ᴘᴇᴄᴜɴɪᴀ ɴᴏɴ ᴏʟᴇᴛ

Joined March 2022

- Tweets 6,362

- Following 1,092

- Followers 30,765

- Likes 92,392

623 Photos and videos

Pinned Tweet

13 Nov 2024

$IREN - Complete A-Z investment case

In this post I’ll cover why I expect this hyper-growth stock to crack $150 over the next 18 months—representing a gain of 1150% from its current price of $12 📈

I went ‘All-In’ this stock, and for good reason….

🧵

123

401

2,186

849,607

Jun 12

$SPCX & the Neo-Cloud Sector

Before getting into why I believe $SPCX could act as a positive tailwind for the broader neo-cloud space, let me first give you my quick take on the newly IPOed stock.

The way I see it, $SPCX is grossly overvalued, trading at an absurd P/S of well over 100. That's insane, especially when you consider they aren't even profitable. In fact, they posted net margins of NEGATIVE 26% in 2025.

In other words, $SPCX is the most expensive turd in the world.

I expect this stock to crash at minimum 50% over the coming 12 months peak to trough, and likely substantially more than that. I wouldn't be surprised to see $SPCX trade sub $1t market cap sometime next year.

That said, this seems obvious to everyone and appears to be the overwhelming consensus amongst investors.

Even most $SPCX bulls seem to hedge their bullishness by claiming to be in the stock for its "long-term" potential. Hardly anyone is bullish over the short-term.

Typically, when opinions are that one-sided, the complete opposite happens, which is what I'm expecting.

In other words, I believe the stock will follow something like this:

→ $SPCX does relatively well initially.

→ A good amount of bears and people on the fence capitulate, FOMOing in and leading to a multi-week / multi-month rally in the stock.

→ Then reality settles in, with the stock eventually crashing dramatically.

This pattern is supported by the fact that the initial float (amount of shares publicly available to trade) is incredibly tiny at sub 5%, while insider unlocks could lead to substantial selling pressure over the coming 3-6 months.

In any case, I don't have a horse in the race. I'm neither long nor short the stock. I'm just an observer.

However, as someone who is long $IREN, I do believe $SPCX could act as a strong tailwind for the broader neo-cloud sector.

Their management, namely Elon, is clearly trying to position SpaceX as an AI cloud provider, as evidenced by the recent deals signed with Anthropic and Google.

Much of the company's future revenue is now inherently tied to this segment.

Ironically, because $SPCX is this expensive, it makes the rest of the cloud sector, including pure plays like $IREN, $NBIS, and $CRWV, look cheap... comparatively speaking.

As a result, I wouldn't be surprised to see some $SPCX enthusiasm trickle over toward the rest of the neo-cloud sector.

31

29

357

34,513

Jun 10

Substack Listening Feature

A really underrated feature of the Substack app is that it lets readers listen to our deep dives as audio.

To my surprise, the AI voice we picked sounds remarkably natural and carries the tone of the writing really well.

If you're someone who likes to consume content while doing other things (commuting, household chores, working out, etc.), this feature is genuinely useful. I personally use it all the time.

The feature also lets you easily adjust the listening speed anywhere between 0.5x and 2x, which is great for tailoring the pace to whatever you're doing.

Go check it out if you haven't already!

13

3

108

8,229

Gabriel Nebreda: $IREN's hidden European edge

As you might recall, during last month's earnings call $IREN announced the acquisition of Nostrum, an emerging Spanish data center company.

Nostrum adds 490 MW of secured power in Spain and serves as $IREN's entry into the European market.

Arguably the most underrated piece of this acquisition is the key man who will now be leading $IREN's European platform: Gabriel Nebreda.

His background is genuinely impressive, and I'd argue it's exactly what this role demands:

→ 15 years at EDP, including running gigawatt-scale renewable assets across multiple European jurisdictions as Global Director of International Business Development at EDP Renewables.

→ Founded EDP Solar Spain from scratch in 2019 and built it into the leading B2C solar player in the Spanish market in under 2 years.

→ Brought into Nostrum by Andera Partners in May 2024 specifically to engineer a strategic exit, which he delivered 2 years later via the $IREN deal

The combination of gigawatt-scale renewable asset management, ground-up business building, M&A execution, and a deep European network is incredibly rare, and represents a hugely valuable asset for $IREN.

It's clear to me $IREN is in the process of building an all-star team that will enable them to scale into one of the largest cloud providers worldwide.

18

44

533

58,004

$IREN: The cloud market's dark horse

I bet most $IREN bulls are starting to get increasingly exhausted by the price action. I certainly am.

However, as long-term investors, we should see day-to-day price action as nothing more than noise.

$IREN is particularly "noisy," which makes it an especially difficult hold. Yet in times like these, it's important to step back and refocus on the company's fundamentals rather than let price action sway one's emotions.

And the way I see it, $IREN's competitive standing is rapidly improving.

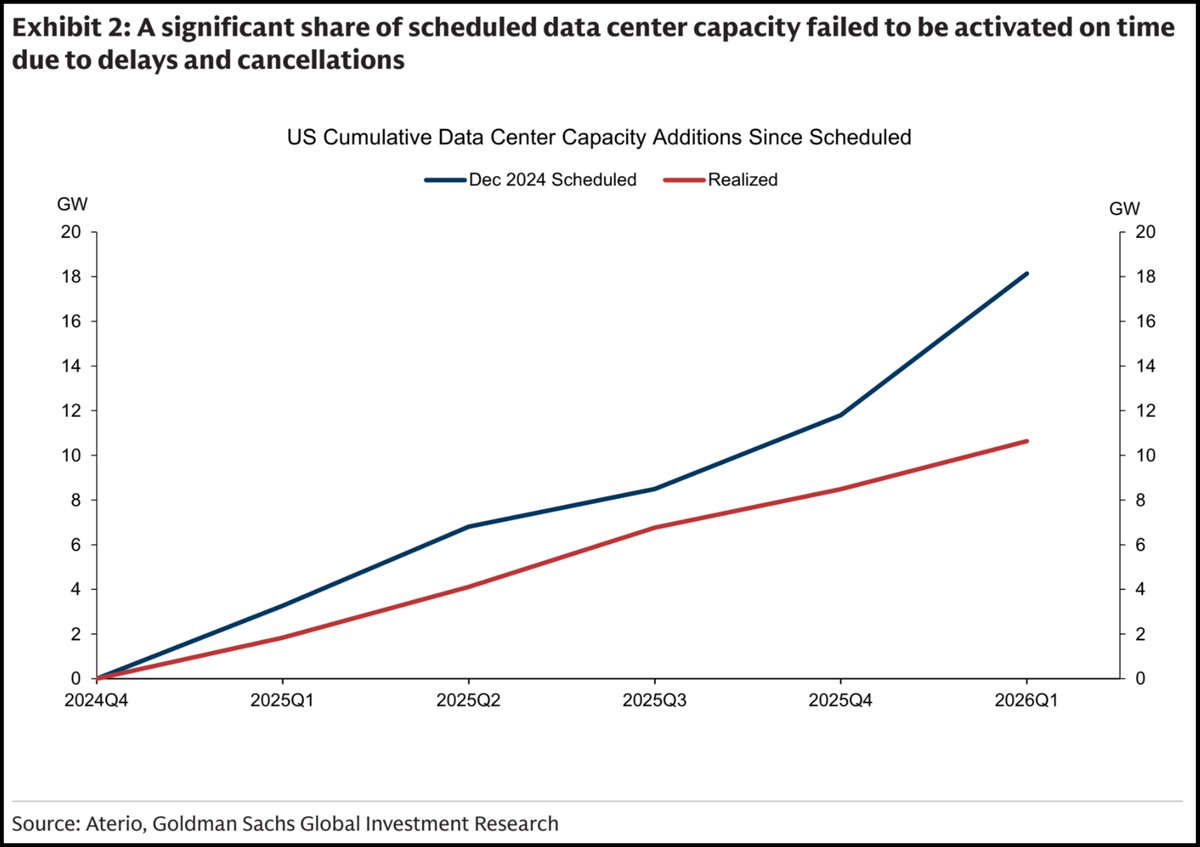

I recently came across an interesting research report by Goldman Sachs that highlighted the discrepancy between planned data center capacity and realized capacity.

Out of the ~18 GW planned to be commissioned over the past 6 quarters, only about ~11 GW actually got built.

Not only is the gap between planned and realized capacity rapidly widening, but the rate at which new capacity is coming online has actually declined over the past couple of quarters.

Much of this discrepancy comes down to power continuing to be a major bottleneck.

As grids get more and more constrained with lead times reaching 5 years, many developers are moving toward behind-the-meter (BTM) generation (on site power generation), circumventing the need for grid connectivity.

Yet that comes with its own set of problems and bottlenecks. The end result is an increasing amount of delays and outright project cancellations.

This industry backdrop plays directly into the hands of $IREN, which now has 5.8 GW of secured grid-connected power across global jurisdictions.

The only reason the industry is switching toward BTM is that it's the only option if you don't want to wait in multi-year queues to secure grid connections. But don't get it twisted, grid-connected power remains the preferred option.

$IREN is in a unique position to capitalize on this structural bottleneck and become one of the few cloud providers that can actually bring on 5 GW of compute capacity over the coming years.

I'd even go as far as saying that this structural advantage is the primary reason the $NVDA partnership came to be.

While $NVDA undoubtedly remains king of the hill, even they face a real dilemma that could cause cracks in their growth trajectory.

On the supply side, they have to come to terms with the fact that the gap between planned and realized data center capacity is widening, while the trend of new capacity coming online is actually decelerating.

This is the issue I just flagged, and it could act as a potential growth bottleneck for $NVDA, since fewer builds means fewer GPU sales.

Layered on top of this is the demand side. It's perfectly clear that demand for $NVDA's AI hardware remains insatiable. However, when looking closer, it's also apparent that competition is increasing.

Pretty much every hyperscaler is working on their custom chips (TPU, Trainium, Maia, MTIA), and not exclusively for internal use cases anymore, but increasingly to service the compute needs of large AI labs. Anthropic alone has signed deals worth billions for Google TPU and AWS Trainium capacity.

Then you obviously have the likes of AMD and Cerebras directly competing against the AI giant, trying to claim market share.

Taken in aggregate, these two issues could gradually lead to a growth problem for $NVDA if not addressed.

This is exactly where $IREN comes in.

They've got the largest secured power portfolio of any neo-cloud at 5.8 GW and growing fast, they develop 100% of their data centers themselves, and they're not building competing silicon.

That makes them the most reliable demand outlet $NVDA can partner with at scale.

The Sweetwater partnership, positioning the 2 GW campus as a "flagship DSX deployment," isn't $NVDA doing $IREN a favor. It's $NVDA solving its two biggest problems at once.

I'm sure you know the popular saying that "history never repeats, but often rhymes." I think today's neo-cloud market is somewhat similar to the dot com era search engine war.

Back then, the front-runners leading the race were AltaVista, Excite, and Yahoo, while Google was a latecomer that ultimately came out on top.

Today, the vast majority of investors in this space are declaring either $CRWV or $NBIS the obvious winners in the race to become the next hyperscaler.

However, I believe the real dark horse that the mainstream doesn't give much credit to is $IREN.

I believe they have all the ingredients to leapfrog every competitor in a short amount of time, in large part due to their structural advantages and pursuing the right long-term strategy from the get go.

The asset-light model, which both $CRWV and $NBIS have been leaning into, doesn't work well in capital-intensive industries, at least not over the long run.

It's somewhat of an oxymoron, since it seems intuitive that one way to circumvent some of the CapEx burden is to outsource from colocation providers.

Yet that approach leaves you with less control, less flexibility, and ultimately higher costs in aggregate in the form of operating expenses (the landlord also has to earn $).

I studied the Bitcoin mining industry for years, and the asset-light model was once a popular strategy around the 2021 bull market. While it proved to be a strong growth lever, it ultimately ended up being a disaster for anyone who adopted it.

Companies like $MARA are the perfect example.

$MARA heavily adopted the asset-light model and grew to become the largest $BTC miner, yet ended up as one of the most unprofitable public miners of all, leading to significant value destruction for shareholders over time.

Once it became obvious that asset-light wasn't a sustainable strategy, $MARA tried to pivot away from it by increasing self-deployments. But developing infrastructure in-house is a much harder discipline to master, and you don't simply switch into it overnight.

$IREN ultimately won the mining race last cycle by doing the exact opposite of $MARA from the start.

They developed all of their data center infrastructure in-house, backed by a seemingly unlimited pipeline of secured power, which ended up making them the fastest growing and most profitable miner of all time.

While the cloud sector has significant differences from the mining industry, the primary drawbacks of the asset-light model carry over.

Over time, it will become obvious to Wall Street and the broader market that this strategy sounds great in theory, but in practice leads to a stack of operational issues and severe margin compression.

Out of the two current front-runners, $CRWV and $NBIS, I think Nebius will do better. They've at least started moving toward a more diversified mix of self-owned capacity rather than purely relying on hosted colocation, which is the right direction even if they're still early in that pivot.

That said, as the $MARA example showed, developing in-house gigawatt projects at scale is not something you learn overnight.

It's clear to me that a player like $IREN, which has been building this discipline from day one, has the most realistic pathway toward sustained, profitable growth in this space.

In my view, $IREN is the dark horse that will end up winning the race. Thus overthinking today’s price action wouldn't do me any favors.

Cheers guys, have a great weekend! ✌️

92

124

1,102

151,211

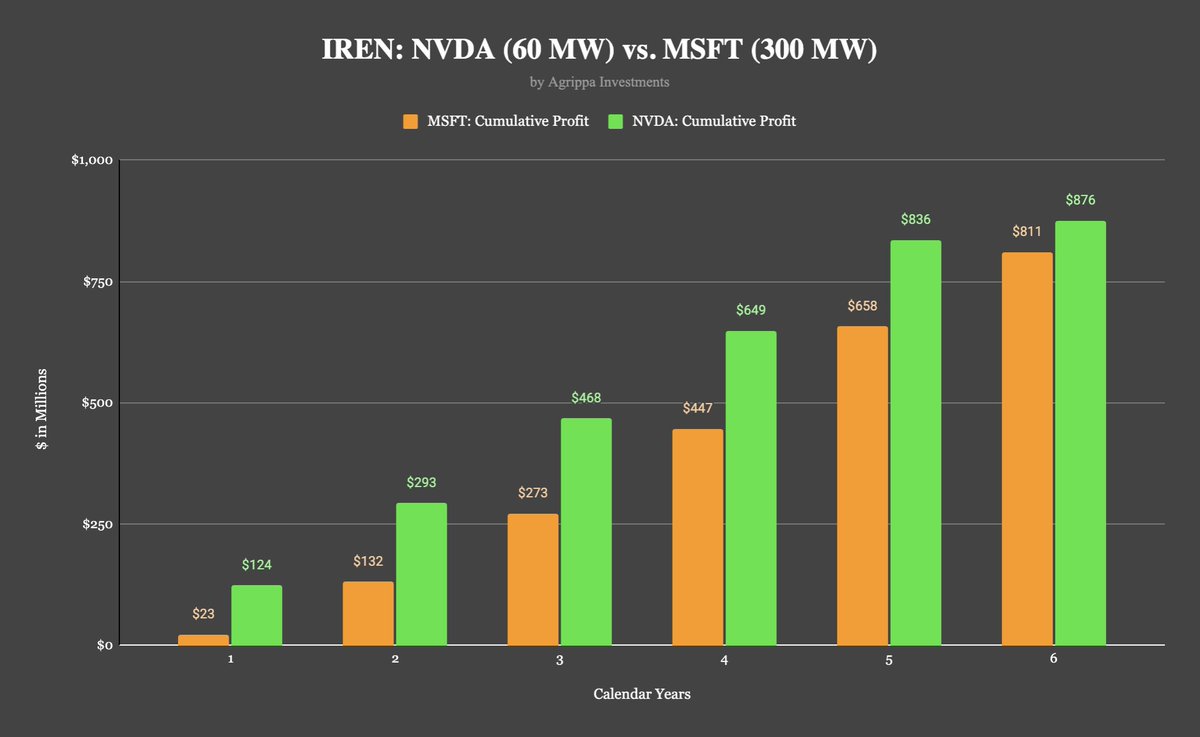

Most $IREN investors don't yet grasp how profitable the 60 MW $NVDA deal actually is.

Despite being just 20% of the MW capacity, it yields more cumulative net income than the 300 MW $MSFT agreement.

This is a direct result of $IREN locking in stronger terms.

Now that $IREN is quickly establishing itself as one of the premier cloud providers with the deepest pipeline in the industry, I expect future deals to land at similar profit margins.

Considering the price action since last earnings, the market clearly hasn't priced that in yet.

38

83

798

103,787

May 30

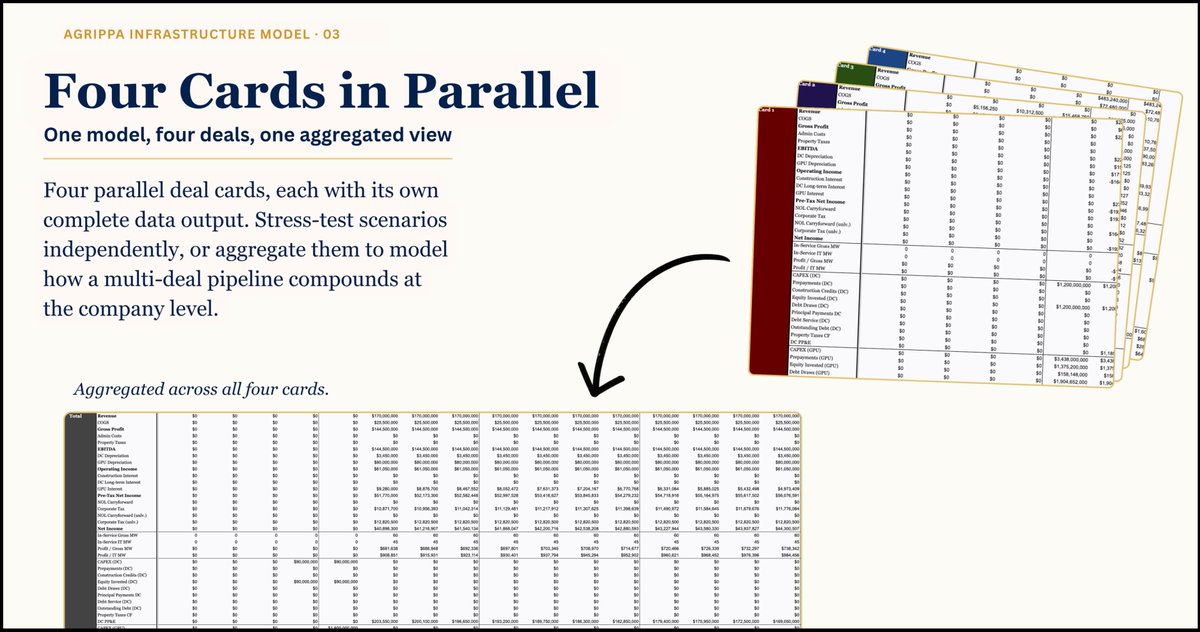

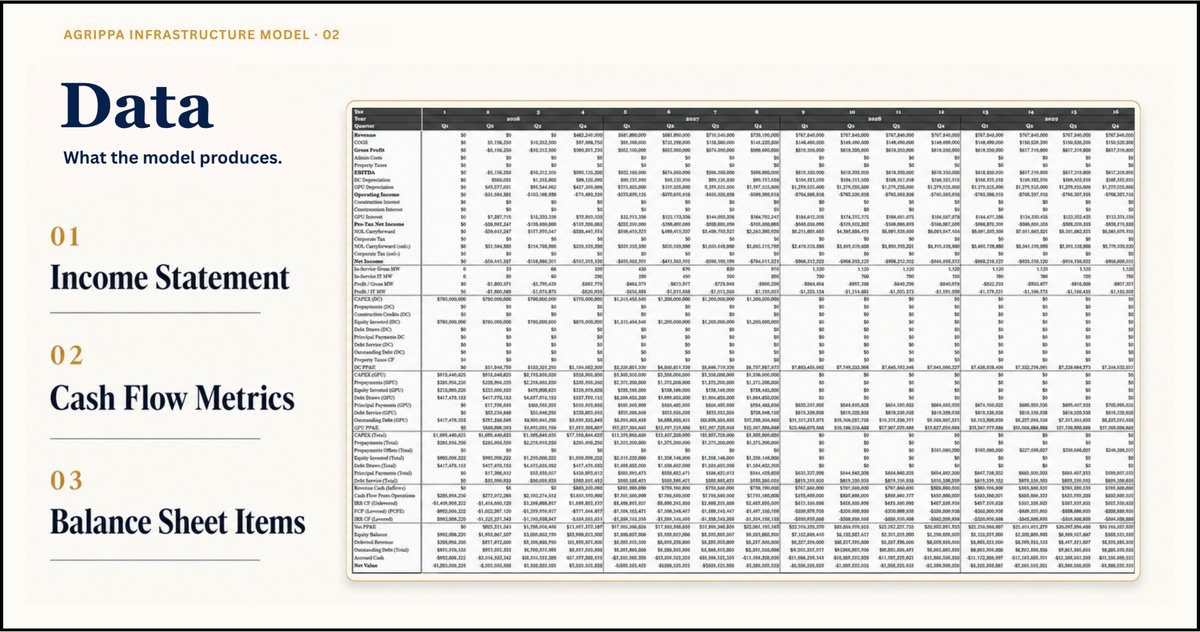

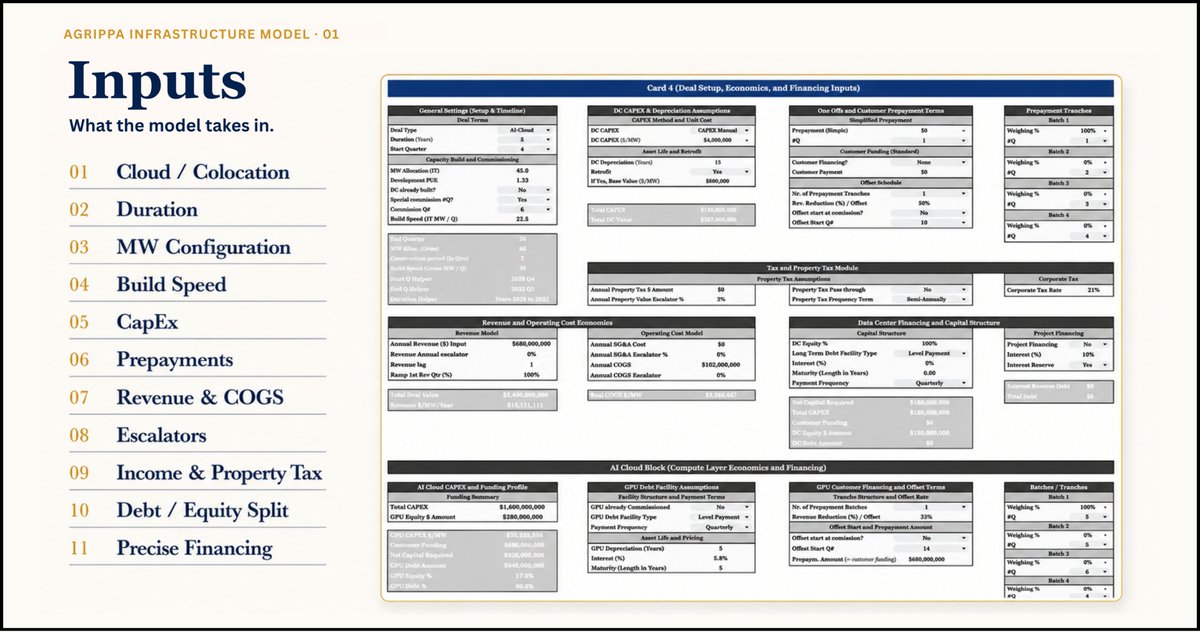

Model Release: AI Cloud & Colocation

We just released the in-house developed infrastructure model behind our $IREN work.

It lets you replicate any AI cloud or colocation lease and gives you exceptional insights into the economics of your favorite AI/HPC stock.

We have been developing and refining this model for well over 6 months, and we genuinely believe it is one of the most powerful tools out there for breaking down the economics of any AI cloud or colocation deal.

In this thread I'll walk you through everything there is to know. 🧵

13

24

252

27,819

May 30

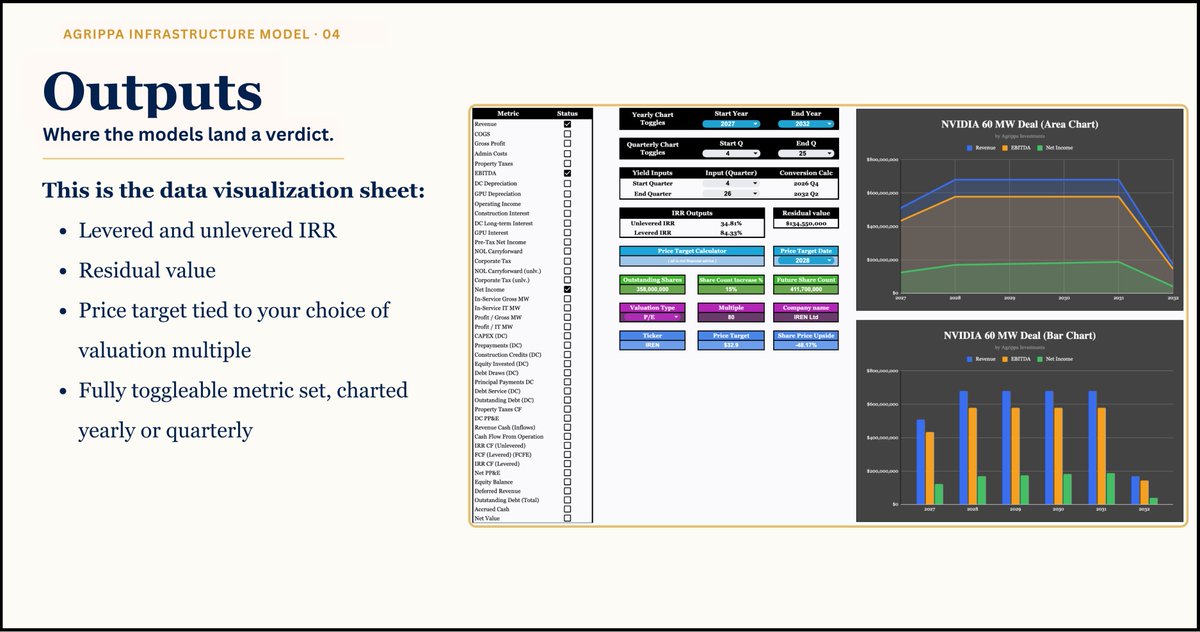

4) Outputs: Visualization

The most powerful element of the tool, and the section I personally use the most, is the data visualization sheet.

From here you can toggle every individual metric from the Data section, and the model automatically projects them onto both bar and area charts for whatever time horizon you select.

This sheet also neatly displays both the levered and unlevered IRR, alongside the final residual value of the infrastructure at the end of the deal or period selected.

And finally, it makes price target forecasting straightforward.

Pick your preferred valuation multiple (Revenue, Earnings, EBITDA, FCF, and so on), estimate dilution out to your target year, and the model returns a specific price target built directly off the underlying contract economics.

1

1

25

5,006

May 30

5) Exclusively available to Advanced ( ) Subscribers

The model is now available exclusively to Advanced ( ) subscribers of our Agrippa Investments Substack.

It also comes with a full explanation sheet built in.

Additionally, over the coming days we will be releasing a deep dive style tutorial on how to use the tool to perfection, so you can pick it up and put it to work straight away.

Advanced ( ) members get the full library of deep dives and Radar Reports, plus exclusive reports reserved only for them, while the annual price actually comes in below twelve months of the standard monthly plan.

We are planning to build additional models like this one for our Advanced ( ) members over time, covering other names outside AI infrastructure that we will be adding to our investment universe in the future.

If you are currently on the standard monthly or annual plan and want to upgrade, Substack makes it easy.

Any existing payments on your annual plan get credited in full against the new Advanced ( ) price, so you only pay the difference.

Click the link below to sign up as an Advanced ( ) member, or upgrade your existing subscription, and get access to one of the best AI/HPC infrastructure deal models on the market. 👇

agrippa.investments/subscrib…

1

1

36

4,593

May 29

$IREN’s new Innovation Officer

A few months ago, $IREN appointed John Gross as their new Chief Innovation Officer, a role in which he'll be pivotal to the development of the company's AI data centers.

The Wall Street Journal recently ran a piece on him that I think is worth commenting on.

Gross specializes in high-density & liquid cooling infrastructure, with over 20 years of experience in the space. That makes him a critical hire for $IREN, given their emphasis on designing & developing all data center infrastructure in-house.

What I particularly found interesting about the WSJ article is that it goes into Gross's approach and philosophy.

He comes across as a very hands-on guy and not some office dweller. He likes being on the ground where the actual liquid cooling tech is being installed and tested, working together with construction crews to fix problems that can't always be foreseen months in advance.

Great to see $IREN's CIO with this kind of attitude. Getting his hands dirty when he needs to and leaving his ego at the door. He's clearly all about pushing $IREN forward and getting things done.

He also pushes back pretty directly against the industry default, which has historically been very risk-averse.

He says the industry “loves innovation as long as it’s 10 years old”, which is pretty funny.

That risk-averse, slow mindset clearly doesn’t work in AI, where chip generations turn over every 12-18 months and thermal envelopes keep climbing.

This kind of attitude combined with $IREN's broader culture is what makes them a disruptive force in the industry that can really challenge the status quo.

Gross also called AI data center tech a bit of a poker game. You can't sit on the sideline waiting for the chip roadmap to be 100% clear, you have to read what's coming and place your bets early.

$IREN has clearly been great at this. Horizon was designed early last year to be future-proof for next-gen chips, more than a year before the official Rubin specs came out. Back then estimates were that Rubin would require densities of ~300 kW per rack, so $IREN's 200 kW design may have looked inadequate initially.

They were obviously proven right...

I know $IREN execs had a very tight relationship with $NVDA well before the official partnership was made public.

That kind of access gives you early visibility into where the industry is heading years in advance, and that's exactly where close ties to $NVDA pays dividends as it relates to developing next-gen infrastructure.

Gross also commented on $IREN's iterative improvement loop, where lessons from each build feed back into the next design cycle.

This reminds me very much of what David Shaw, $IREN's Chief Operating Officer, told me about a year ago when I visited the Childress site with @FransBakker9812 and a few other friends.

Shaw and the other ops execs really emphasized the same design and development philosophy of replication and continuous improvement.

Every individual new build is slightly different from the last as the team implements lessons learned from the previous one. That will mean Horizon 2 will have improvements over Horizon 1, Horizon 3 over Horizon 2, and so on.

The advantage of that approach is that it directly leads to faster, cheaper, and more robust builds, which is a critical trait when you're developing a gigawatt-scale data center portfolio.

This isn't something they started doing recently either. It has been part of the company's DNA since day one.

It only works because of $IREN's very flat hierarchy and very healthy work culture, which encourages every construction crew member to spot flaws or find better ways of doing things.

This is also how they managed to bring the development cost per MW of their air-cooled data center shells down from $750k/MW to $600k/MW.

Going forward this is going to be one of the key competitive differentiators.

While other neo-clouds heavily rely on a patchwork of developers across their data center pipeline, $IREN is the head contractor on 100% of their projects.

The amount of operational experience they'll accumulate as they rapidly scale will become unmatched and very difficult to catch up to.

I also must say, this WSJ article is a real win for $IREN on the IR and marketing front, and they deserve credit for setting it up.

The company's comms had undoubtedly been pretty weak leading up to the recent earnings call, but over the past 3 weeks they've gotten noticeably better imo.

From the CEO’s mega thread here on X that cleared up a lot of confusion to now this WSJ collab… these are real positive moves from the team and they're worth praising.

Overall the WSJ piece does a great job giving us good visibility into Gross himself and his role at $IREN, as well as the company's broader strategic positioning.

I really enjoyed going through it. Definitely worth a read.

partners.wsj.com/iren/buildi…

30

56

526

53,774

May 27

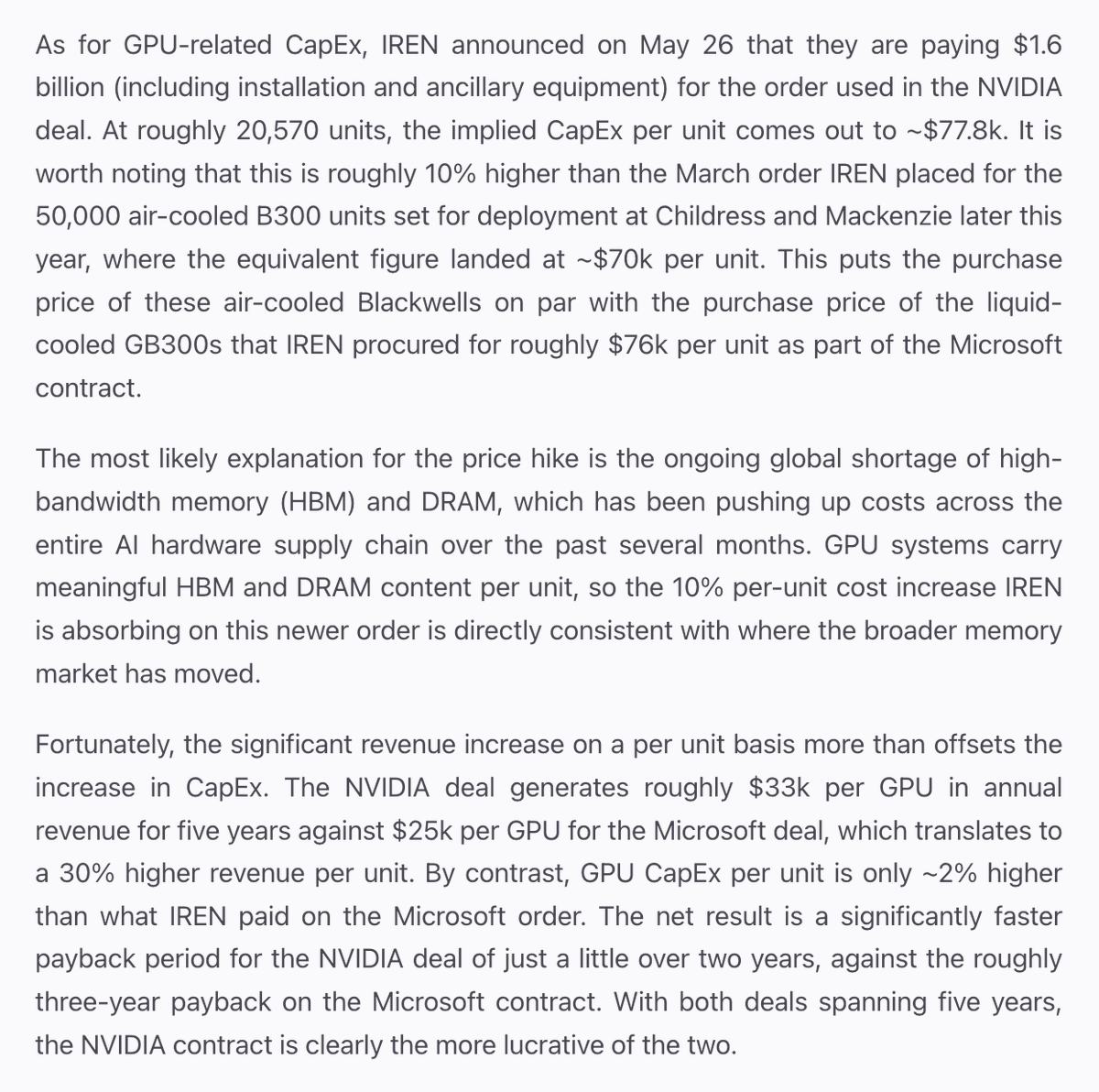

For anyone wondering if the new $IREN deep dive takes into account yesterday's Dell announcement: YES, it does.

I fully updated the section covering the 60 MW $NVDA deal, including the graphs used to visualize certain data (net income, cash flow, etc.).

I've included a small snippet below to give you a glimpse of the updated section.

Luckily, not much actually changed, since my original assumptions used $1.5b in GPU-related CapEx, which has now been confirmed at $1.6b.

As for the ARR "upgrade" from $3.7b to $4.4b, anyone who has been paying attention knows this is NOT anything new 😂

Don't let me be the party pooper, but the $NVDA top-line figure was already known: $3.4b. This is simply the annualized $NVDA run rate added on top of the year-end ARR guidance.

Nothing new here, so there was no need to change anything on that front in the deep dive. That said, I'm happy about how the market and FinX reacted to these "news".

May 26

New $IREN Deep Dive

Our new $IREN deep dive is finally live!

It's honestly the most comprehensive report we have ever released and something I'm firmly convinced will age like fine wine.

Even though it goes into great depth, it's written in a way that virtually every investor can understand. I purposefully went light on industry and finance jargon, and whenever I did use technical terms I made sure to explain them properly.

This time around I've also unlocked the entire first chapter for free Substack subscribers to read.

So if you're on the fence, I encourage you to read the first pages to get a sense of the depth and analytical quality you can expect from the rest of the deep dive.

I'm sure every $IREN shareholder, analyst, or investor curious about the company will derive great value from this deep dive.

I very much appreciate everyone's patience. This one took a while.

Enjoy! ✌️

agrippa.investments/p/irens-…

25

26

416

49,329

May 26

New $IREN Deep Dive

Our new $IREN deep dive is finally live!

It's honestly the most comprehensive report we have ever released and something I'm firmly convinced will age like fine wine.

Even though it goes into great depth, it's written in a way that virtually every investor can understand. I purposefully went light on industry and finance jargon, and whenever I did use technical terms I made sure to explain them properly.

This time around I've also unlocked the entire first chapter for free Substack subscribers to read.

So if you're on the fence, I encourage you to read the first pages to get a sense of the depth and analytical quality you can expect from the rest of the deep dive.

I'm sure every $IREN shareholder, analyst, or investor curious about the company will derive great value from this deep dive.

I very much appreciate everyone's patience. This one took a while.

Enjoy! ✌️

agrippa.investments/p/irens-…

75

141

1,094

357,568

May 25

New $IREN Deep Dive dropping tomorrow (on Substack).

Over two weeks of work, 50 pages, and honestly the most comprehensive report I've ever released.

I'm constantly on X reading everything there is on $IREN. I'm also routinely checking sell-side and institutional coverage of the ticker.

Trust me when I tell you that there is nothing in the public sphere that comes close to the depth this deep dive delivers.

Very excited for the release!

67

53

1,031

67,247

May 22

My take on @danroberts0101 new post

$IREN Co-CEO just dropped a beautifully written thread on the company's compounding competitive advantages.

Seriously, a must read for every $IREN investor or folks who are on the fence.

My highlights:

- Dan confirmed that the 60 MW cloud contract with $NVDA is in fact measured in 'gross' MW, not IT. That was already obvious to me based on the earnings call material, however, it's great to get definitive confirmation.

The implications of this is ENORMOUS. The $NVDA contract has incredible economics, something I've analyzed extensively in my upcoming $IREN deep dive (released in a couple of days on Substack).

- Dan firing shots at the likes of $NBIS & $CRWV:

"And the asset-light neocloud trying to compete by renting capacity is discovering that sites were locked up years ago, and the operators utilizing them aren’t subletting. By the time new entrants solve for land, power and permitting, IREN will have gigawatts online, execution track record, and customer relationships that took years to build. That gap doesn’t close. It compounds."

This is by far my favorite quote coming out of Dan. Eventually, everyone will realize that the real advantage $IREN has over the rest of the neo-cloud sector, is the fact that they are the only provider that's 100% vertically integrated.

They don't have to deal with any land-lords. They don't have to pay billions to $BE to secure fuel cells in a desperate attempt to salvage a project that is tied to a large customer contract. $IREN is in control of its own destiny, and eventually that will show up in the bottom line (profits).

The “asset-light” model never works in an infrastructure-heavy industry. It works for hardware, when you are the high-margin designer and outsource the manufacturing process to a specialized entity. But it doesn’t work when the infrastructure itself is the product.

In cloud, the value is not just in having access to GPUs. The value is in controlling the full stack, which mostly consists of physical infrastructure.

If you outsource all of that to colocation partners, you are not building an AI factory. You are renting someone else’s factory, layering a spread on top, and hoping the economics still work after the landlord, the power provider, the OEM, and the lender have all taken their share.

That model can look attractive in the early innings because it allows rapid capacity announcements without heavy upfront CapEx. But structurally, it leaves the operator with the worst part of the value chain.

I'm really looking forward to comparing the net income lines between $IREN, $CRWV, and $NBIS a few years from now. I wouldn't be surprised if two out of the three remain unprofitable by then.

- I really enjoyed Dan's section about becoming a global cloud provider.

He did a great job in explaining the importance of being locally present in the markets you want to source customers from. Not just due to local proximity for inference, but also due to compliance & sovereignty.

These were my highlights, I'll let you discover the other gems yourself. This is easily Dan's best post and I think it does a lot in terms of IR, especially as it's coming from him; the co-founder and co-CEO of $IREN.

As mentioned earlier, very soon I'll be releasing a new deep dive on $IREN. It goes deep into the implications of the $NVDA partnership and Mirantis acquisition, including a bunch of different topics worth exploring. So far, the report is 30 pages long (including graphs / images) and I'm in the process of finalizing it.

Honestly, one of my best deep dives to date. I know I'm saying that for each release, but the depth and quality of our work is undoubtedly increasing. Can't wait to publish it.

Cheers guys! ✌️

May 22

𝐓𝐡𝐫𝐞𝐞 𝐋𝐚𝐲𝐞𝐫𝐬. 𝐎𝐧𝐞 𝐂𝐨𝐦𝐩𝐨𝐮𝐧𝐝𝐢𝐧𝐠 𝐀𝐝𝐯𝐚𝐧𝐭𝐚𝐠𝐞. 𝐓𝐡𝐞 𝐈𝐑𝐄𝐍 𝐓𝐡𝐞𝐬𝐢𝐬.

There's been a lot happening at IREN recently.

Expansion across North America, Europe and Asia-Pacific.

The NVIDIA partnership.

The Mirantis acquisition.

New GPU deployments.

New customer discussions.

A growing global footprint.

Underneath all of it is a fairly simple view of where the world is heading, and a deliberate strategy for how we position IREN within it.

That strategy is built on three layers. Together, they compound into a structural advantage that gets harder to replicate every quarter we execute.

Layer 1: Physical infrastructure. Power, land, substations, data centers, cooling. The foundation that everything else sits on.

Layer 2: Compute infrastructure. The GPUs, servers and networking that go inside those buildings. Deployed at scale. Generating revenue. Building execution track record.

Layer 3: Software and operational capability. The orchestration, deployment tooling and enterprise expertise that makes the first two layers work harder for customers, and opens the door to a broader, higher-value market over time.

Layers 1 and 2 are where the overwhelming majority of IREN's value is being created today. Layer 3 is where that advantage compounds further over time, but only because Layers 1 and 2 are built, owned and controlled at scale by IREN, not subscale nor contracted from a third party.

Think of Amazon. They didn't win e-commerce by building a great website. They won it by controlling the fulfilment infrastructure at a scale nobody else could replicate. The foundation you don't control becomes the ceiling on your business.

That is exactly how we think about IREN. The physical infrastructure - the land, the power, the substations, the data centers - is owned and controlled by us. The compute deployed into it generates the revenue and execution track record. And the software, orchestration and enterprise capability we are more methodically building on top is what turns the total product into a vertically integrated AI Cloud platform that compounds over time and deepens into a competitive moat.

AI is still early. The bottleneck is increasingly physical. And we have spent eight years building the foundations.

73

107

1,093

181,497

May 12

$IREN's new convertible offering is arguably the strongest one to date.

- Size: $2.6b, up to $3b if extension option is exercised

- Conversion Premium: 32.5%

- Annual Coupon: 1%

- Maturity Date: December, 2033

These are incredible terms!

The only prior note offering that comes close to this is 'Convert 3', which on paper may look stronger (0% Coupon /42.5% Conversion).

But keep in mind, that convert's size is ~1/3 of today's and expires 2 years prior. Generally speaking, the more capital you raise & the further out the maturity date, the worse terms you get.

I'm a very happy shareholder today. This offering proves once again that $IREN's finance team is amongst the best in the industry.

May 12

$IREN Prices Upsized $2.6 Billion 1% Convertible Senior Notes Due 2033

@IREN_Ltd announced the pricing of its upsized private offering of $2.6 billion in 1.00% convertible senior notes due 2033 (increased from the previously announced $2 billion).

Key Terms:

- Coupon: 1.00% (paid semi-annually)

- Maturity: December 1, 2033

- Initial Conversion Price: ~$73.07 per share (32.5% premium to the $55.15 closing price on May 11, 2026)

- Conversion Rate: 13.6848 ordinary shares per $1,000 principal

- Capped Calls: Entered with a cap price of $110.30 (100% premium) to reduce dilution upon conversion

Proceeds & Use:

- Expected net proceeds: $2.57 billion ($2.96 billion if the $400 million option is fully exercised)

- ~$174.5 million to fund capped call transactions

- Remainder for general corporate purposes and working capital

The notes settle on May 14, 2026. This move provides IREN with significant low-cost capital to support its AI cloud and data center growth.

43

87

760

89,046

$IREN just entered the European market with the acquisition of Nostrum, a data center developer based in Spain.

This acquisition adds 490 MW of grid-connected power (in Spain), with the total *secured* power portfolio now consisting of 5 GW!

Wow! $IREN is really on a massive roll right now. Nothing is stopping this train...

27

79

742

49,241

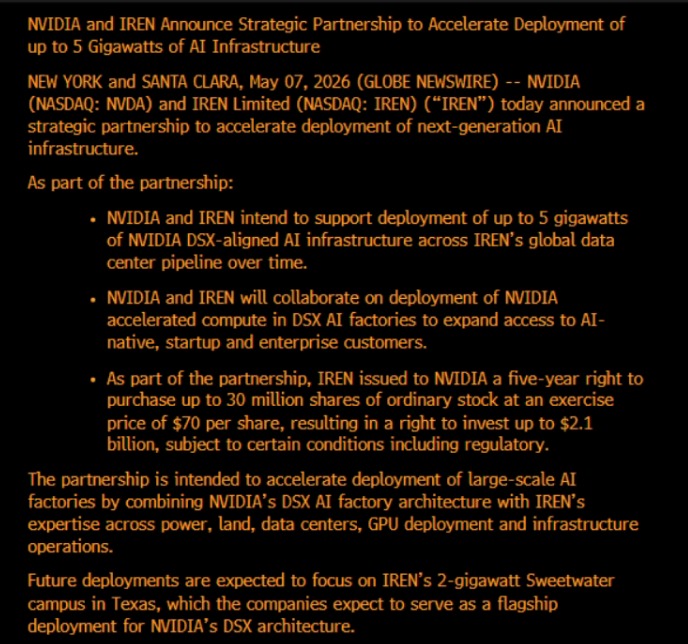

The crazy thing about this announcement is that $NVDA has to PAY $IREN $70 per share for exposure in the company.

Keep in mind, $IREN was just trading at ~$56 before this news dropped... No free lunch.

As I have said for a while, $IREN's management is playing hardball with EVERYONE in the industry, including titans like $NVDA.

This leadership knows what kind of leverage they have and they are not afraid to exercise it....

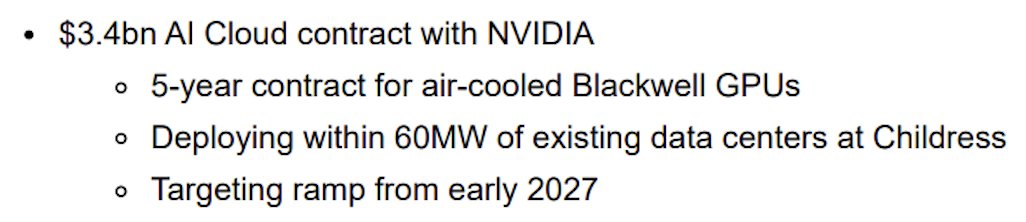

$IREN just announced a massive 5 GW partnership with none other than $NVDA....

I love how it references $IREN's "global" pipeline.

$IREN is fast fast-tracking its path to becoming the next hyperscaler.

It turns out that having gigawatts of grid-connected energy, while everybody else is severely power-constrained, is a real MOAT.

$IREN shareholders have just been validated BIG TIME.

We are just getting started! 📈

70

74

843

202,115