Value investor. Istanbul. Nothing I post is investment advice. All my writeups are free. No paywalls. altaycap.substack.com/

Joined March 2022

- Tweets 7,854

- Following 988

- Followers 14,740

- Likes 33,557

730 Photos and videos

$4628 Sk Kaken thesis:

1. The stock is currently a modest value trap. 10x earnigns with a 2% dividend that has been going up with Japan's shareholder pressure campaign. I'll arbitrarily assume that'll normalize to a 3% dividend on average - sometimes it'll be a bit worse, sometimes a bit better, but that's a fine guess. On top of that, the cash pile will grow with earings which you can discount say 70%, so another 3%. Total is a low downside risk 6%/year expected return. Not great, but honestly not that bad.

2. Founder/family control is the blocker. Shikoku Kousan owns 31.88%, and Fujii Minoru, Fujii Kunihiro, and Fujii Mitsuhiro own another roughly 9.3%, so the Fujii-side block is about 41% excluding treasury shares. The company also has 2.18m treasury shares, about 13.9% of issued shares, with no votes.

3. The relevant entity is 四国興産有限会社 / Shikoku Kousan, located in Takarazuka, Hyogo. It is listed as established on September 1, 1998, so as of June 16, 2026, it is 27 years and about 9.5 months old.

That is much younger than SK Kaken itself, which was founded in 1955 and incorporated in 1958.

4. The patriarch is almost certainly Fujii Minoru, the SK Kaken founder. He is 93, turning 94 on September 1, 2026.

-

Heads you get a safe 6%/year turn.

Tails, the patriarch passes away and you get a 15% /year expected return. If you assign even 30% odds to tails, this is a fantastic risk adjusted bet.

If the patriarch was even 10 years younger, that looks far more questionable.

If anyone else has these age-as-a-catalyst plays, please comment or DM me.

5

2

39

7,747

Jun 15

I am bearish Kadokawa here. This is a tough biz and they need a turnaround to improve their awful margins/bloated business. Anyone who wants alternative exposure to manga/anime can consider:

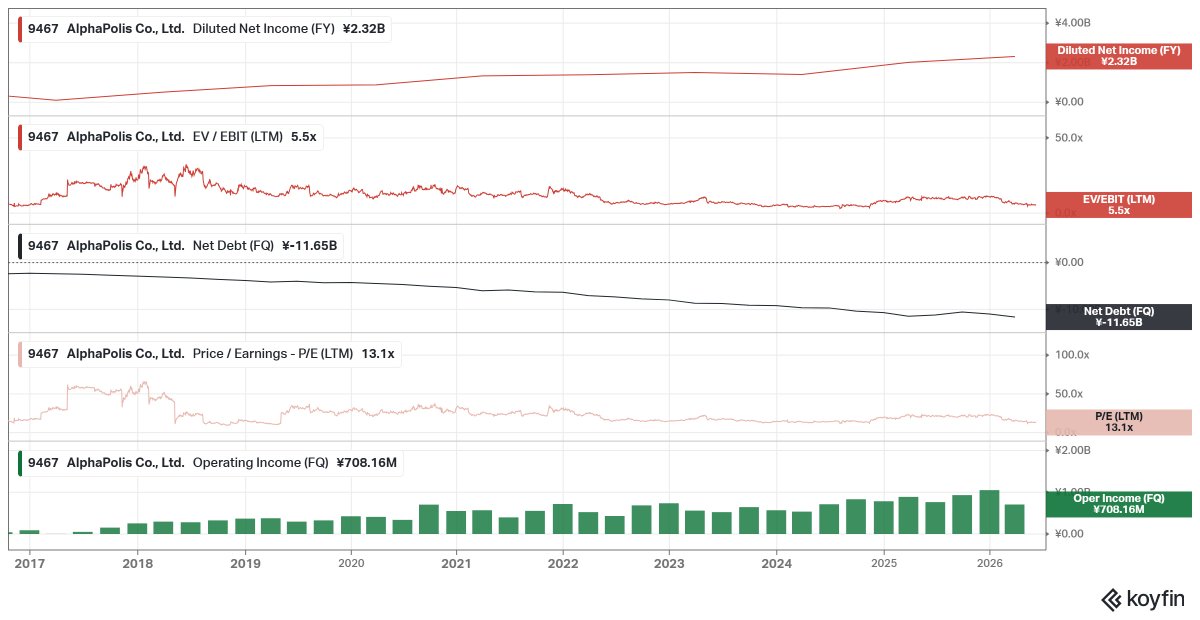

AlphaPolis (9467): 5.5 ev/ebit

With exposure to anime/manga/light novels

May 27

The folks at Oasis are sharp, but not sure how well Kadokawa (TYO 9468) will work. I lost patience on the co. Large trove of IPs but awful execution. Oasis is spot on in their activist pitch to replace the CEO.

Even at peak ebit (fy23) though of ¥26bn it would trade at a bit over 15x ev/ebit. Not cheap. Anime manga is growing worldwide, but they can't seem to capture much of the economics.

I've also grown much more bearish on gaming. They also have an education / web services biz hodgepodge of random 'other' businesses unrelated to core.

Bandai namco isn't a pure play, but much cheaper. Toei animation is pure play, but basically a bet on 2 IPs. Other names are too small for institutional / bigger investors. I'd rather own either Toei animation or Bandai namco today. I don't own any of these though. Still wishing Oasis luck. Their deck on Kadokawa is spot on. If oasis can really replace the ceo and change management mentality fully, this bet could work. The peak ebit figure would have been a lot higher if the co was leaner and didn't give up Elden Ring economics to BandaiNamco. Trying to make a big Japanese co leaner seems very hard though.

2

18

5,782

Jun 15

AlphaPolis publishes a lot artistically slop Isekai content, but so does Kadokawa. Kadokawa's poor performance is AlphaPolis and other small cos opportunity (TO Books, Overlap, etc). Kadokawa is asleep at the wheel, which gives competition room to eat their lunch.

1

4

1,515

Jun 15

AlphaPolis is increasingly looking to expand into anime and own more of the economics surrounding their anime. They bought 2 anime studios (which are historically awful businesses) with an aim to vertically integrate to retain more upside.

These stocks aren't stupid cheap, but are much cheaper than Kadokawa.

1

4

1,429

Jun 12

If you aren't on one of the $100 or $200/mo plans on Claude or ChatGPT (or both), why not? Revolutionary tech that's massively subsidized in pricing. GPT Pro Fable are worth it

I'm building tools / automation for several side projects, equity research, and just messing around

10

1

63

10,841

Jun 13

I'd like to add, Claude fable and 4.8 are awful for equity analysis. Really bad from my experience. I always try and always disappointed. ChatGPT is much better for investment research.

4

12

2,561

Been reviewing Japanese longs all morning.

Look at this example Tanabe Engineering $1828. It now trades for 7x earnings with 16% return on capital. It has a 4.5% dividend yield. They tripled operating income in a decade.

There are so many companies like this, from unrelated industries, that peaked exactly at the end of February.

This type of small cap Japanese value / GARP stock is in a bear market. This one had a 25% drawdown.

18

18

244

36,127

Jun 2

Japan deep value getting clobbered last few days. Rough out there!

9

52

17,210

May 30

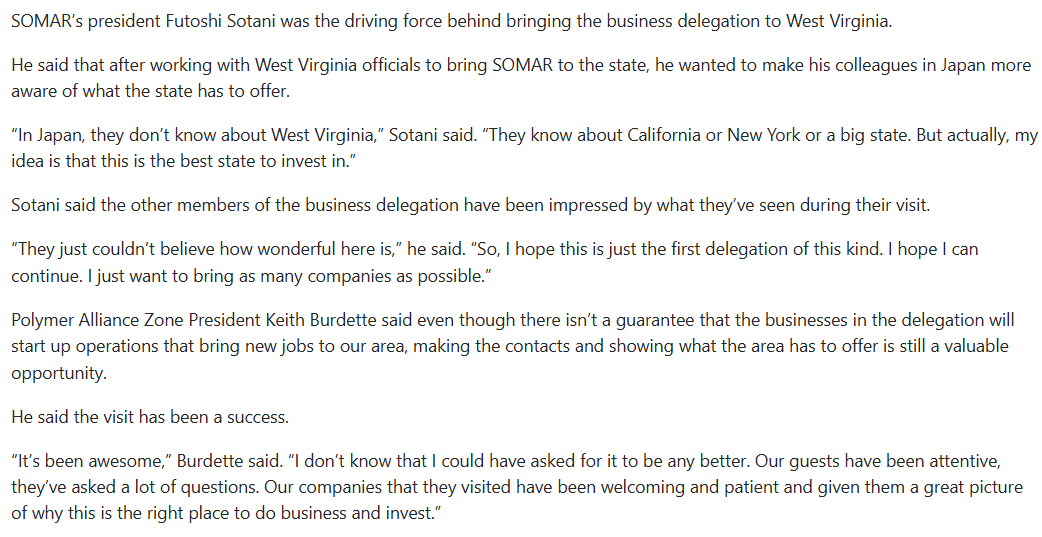

New reporting from local news 2 days ago. One reason I added to Somar last year was the quote post about Somar being thrilled with West Virginia. That plant isn't even fully online yet and talk of an expansion? This was not disclosed in full year financial report on 5/15.

15 May 2025

One of my basket names SOMAR (8152) announced a new facility in West Virginia (USA) last year. Somar president was so impressed/happy with West Virginia he brought 18 other JP businessmen to tour the area and consider investing. Local news covered the story.

1

1

14

5,067

May 30

There's sometimes alpha in tiny companies and looking at local reporting. For conservative Japanese company to talk of expansion with local officials suggests demand from customers is there (my speculation)

1

9

2,343

May 29

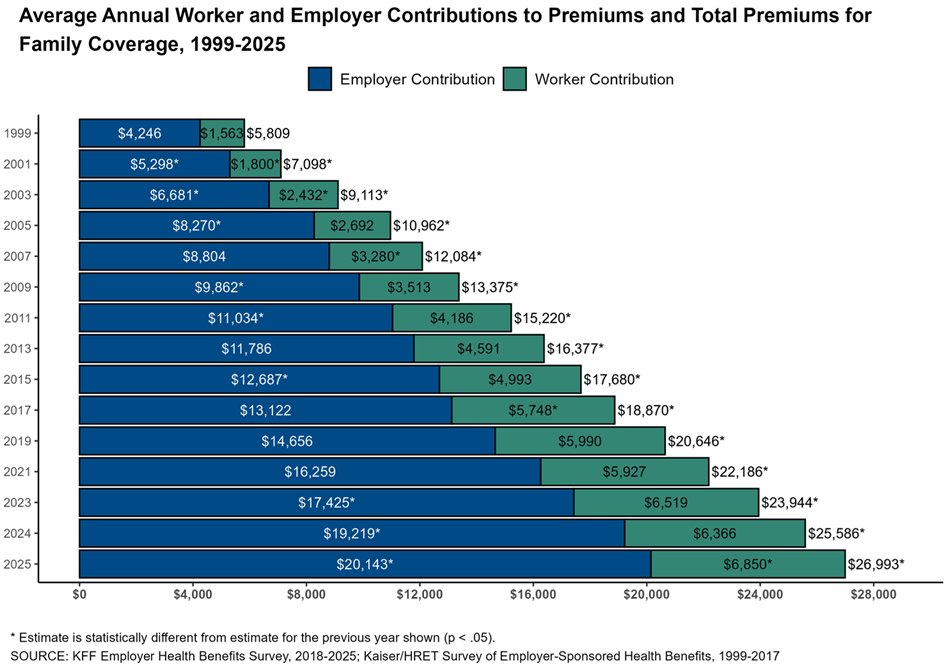

The single biggest issue in American society by a wide margin.

May 28

Nearly $27,000 a year for family health insurance premiums, up from $6,000 in 1999.

And that’s before deductibles, copays, and surprise bills.

The system is fundamentally broken.

5

1

44

7,503

May 27

The folks at Oasis are sharp, but not sure how well Kadokawa (TYO 9468) will work. I lost patience on the co. Large trove of IPs but awful execution. Oasis is spot on in their activist pitch to replace the CEO.

Even at peak ebit (fy23) though of ¥26bn it would trade at a bit over 15x ev/ebit. Not cheap. Anime manga is growing worldwide, but they can't seem to capture much of the economics.

I've also grown much more bearish on gaming. They also have an education / web services biz hodgepodge of random 'other' businesses unrelated to core.

Bandai namco isn't a pure play, but much cheaper. Toei animation is pure play, but basically a bet on 2 IPs. Other names are too small for institutional / bigger investors. I'd rather own either Toei animation or Bandai namco today. I don't own any of these though. Still wishing Oasis luck. Their deck on Kadokawa is spot on. If oasis can really replace the ceo and change management mentality fully, this bet could work. The peak ebit figure would have been a lot higher if the co was leaner and didn't give up Elden Ring economics to BandaiNamco. Trying to make a big Japanese co leaner seems very hard though.

3

22

16,463

AltayCap retweeted

I sat down with Taiwanese investor @DaBao_ in his first-ever recorded video interview

Key takeaways:

- The Taiwanese stock market is becoming overheated

- He likes companies that offer mission-critical services

- TSMC's story is intact

- The Taiwan invasion threat is overblown

22

34

291

44,384

May 26

Great writeup by @travislundyasia on @smartkarma on Mitsui Matsushima (TYO 1518). I bought some at open. Stokc has run up, but remains very cheap.

Murakami group has a large stake. Company buying back shares and paying out big dividend (5%). Not net-net cheap, but cheap!

4

2

37

6,951

May 26

I am not paid to promote this. I paid for a smartkarma sub a while ago (via bundle with Caixin). When renewal came around they gave me a free sub since they syndicate some of my writeups.

2

7

1,781

AltayCap retweeted

May 21

One of my favourite Japanese ideas is Kitazato corp $368A. Founder led, Japanese company with a large (30% ex US) market share in IVF fertility treatment. Large tailwinds as popularity of IVF continues to grow. The co has been smashed down 25% from IPO last year. This isn't an

7

10

108

17,372

May 20

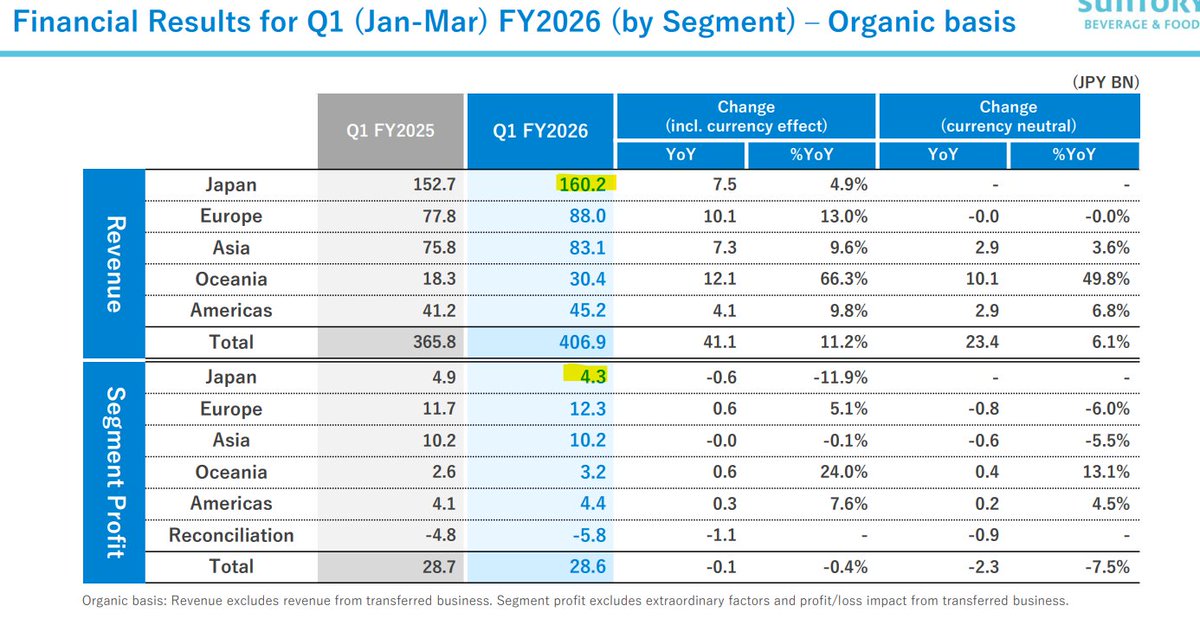

Bought some Suntory Beverage (2587) today. This is a cheap large cap JP consumer staple (most profits ex Japan from Europe/Asia).

EV/EBIT of 8.6 (vs 24.6x for $KO). Yeah, KO is the better 'asset light' biz, but this is so much cheaper (and bit better yield too).

4

2

52

6,739

May 20

The margin in the JP biz is crazy low, which is why most profits are ex Japan. If they ever improve margins there, there's big upside.

yeah yeah, not a nanocap or net net, or even the cheapest staple, but it'll offset some of my staple etf short XLP.

3

12

1,827

May 19

Neowiz Holdings is up 30% today. It's a discounted way to own Neowiz. Neowiz Holdings announced ~8% share buyback cancellation plan.

Prior to today's move Neowiz holdings gave you Neowiz at a discount a ton of other goodies in the hold co. Discount narrowed A LOT. I sold.

1

11

3,130

May 19

The discount still exists since you get the other random goodies in the holdco, but not as obviously cheap anymore. Would love to see other KR companies narrow the discounts to NAV.

Got lucky with this one. It was a small position that i sold out of today at 26%.

1

1,496