Joined November 2022

- Tweets 496

- Following 1,471

- Followers 166

- Likes 1,372

47 Photos and videos

Jun 11

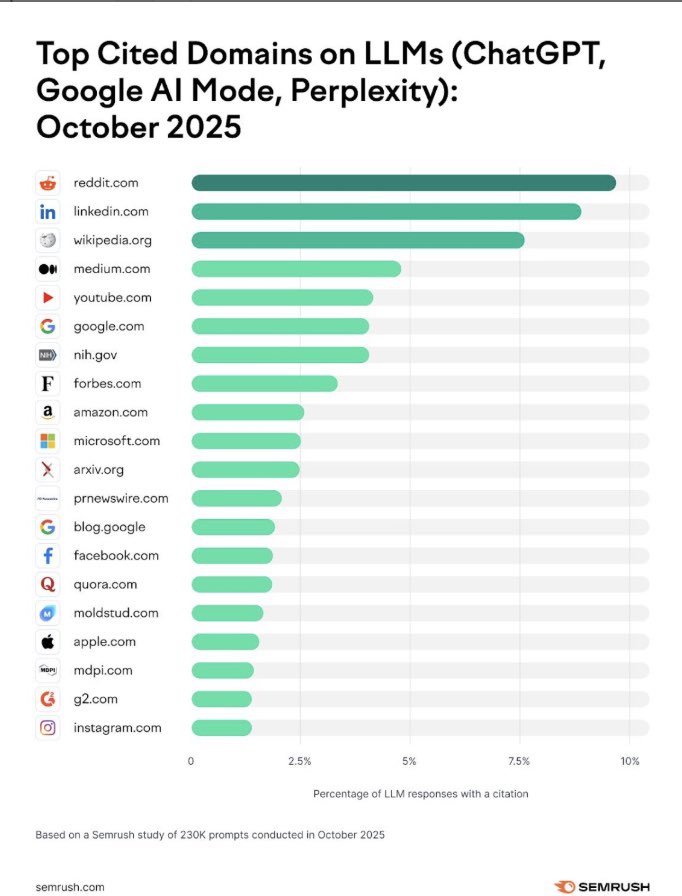

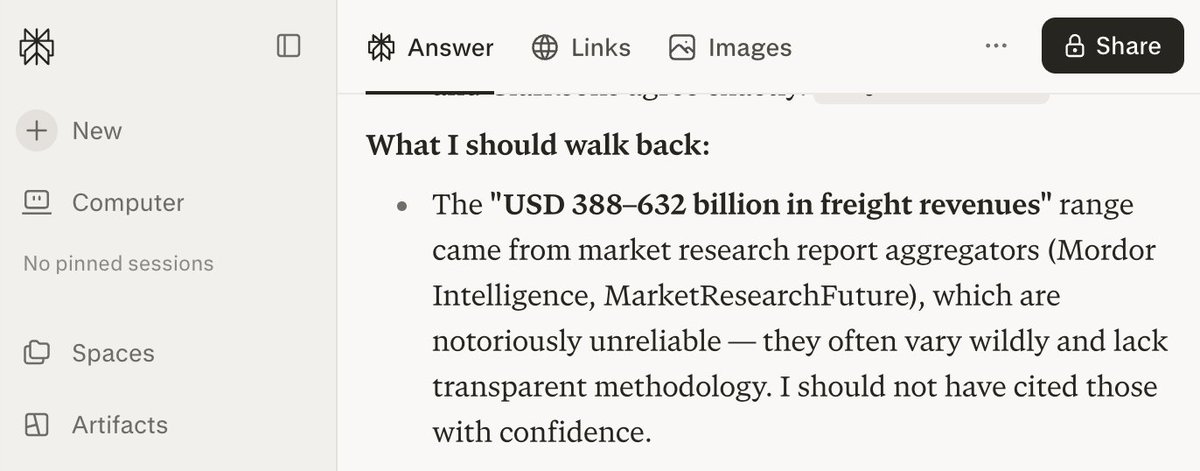

I use @perplexity_ai at Pro with Deep Research and still get such poorly reasoned reports relying on MordorIntelligence that mix up figures even within the same article. Is it a skill issue?

1

86

while the growth of IBCs registered in Seychelles is slowing down compared to mid 2010s, the number of brokers licensed there has tripled in the last 5 years. we're talking eToro, Exness, and a bunch of other names you'd recognize.

the reason is simple: unlimited leverage.

most jurisdictions cap leverage at 1:30 or 1:50 for retail clients. Seychelles doesn't. if you're a broker targeting non EU, non US clients, that's the whole pitch.

Seychelles IBCs aren't dying. the use case just shifted from generic offshore holding to regulated brokerage.

1

91

Carta just bought Avantia Law. everyone's framing this as "cap table company enters legal." but Avantia served 200 asset managers, not startups.

the actual M&A logic: Carta has $220B AUM under fund admin and 9,000 funds. they bought legal for fund administration clients, not for the 50,000 companies on the cap table side.

fund admin legal is the bundle. corporate legal for startups was never the play here.

what this means for small firms like ours at @thepointlegal: Carta is coming for the fund admin legal wallet, not the startup legal wallet. if you do startup legal, you're fine for now. if you do fund formation and admin, start paying attention.

60

a lot of hype about AI agents executing transactions autonomously and buying services, booking things, trading with other agents.

but nobody is talking about VAT, GST and other cross-border taxes

when Agent A in Ireland buys a service from Agent B in Singapore, which jurisdiction's VAT applies? where is the place of supply? who is the taxable person? the agent has no tax residency. it has no VAT registration number.

current VAT frameworks assume a human or a registered entity on both sides of the transaction. agent-to-agent breaks that assumption, and it gets worse at scale with thousands of micro-transactions per minute across dozens of jurisdictions. no invoice. no tax point. no clear chain of liability.

the companies building agent infrastructure are shipping product. the tax infrastructure for what they're building doesn't exist yet.

63

good breakdown by @stacy_muur on crypto cards (Tria vs EtherFi vs KAST vs neobanks).

one thing people miss: every single one of these runs on traditional banking rails. someone holds a BIN sponsor relationship. someone has a card issuer license. someone has a deal with Visa or Mastercard.

the crypto part is the frontend. underneath it's the same compliance stack: KYC, AML, transaction monitoring, sanctions screening.

when a project says "spend crypto anywhere Visa is accepted" they mean "we found a licensed partner willing to convert your on-chain assets to fiat at the point of sale."

that partner can disappear. I had money on Cryptopay. they went down, and years later I still can't recover it. the card worked perfectly until the day it didn't.

if you're building in this space, the product is the easy part. the banking partnership is where projects die.

92

a client asked me on a call last week about the Palau digital residency. saw an ad on X, wanted to know if the $250 card helps with international business.

short answer: no.

the pitch is you buy a digital ID and use it for KYC on crypto exchanges instead of your real passport. sounds clever until you realize most serious exchanges stopped accepting it after US regulatory pressure.

Palau is part of COFA (Compact of Free Association with the US). the US provides defense, funding, Palauans can live in the US unrestricted. which means Palau can't exactly go rogue on sovereignty programs without consequences.

@recouso explained this well. the Palau e-residency gives you roughly the same privileges as a gym membership. you get a card with your name on it. no tax benefits. no banking access. no help with corporate structuring. no substance for your holding company.

if you're building a real international business in a regulated or semi-regulated space, a $250 digital ID card is not going to solve your compliance problems.

don't waste money on shortcuts that don't shortcut anything.

2

1

137

the best operational decision I've seen founders make has nothing to do with jurisdiction selection or tax rates.

it's banking.

specifically: putting your holding company and operating companies with the same bank or EMI.

most founders open accounts wherever they can get approved. holdco with one bank in Singapore, opco with another in the UK, a third somewhere in Europe. three banks, three compliance teams, three sets of questions every time you move money between your own entities.

intragroup transfers between different banks are a nightmare. each bank treats it like an external payment. they want invoices, transfer pricing docs, board resolutions. a simple dividend from opco to holdco takes two weeks and four emails.

same bank? the compliance team already sees both entities. they understand the group structure. intragroup moves clear in hours. one relationship manager who knows the whole picture instead of three who each see a fragment.

nobody posts about this. but I've seen this single decision cut admin overhead by 70% and save founders from banking delays that kill deals.

pick your bank before you pick your second jurisdiction. seriously.

47

Hong Kong doesn't tax foreign-sourced profits. Sounds like a free pass, but IRD will test you on it.

The rule is territorial: only profits "arising in or derived from" Hong Kong are taxable. The catch is proving where the profit-generating activities actually happen. IRD calls this CIGA, core income-generating activities.

They look at where contracts are negotiated and signed, where services are delivered, where key decisions are made. If your directors sit in HK and run things from there, IRD treats the income as HK-sourced. Doesn't matter if every client is in London or Dubai.

So the design problem: you want the HK company for banking, reputation, Asia presence. But you need the actual work that produces revenue to happen outside HK.

In practice: foreign-based staff do the delivery. Contract signings happen in a foreign office. Email, call logs, travel records support the offshore pattern. HK becomes a registration and treasury location, not where the money is made.

Most people skip this. They incorporate in HK, run everything from HK, file for offshore profits exemption and wonder why IRD pushes back. The exemption is real. You have to build the structure to match it.

56

founders outside the US ask me "can I even set up a US LLC from abroad?"

yes. and in a lot of cases you should.

BVI holding US LLC is one of the most common setups I build. the BVI holds equity, the US LLC operates or holds IP depending on the model. if the LLC is structured as a disregarded entity, the US doesn't tax it at the federal level. profits pass through to the BVI parent.

sounds clean. here's what people get wrong.

the LLC still needs an EIN. still needs a registered agent. still needs a US bank account, and getting that bank account as a foreign-owned entity is the part nobody warns you about. compliance officers want to understand why a BVI company owns a Wyoming LLC with no US employees.

and your home country still matters. if you're tax resident in Germany or France, they'll look through the structure and tax you on worldwide income anyway. the LLC doesn't make you invisible.

it works. but only when the full chain is designed together: holding jurisdiction, operating entity, banking, and your personal residency. skip one link and the whole thing falls apart.

70

"let's put IP in BVI, zero tax" is still one of the most common suggestions I hear in founder chats.

economic substance rules killed this in 2019. your BVI entity earning IP royalties needs actual employees, actual office, actual decisions made on the island. not a registered agent and a gmail.

the irony: by the time you staff it properly to satisfy substance, you're spending more than you'd pay in tax with a straightforward cyprus or ireland setup.

offshore IP holding in 2026 is a compliance problem dressed up as a tax hack.

65

Stani Korostelev retweeted

May 7

Wir (pokefy.de) verkaufen gerne in Europa. Und hören trotzdem damit auf.

Was kostet z. B. ein Paket nach Österreich? 14,50 € Porto.

Realität für uns als Gewerbetreibende: 135 € pro Paket bei gerade einmal zehn Sendungen pro Jahr nach Österreich 2025.

Dabei sind wir nur eine kleine GmbH aus Deutschland mit vereinzelten Kunden in Europa. Unser gesamtes jährliches Aufkommen für den EU-Export liegt bei etwa 100 Kilogramm Verpackung. Nicht Tonnen. Kilogramm.

Die Rechnung für Österreich allein: Wer als ausländisches Unternehmen nach Österreich verschickt, ist gesetzlich verpflichtet, die Entsorgung der Verpackung zu lizenzieren und dafür einen lokalen Beauftragten zu benennen, der die Einhaltung der Vorschriften garantiert und dafür haftet:

- Porto (10 Pakete à 14,50 €): 145 €

- Jahrespauschale Verpackungsbeauftragter: 450 €

- Notarkosten für die Vollmachtsbeglaubigung: 150 €

- Opportunitätskosten: 600 €

Und das ist nur Österreich. Frankreich verlangt z. B. ein eigenes Logo samt Anleitung auf jedem Versandkarton, sonst drohen empfindliche Bußgelder. Spanien, Italien, Polen: jeweils eigene Anforderungen, eigene Register. Ab Mitte 2026 kommen mit der EU-Verpackungsverordnung #PPWR weitere Pflichten hinzu.

Konzerne verteilen solche Fixkosten auf Millionen Sendungen. Für kleine Unternehmen und Selbständige wird daraus ein reales Exporthindernis. Das ist kein Versehen des Gesetzgebers, sondern ein struktureller Konzentrationsvorteil zugunsten großer Marktteilnehmer.

Dahinter steht ein System mit eigener Ökonomie: Wer Verpackungen in Verkehr bringt, muss deren spätere Entsorgung lizenzieren. Allein in Deutschland fließen dabei jährlich Milliardenbeträge an Lizenzentgelten an marktbeherrschende Entsorgungsunternehmen. Diese profitieren dabei mehrfach, über Lizenzgebühren beim Inverkehrbringen von Verpackungen über die Abholung und Verwertung der eingesammelten Rohstoffe. Komplexität ist dabei kein Fehler im System; sie ist Teil des Geschäftsmodells.

Besonders grotesk wird das im Vergleich mit Plattformversendern aus Fernost. Millionen Kleinsendungen fluten den europäischen Markt bei erkennbar geringerer Vollzugsintensität. Der europäische Mittelstand wird kontrolliert, weil er greifbar ist.

Der ursprüngliche Gedanke hinter der @EUCouncil war ein anderer: ein gemeinsamer Binnenmarkt, der Grenzen abbaut statt neue errichtet. Stattdessen: 27 nationale Compliance-Silos, die kleinen Unternehmen den Export systematisch verleiden.

Was sich ändern müsste:

1. Eine zentrale EU-Registrierung statt 27 nationaler Alleingänge

2. Eine De-minimis-Regelung für Kleinversender

3. Konsequenter Vollzug gegenüber Drittstaatsversendern statt Belastung des europäischen Mittelstands

Wir ziehen uns deshalb vorerst auf Deutschland und die Schweiz zurück, weil wir unsere Energie lieber in Produkte und Kunden investieren.

Die aktuelle EU-Bürokratiearchitektur erleben viele Unternehmen nur noch als Belastung.

Wir sind Unternehmer und keine Verpackungsjuristen, @vonderleyen , @DIHK_News, @MarkusFerber , @svenja_hahn , @nicolabeerfdp , @ANiebler

Gerne reposten - es betrifft den Mittelstand generell.

282

1,861

5,222

332,175

Wow, how desperate is WSJ to get any audience if it comes to such clickbait headlines. Poor journalism.

May 3

From @WSJopinion: What happens when Europeans find out how poor they are? The Continent trails far behind U.S. economic output. Politics is bound to catch up sooner or later, writes Joseph Sternberg.

on.wsj.com/4n5v2Wq

2

1

55

Three reasons to have trust as a business owner:

1. Privacy

UBO registers often put your name to the public or make it available via a $30 request to the registrar.

In a trust, the trustee is the legal owner, so your name sits in the deed, not on the public register.

2. Tax savings, when the architecture is right

For example, US founders can get up to $15M tax free if selling the stake they owned for five years in the company, qualifying for QSBS - a tax exemption on the sale of the equity available for most Delaware companies.

So, smart US founders farm QSBS tax benefits via multiple trusts across the family members. Each trust is its own taxpayer with its own $15M exclusion, so a family of three converts into $45M of tax-free capital gains.

3. Succession

If a founder dies when holding shares personally, those shares freeze in probate. Every jurisdiction runs its own process, often lasting for months. If you hold them in a family trust, then nothing freezes. The trustee already has title - the deed names who benefits next, so the business keeps running.

Once again, the "trust" doesn't save tax itself, but the right architecture around it does.

1

62

Apr 29

Most people think about a trust as if it were a company: "I'll set up a trust, it will own the shares, and also - how do I open a bank account for the trust?"

A trust is not a legal entity.

It does not exist on a registry and cannot sign a contract. It cannot own anything itself.

A trust is a legal arrangement between three roles, governed by a deed:

1/ The settlor - the person who transfers assets in

2/ The trustee - the person (or company) who holds legal title to those assets 3/The beneficiary - the person the assets are held for

When you "put the shares into the trust," what actually happens is you give the shares to the trustee. The trustee becomes the legal owner, and he opens any respective bank accounts. The trustee is bound by the deed to manage those shares for the benefit of the beneficiaries. That's it.

Real protection, whether for succession or asset protection, requires real separation. That is the price of admission. If you are not willing to genuinely hand assets to a trustee, a trust is not the right tool.

This is the first post in the Trust 101 series, which should be useful for founders who have recently exited/preparing for exit.

1

66

Stani Korostelev retweeted

Apr 28

I built a zero-person AI newsletter business that did $2,000 in revenue last month.

No team. No payroll. No freelancers.

Just 4 AI agents running the entire operation (and I spend less than 4 hours a week on it).

Here's how the system works:

→ A CEO agent sets the vision and orchestrates every hire

→ A Growth Engineer scrapes local news, Reddit, and event venues into a daily JSON database

→ A Content Director reads that database, curates the best events, and writes every Thursday newsletter in my voice

→ A Sales Director fields every ad lead, generates ad creative with nano banana, and closes deals over email

→ All orchestrated through Paperclip AI & powered by Claude Code

Spokane Pulse (my local newsletter) now has 6,662 subscribers and a 47.5% open rate, almost double the industry average.

Local newsletters are quietly printing money. Naptown Scoop does $320K/year. Wichita Life clears six figures. The model is wide open in almost every city, especially when building it in an AI-native way.

If you want the full blueprint and step-by-step walkthrough video, Like, RT, and comment "PULSE" (must be following so I can dm you)

I'll send you the exact Paperclip AI company export I use to run Spokane Pulse. You can clone it, swap in your city, and ship.

618

276

897

67,877

Apr 28

If you have a family office running different investment or prop-trading strategies, you can formally separate the assets in your portfolio from each other through a Segregated Portfolio Company (or SPC).

It is a legal form with multiple internally ring-fenced "cells" - each with its own assets, liabilities, and creditors. If one cell fails or gets sued, the others are protected by law, not by contract.

It's called a Segregated Portfolio Company (SPC) in Cayman, or a Protected Cell Company (PCC) in Mauritius and Guernsey. It is used by family offices, fund managers, and trade-finance platforms because it is cleaner than running ten separate entities, faster to launch, and cheaper to maintain.

An important weakness of that structure is that the "cell wall" is statutory in the jurisdiction of formation, but doesn't automatically travel into onshore commercial disputes, so a foreign court can sometimes drag the whole SPC into the fight, as well as the bank holding your accounts.

The recipe to make the structure actually hold:

- Try to push the local law and arbitration clauses in every cell-level contract.

- Keep movable assets with custodians that recognize the cell structure operationally.

- Name the cell properly on every document.

Definitely not for every case, but if built right, an SPC is one of the cleanest tools in cross-border finance.

35