half an hour because no one had ever done it. That is what hardware conviction looks like measured in cash.

4. Two Years Too Early. Cerebras solved one of the hardest problems in the computer industry and then watched two years pass with almost no one caring. Gen 1 sold around a dozen units, Gen 2 around 300, Gen 3 will sell tens of thousands. Being blisteringly fast was worthless while AI was still a novelty, because nobody uses a novelty every day. The gap between "we built it" and "the market wants it" decides whether deep-tech companies live long enough to enjoy being right.

5. Bridging The Chasm. New compute architectures usually start with supercomputer customers who love speed and tolerate immature software. Cerebras ran the table at the National Labs, then won oil and gas and pharma, then sovereign G42 placed a $1 billion order. That capital let them rebuild the supply chain and battle-test at scale, because you cannot put $100 million of your own gear in a QA lab. By the time OpenAI and AWS showed up, the capacity was ready.

6. OpenAI In 4.5 Weeks. A $20 billion-plus deal went from "first conversation with Sam" to signed master agreement in 4.5 weeks. Term sheet the night before Thanksgiving, master agreement on Christmas Eve, working seven days a week with multiple law firms. Feldman's takeaway: many of the timelines he assumed were the speed of light in dealmaking were soft. Operators in this market are compressing M&A, financing, and data-center build-outs at the same time.

7. The Professional David. Cerebras is Feldman's fifth startup, and every one has been a David against a Goliath. He frames it as identity: if his mother could buy the product, he does not want to make it. The hard part is loving the underdog role for a decade, well past where most founders quit. If you do not love being a David, do not pick a fight with Nvidia.

8. $30K Of Tokens Per Engineer. Eight months ago Cerebras spent under $1,000 per engineer per year on inference tokens; today it is $25 to $30,000. The engineers who have figured it out run eight or ten agents around the clock, with their own QA agents to compensate for known coding-model weaknesses. They went from 10x to 100x. Most people, Feldman included, are still limping along trying to figure out the workflow.

9. The IPO Trade. Going public swaps technology-savvy venture investors for "my dad" in exchange for a slightly lower cost of capital and a much heavier compliance burden. The new wrinkle: three or four companies, OpenAI, Anthropic, Databricks, can now raise public-market sums in the private market. Everyone else still needs the IPO for legitimacy and the right to sell into public-company procurement. Cerebras had something no one else could offer: the only AI pure-play on the market, with 100% of revenue coming from this exact category.

10. The 1,000-Person Malaise. Companies between 1,000 and 3,000 people quietly stop taking the risks that built them. The culture shifts from "what extraordinary thing can we attempt" to "what can we ship in the next rev." Feldman's stated preference: rather fail in pursuit of the extraordinary than succeed in the ordinary. The corollary is recruiting discipline, because putting a butt in a seat to clear a req is death.

11. When To Quit. The honest moment to stop is when you laid out hypotheses for what it would take to win and every one came back negative. The trap is doing this sequentially, "let me test one more thing," and the slippery slope is a beast in business the way it is in ethics. The defense is other former CEOs who remember what you committed to a year ago and pull you back from the warm water before it boils. Articulate what has to change, put a time frame on it, and let someone hold you accountable.

12. Open Source As Oxygen. Open source kept AI research alive when closed-source frontier models were too expensive to use, and now it pressures the leading labs to stay ahead of techniques shipped out of Chinese projects. The result is an active ecosystem where other people's ideas do interesting things on your hardware. Feldman's filter: if you do not love watching other people's ideas take flight on what you built, the infrastructure business is not for you. The flame stays alive because someone keeps pushing the closed labs.

36

14

131

27,181

Jun 6

my iPhone takes pictures and 99% of them are poorly shot, unsharable.

so should be apps.

1

1

149

Jun 5

Really like the way Eric is thinking about this.

At quolum, we attempted solving this conundrum in SaaS spend -- tool A vs tool B. But, it was hard to recommend a specific tool just on spend, without any qualitative benchmarks.

But now for specific models -- the benchmarks are a clear answer.

Route to a cheaper model that ranks around the same on a task benchmark compared to a state of the art.

Jun 5

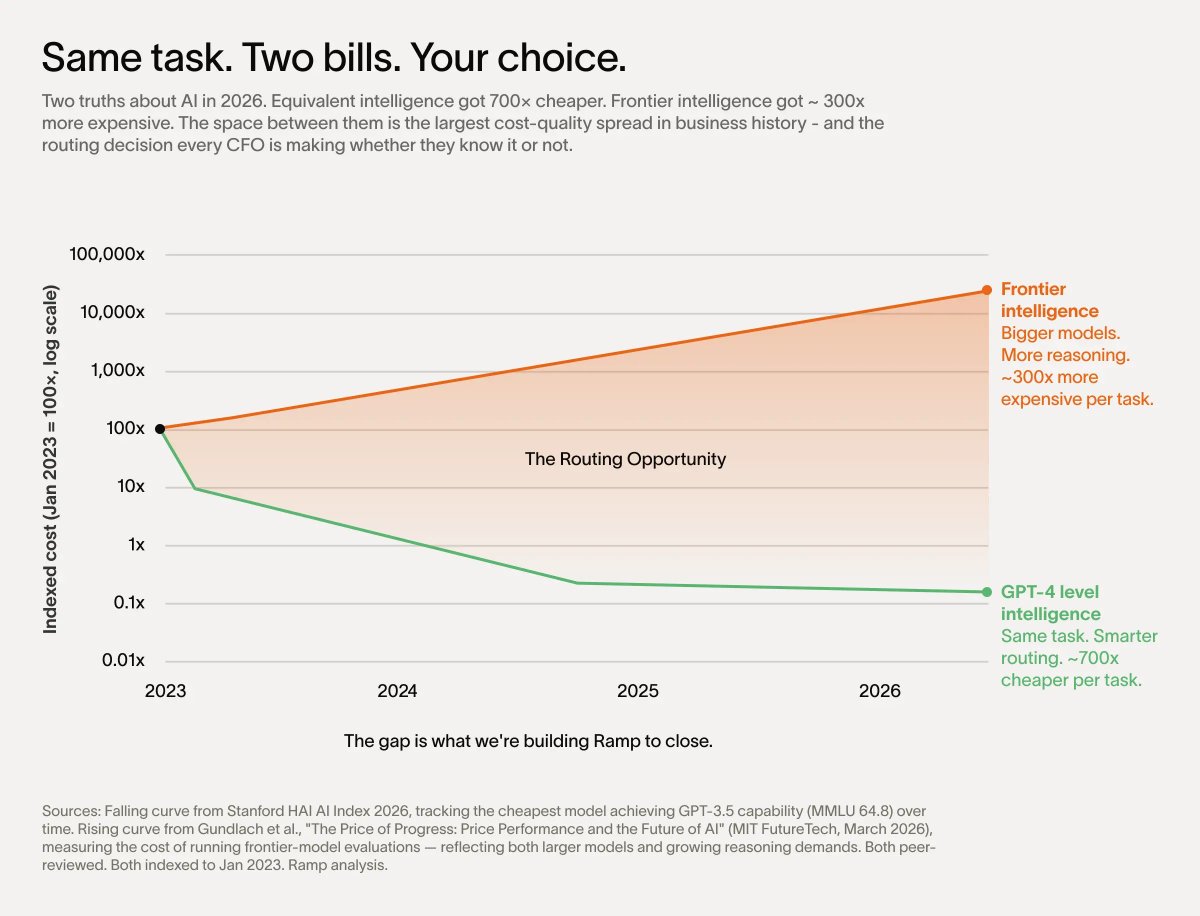

As I wrote this, I saw X go into meltdown over tokens.

You've seen the headlines: “Uber blows yearly AI budget in just one quarter.” “Meta employee burns 281 billion tokens in April.”

But, the problem isn't spending. Spending works. Since 2023, the top quartile of our AI spenders doubled their revenue. The bottom quartile? Flat.

It's blind spending. We don’t know which spend worked.

A sales team has qualified leads. A support team has resolved conversations. These are units you can measure against. All a token tells you is the meter ran, not whether the work was worth it or not.

Finance says, “half the budget,” engineering says, “double it” and you don’t know who’s right because there is no shared language of value. There’s no attribution, and no attribution means no allocation.

For example, right now, all work, no matter the size or shape, defaults to frontier models. But meeting summaries and calendar updates don’t require GPT-5.5 Pro.

In isolation this seems trivial, but re-route just 10% of a $10M AI bill from frontier to GPT-4 level intelligence you’ve saved nearly one million dollars. This sounds like a made-up stat — it’s not. It truly is that much cheaper.

This is the future of finance: not blindly rubber-stamping or rejecting AI spend, but allocating it with the same rigor companies apply to headcount.

2

175

Jun 5

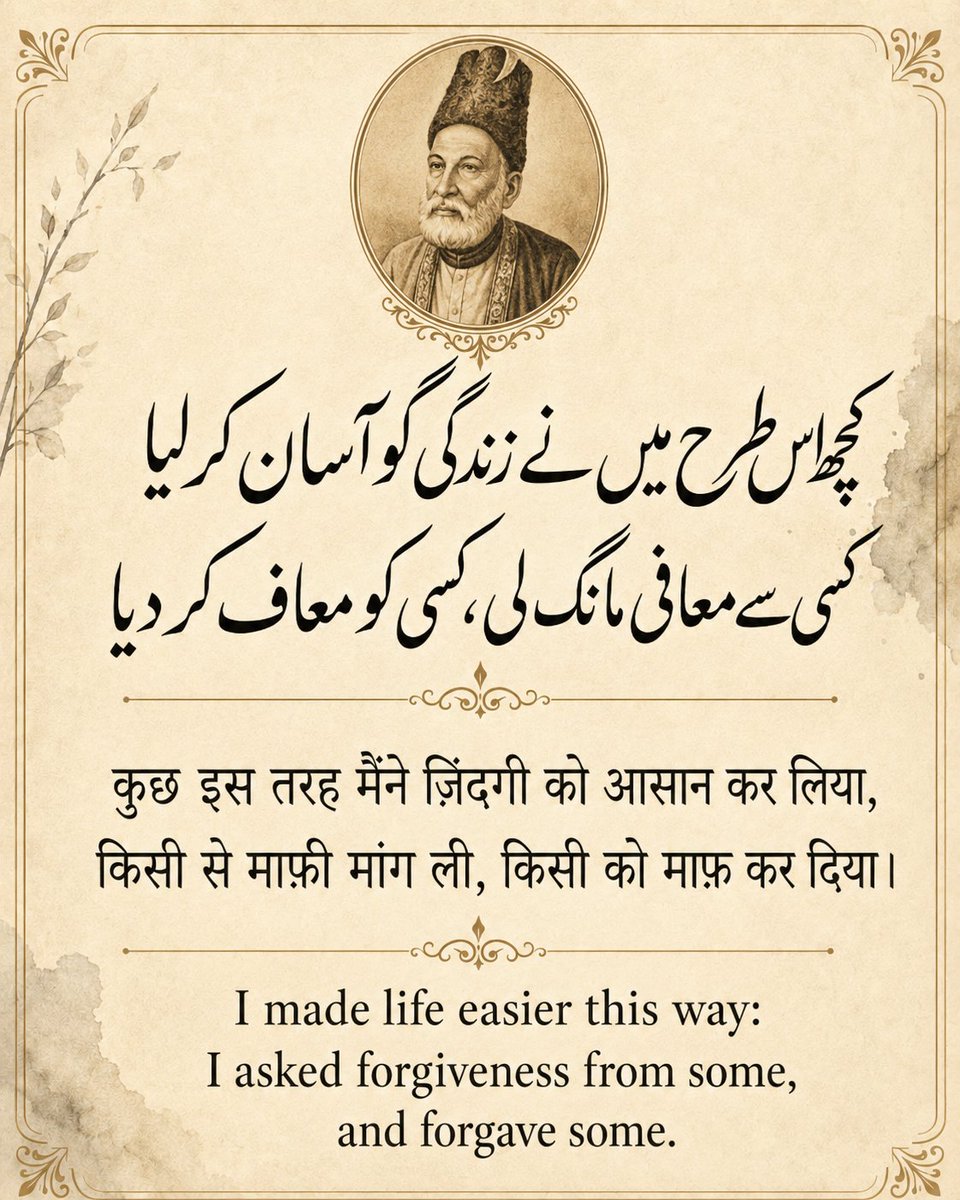

On my third startup. I keep this Ghalib as an amulet, but haven't forgotten any incidents.

My most interesting one was where I was asked,

"which IIT?" (I'm none).

Jun 3

In 2001 I intercepted a partner at a VC who was trying to escape his office before our meeting was supposed to start. I ended up pitching him in his parked Lexus from the passenger seat.

At one point he grabbed my laptop placed on his large belly which was pressed against the steering wheel and rapidly flipped through the slides himself.

2001 fundraising hit different

1

2

554

Jun 2

The below is over-generalized and certainly not true for selling to the Top 100K enterprises in the world.

Also, the death is not of the 3-act playbook. It is the gap between the acts.

Plus there’s one more thing. Distribution.

Let me explain and start with buyers.

1. Very few buyers especially with CIO/CISO title are going to say, “come, son, replace my chessboard.”

Instead, they would want you to play with their pieces.

And that’s where the wedge comes handy.

2. Big platform budgets do not exist for new products until there is a positive category signaling from analysts. This takes a few years. 99% of enterprise buyers wait for categories to mature and a few vendors to come in before pushing the RFP.

Early adopters are only 1000 or so for any category. So you can’t create a billion $ business even with large ACVs such as 250K.

3. Much of the large ACV sales plays are driven by channel & other indirect relationships. Take pao alto for example. 70% is indirect and that take years to build.

Building an indirect channel takes maturity of product and starts with a wedge that everyone is asking for.

4. Most founders are ambitious. Calling them under ambitious is disservice. Ambition is not one thing but is layered with access to capital. It is like saying that if you are currently attempting the climb to a smaller hill you are under ambitious. But given even capital the same founder will get trained with a professional, and then hire a Sherpa, ferry supplies ahead of time.

5. Last point, it is the gap between the acts that is reducing. You will still build it in acts but go out to the customer and expand the deal size with new features and adjacent products.

Aside, much of what’s getting written as wisdom requires nuance. Who does this apply to and that’s missing in the public discourse.

Aside, aside, no tokens were harmed writing this.

1

4

785