Joined August 2024

- Tweets 2,547

- Following 1,547

- Followers 139

- Likes 10,087

239 Photos and videos

AR Alman retweeted

Jun 12

Russia that is acclaimed to be the bad guys, hosted World Cup without any problem. The accuser of the brethren is hosting the worst World Cup ever.

199

2,894

14,122

145,689

انا كل يوم بيزيد حبي وتقديري للسنغال👏👏

مدرب السنغال بابي ثياو تريند دلوقتي في امر ىكا بسبب تصريحاته في المؤتمر الصحفي

الصحفي : كانت هناك رياح شديده في ولايه نيوجيرسي اليوم والامن طلب من اعضاء البعثه عدم الخروج حفاظا علي سلامتكم لماذا خرجتم للصلاه؟

بابي ثياو : وهل يوجد شيئ اهم من الصلاه؟؟ اعتقد ان هذا سؤال ليس من شأنك انت خائف من رياح ونحن نخاف من الله الذي صنع الرياح نحن هنا من اجل لعبه ترفيهيه ونسينا اننا مخلوقين من اجل عباده الله

لو كان نهائي كاس العالم اليوم ونحن طرف في النهائي لخرجنا لأداء صلاه الجمعه حتي لو كلفنا خساره البطوله لاتتحدث معنا عن شعائر تخص ديننا.

افسم بالله الواحد فخور بالسنغال وخير ممثل للقاره الافريقيه تصريحات بابي ثياو عملت جدل كبير النهارده انا مشوفتش قوه وايمان كده في حياتي الصحفي حرفيا سكت ومعرفش يتكلم بعد الكلمتين دول....انا من النهارده سنغالي👏👏👏♥️♥️♥️

731

9,709

52,725

2,131,381

AR Alman retweeted

Jun 13

You cannot bet against the man who never stopped moving.

The amount of information available to Elon Musk at a young age was unprecedented. The more high-level information you have access to, the better your leverage.

Though we can say thanks to the resourceful society he grew up in, but despite the massive rise in the internet and information today, we still don't get to see this level of structural clarity in youth at a young age running a hugely capital-intensive venture.

Looking at him back then, he spoke with so much clarity and knowledge of what he is doing, even as a young man in his late twenties and early thirties.

Why is that? At least, there is a measurable increase in access now compared to then, but why are we not seeing this kind of deep clarity and execution?

6

20

82

3,315

AR Alman retweeted

Jun 13

Bismillah Ar-Rahman Ar-Raheem

This is a Misconception. Bank Interest is Riba

One of the defining characteristics of a Shubha (misconception), is that it masquerades as deep, enlightened research. It dresses itself in classical terminology and exploits minority historical anomalies to look like the truth, precisely because it aligns with human whims and the desire for easy, risk-free returns.

To the untrained eye, it looks academic. But when the card deck is separated by those grounded in knowledge, the flaws and falsehoods are laid bare for all to see.

I shouldn’t have refuted this brother because I had initially saw what he wrote and I intentionally didnt want to draw attention to it. However, I believe the calls and tags are enough. Our people should not be swindled by this kind of deceptive wordplay.

In light of this, let me prepare your mind that this refutation will be long, and it’s purely academic. So, let us lay out his claims side by side with the true position of Islamic jurisprudence to show the clear flaws in his understanding.

(1). The first of his gaps is the currency loophole.

He said: Modern paper currency is identical to classical copper tokens (Fulus). Because early scholars did not apply the strict rules of gold and silver usury to copper tokens, modern paper money is exempt from the laws of Riba. He tried to use a narrative about Abu Dharr buying copper tokens to back this up.

When the statement above is placed under the textual lenses of the Sharia, it is clear that this is a major misunderstanding of monetary history and law.

Classical Fulus were minor token change used for cheap items like vegetables because you could not cut a gold Dinar into tiny pieces. Modern paper currency does not function like minor copper change. It has complete monetary status (Thamaniyyah). It is the global medium of exchange, the measure of value, and the store of wealth.

To show his flaw, we look at the words of Imam Malik ibn Anas in Al-Mudawwanah (Vol. 3, p. 90.) He explicitly stated that monetary value is determined by its social function as a currency, not the material it is printed on:

وقال مالك: لو أن الناس أجازوا بينهم الجلود حتى تكون لها سكة وعين لكرهت أن تباع بالذهب والورق نظرة

"Malik said: If the people were to make leather tokens legal tender among themselves, such that they possess a coin-stamp and function as money, I would strictly forbid them to be exchanged for gold or silver with any delay on credit."

He also tried to hide behind Ibn Taymiyyah,however, Ibn Taymiyyah in Majmu' al-Fatawa, Book of Fiqh, Vol. 29, p. 404, stated that when Fulus become a widely circulating medium of exchange, they carry the identical ruling of gold and silver:

فإذا صارت الفلوس أثمانا صار فيها المعنى فلا يباع ثمن بثمن إلى أجل... فإن الفلوس النافقة يغلب عليها حكم الأثمان وتجعل معيار أموال الناس

"When copper coins (fulus) become price-currencies, they carry the same underlying legal meaning, so a price-currency cannot be sold for another price-currency with a delay; for widely circulating fulus are dominated by the ruling of price-currencies and are made the measure of people's wealth."

In fact, the global consensus of contemporary jurists through the International Islamic Fiqh Academy completely closed this door decades ago. They stated in Resolution No. 21 (3/9) Third Session, Vol. 3, p. 1645:

بخصوص أحكام العملات الورقية: أنها نقود اعتبارية، فيها صفة الثمنية كاملة، ولها الأحكام الشرعية المقررة للذهب والفضة من حيث أحكام الربا، والزكاة، والسلم، وسائر أحكامها

"Regarding the rulings on paper currencies: They are fiat money possessing complete monetary value. They carry the identical Shari'ah rulings established for gold and silver concerning the laws of Riba, Zakat, Salam, and all other transactions."

Jun 10

Bismillah Ar-Rahman Ar-Rahim

Bank Interest Is Not Riba

Before discussing interest, it is necessary to clear up a common misconception among Muslims: that loans in the modern banking system are identical to the concept of a loan in the Shari'a. In reality, the Shari'a definition of a loan does not exist within the current banking system.

A loan (Al-Qard) from an Islamic perspective is a transaction where one person provides another with something of financial value purely as a favor. It does not imply the permissibility of unlawful usufruct, and the condition is that the lender will receive back only the equivalent of what was originally given, no more, no less.

This concept differs significantly from the loans provided by banks. Bank financing is not a favor; it is a business transaction. It typically takes the form of Al-Qirad (القِراض), a classical Islamic term synonymous with Mudarabah (المُضارَبة), which is a partnership where one party provides capital and the other provides labor/management, or general Finance (التمويل), which is the activity of managing, allocating, and investing funds to achieve productive or consumer goals while establishing a clear mechanism for repayment. Since banks are not charitable organizations, they cannot be accused of exploiting the weak in the same way a predatory lender would.

In Islamic Shari'a, there are 25 recognized types of financial transactions, whereas the conventional banking system utilizes over 70. Crucially, it is the true nature and substance of these transactions that must be evaluated, rather than their superficial labels. As the legal maxim states: “العبرة بالحقائق لا المسميات” (Regard is given to the core realities, not to the names or terms used).

Ibn Taymiyyah explained in his work that introducing new forms of transactions beyond these 25 classical models is entirely permissible. Consequently, we should not constrain ourselves by trying to fit every modern financial instrument into one of these 25 traditional archetypes. Instead, we must analyze the true economic nature of new transactions and ensure they align with Islamic principles. Hence, they are governed by the fundamental legal maxim:

“لا ضرر ولا ضرار”

(There should be neither harming nor reciprocating harm).

The Misunderstanding of Terminology

Much of the confusion stems from the use of shared terminology, similar to the history of coffee (Al-Qahwa). Historically, the word Al-Qahwa was one of the many names for alcohol. When people asked scholars about the ruling on Al-Qahwa, they received a verdict of Haram. This continued for over a century until Sheikh Zakariyya Al-Ansary (author of Lubbul Usul) decided to investigate. He gathered ten students from Al-Azhar and prepared Al-Qahwa for them without their knowledge. As they drank and discussed knowledge, he observed how sharp and sound-minded they remained. He concluded that this was not the alcohol previously prohibited, and he distinguished it by renaming it Qahwatul Bunn.

A similar scenario occurred with photography. For over a century, it was forbidden in the Islamic world because it shared the same Arabic name as carving sculptures (At-Taswir). Eventually, the Mufti of Egypt, Muhammad Bakheet, who was among the most knowledgeable of the Muftis in Egypt's history, wrote a short book titled Al-jawabu Ash-Shafy fi Ibahati at-taswiril photography, explaining how these were two different things, despite sharing the same name.

In banking, the term "speculation" is used for both Al-Mudarabah and Al-Muqamarah (gambling). Any scholar who is asked about the ruling on "speculation" and interprets it as gambling will naturally forbid it. This is the reality regarding the word "loan" in the financial system; it does not match the legal definition of Al-Qard in Islamic law.

Defining Bank Interest and Riba

Bank interest is defined by the Bank of London as the cost of borrowing and a reward for saving. Money saved by customers is lent to other customers in need (not as a favor or charity). This money loses purchasing power over time due to inflation and other factors. Interest from the money borrowed is used to compensate the owner and restore the purchasing power of that money. In reality, it is not truly an increment on the initial capital.

However, many people confuse this with Riba, which affects loans in the Islamic sense. What then is Riba?

Riba is forbidden by the Law, and no Muslim scholar disagrees on this. In fact, whoever disputes its prohibition is on the verge of Kufr by rejecting a clear message of the Holy Qur'an.

In Shari'a, Ibn al-Arabi explains:

«أحكام القرآن لابن العربي ط العلمية» (1/ 320):

«[مسألة كل زيادة لم يقابلها عوض]

المسألة الثالثة: قال علماؤنا: الربا في اللغة هو الزيادة، ولا بد في الزيادة من مزيد عليه تظهر الزيادة به؛ فلأجل ذلك اختلفوا هل هي عامة في تحريم كل ربا، أو مجملة لا بيان لها إلا من غيرها؟ والصحيح أنها عامة؛ لأنهم كانوا يتبايعون ويربون، وكان الربا عندهم معروفا، يبايع الرجل الرجل إلى أجل، فإذا حل الأجل قال: أتقضي أم تربي؟ يعني أم تزيدني على مالي عليك وأصبر أجلا آخر. فحرم الله تعالى الربا، وهو الزيادة؛ ولكن لما كان كما قلنا لا تظهر الزيادة إلا على مزيد عليه، ومتى قابل الشيء غير جنسه في المعاملة لم تظهر الزيادة، وإذا قابل جنسه لم تظهر الزيادة أيضا إلا بإظهار الشرع، ولأجل هذا صارت الآية مشكلة على الأكثر، معلومة لمن أيده الله تعالى بالنور الأظهر.»

"Ahkam al-Qur'an by Ibn al-Arabi (Dar al-Kutub al-Ilmiyyah edition)" (1/320):

[Issue: Every increase that is not countered by a consideration/repayment]

The Third Issue: Our scholars have stated: Linguistically, Riba means 'increase' (surplus). In any increase, there must necessarily be a base amount (the principle) against which the increase becomes apparent. Because of this, scholars differed as to whether the [Quranic] verse is general in its prohibition of all forms of Riba, or whether it is homonymous/ambiguous (mujmal) and cannot be clarified except through external evidence.

The correct view is that it is general, because people used to engage in trade and practice Riba, and Riba was well-known among them. A man would sell to another man for a deferred period. When the term expired, he would say: 'Will you settle [the debt], or will you increase?', meaning: 'Will you add an increase to the capital I gave you, and in return, I will grant you a further extension of time?'

Thus, Allah the Almighty prohibited Riba, which is the increase. However, since an increase, as we have established, cannot become apparent except when compared to a base amount, the increase is not readily apparent when an item is exchanged for a different genus/category in a transaction. Likewise, when it is exchanged for its own genus, the increase only becomes fully apparent through the clarification of the Divine Law (Shari'ah). For this reason, the verse became problematic for the majority, yet clear to those whom Allah the Almighty has supported with the clearest light."

The most important point is that the Shari'a defines what is affected by Riba. On this note, the currency used today, known as fulus, is not considered a usury-affected item according to the four schools of thought.

Ibn al-Musayyib, who is considered the most knowledgeable among the Tabi'un regarding finance, stated that Riba only affects gold and silver, or anything measured by scale or weight. In Muwadda Malik:

وحدثني عن مالك، عن أبي الزناد، أنه سمع سعيد بن المسيب يقول: «لا ربا إلا في ذهب أو في فضة، أو ما يكال أو يوزن بما يؤكل أو يشرب»

"And he (the narrator) narrated to me from Malik, from Abu al-Zinad, that he heard Sa'id ibn al-Musayyib say: 'There is no Riba (usury/interest) except in gold or silver, or in what is measured or weighed of that which is eaten or drunk.'"

The Prophet (SAW) mentioned items affected by Riba in his Hadith:

قال رسول الله صلى الله عليه وسلم: "الذهب بالذهب، والفضة بالفضة، والبر بالبر، والشعير بالشعير، والتمر بالتمر، والملح بالملح، مثلا بمثل، يدا بيد، فمن زاد أو استزاد فقد أربى، الآخذ والمعطي فيه سواء."

"The Messenger of Allah (peace and blessings of Allah be upon him) said: 'Gold for gold, silver for silver, wheat for wheat, barley for barley, dates for dates, and salt for salt, like for like, equal for equal, hand to hand (immediate exchange). Whoever increases or asks for an increase has engaged in Riba. The taker and the giver in this are the same.'"

Any item not mentioned in the Hadith can only be subject to these rulings if it shares the same legal reason (‘illah) through Qiyas (analogical reasoning). Scholars after the four Imams, majorly after the oil embargo, tried to include fulus in the rulings of gold and silver, arguing that it is now used for trade. They overlooked the fact that fulus was in use during the time of the Prophet (SAW).

Ibn Kathir, in his Tafsir, mentioned how Abu Dharr (RA) differed with other companions on the meaning of the verse:

«والذين يكنزون الذهب والفضة»

(And those who hoard gold and silver...).

He held the opinion that whoever kept gold or silver in his possession without giving it out in charity had fallen under Allah's curse. The companions cautioned him, telling him that was not the intended meaning. Mu'awiyah (RA) tested his conviction by giving him his share from the Baitul-Maal. Imam Ahmad reported:

> وقال الإِمام أحمد عن عبد الله بن الصامت رضي الله عنه أنه كان مع أبي ذر، فخرج عطاؤه، ومعه جارية، فجعلت تفضي حوائجه، ففضلت معها سبعة، فأمرها أن تشتري به فلوسًا»

"And Imam Ahmad narrated from Abdullah ibn al-Samit (may Allah be pleased with him) that he was with Abu Dharr when his stipend arrived. He had a slave girl with him who used to take care of his needs, and there remained with her seven [units of currency]; so he commanded her to buy *fulus* (small copper coins) with them."

This shows that fulus was in circulation, and that Abu Dharr knew the rulings of gold and silver did not apply to fulus, which is why he ordered her to exchange the currency for them.

In essence, since the Shari'a did not include fulus in the list of items affected by Riba, no one else can. This is what Ibn al-Arabi meant by:

وإذا قابل الشيء جنسه لم تظهر هذه الزيادة إلا بإظهار من الشرع.

"And when a thing is exchanged for its own kind, this increase does not become apparent except through an explicit declaration from the Shari'a."

To further clarify this, I will mention an incident between Mu'awiyah and Umar (RA). When Umar appointed Mu'awiyah as his Governor in Syria, Mu'awiyah wrote to him:

إني وجدت أموال أهل الشام الخيل والرقيق. فكتب إليه عمر أن دعهما. فاستشار عثمان فقال له مثل ما قال عمر.

"'I found that the wealth of the people of Syria consists of horses and slaves.' So, Umar wrote to him [instructing him] to leave them [untaxed]. Then he consulted Uthman (RA), and he said to him the same as what Umar had said."

Mu'awiyah wanted them to pay Zakah, but because the Shari'a did not impose it on horses and slaves, no one is allowed to.

Sheikh Abubakar Mahmud Gumi said:

﴿ يَمْحَقُ اللَّهُ الرِّبَا ﴾ ينقصه ويذهب بركته ﴿ وَيُرْبِي الصَّدَقَاتِ ﴾ أي يزيدها وينميها ويضاعف ثوابها ﴿ وَاللَّهُ لَا يُحِبُّ كُلَّ كَفَّارٍ ﴾ بتحليل الربا ﴿ أَثِيمٍ ﴾ فاجر بأكله أي يعاقبه.فائدة : معروف أن بيوع الربا مقيدة على عيون الأشياء الربوية لا على قيمها، فأوراق البنوك أو العملة المستعملة اليوم قيم لها في البنوك من الأملاك وإن كانت تستعمل للأثمان، فكل مبيع ثمني وليس كل ثمني ربوياً. فعلى هذا ففوائد البنوك أجور. والله أعلم.

"276: 'Allah destroys interest and gives increase for charities...'

Sheikh Abubakar Gumi said: It is well known that usurious transactions are restricted to the specific physical commodities subject to usury, not to their values. Banknotes or currency used today serve as values held in banks against properties, even if they are used as prices. Thus, every sold item has a monetary value, but not every monetary item is subject to usury rules. Based on this, bank interest [or profits] is considered wages. And Allah knows best."

Everything we have mentioned applies equally to the so-called Islamic banks. They have simply modified their procedures and renamed some of their transaction types, calling them Mudharabah and rewarding their customers with profits.

Allah knows best.

10

44

98

8,559

AR Alman retweeted

Jun 12

Kenya hosts millions of them from South Sudan, Ethiopia, Eritrea, Somalia, Rwanda, Burundi and even Nigeria yet we don't go about beating them on the streets.

Jun 11

NOT a single country in African allows illegal foreigners. Why must SA 🇿🇦🇿🇦🇿🇦 be an exception?

953

4,963

25,241

902,409

AR Alman retweeted

Jun 12

Nigerian supporters club would never have gotten the visa if we qualified. Let this be the last time the US host the World Cup. If you would not give access to the world, you have no business hosting the World Cup.

Nonsense!

Jun 12

🚨🚨| OFFICIAL: Senegalese supporters will 𝐍𝐎𝐓 𝐀𝐓𝐓𝐄𝐍𝐃 the 2026 World Cup in the USA after visa applications were denied. 🚫🇸🇳

Senegalese authorities confirmed to AFP that no official supporters' delegation will make the trip.

145

937

4,495

149,701

AR Alman retweeted

Jun 12

One time I was scared of South Africans was the time two passengers strangled an Uber driver to d£ath.

I read comments from them, they said the guy was a student and should not even be working, hence, his d£ath was justified.

Those guys are disgusting and one of the most despicable people on earth.

164

2,878

11,327

277,100

AR Alman retweeted

Jun 12

He’s trying to show them his documents, but do they even want to see?

Oh we’re fighting against “illegal migrants”, useless set of people.

482

2,665

9,563

481,629

The outcome of the marriage doesn’t have anything to do with her just having ND or being covered in niqab. Even people that has MSc and not covered still dey suffer for marriage, their partners inclusive. Businesses fails, retrenchment happens. As Muslims, Allah has predestined whatever that will happen to us, regardless of the degree you have or skills acquired.

You can advise her to learn a craft or have a small business to support herself and husband in marriage.

But my real concern is how do you want your cousin to feel if she sees this your tweet and the ridiculous negative projection on her in the CS and quotes?

My cousin just finished ND and announced she wants to get married immediately. Family said, At least get your degree first. She said no. Then we heard her fiancé wants her fully covered, and the whole family started crashing out.

After weeks of arguments, they finally called me to talk sense into her. I said, Leave her. She's an adult. Let her learn outside.

Now!! I'm the wicked one.😭😭😭

14

42

190

12,868

AR Alman retweeted

Jun 12

Thank you all. JazākumuLlāhu khayr. Āmīn.

Yesterday alone, a total of ₦499,925.78 has been raised for our dear brother. It is a lot and big thanks to everyone who sent their donations and thos who reposted so it could reach others.

There is ₦3.5m more needed. So, today, we go again. To support him and his family, please, send your donations here:

8022039083/Opay/Idris Oni

Thank you and God bless you.

Jun 11

The brother has reached out and he is someone we know and trust very well. Unfortunately, we cannot put out personal account so we do not expose his identity. He is indeed in need of urgent support, and I am openly pleasing and seeking support for this very dear brother. To support him and his family, please send your donations here:

8022039083/Opay/Idris Oni

God bless you/JazākumuLlāhu khayr. Āmīn.

4

135

160

8,339

AR Alman retweeted

Jun 11

This is the opening ceremony of the 2022 World Cup.

This was the World Cup everyone claimed Qatar couldn't pull off, but they ended up hosting arguably the best, most organised World Cup in recent memory.

The Quran recitation and the calm atmosphere gave it a unique feel never seen before.

Now, we wait to see what the upcoming tournament in North America will bring.

The bar has been set incredibly high, and it is going to take a lot more than the usual American corporate and media hype to match this level of soul and standard.

86

2,214

12,945

2,032,217

AR Alman retweeted

Jun 11

While in Makkah, I fell ill.

I was given paracetamol, our regular Nigerian brand. Nothing changed. In fact, it felt as though my condition was getting worse. Thinking it might have been one particular manufacturer, I tried another Nigerian brand. The result was the same.

I am not someone who takes medications casually. I rarely use drugs except when genuinely necessary, so I know how my body usually responds to basic medications such as paracetamol.

As we approached the end of our pilgrimage, I still had my Farewell Tawāf to perform. Feeling weak and concerned, I requested our dear Shaykh, Mansur B. Kareem, to please get me a Saudi brand of paracetamol or anything similar. The very first dose brought a relief that was difficult to ignore. Within a short time, it felt as though the burden of the illness had been lifted from me.

The experience reminded me of an incident from last year. A pilgrim who travelled with us was detained for over an hour because he was carrying a Nigerian-made Vitamin C supplement. Saudi officials found it difficult to believe that the product was indeed Vitamin C. They conducted several tests before eventually releasing him. Throughout the process, he kept explaining that the product had been purchased from one of the largest and most reputable pharmacies in Nigeria.

I am not a scientist, pharmacist, or laboratory analyst. Therefore, I cannot make any definitive claims regarding the medicines involved. There may be explanations that experts can provide. However, as an ordinary citizen and consumer, these experiences raise questions that deserve serious attention.

Millions of Nigerians rely daily on medications purchased from local pharmacies. They trust that the medicines they buy contain what they claim, are stored properly, and will perform as expected when needed. That trust is too important to be taken for granted.

Beyond business and profit, healthcare is about human lives. Every tablet, capsule, syrup, or injection may represent someone's hope for recovery, relief, or survival. There is no profit greater than safeguarding the health and wellbeing of people.

I therefore appeal to @NafdacAgency and all stakeholders in the pharmaceutical industry to intensify efforts toward quality control, routine inspections, anti-counterfeit measures, and public confidence building. Nigerians deserve medicines they can trust without fear or doubt.

May Allah protect us, grant healing to the sick, and bless all those who work sincerely to safeguard public health. Āmīn.

81

361

962

54,769

AR Alman retweeted

Jun 10

Why Christians are obsessed with Muslim women covering their bodies? You have your own women whose bodies everyone can see, and Muslims don’t have a problem with that. So why do you have a problem with Muslim women choosing to cover themselves? Are you insane? Is all the nakedness you’ve already seen not enough for you?

I think religion should be kept away from sports, players should not come to the field wearing hijab.

204

2,569

14,071

465,373

AR Alman retweeted

Jun 10

Another wife is good but women barely love men throughout a lifetime,saving and investing for old age is the only genuine safe net a weak old used man can have

1

1

3

345

Messi's face when he realized he was talking to Daníel Guðjohnsen, son of his former Barcelona teammate Eiður Guðjohnsen 😂

Messi and Eiður played together and won a treble in 2009. Now, Messi is about to play in his sixth World Cup 🤯

691

6,461

118,243

14,025,705

AR Alman retweeted

Jun 10

Good point.

But:

1. What is the incentive for 1st class and Second Class Upper if it doesn't confer any advantage after school? Everyone should just work for 3rd class then.

2. If a recruiter invites everyone, regardless of grade, to come and write their test and interview, recruitment cost will be much higher. Bigger pool of applicants > more resources required for recruitment. The grade cutoff is usually a means to keep applicants number manageable.

That said, I believe there are many low graders that are as smart as top graders, especially outside academics. And they have always proved themselves even under the current screening system. They will always manouvre their way to where the academic toppers get to, through, for example, starting in the few organizations that don't care about grade or having some extraodinary skills.

Jun 10

Students with a Third Class or Second Class Lower degree should be allowed to compete alongside First Class graduates at every level. Let competence, skills, experience, and performance speak for themselves. Not everyone starts from the same position, and academic results don’t always tell the full story

16

67

455

44,542

AR Alman retweeted

Jun 10

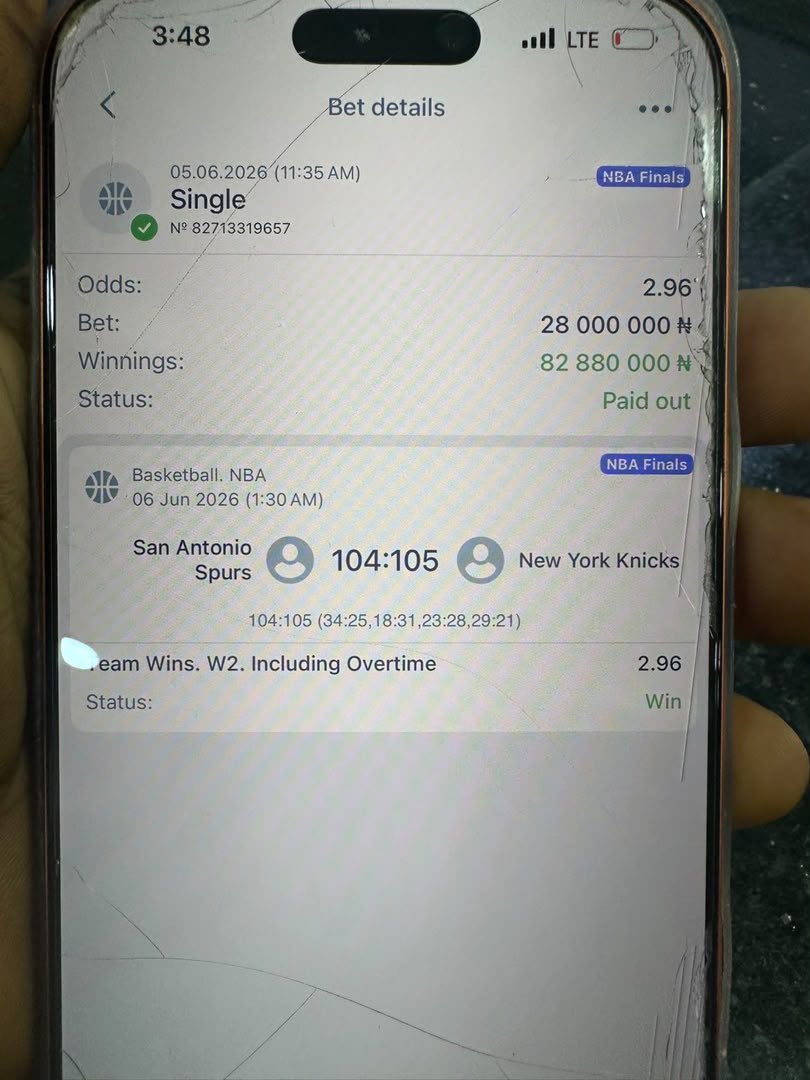

This is one of the evils of gambling in HD.

Both the gamblers and the gamblees are playing themselves.

Funny enough, these betting companies are businesses, not charities. And they are withholding that money because they cannot stomach the fact that he will cart away such a huge amount of wealth without working for it.

When you lose millions, they smile and keep quiet. The moment you win big, they pull out the verification terms, freeze your account, and lock you out.

Like I always say, gambling is not a path to wealth. If you win 10 naira and laugh today, you will lose 1,000 naira and cry tomorrow. The house always wins at the end of the day.

Halal wealth over everything €£¥>>>>>

Allah knows best.

Just in: “Nigerians please come and help me, I placed a bet of N28Million on 1xbet and I Won N82Million but I was only allowed to redraw N31Million and now 1xbet has refused to pay my remaining N51.8Million but instead Closed down my account” - Nigerian man cries out for help

9

21

152

19,106

AR Alman retweeted

Earlier today at Cairo airport, I had just led others in Fajr prayer and was about to sit down when Mallam Musharraf Aderogba beckoned to me to come over. On getting there, he asked me to engage the young man sitting next to him, who was questioning some verses of the Qur’ān that he considered to be vi0lent. I obliged him and engaged the young man. One of his issues was with Q.9:29. To begin with, I asked if his phone had internet connection, as I would be providing real and verifiable contexts to the verses. Alhamdulillaah I was able to educate him, and he agreed totally with me.

Next, I showed him verses of the Bible such as 1Samuel 15:3, Luke 19:27, Mathew 10:34-36, etc., to buttress the importance of reading contexts to religious texts, lest one ignorantly commit mischief. I told him that Jesus gave an instruction that those who wouldn't allow him reign over them be brought before him and kpai-ed (Luke 19:27). Similarly, he boldly claimed that he had not come to bring peace to the world, but to cause chaos (Mathew 10:34-36). If we put literal interpretations to those texts, without considering their contexts what does that make Jesus?, I queried.

Surprisingly, he had never read those texts before. He couldn't believe his eyes. At first, he doubted them, but I told him to look up the verses in his personal Bible. Then, he tried playing the "Old Testament" card, but I reminded him that Jesus himself said that he hadn't come to abolish the ways and teachings of the past prophets, but to fulfil them (Mathew 5:17).

Next, I brought out my phone and showed him videos of some of my Friday Khutbahs, in which I refuted Abel Damina and others like him who deliberately quote the Qur’ān out of context in order to achieve certain premeditated objectives of rubbishing Islam and criminalizing Muslims.

Next, I showed him verses of the Qur’ān such as Q.60:8 & 9 which explicitly instructed the Muslims to be kind and just in dealing with non-Muslims who are not hostile towards them or cooperative with their enemies against them. I also showed him Qur’ān 5:82 which designated the Christians as the closer in affection to the Muslims. I also showed him verses that condemn unjust taking of life, and how one life unjustly taken equals genocide (5:32), as well as the punishment for armed brigandage (5:33), among others.

Next, I asked him to mention any other country which, in the last 50 years has brought terror, destruction, and disability to the world apart from the US. Japan, Vietnam, Afghanistan, Iraq, Libya, Somalia, Syria, Venezuela, Cuba, Iran, etc. Being a Christian country, why isn't Christianity designated as a ter0rist religion? I asked him if Islam was synonymous with terr0rism, why are our people living freely and making it big in Malaysia, Qatar, Dubai, Saudi Arabia, Egypt, Turkey, etc?

In the end, we both agreed that we have a common enemy in the terrorists and bandits, and that religious or ethnic coloration of crimes is a deliberate strategy to spilt us so as to make defeating us easier.

As a Muslim, you have no business taking blame for the crimes of the terr0rists and bandits. You must never allow anyone to guilt trip or gaslight you to accepting blame on behalf of your religion. Bandits do not represent our religion or our character. They are free to shout Allahu Akbar as they wish. We cannot take the blame for their crimes which they perpetrate against innocent citizens regardless of their faith. These criminals have wasted more Muslim lives, and have more Muslims in captivity. How does that justify the bogus claim of Islamization ?

_ Sanusi Lafiagi Ph.D

13

177

383

8,739