Joined October 2020

- Tweets 873

- Following 63

- Followers 808

- Likes 2,272

375 Photos and videos

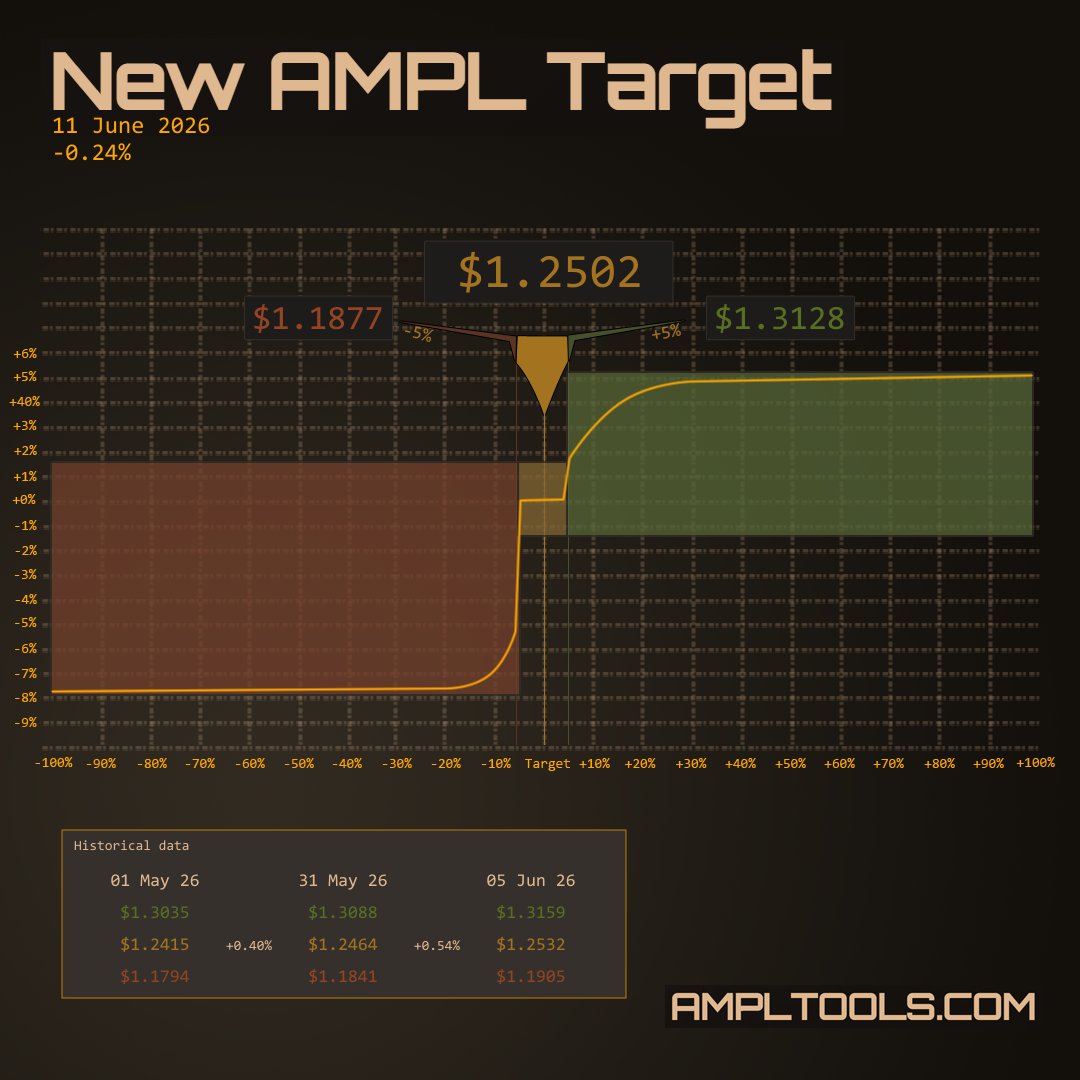

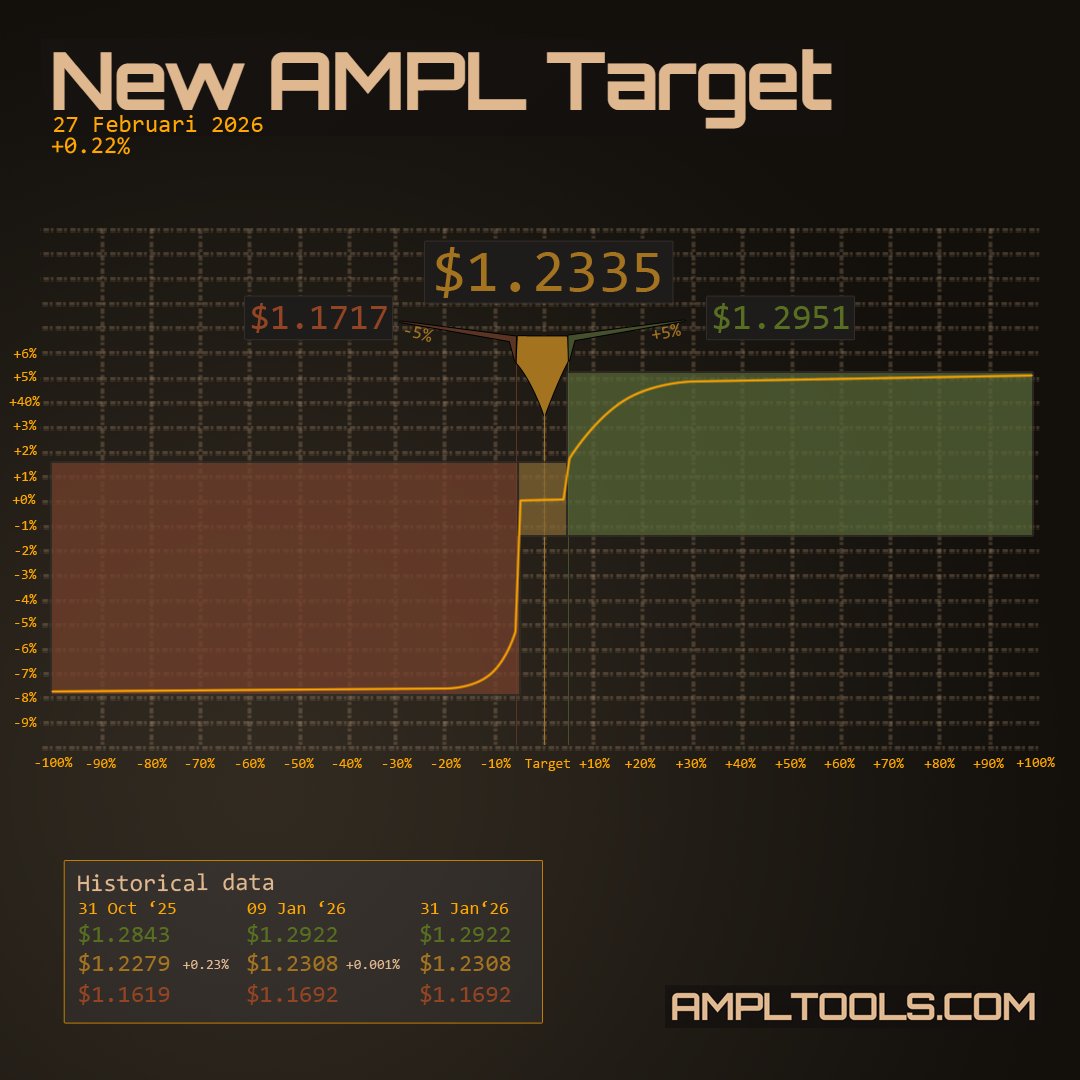

New $AMPL Target $1.2502

Negative rebase starts at: $1.1877

Positive rebase starts at: $1.3128

The target dropped -0.236%. This marks the 7th downward target correction since inception.

50

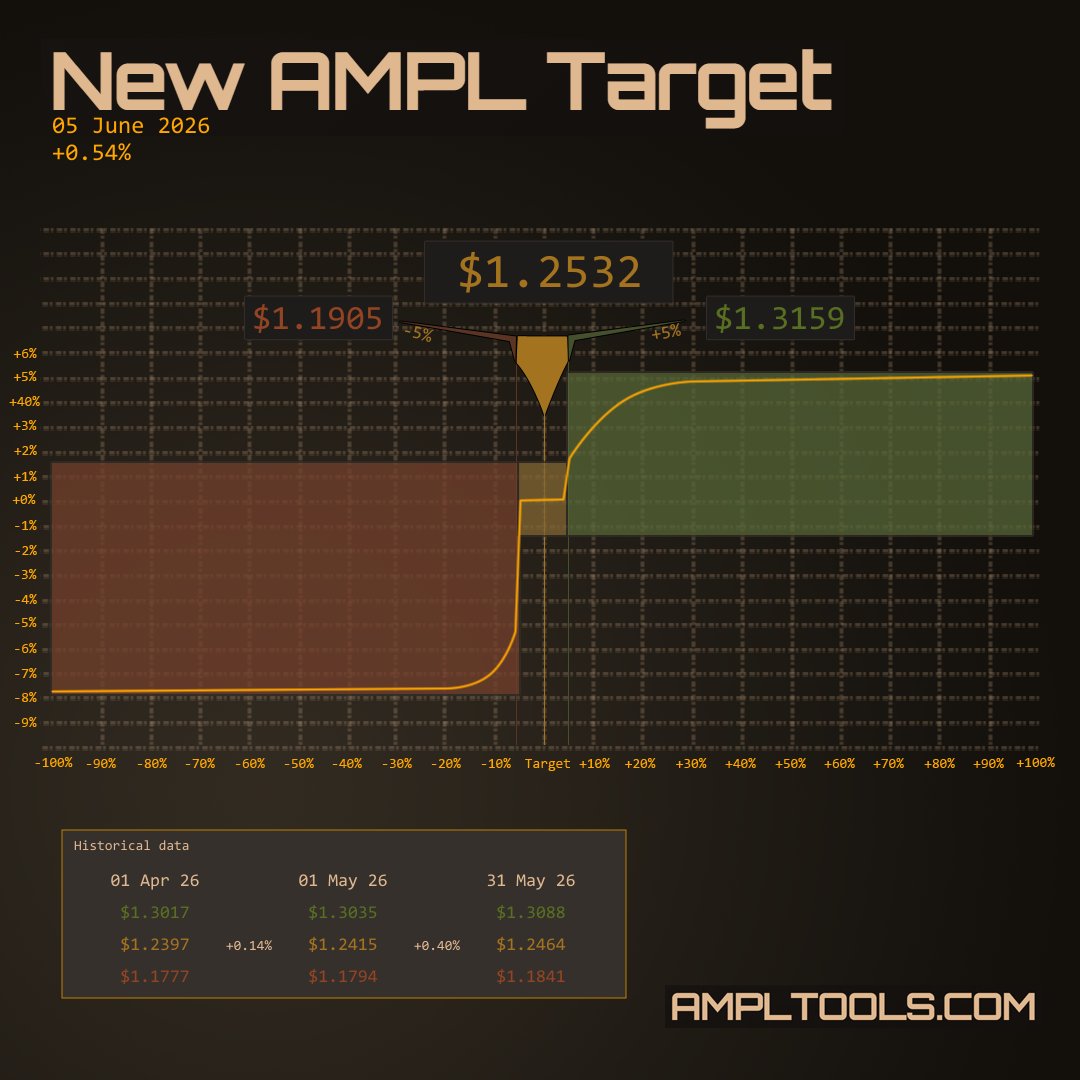

New $AMPL Target $1.2464

Negative rebase starts at: $1.1841

Positive rebase starts at: $1.3088

2

1

104

🚨🚨

UPDATE: CoW Swap experienced a DNS hijacking at 14:54 UTC (approximately 90 minutes ago).

The CoW Protocol backend and APIs were not impacted, but we have paused them temporarily as a precaution.

We are now actively working to resolve the situation. Please continue to refrain from using swap dot cow dot fi until we confirm that it is safe to use.

28

80

317

300,644

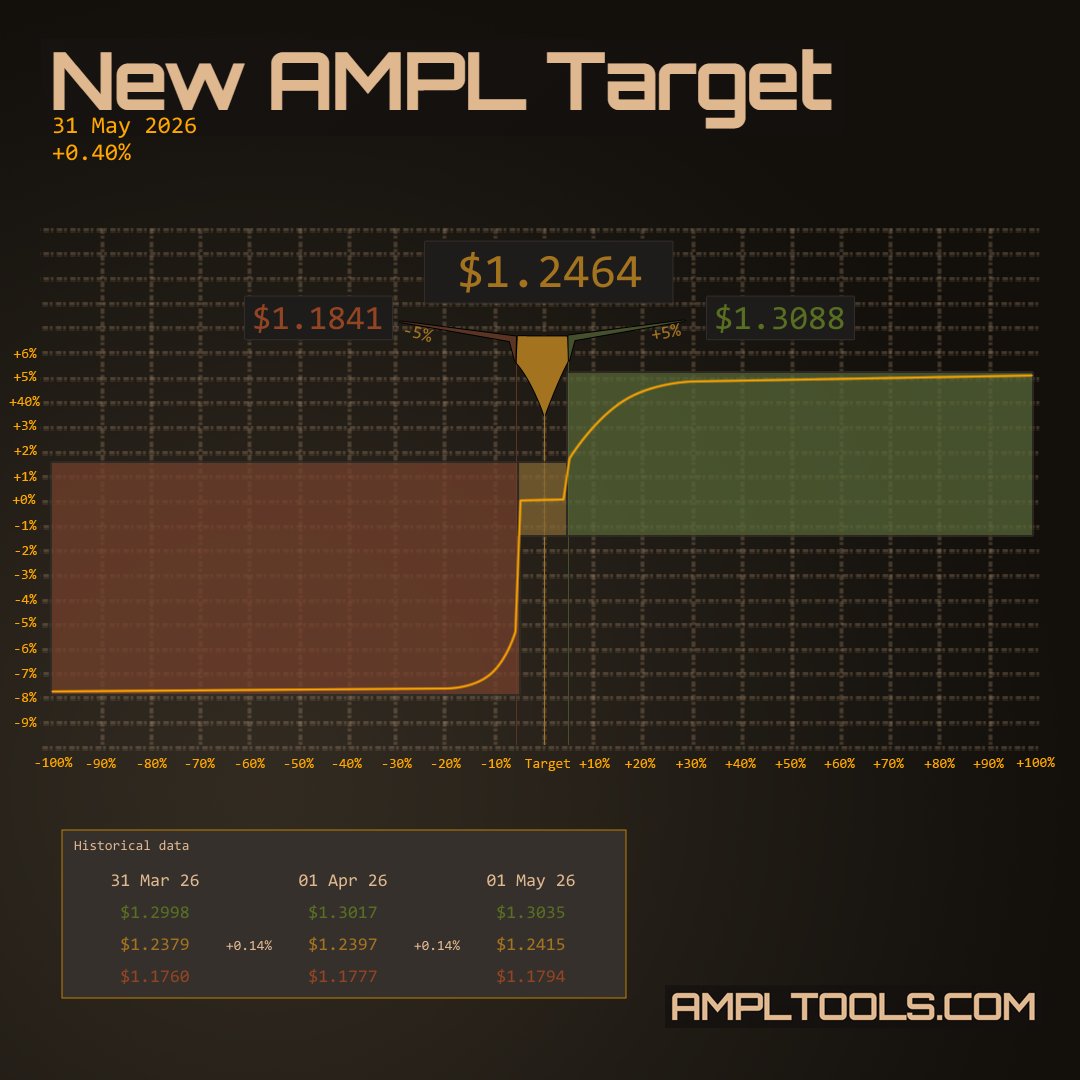

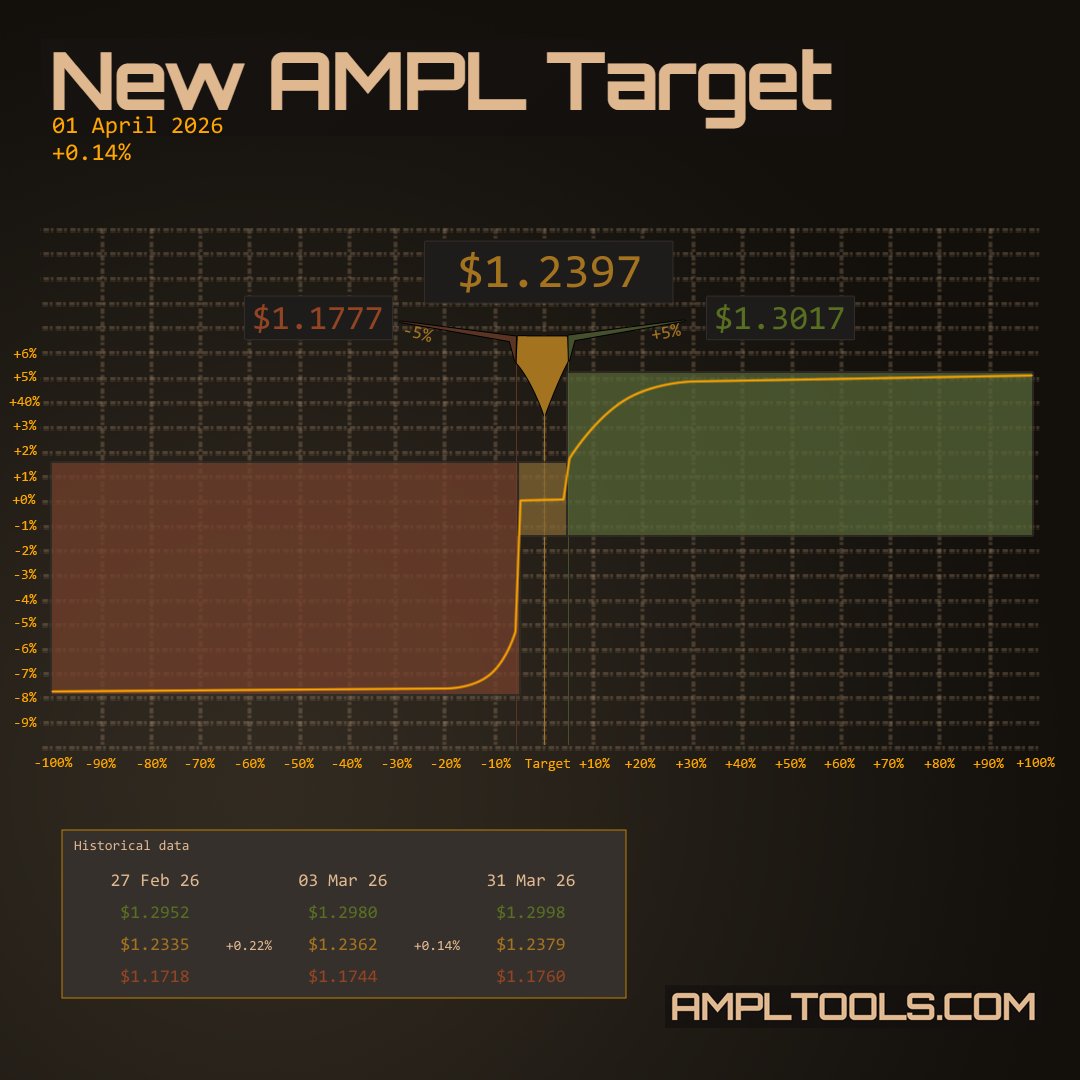

New $AMPL Target $1.2397

Negative rebase starts at: $1.1777

Positive rebase starts at: $1.3017

1

129

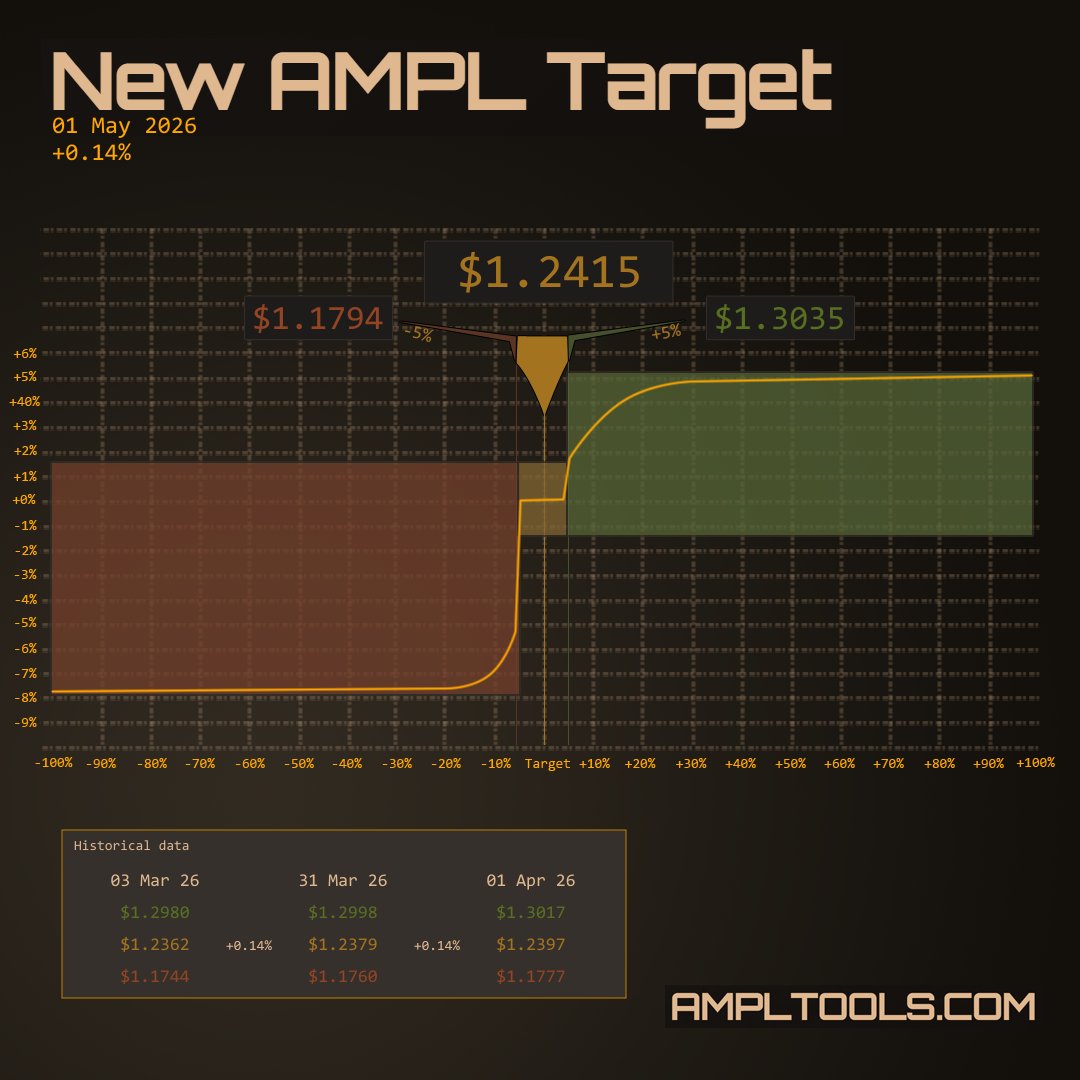

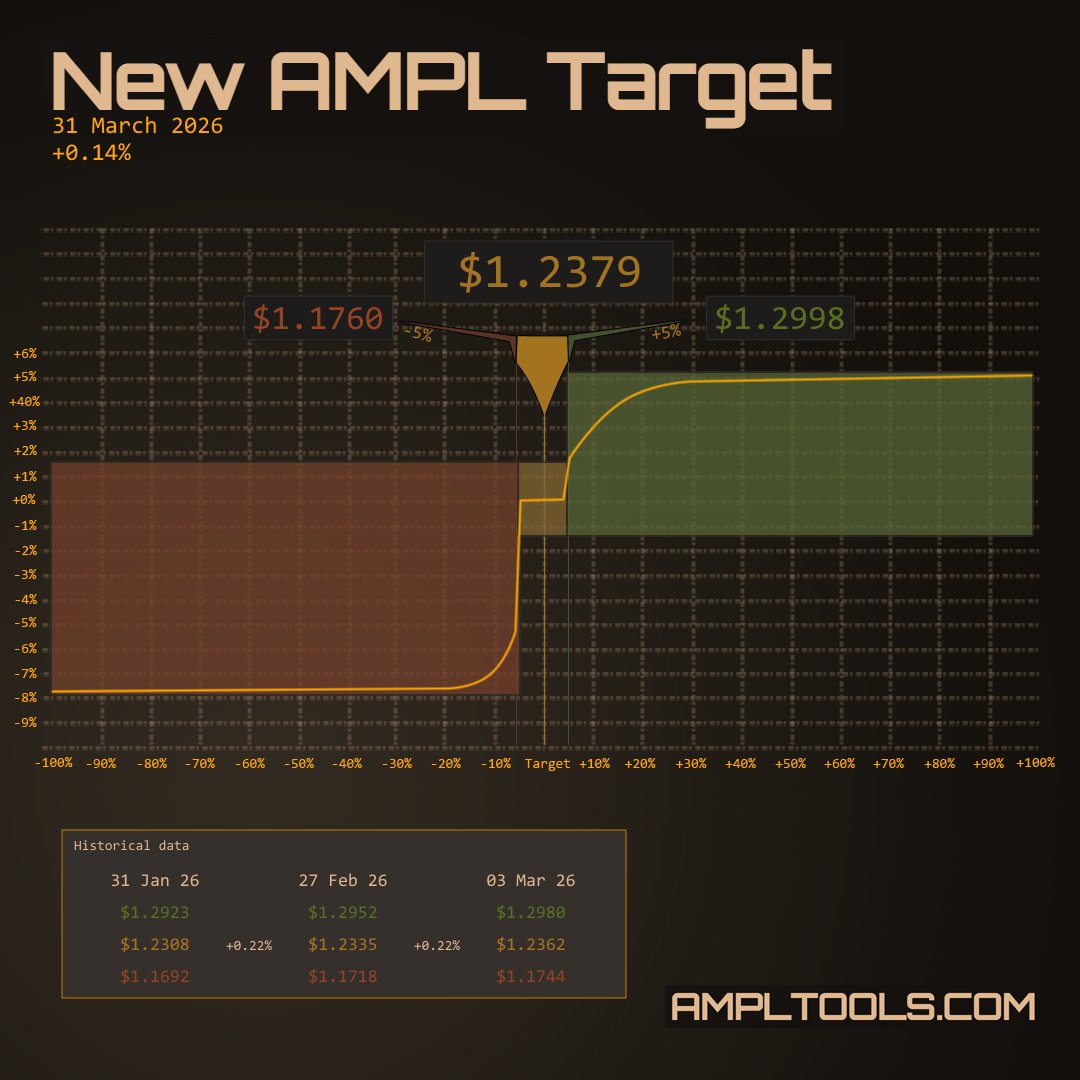

New $AMPL Target $1.2379

Negative rebase starts at: $1.1760

Positive rebase starts at: $1.2998

1

108

63

29

429

157,156

Ampltools.eth | Ampltools.com | Λ retweeted

Mar 4

11

4

34

5,259

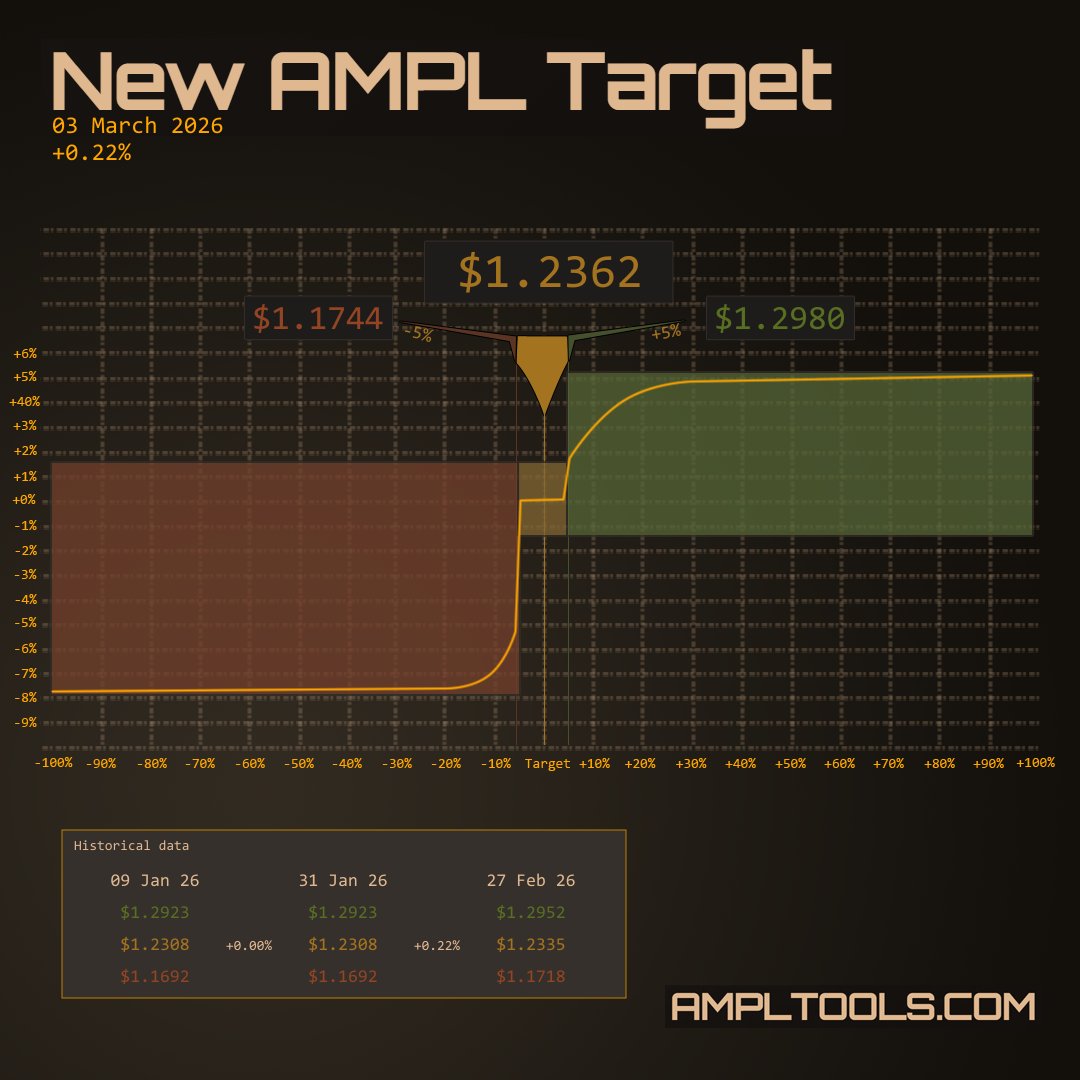

New $AMPL Target $1.2362

Negative rebase starts at: $1.1744

Positive rebase starts at: $1.2980

5

228

1

2

11

390

Ampltools.eth | Ampltools.com | Λ retweeted

Feb 18

Market extremes expose monetary design.

In euphoric phases, $AMPL tends to trade above its purchasing power target.

The protocol responds with positive rebases, expanding supply into demand. Instead of forcing price to absorb all upside pressure, AMPL distributes part of that pressure into balances.

Volatility still exists, but it is reorganized across supply rather than concentrated purely in price.

In panic phases, AMPL often trades below the target.

The response is negative rebases, contracting supply as demand collapses. While frequently misunderstood as “loss,” it is actually the system expressing monetary policy: when demand falls, units contract so the discount can compress over time.

There is no peg defense, no collateral liquidation, and no discretionary intervention. The response is mechanical.

Across extremes, AMPL does not attempt to suppress volatility. It routes volatility through supply adjustments.

Fixed-supply assets force all shocks into price. Pegged assets externalize shocks into collateral and liquidations. AMPL internalizes them through rebasing.

The tradeoff is psychological, not structural: balances change visibly. The benefit is policy consistency.

Overall, AMPL behaves less like an equity and more like a monetary system with supply as its control surface.

14

5

39

5,334

In January, the Ampleforth oracle system faced its first real stress test - a $0 target price caused by the longest US government shutdown in history. The protocol bent, but it didn't break. Here's what happened.

1

3

137

This was the first time in AMPL's history that the target price reached $0.00. It demonstrated both the vulnerability of oracle systems to external government events and the effectiveness of the protocol's safety mechanisms in preventing catastrophic rebases.

1

1

33

Full details are now documented on the AMPLtools dashboard, both the Target and Rebase analytics pages include a Knowledge Center entry explaining the event, with affected data rows flagged for transparency.

ampltools.com/SoTN/target

1

34