Investing. Any opinions my own.

Joined January 2022

- Tweets 1,946

- Following 950

- Followers 5,276

- Likes 33,568

426 Photos and videos

Pinned Tweet

20 Mar 2023

$SYF Quick pitch: bank that trades at 1.25x tangible book, has de minimis deposit flight risk, & targets (earns) a 28% return on tangible equity. While perennially discounted in relation to business quality, SYF is now exceptionally cheap (less than 5x earnings).

19

13

132

86,440

Jun 9

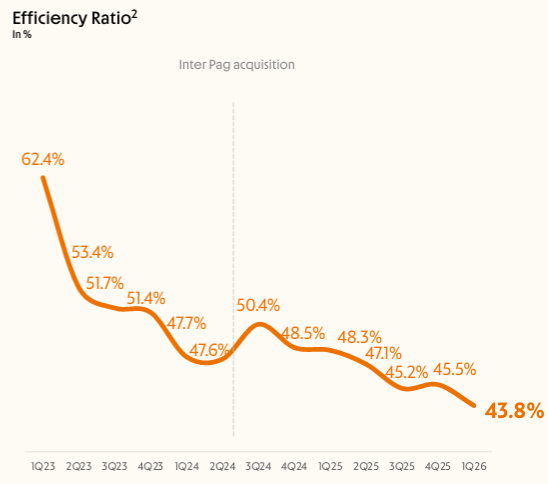

$VBNK expects to exit '26 w/US eff. ratio <20% vs 37% in Q. Also claims 6B credit assets in bag(tipping point for scale)-ignoring RBTDs, grows to 10B in <3yrs at current rate. 3x '29 EPS if biz scales the way mgmt claims w/60% annual EPS growth thru '30. Ambitious, but maybe?

1

2

12

2,276

Jun 9

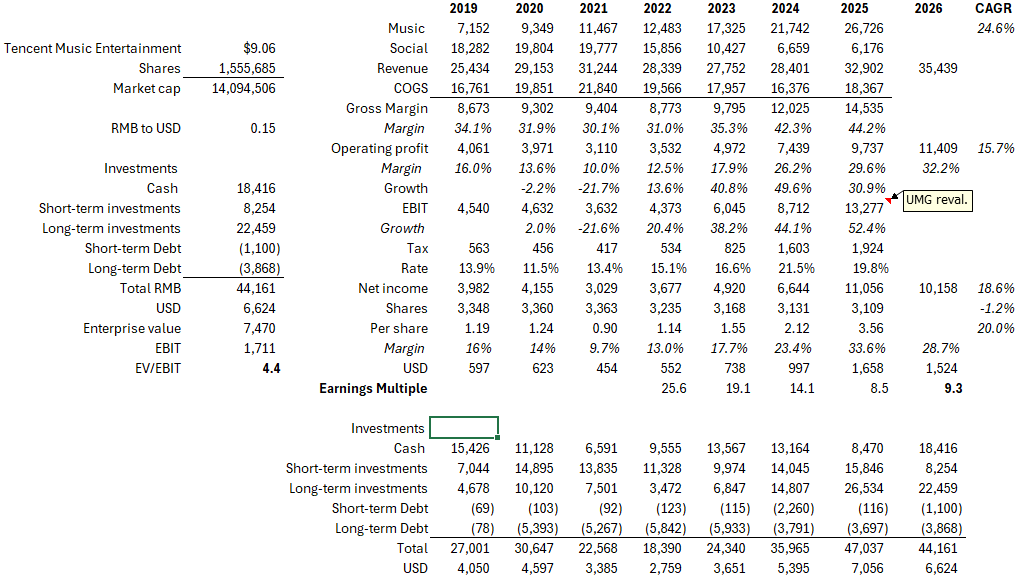

$TME core music-sub biz actually growing faster than SPOT's (25% CAGR vs 17%) & now 80% of the pie. What's the appropriate China discount? 9x EPS vs 40, 4x EV/EBIT vs 33, but TME probably further along monetization curve.

12

1,661

May 22

Alcohol is the new tobacco continues--Cuervo now off 70% over the last five years. What's wild is that it isn't even levered—lost 70% of its enterprise value since 2021.

11

11

118

18,408

May 21

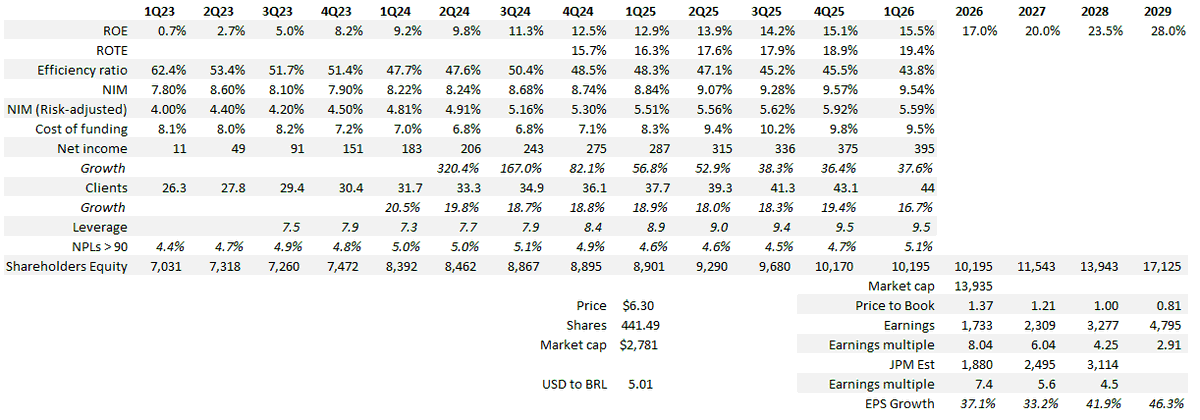

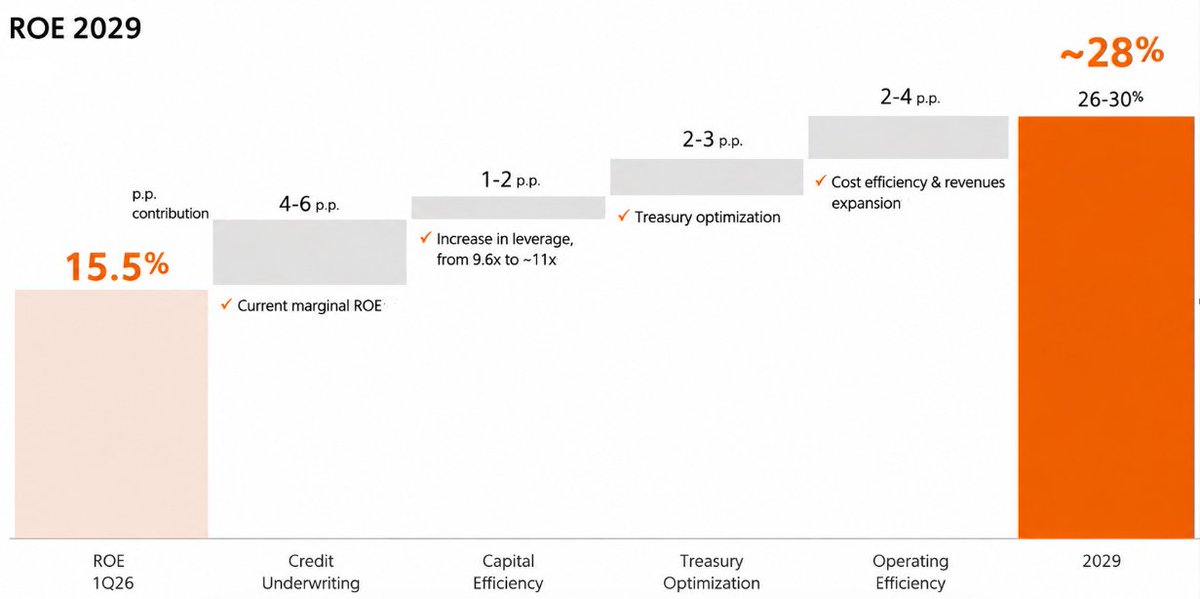

$INTR is a long @$6.40. Materially oversold over past month. Hyper-growth digital banking powerhouse in Brazil trading at 7x EPS. Currently running a 15.5% ROE but guiding a 28% ROE at mid-point by 2029. If mgmt hits target, co is sub-3x 2029 EPS. ROE target highly achievable 1/n

10

7

94

10,427

May 21

Nu is more mature in its core market w/penetration at 60% of adult population, so heavy lifting is coming from newer & less proven foreign markets. Nu is also operating closer to peak efficiency, so additional operating leverage will only provide a modest tailwind to earnings.

1

2

7

1,427

May 21

$INTR has good visibility into another 300 bps of ROE expansion thru year-end. At this point, it will trade at 5.5x EPS & 4x FWD. It should also still be growing EPS at 35-40% per year. Combine this w/multiple expansion & co offers a 3-4 bag opportunity over the next few yrs.

2

12

1,634

May 21

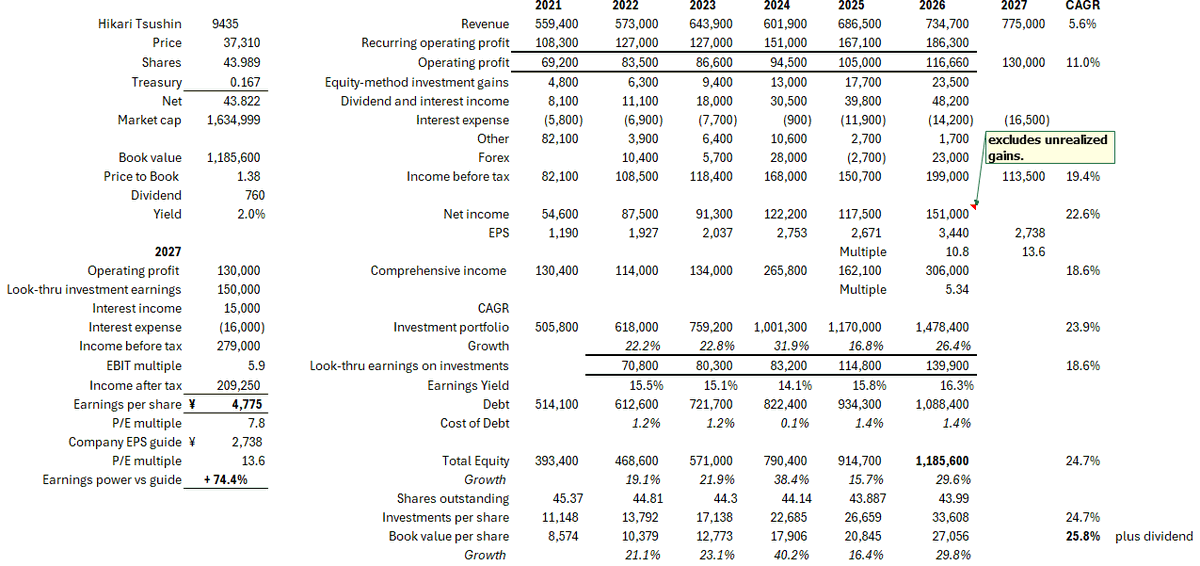

$9435 Hikari still a great way to play value in Japan. Just ran a 30% ROE & you can buy for 1.3x materially understated book. 27' ¥2,738 EPS guide is nonsensical. Co is operating biz investments. Better framework: value like BRK:¥4,800 EPS, or 7.5x vs 13.6x based on guide. 1/n

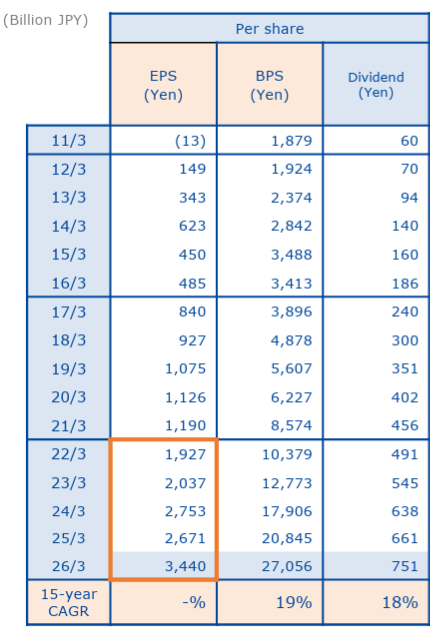

2

5

65

9,675

May 21

Then to the extent that the CEO has investing skill, the investment portfolio return potentially runs higher than its look-thru earnings. Book value has continually benefitted from this: 15-year CAGR is 19% excluding dividends, 5-year CAGR is 28% when dividends are included.

1

2

1

984

May 21

A look-thru investment earnings figure of ¥150B for 2027 seems reasonable. Interest income mostly offsets interest expense. Effective tax rate is generally ~25% range. So, pay sub-8x EPS for a Japanese compounder run by an operator that actually understands capital allocation.

2

2

4

934